JimSchemel

Santa looks to be arriving early, as stocks soared yesterday on a combination of better-than-expected consumer confidence and lower inflation expectations. That trumped a weak housing report that showed existing sales were down 7.7% last month and 35% over the past year, but that comes as no surprise given the doubling in mortgage rates. The bears on Wall Street got to revel in a five-day decline for the major market averages, emboldening their grim outlook for the economy and markets, but consumers on Main Street don’t appear to be listening. That is breathing life back into the bullish narrative just in time for a Santa Claus rally.

Finviz

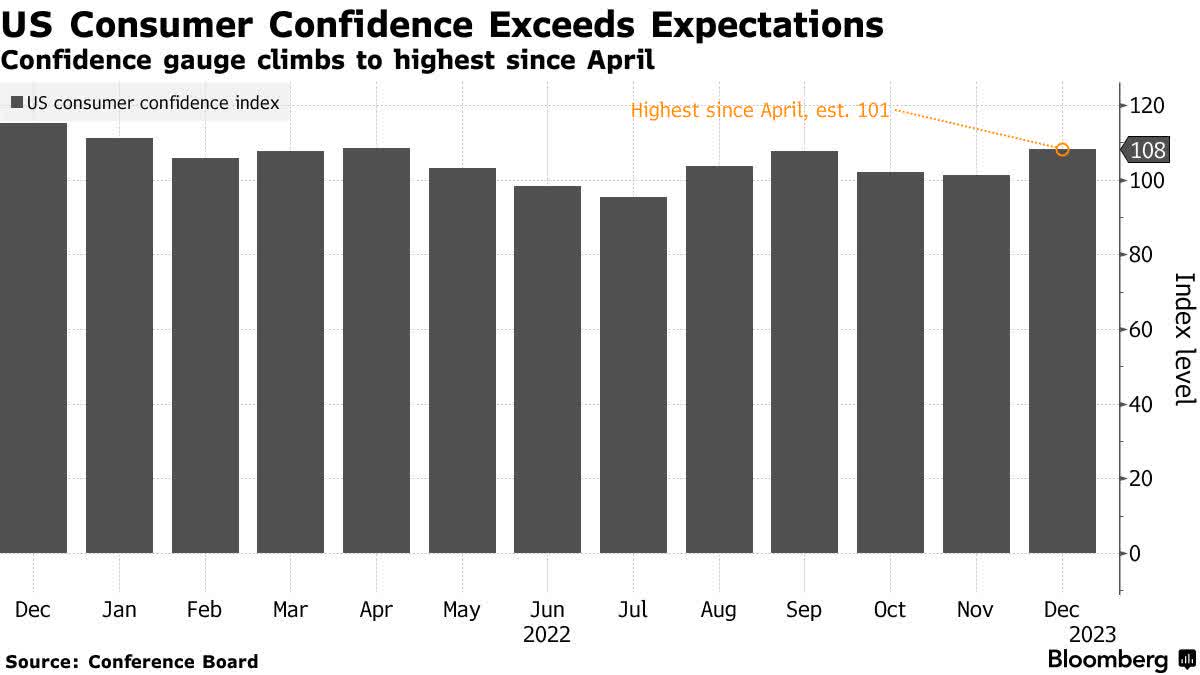

The Conference Board’s index of consumer confidence soared well above expectations to an eight-month high, while the six-month outlook rose to its highest level since January. Better yet, inflation expectations fell to the lowest level in more than a year, which is welcomed news for the Fed. This is not what you see when the economy is on the cusp of a recession.

Bloomberg

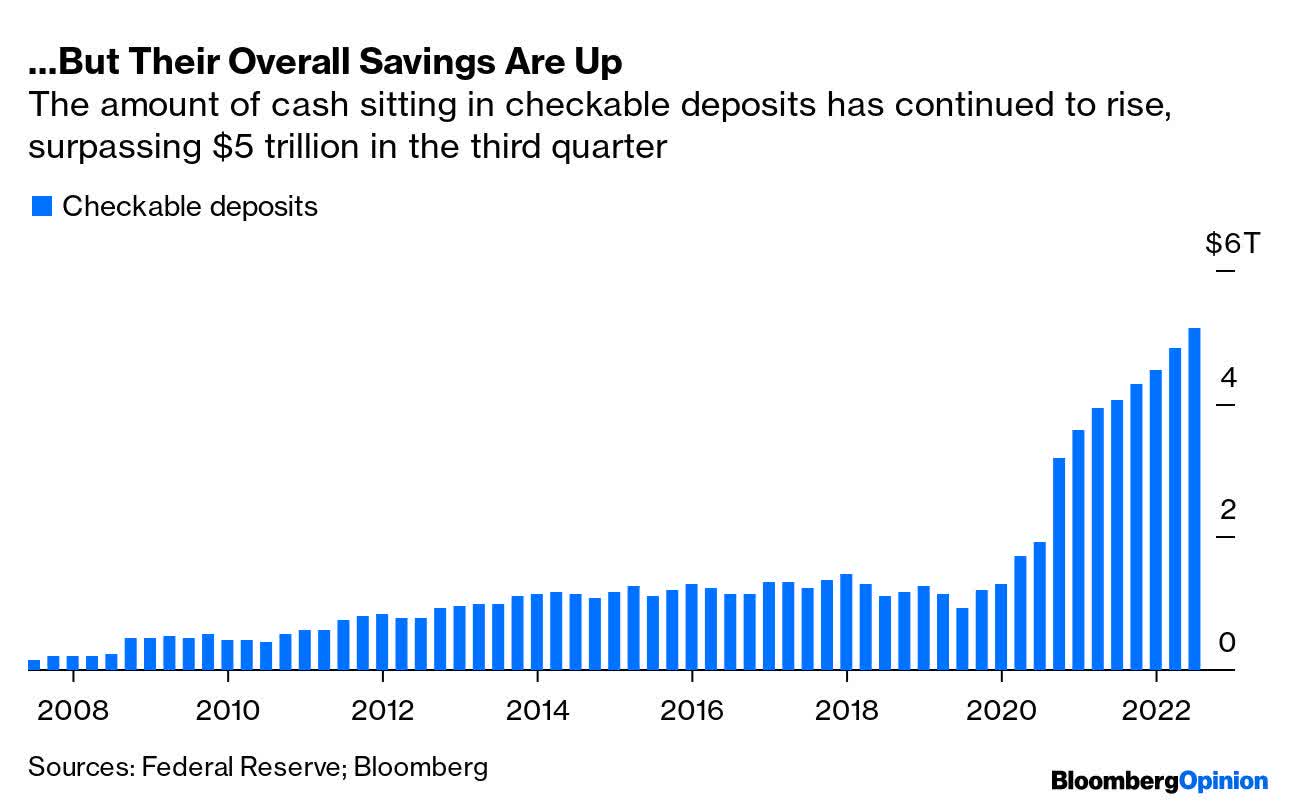

A lot has been made recently about the collapse in the personal savings rate to a near record low level of 2.3%, which suggests that inflation has devoured disposable income, forcing consumers to borrow at record levels to purchase basic necessities. I am sure that many American households are facing that plight, but markets respond to the majority, which is what dictates trends in the macroeconomic data. The majority of consumers are doing much better than the record low savings rate suggests.

That is because checking deposits continued to soar over the past year to what is now $5.12 trillion, according to the Fed’s quarterly Flow of Funds report, despite the decline in the savings rate. This is up from $4.28 trillion at the beginning of the year and $1.2 trillion before the pandemic. This is also why bank CEOs, like Brian Moynihan at Bank of America, continue to assert that consumer balance sheets remain strong. Why the discrepancy between cash levels and the savings rate? Some suggest that the method of estimating savings, which follows a similar methodology as estimating GDP, is skewed by the unusual nature of this business cycle. Another possible answer is that investors sold stocks and bonds to bolster savings in what has been the worst performing year for both asset classes combined in decades.

Bloomberg

Regardless, the cash is there. In my view, it has served as a buffer to the extraordinary price increases we have seen over the past 18 months, allowing consumer spending to continue growing on a real basis. It is not causing inflation as much as it is helping consumers overcome it. It could also become a source of fuel for the next bull market when financial market prices begin to recover and investor sentiment turns back up. It remains one of the most important reasons why we should be able to avert a recession next year, as the rate of economic growth slows and the rate of inflation falls closer to the Fed’s target of 2%.

Lots of services offer investment ideas, but few offer a comprehensive top-down investment strategy that helps you tactically shift your asset allocation between offense and defense. That is how The Portfolio Architect compliments other services that focus on the bottom-ups security analysis of REITs, CEFs, ETFs, dividend-paying stocks and other securities.

Be the first to comment