Klaus Vedfelt

Main Street Capital (NYSE:MAIN) is a high0quality business development company that has delivered strong and consistent results related to its lower middle market loan portfolio in the last couple of years.

Even though the BDC comfortably covers its dividend with net investment income, the stock has gotten a little bit ahead of itself lately, in my view, and is now selling at a very high premium to net asset value.

As a consequence, I think passive income investors should tread lightly here and wait for a correction before buying Main Street Capital.

My Rating History

I called Main Street Capital A Great Income Stock For 2024 as the BDC presented robust loan portfolio results in 2023. The Q4 earnings release proved what we already knew, which is that the BDC continued to deliver excellent distributable income results.

With that being said though, I think that the stock is now too expensive for passive income investors to consider and I correspondingly modify my stock classification to Hold.

Record Results From A Top-Notch Business Development Company

Main Street Capital achieved multiple records in the fourth quarter of 2023 including all-time high net asset value and record distributable net investment income amid strong originations after the pandemic. The central bank further aided the company’s net investment income by providing tailwinds for the company’s floating-rate portfolio.

Furthermore, the U.S. economy grew even more quickly than projected in the fourth quarter as the most recent GDP growth estimate was revised upward to 3.4%, up from an earlier 3.2%.

ADP payroll data also showed that the U.S. economy is adding jobs at a good clip and with inflation receding, there is a strong case to be made for pro-cyclical BDCs like Main Street Capital to continue to see robust net investment income.

Main Street Capital’s portfolio as of December 31, 2023, included (lower) middle market and private loans which combined had a value of $4.1 billion and primarily included Senior Secured First Liens.

Balance Sheet Summary (MAIN Street Capital)

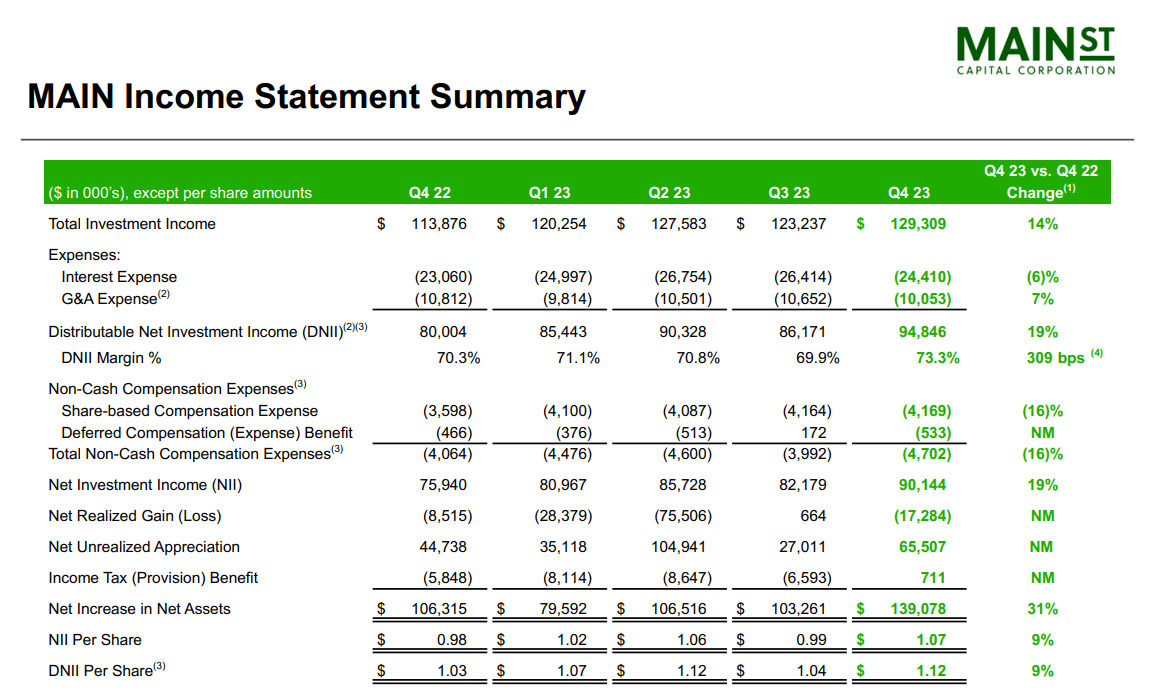

In the fourth quarter, Main Street Capital earned $94.8 million in distributable net investment income, reflecting 19% YoY growth. The BDC’s net investment income hit $90.1 million, also up 19% YoY, and a new record for Main Street Capital.

Because of this strong net investment income growth, the BDC, in addition to a monthly dividend of $0.24 per share, declared a special dividend of $0.30 per share. Main Street Capital regularly pays supplemental dividends in order to distribute excess portfolio income.

Main Street Capital is growing its portfolio and net asset value and it has the pay-out metrics to prove that the BDC provides passive income investors with a low-risk dividend. The BDC earned $4.36 per share in distributable net investment income in 2023, which is the basis for the pay-out ratio.

With a total dividend of $3.70 per share last year, the pay-out ratio for 2023 comes out to 85% (the pay-out ratio was also 85% in 2022). The dividend, including both the regular and the supplemental, is well-covered by distributable net investment income.

Income Statement Summary (MAIN Street Capital)

Main Street Capital’s Valuation Now Too High

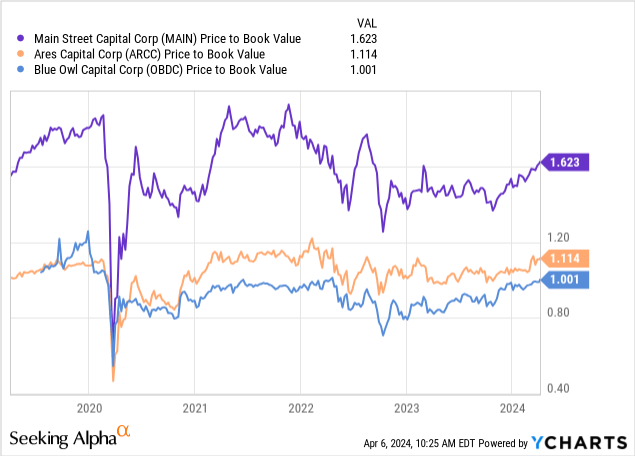

It is perfectly understandable that passive income investors reward those BDCs that deliver predictable and high-quality business results with a higher net asset value premium than more average BDCs.

Main Street Capital generated its sixth consecutive quarter of net asset value growth in Q4’23 as its NAV reached its highest level ever at $29.20, reflecting 3.1% QoQ growth. With that being said, though, I think that Main Street Capital’s net asset value premium, which presently sits at 61% is quite rich, despite the clearly well-performing loan portfolio.

Other BDCs like Ares Capital (ARCC) or Blue Owl Capital Corp. (OBDC) are selling at much more reasonable net asset value premiums and they have also enjoyed considerable net investment income tailwinds in the last year, thanks to the central bank.

Ares Capital Corp. had a pay-out ratio of 84% in 2023 whereas Blue Owl Capital paid out only 69% of its net investment income. Both BDCs also provide passive income investors with yields between 9-10%.

Why Main Street Capital’s NAV Premium Might Continue To Expand

The stock market is trading at all-time highs and the economic backdrop is generally favorable to BDCs. The central bank has said that it is considering three rate cuts in 2024 which could make credit more affordable and spur investment activity on the part of Main Street Capital’s portfolio companies.

In this case, Main Street Capital might profit from increasing demand for new loans and boost its net investment income as a consequence.

My Conclusion

Main Street Capital is one of the best BDCs in the market that has consistently delivered strong portfolio results and predictable dividend growth.

Furthermore, the BDC is paying its dividend on a monthly basis which makes Main Street Capital’s stock particularly attractive for passive income investors.

On the flip side, I do have issues with the BDC’s very rich valuation which, in my view, translates into an unattractive risk/reward relationship.

Though the dividend is fairly safe, given Main Street Capital’s stable 85% pay-out ratio based on net investment income, I think passive income investors should tread carefully here and not chase the BDC’s 8% yield. Hold.

Be the first to comment