lchumpitaz/iStock via Getty Images

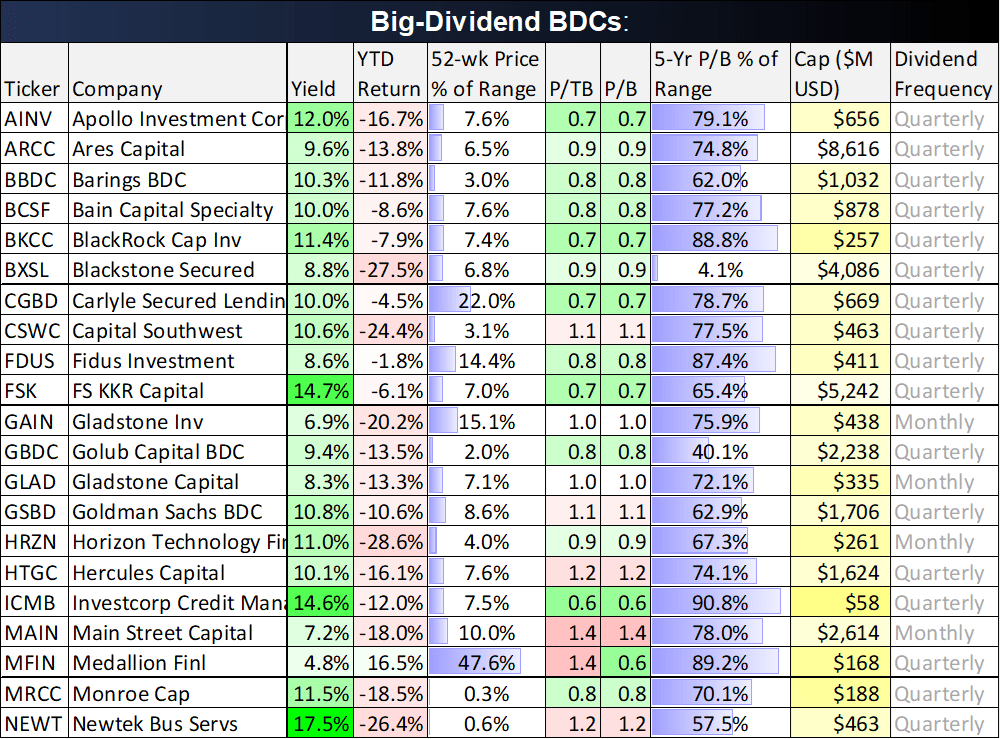

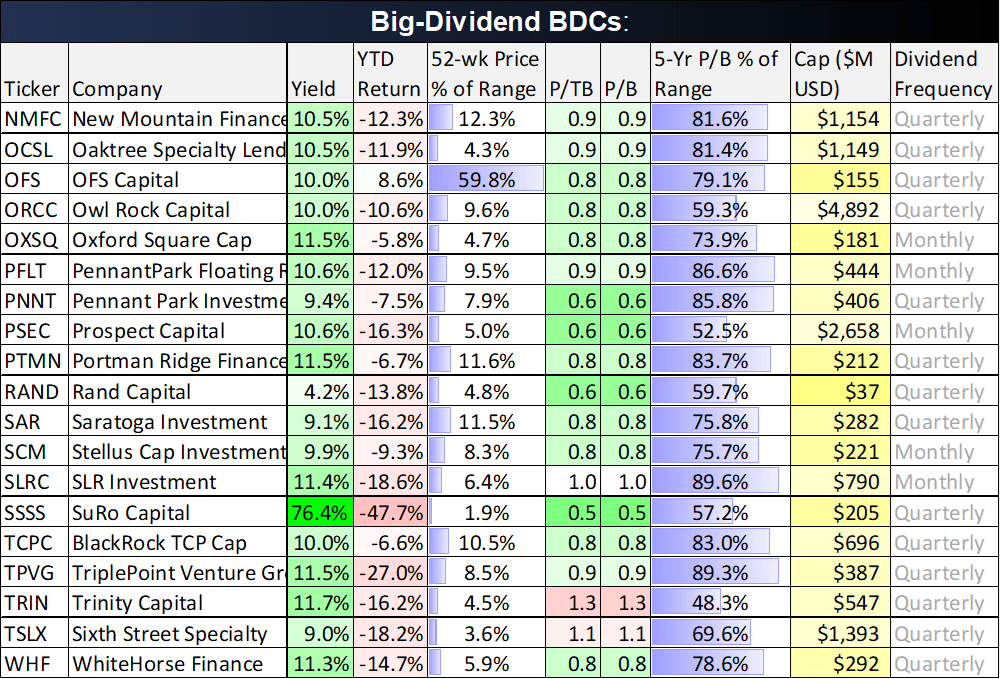

The Fed’s increasingly aggressive interest rate hikes are slamming high-yield investments, and big-dividend BDCs have not been spared (see table below). In this report, we review Houston-based Main Street Capital (NYSE:MAIN), an internally-managed blue-chip BDC that normally trades at a very large premium to book value. We review the business, its liquidity, the dividend, valuation and risks, and then conclude with our opinion on investing.

Data as of Fri 6/17 (source: Stock Rover) Data as of Fri 6/17 (source: Stock Rover)

(ARCC) (CSWC) (FDUS) (FSK) (HRZN) (HTGC) (OCSL) (ORCC) (SAR) (TPVG)

BDC Markets:

Generally speaking, Business Development Companies, or BDCs, provide financing (capital) to companies that are often too small, unique or risky for traditional banks. For example, Main Street Capital takes debt (they make loans) and equity (they take partial ownership) positions in the companies they provide financing too, and they eliminate a lot of the company-specific risks by prudently diversifying their portfolio.

For most BDCs (including Main Street), share prices are down this year, and valuations are increasingly attractive, due to the current market cycle (the Fed is raising rates to slow inflation). Many (but not all) BDCs will continue to pay big, healthy, dividends as they wait for their share prices to eventually rebound. The rebound will be driven by higher rates (similar to a traditional bank, BDCs earn higher net interest margins as rates rise) and the shares will also benefit as the market eventually recovers from the current slowdown (shares are already pricing in a recession, in many cases).

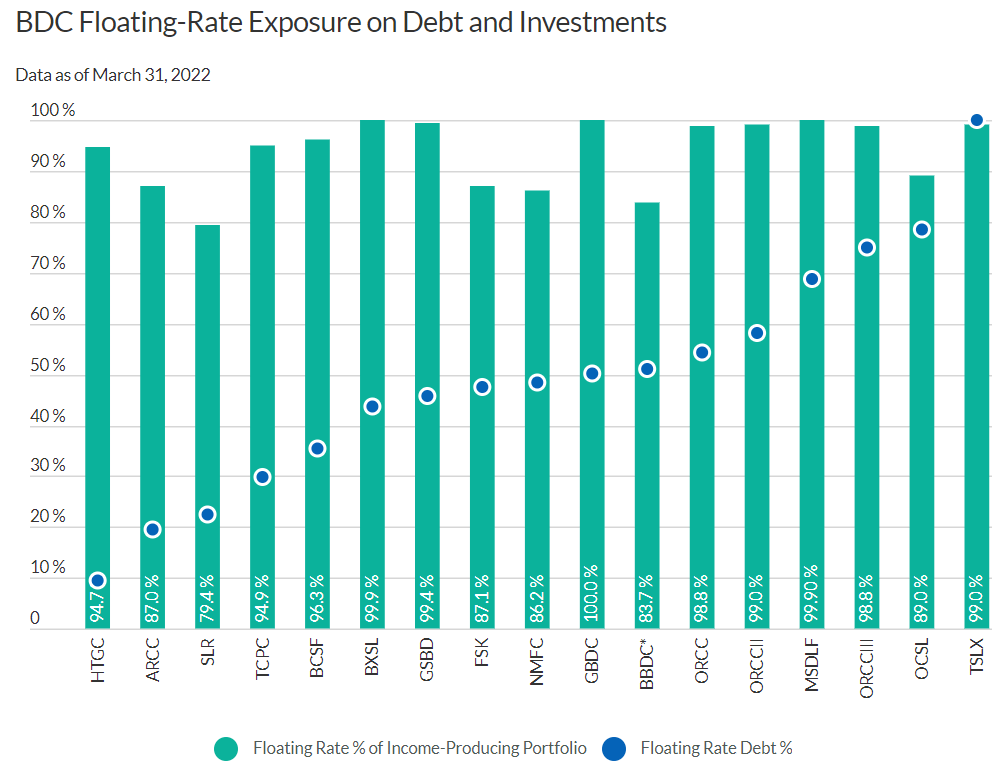

For more perspective, here is a look at how BDCs could benefit in a rising interest rate environment, considering a lot more of their investments pay floating rates as compared to the fixed rates the BDCs pay on their own balance sheet debts.

Fitch Ratings

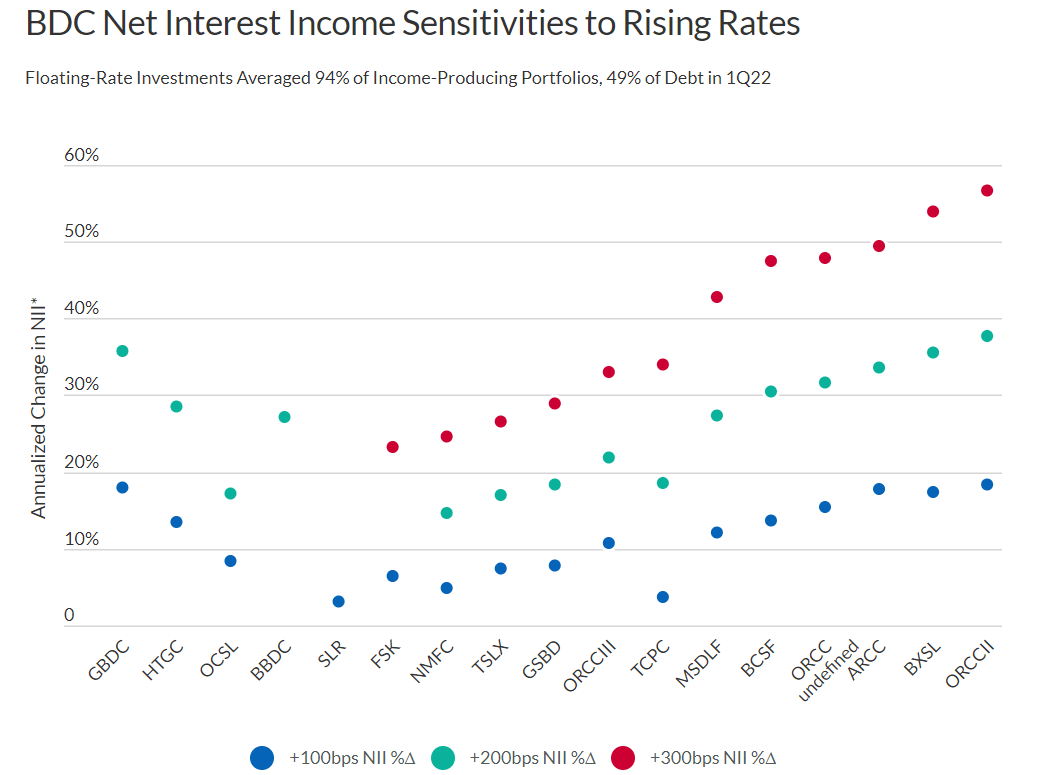

Importantly, according to Fitch Ratings, interest rates impact net investment income (“NII”) in different ways for BDCs. For example:

Higher interest rates pressured NII in 1Q22 as rates had yet to surpass average portfolio investment floors of around 1% while funding costs rose more immediately, but NII is expected to benefit in 2H22 as recent hikes have raised rates above floors. Based on interest rate sensitivities reported by rated BDCs as of March 31, 2022, Fitch estimates that annualized 1Q22 adjusted NII for the rated portfolio could increase by averages of 11% and 26% for 100-basis point (“bp”) and 200-bp parallel rate hikes, respectively. The impact will vary depending on individual BDC’s funding profile and hedging practices.

Fitch Ratings

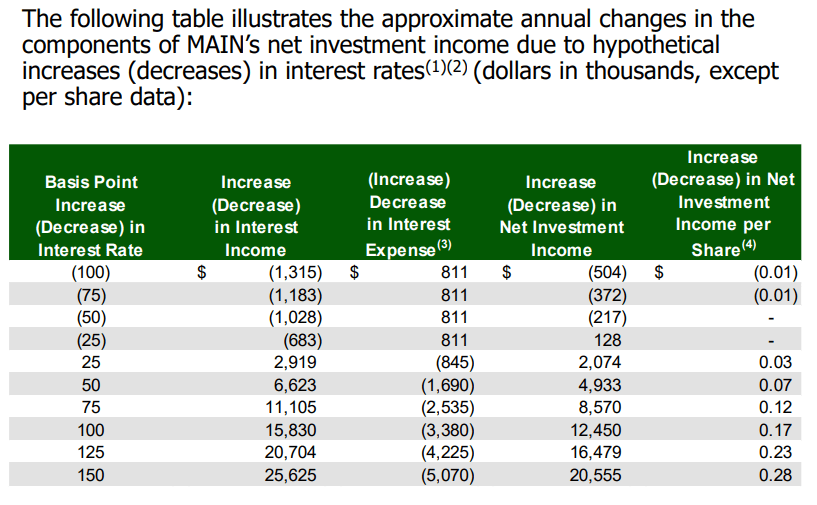

However, it’s also important to note, if the Fed’s interest rate hikes drive us into an ugly recession — then BDC portfolios could face stress, thereby increasing the likelihood of defaults. It’s important to consider each BDC independently. For example, here is a look at interest rate sensitivities for Main Street Capital.

MAIN Q1 Investor Presentation

Main Street Capital:

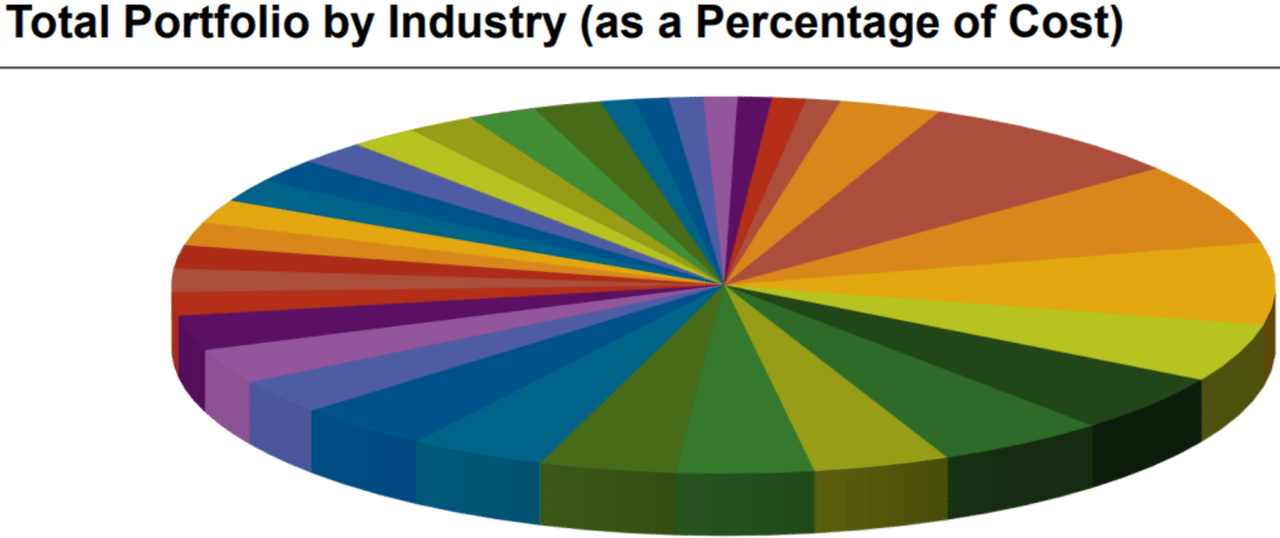

Based in Houston, Texas (but with business diversified across the US), Main Street basically divides its business into four parts, including Lower Middle Market (49% of the investment portfolio at fair value), Private Lending (34%), Middle Market (11%) and Other Portfolio Investments (6%).

Main Street believes its heavy focus on lower middle market opportunities (basically businesses with revenue between $5 million and $50 million, roughly) gives it a unique advantage (because they have less competition and more opportunity in this space, as compared to the simply “middle market” opportunities where many other BDCs focus).

Internal Management: Main Street’s internal management team also gives the business an advantage as compared to most other BDCs which are externally managed. Main Street’s internal management team is able to offer lower management fees (a good thing for investors) and fewer conflicts of interest (also a good thing). Main Street’s management team also has a significant ownership interest (owning 3,125,030 shares as of March 31st), owing about 4.2% of the shares outstanding.

Main Street quarterly investor presentation Main Street quarterly investor presentation

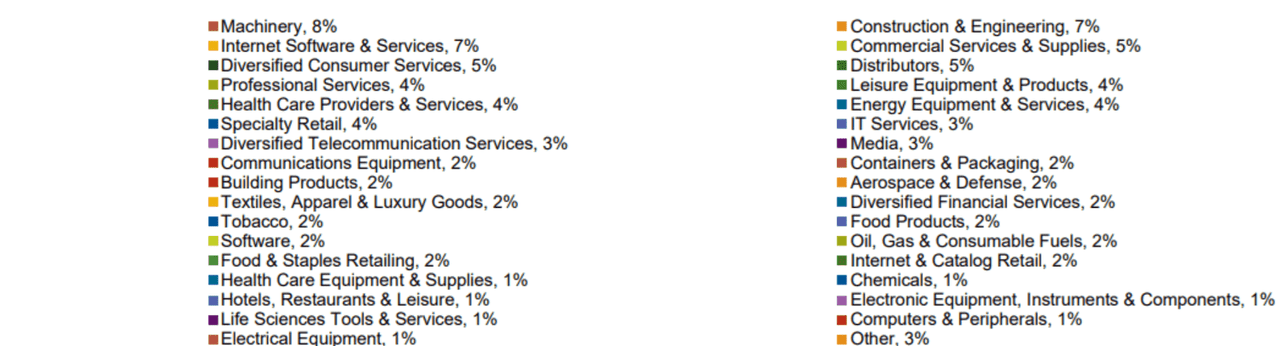

Strong Capitalization And Liquidity Position:

Important to note, Main Street is in a healthy liquidity position, and this will help the company whether challenges as well as take advantage off opportunities. For example, Main Street maintains an investment grade rating of BBB-/Stable from Standard & Poor’s Rating Services.

Main Street quarterly investor presentation

Main Street also owns two Small Business Investment Company (SBIC) Funds, and this provides it access to 10-year, low cost, fixed rate U.S. government-backed leverage. Specifically, Main Street has total SBIC debenture regulatory financing capacity of $350.0 million, the maximum amount permitted under current SBA regulations. The two funds are (1) Main Street Mezzanine Fund (2002 vintage), and (2) Main Street Capital III (2016 vintage).

The Dividend:

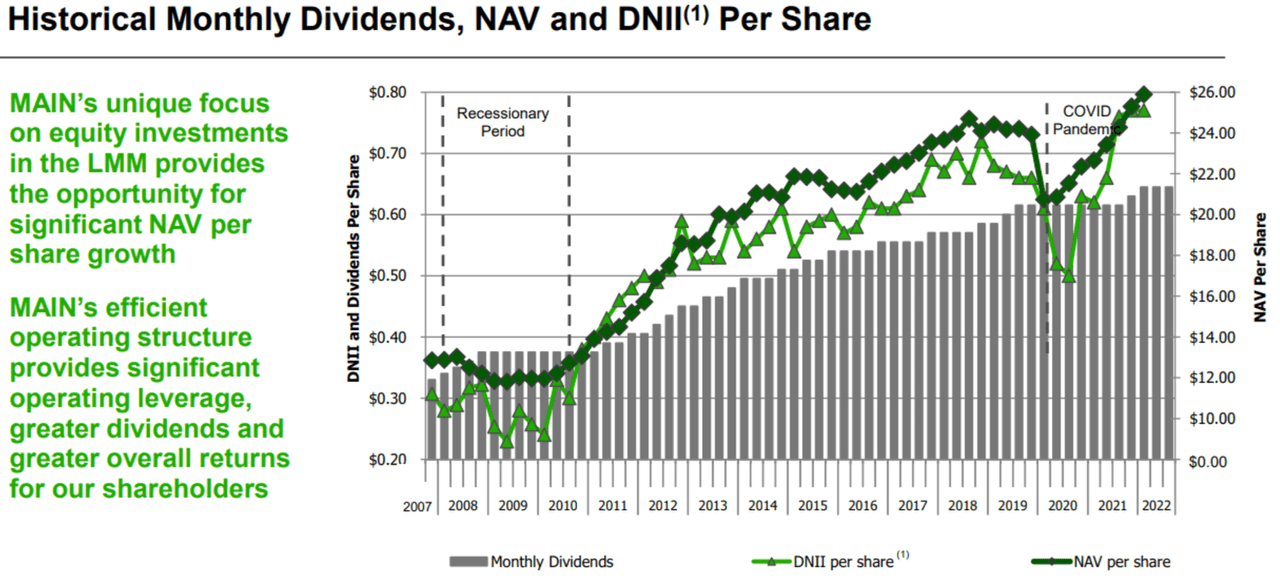

Main Street currently offers a 7.2% dividend yield (paid monthly), as well as ongoing supplemental dividend opportunities. What’s more, Main Street has never reduced its dividend (including through the 2008/2009 recession and the 2020/2021 COVID-19 pandemic). In actuality, Main Street has increased its monthly dividend 95% from $0.33 per share paid in Q4 2007 to declare dividends of $0.645 per share for Q3 2022. Furthermore, (and importantly) Main Street has grown its net asset value (“NAV”) per share by 101% from $12.85 at December 31, 2007, to $25.89 at March 31, 2022 (a CAGR of 5.0%).

Main Street quarterly investor presentation

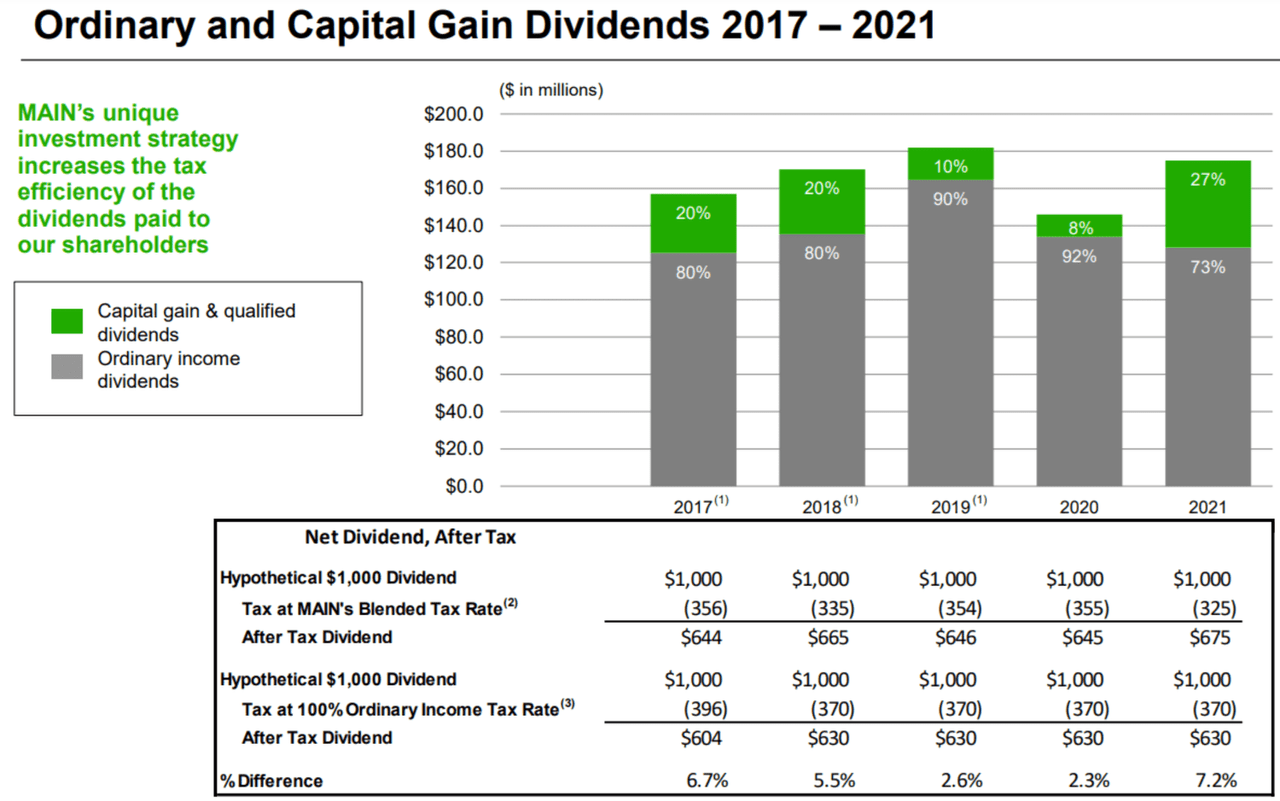

And worth mentioning, for those of you that own MAIN in a taxable account, the operating structure allows a portion of the dividend payments to be qualified, thereby potentially reducing your tax liability (a good thing).

Main Street quarterly investor presentation

Valuation:

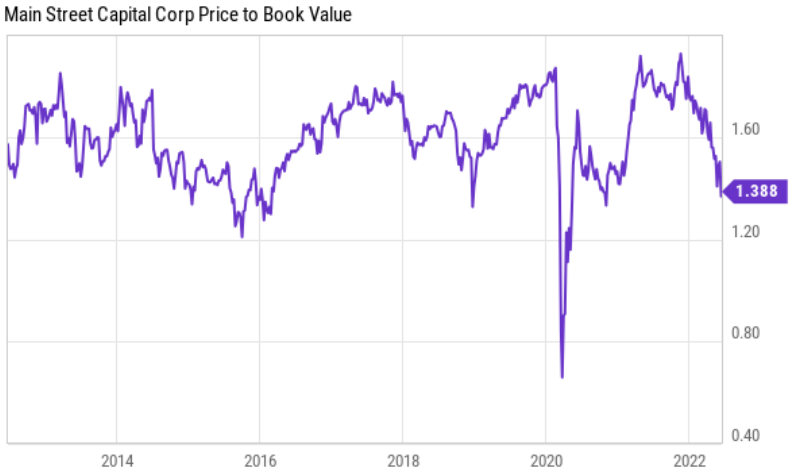

Similar to traditional banks, one of the most basic ways to value a BDC is by considering the share price-to-book-value multiple. For perspective, we provided details on Main Street (as well as 39 BDCs) in the table earlier in this report.

The first thing you might notice (in our earlier, 40-stock, BDC table) is that Main Street appears expensive relative to other BDCs on a price-to-book basis. However, Main Street has historically always traded at a significant premium (investors appreciate the unique lower middle market strategy and the internal management team). Further, Main Street actually trades at a low valuation multiple as compared to its own history (also a good thing, considering the strong liquidity, dividend and business). Historically, it has not been uncommon to see Main Street trading at a price-to-book of 1.8x and 1.9x for an extended period of time. It is currently below 1.4x.

YCharts

Risks:

The market cycle is perhaps the biggest risk for Main Street Capital. Because Main Street provides financing to riskier small and micro-cap companies, this increases the risks during downturns in the market cycle. For example, as you can see in our earlier chart, Main Street’s “Distributable Net Investment Income” (or DNII) pulled back significantly in ’08-’09 (Financial Crisis) and again in ’20 (when the covid pandemic hit). It is true the business faced significant challenges during these periods (as some of the underlying portfolio companies struggled mightily), but it is important to note that Main Street never reduced its dividend payment.

Currently, we are at a point in the market cycle where the Fed is tightening, and this is coming at a very short time period after the Fed was loosening dramatically to deal with covid. Share prices across the market (including BDCs) have fallen this year. Depending on the severity of the current market pullback (which remains to be seen), Main Street could fall further. However, given the company’s strong liquidity position (and well-diversified portfolio), we believe Main Street will be able to weather even a significantly more extreme pullback, and we also believe the dividend will likely remain steady. Further still, we believe the market will get better, and Main Street’s share price, dividend and NAV will all rise again in the future.

The Bottom Line:

BDCs are a bit risky by nature. That’s why banks generally stay away from the types of loans and financing that BDCs provide to portfolio companies (especially considering the more stringent bank regulations put in place following the ‘08-’09 Financial Crisis). Further, if the Fed’s interest rate hikes lead us into an ugly recession, a lot of BDC portfolio companies could be particularly sensitive considering they are smaller and riskier by nature.

Nonetheless, we view Main Street Capital’s business and current valuation as compelling enough to add it to our top 10 list of big dividends. In particular, Main Street has a relatively strong liquidity position, a healthy dividend, a lower price-to-book (by historical standards) and an experienced internal management team with a growing track record of successfully navigating business cycles. We are currently long shares of Main Street in our Income Equity portfolio, and regardless of any near-term volatility—in the long term we expect the dividend, NAV and share price to all increase.

Be the first to comment