FreezeFrames

In a recent piece, I laid out the case for going long energy stocks at this time by stating:

“Going forward, as such artificial manipulative measures as SPR releases and zero-Covid conclude, we will likely find tailwinds gathering strength in the near future… I continue to believe the structural oil bull market is intact in the medium to long term, and the physical oil supply-demand dynamic remains strong in the near term in spite of the apparent weakness in the financial oil market.”

I also mentioned that, generally speaking, the capital efficiency of exploration and production (E&P) companies tends to decrease during the latter part of an oil bull market, while the profitability of oilfield service companies tends to increase. This generally favors oilfield service stocks.

To clarify, I did not mean to suggest that E&P stocks are no longer worth investing in during the middle and late phases of an oil cycle. Rather, I merely implied that investors should focus on the sustainability of profitability of oil and gas producers as they enter the middle-late cycle, and pay particular attention to the specific risks associated with this phase.

- Whether an oil and gas producer can maintain high levels of profitability during the latter half of an oil cycle depends on both the characteristics of its producing fields and the efficiency and financial management skills of its management. To assess these factors, investors should consider the following variables: (1) the price at which the company is able to sell its commodities; (2) the cost of finding and developing new reserves (F&D cost) and the operating cost per unit of production; and (3) the rate of production growth, as I explained in a previous interview.

- Investors should consider whether it is still a good idea to continue investing in a jurisdiction where the government may cause geopolitical tensions in order to boost revenue, or where it plans to increase its share of profits from rising commodity prices. There are many ways in which a government can increase its take, such as implementing a windfall tax like in the U.K.’s North Sea and Colombia, or introducing local commodity price controls as may be implemented in Australia, or by nationalizing oil and gas assets. The sliding-scale royalty system in Canada is another example of a windfall tax that automatically increases royalties as oil and gas prices rise.

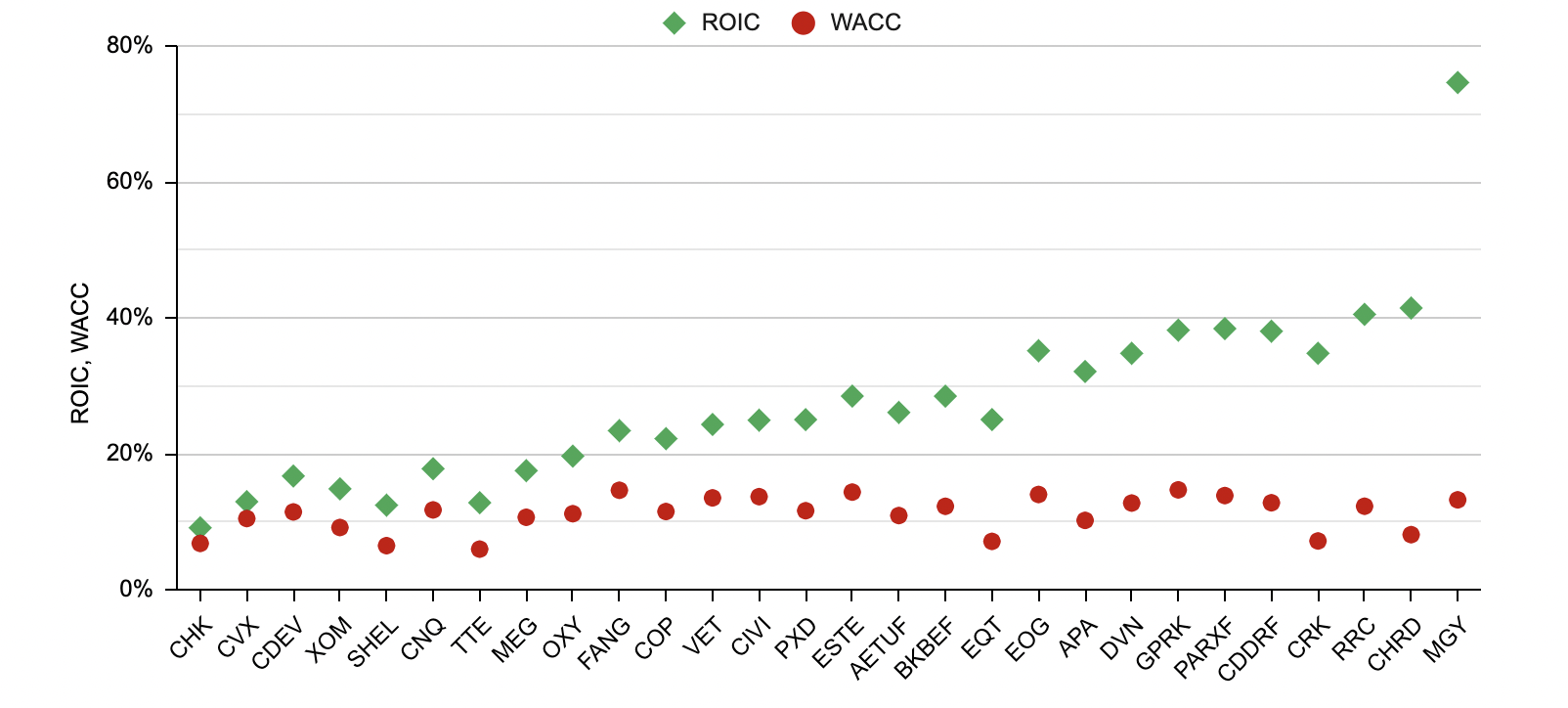

Below, I present an E&P company called Magnolia Oil & Gas Corp. (NYSE:MGY) that, in my opinion, is well-positioned to maintain its high profitability without exposing investors to excessive risks. As a result, I believe this company has a good chance of outperforming other E&P companies as the oil cycle progresses in the next few years (Fig. 1). Magnolia Oil & Gas is a pure-play in the re-emerging Austin Chalk play in Texas. I first discussed the investment potential of Magnolia in an article published in May 2022.

Fig. 1. The ROIC and WACC of a select group of oil and gas producers arranged in the order of rising ROIC – WACC from the left-hand to the right-hand side (Laurentian Research based on ROIC and WACC estimates from Gurufocus, with some WACC estimates therefrom recalculated)

Business model

Since the passing of former Chairman, President, and CEO Stephen Chazen in September 2022, Magnolia Oil & Gas – the company he founded after leaving Occidental Petroleum (OXY) – seems to have continued to perform well, under the leadership of current Chairman Dan F. Smith (formerly of Lyondell Chemical) and CEO and President Christopher G. Stavros (a long-time protege of the late Chazen). Stavros said:

“The principles of the business model that Steve established during Magnolia’s founding over four years ago are expected to remain unchanged. We will continue our discipline around capital spending, while maintaining low levels of debt. We expect our record of achieving moderate annual production growth, while generating significant free cash flow and strong pre-tax margins to continue.”

Operations

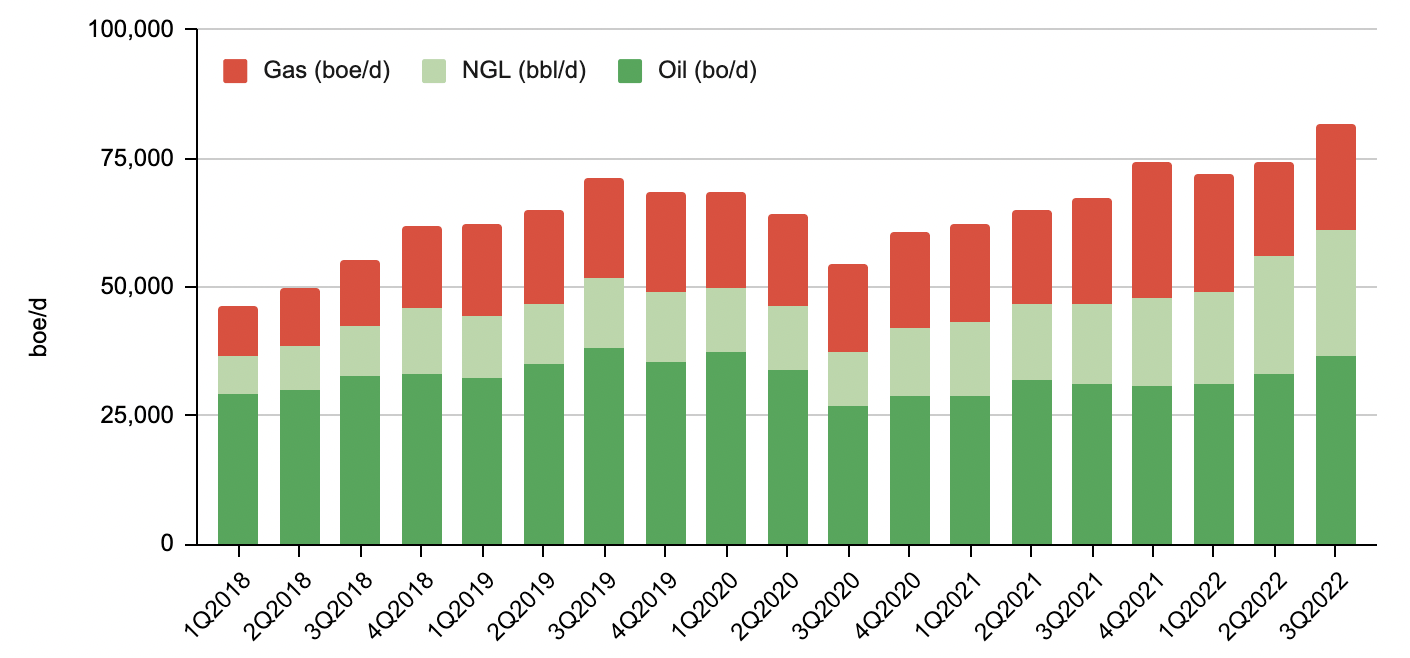

In 3Q2022, Magnolia reached a quarterly record of average total production of 81,529 barrels of oil equivalent per day (boe/d), representing a 9.9% increase from the previous quarter or a 21.0% year-over-year growth (Fig. 2).

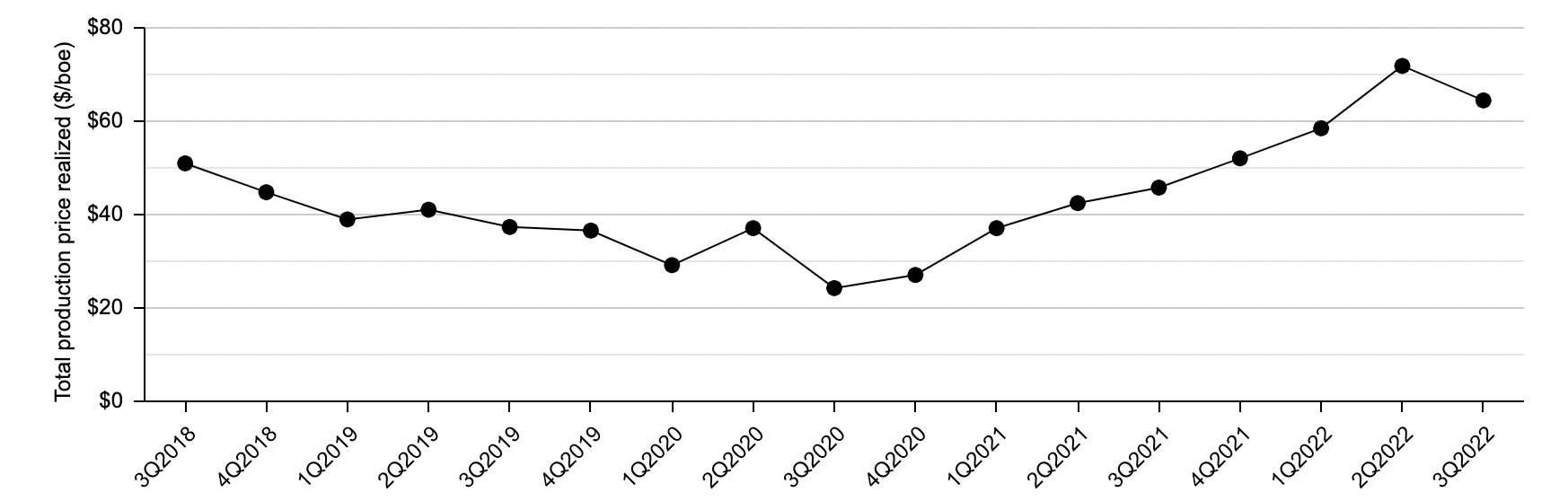

In the first nine months of the year, Magnolia received prices for its commodities that were 101% of the West Texas Intermediate (or WTI) price and 93% of the Henry Hub price. This excellent commodity price realization was due to the company’s land holdings in the Austin Chalk and Eagle Ford plays being located close to infrastructure and downstream markets in the Gulf Coast. With liquids production stabilizing at around 70%, Magnolia achieved a realized price of $64.40/boe in 3Q2022, which was 10.3% lower than the previous quarter but 40.8% higher than the same quarter one year prior (Fig. 3).

Fig. 2. Quarterly average production of crude oil, NGLs and natural gas of Magnolia (Laurentian Research based on Magnolia financial filings and Seeking Alpha)

Fig. 3. Quarterly total production price realized by Magnolia (Laurentian Research based on Magnolia financial filings and Seeking Alpha)

Costs and profitability

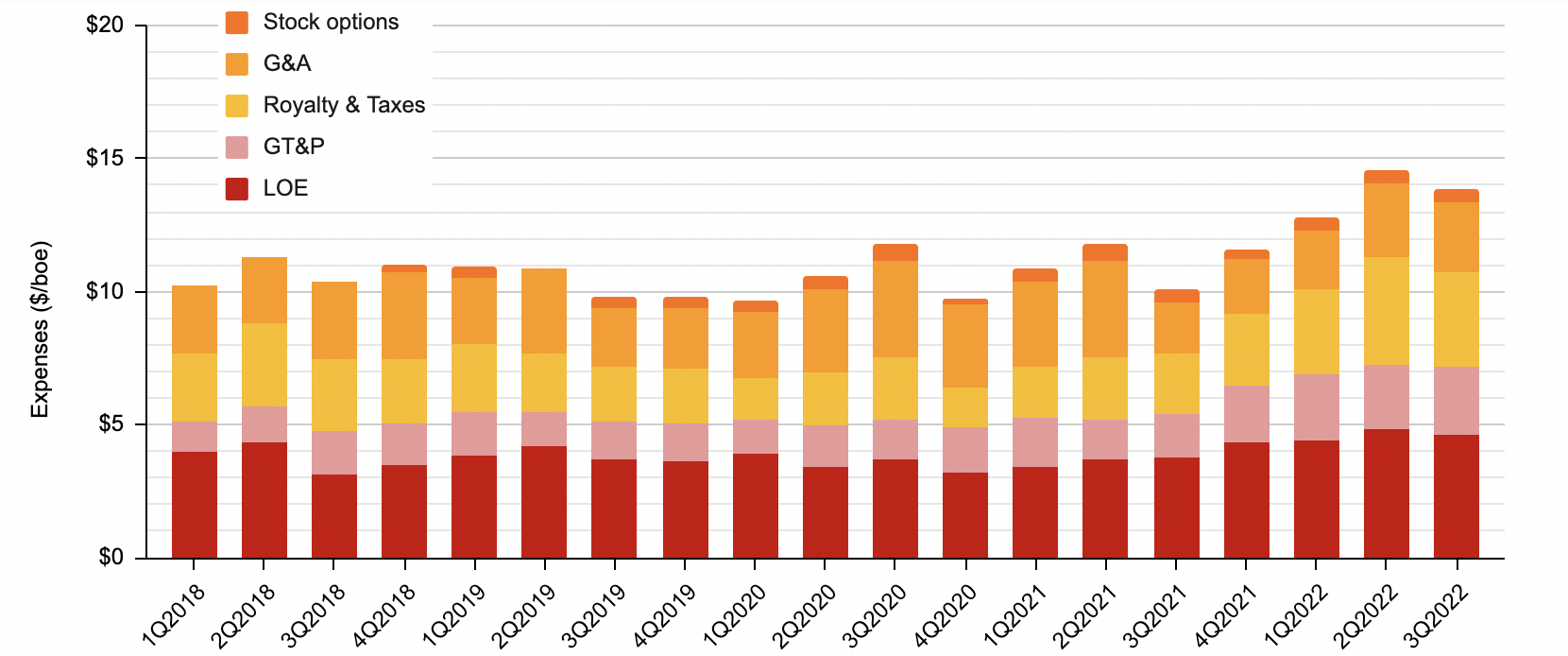

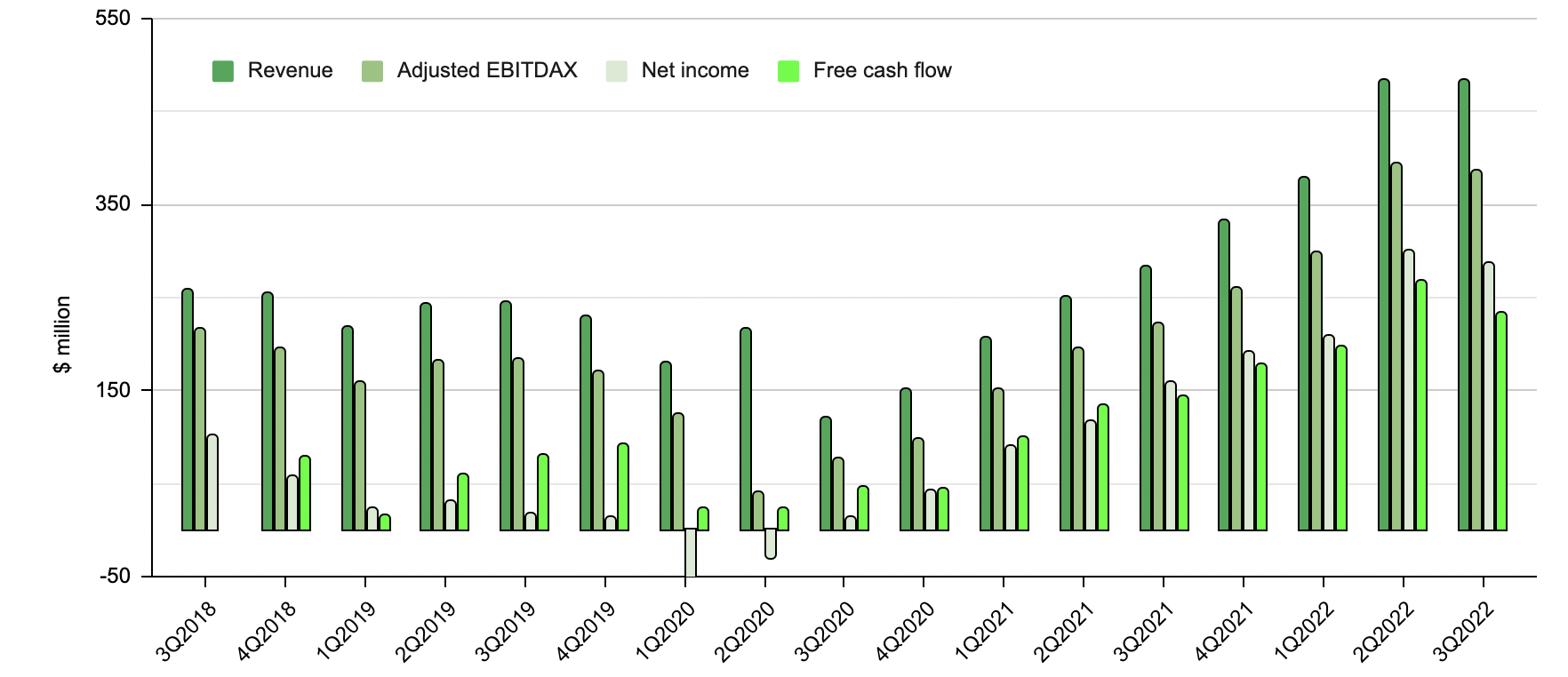

On a per barrel of oil equivalent basis, cash operating costs have increased by 39.1%. However, this is still below the rate of commodity price appreciation, with industry-wide cost inflation partly offset by economies of scale resulting from production expansion (Fig. 4). As a result, Magnolia’s revenue was essentially the same as the previous quarter, and it generated slightly less adjusted EBITDAX, net income, and free cash flow sequentially. However, year-over-year, the company achieved spectacular growth of 70.3%, 74.3%, 79.5%, and 63.0% in revenue, adjusted EBITDAX, net income, and free cash flow, respectively (Fig. 5).

Fig. 4. Unit costs of Magnolia by quarter (Laurentian Research based on Magnolia financial filings and Seeking Alpha)

Fig. 5. Quarterly revenue, adjusted EBITDAX, net income and free cash flow of Magnolia (Laurentian Research based on Magnolia financial filings and Seeking Alpha)

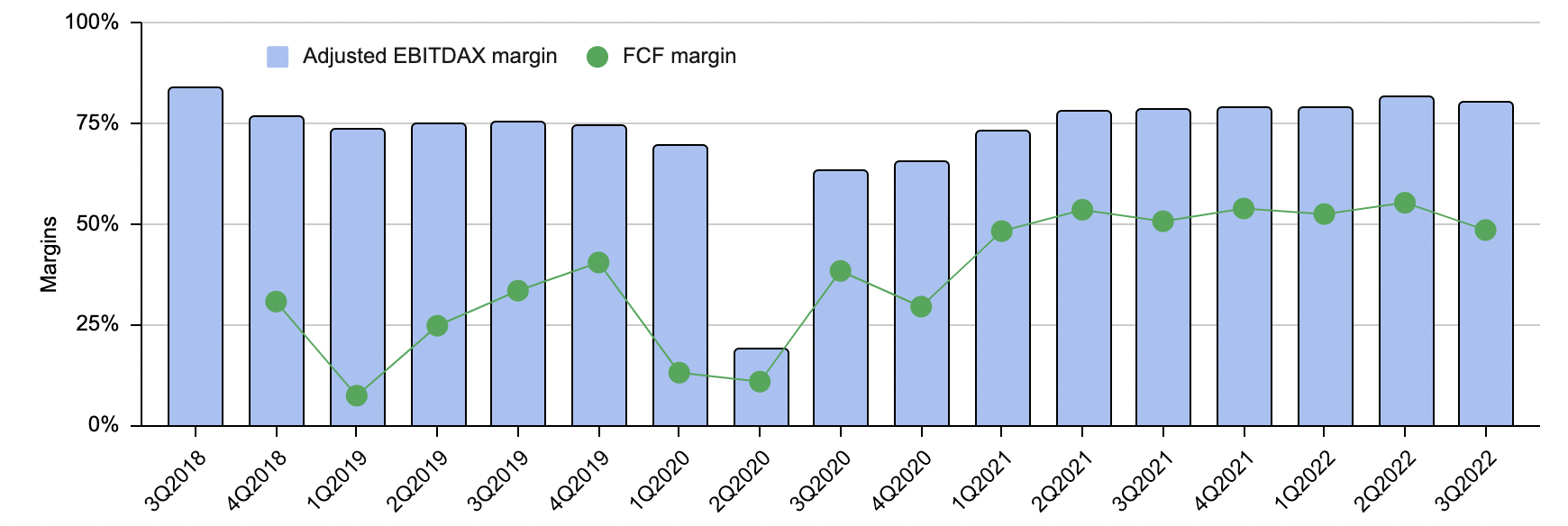

The adjusted EBITDAX margin and free cash flow (or FCF) margin have recovered from the trough caused by the Covid-19 pandemic to levels that are higher than in pre-pandemic 2019. These margins did decline by 1-7% sequentially, but they remained at high levels of 79.9% and 48.4%, respectively (Fig. 6). In other words, Magnolia continues to be highly profitable in the current inflationary environment.

Fig. 6. Quarterly adjusted EBITDAX and FCF margins of Magnolia (Laurentian Research based on Magnolia financial filings and Seeking Alpha)

Shareholder rewards

Out of the $233.9 million in free cash flow, the management used $62.4 million for share repurchases, $21.8 million for dividends, and $114.5 million for drilling and completions capital expenditures. This resulted in a net cash position of $20.9 million.

Outlook

Magnolia plans to spend $125-$140 million in capital in 4Q2022. However, the resulting production additions will mostly occur toward the end of the quarter and in early 2023. The company expects its 4Q2022 production to average 77,000-79,000 boe/d, with no hedging. Magnolia also expects to reduce its fully-diluted total share count by 6% year-over-year to 216 million in 4Q2022, and it purchased 2 million class-B common shares for approximately $48.8 million.

In 2023, the company plans to operate two drilling rigs and one completion crew, targeting a 10% production growth over the 2022 full-year average and expecting to generate a significant amount of free cash flow. In addition to continued share buybacks, Magnolia plans to raise its dividend by 10% in early 2023.

Valuation and risks

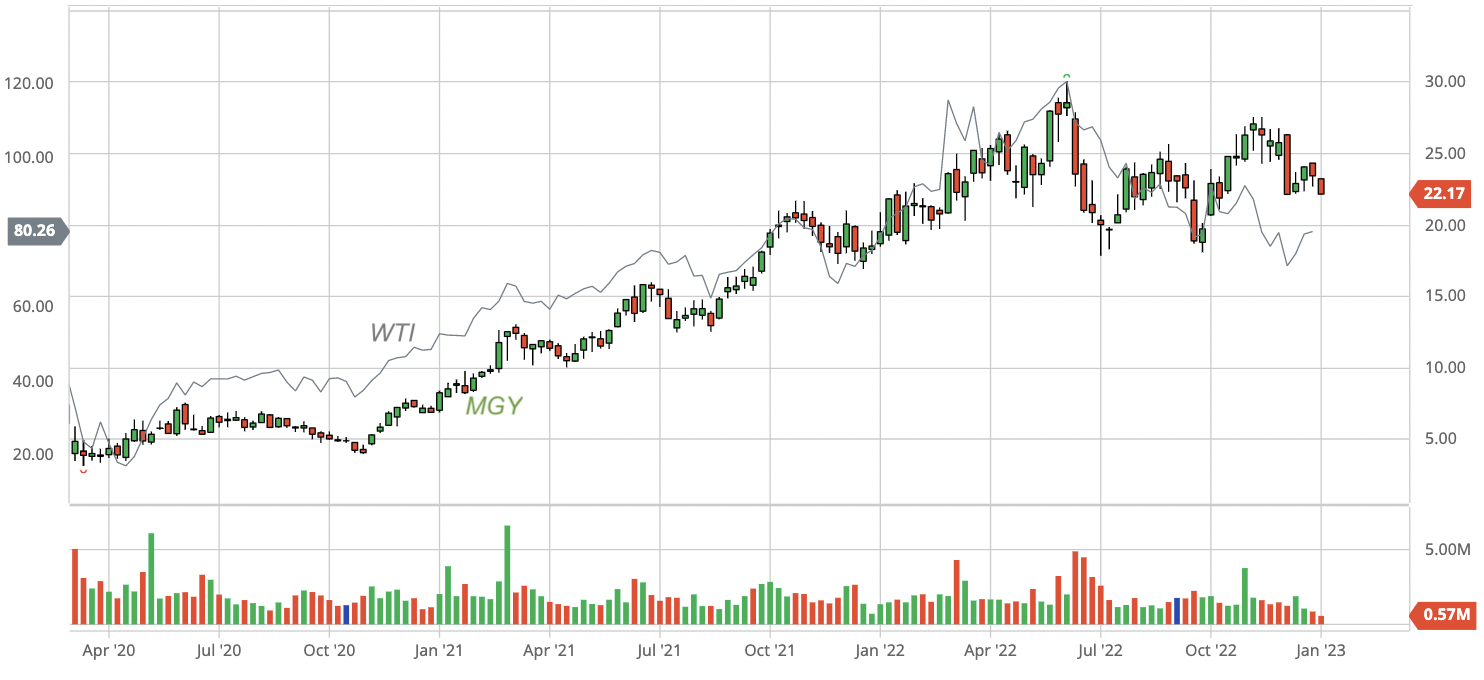

Assuming a 10.79% production growth rate over the next five years, and maintaining flat production for an additional five years before a 10% per year terminal decline, Magnolia is estimated to have an intrinsic value of $42 per share on a ceteris paribus basis, implying a discount of 47% to the share price of $22.14 as of January 3, 2023 (Fig. 7). This represents a large margin of safety, considering that Magnolia is a high-margin, debt-free business.

Fig. 7. Stock chart of Magnolia Oil & Gas (MGY), dividend back-adjusted, as compared with the WTI benchmark oil price (modified from Barchart and Seeking Alpha)

The main risks to this upside include:

- The Giddings field in the Austin Chalk play used to have poor repeatability of well productivity, as I previously discussed, but Magnolia appears to have addressed this issue through horizontal drilling and hydraulic fracturing. However, investors should continue to monitor this issue.

- Magnolia has been conservative in reserves booking, which the market may not appreciate. The market may not give the Eagle Ford and Austin Chalk participants the same premium valuation as operators in the Permian Basin, despite the favorable price realization of South Texas oil and gas.

- Magnolia does not hedge commodity prices, which may introduce volatility in the event of a commodity price crash, but can serve as tailwinds in a bullish environment.

The main attraction of Magnolia as an investment is its ability to achieve decent annual production growth and high profit margins during the oil up-cycle while maintaining a squeaky clean balance sheet, which exposes shareholders to relatively low risks. It follows that an investor should be prepared to exit the investment if management abandons its characteristic financial conservatism, or if an end of the oil bull market appears to be near, which I believe is still years away.

Investor takeaways

Magnolia Oil & Gas Corp. may be a great stock to own for investors who are bullish oil but are worried about potential stock market volatility due to a recession. Magnolia has a track record of steady production growth and maintaining high profit margins while remaining debt-free. Additionally, the stock is currently trading at a significant discount to its estimated intrinsic value, which offers an asymmetrical risk-reward profile that favors the investor.

Be the first to comment