mi-viri

Madrigal

The most important quality for an investor is temperament, not intellect. – Warren Buffett

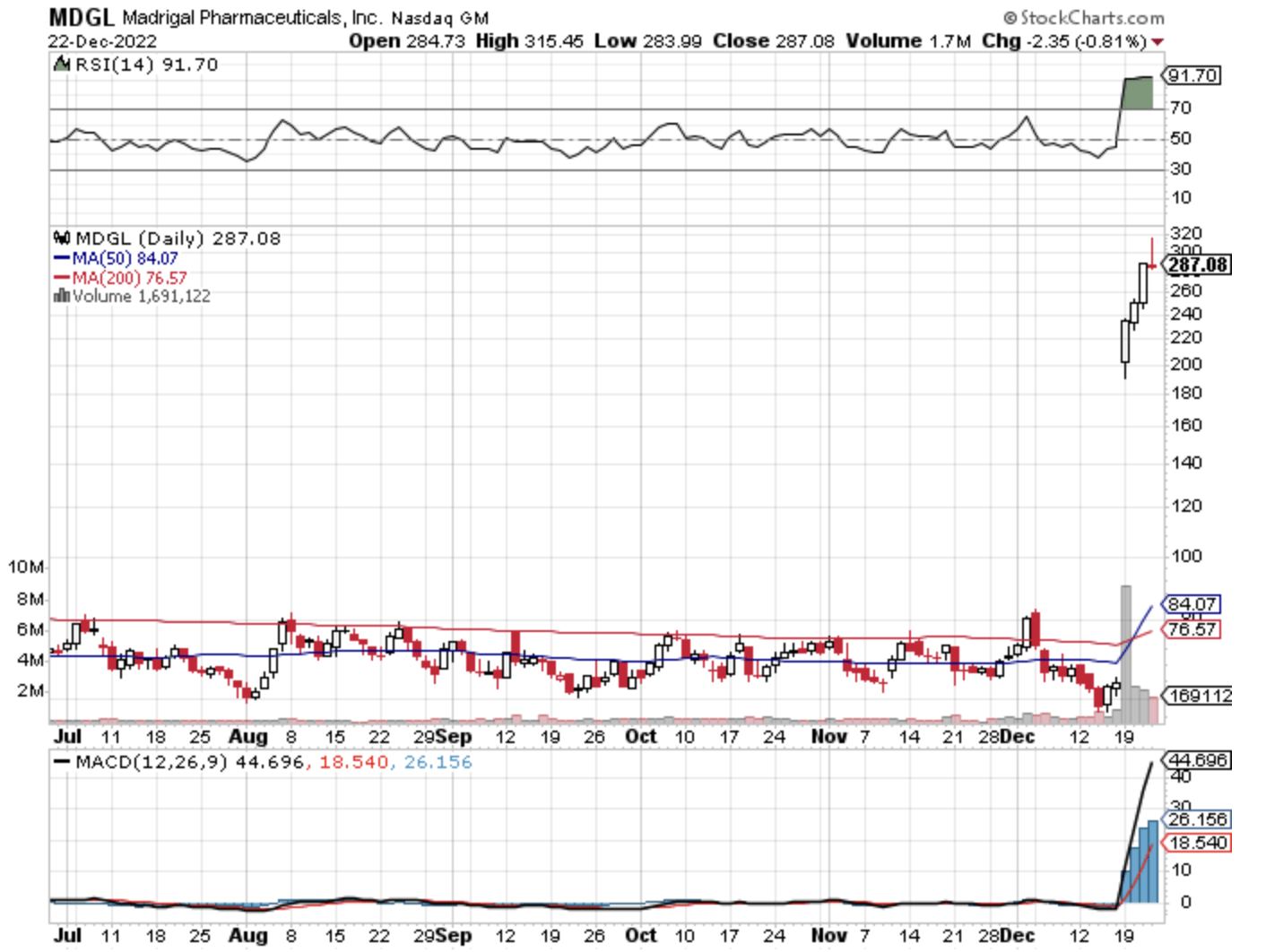

After shares gap up following either a drug approval or a Phase 3 data release, they usually trade lower in the following days. Nevertheless, there is certain equity that continues to rally due to extremely powerful fundamental developments. That is to say, if the aforesaid event would unlock the mega-blockbuster value of a lead drug, chances are that the stock would rally much higher.

Following robust MAESTRO-NASH for resmetirom (as I forecasted), Madrigal Pharmaceuticals (NASDAQ:MDGL) stock continues to exchange hands much higher even after its meteoric rise. Precisely speaking, there is a good chance that Resmitirom would gain approval and thereby generate windfall profits. In this research, I’ll feature a fundamental analysis of Madrigal while focusing on the latest corporate developments.

StockCharts

Figure 1: Madrigal chart

About The Company

As usual, I’ll present a brief corporate overview for new investors. If you are familiar with the firm, you should skip to the next section. I noted in the prior research,

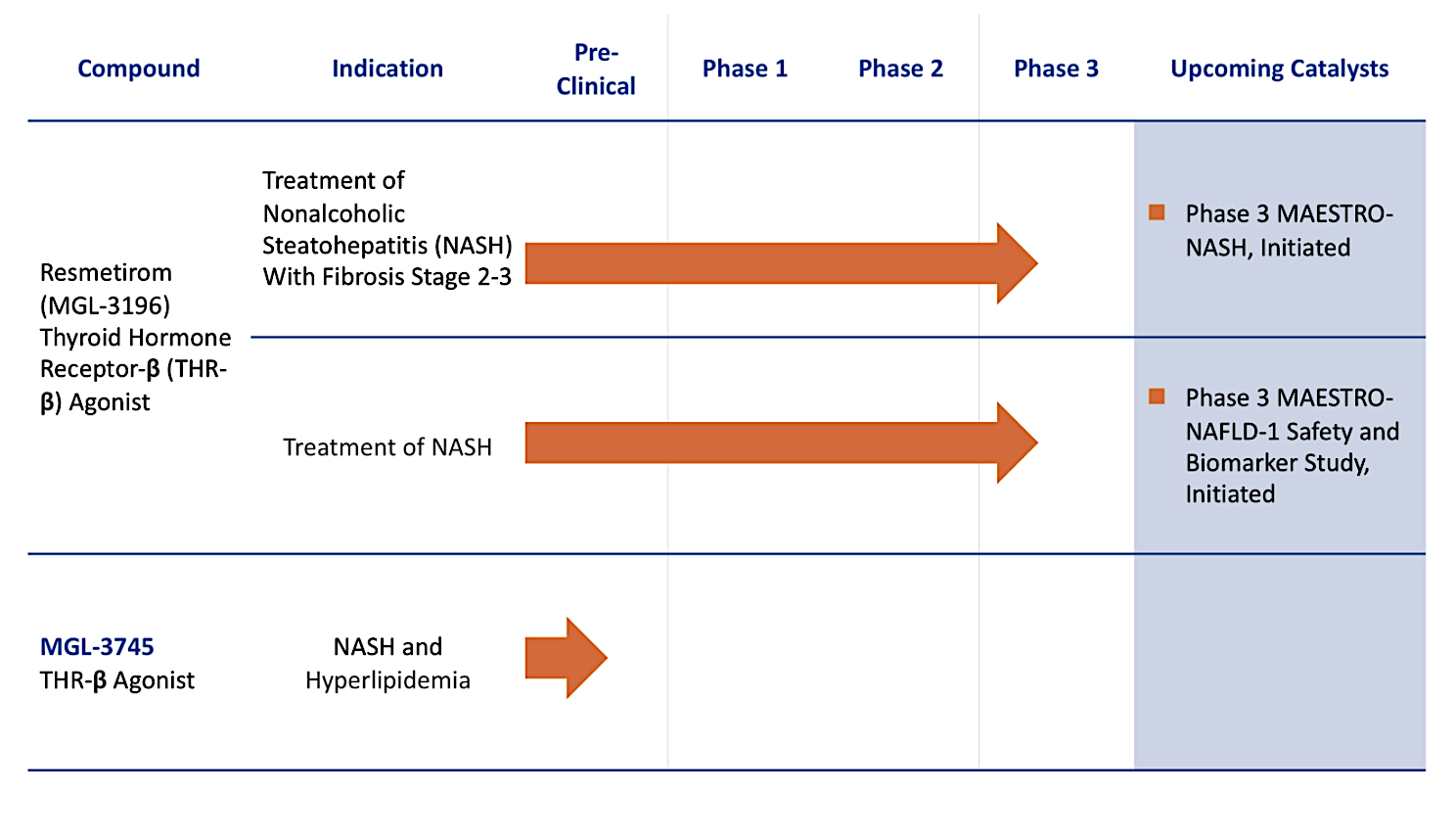

Headquartered in Conshohocken, Pennsylvania, Madrigal is focused on the innovation and commercialization of stellar medicine to serve the unmet needs in heart and liver diseases. In executing a laser-beam-focused approach, the company is innovating only two powerful medicines for non-alcoholic steatohepatitis (i.e., NASH) and related conditions. As the crown jewel, resmetirom (i.e., Resme) is a thyroid hormone receptor-beta (THR-B) designed to treat NASH. Due to the robust data, it is likely to become the first approved medicine for this untapped market.

Madrigal

Figure 2: Therapeutic pipeline

Non-Alcoholic Steatohepatitis

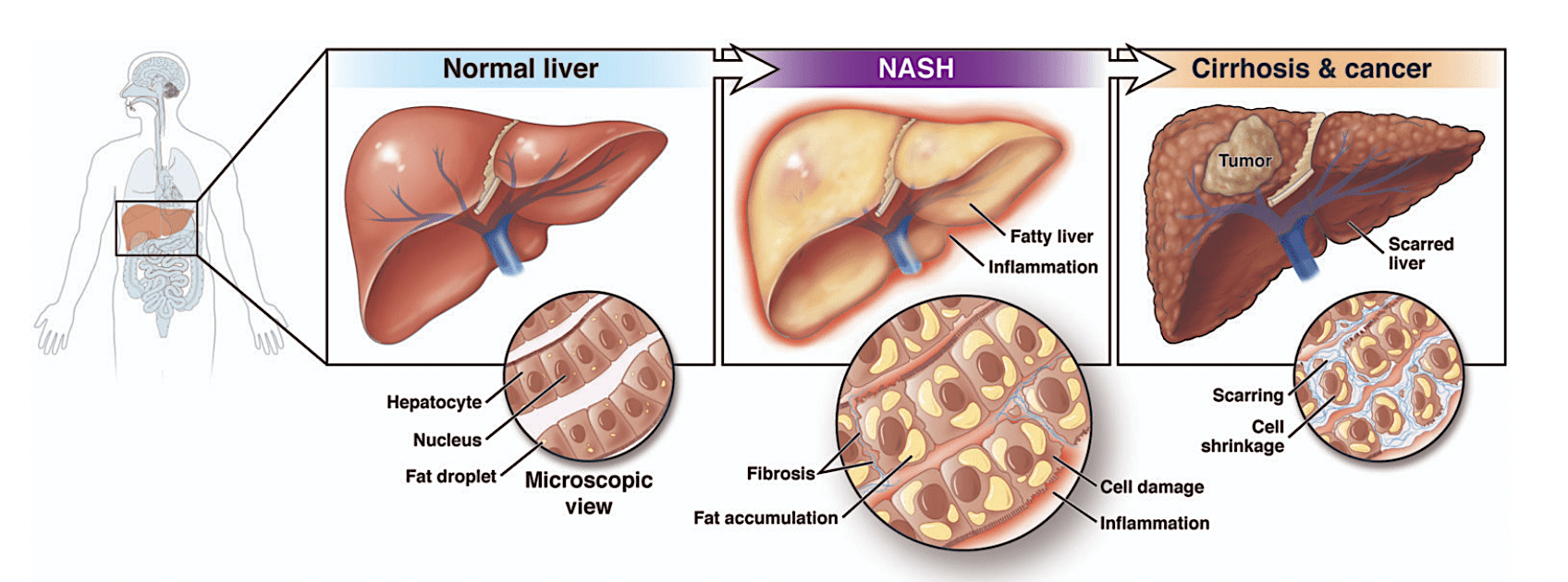

Shifting gears, let us quickly go over the science of NASH. After all, it would allow you to better appreciate the clinical data of Resme. As shown below, NASH occurs on a spectrum of liver diseases. Characterized by a fatty liver with cellular inflammation and fibrosis, NASH progresses over time to liver cirrhosis. At this point, the liver is dead with scarred tissues, and thereby lost its function.

AGA

Figure 3: NASH pathology

Resmitirom Is The Silver Bullet NASH

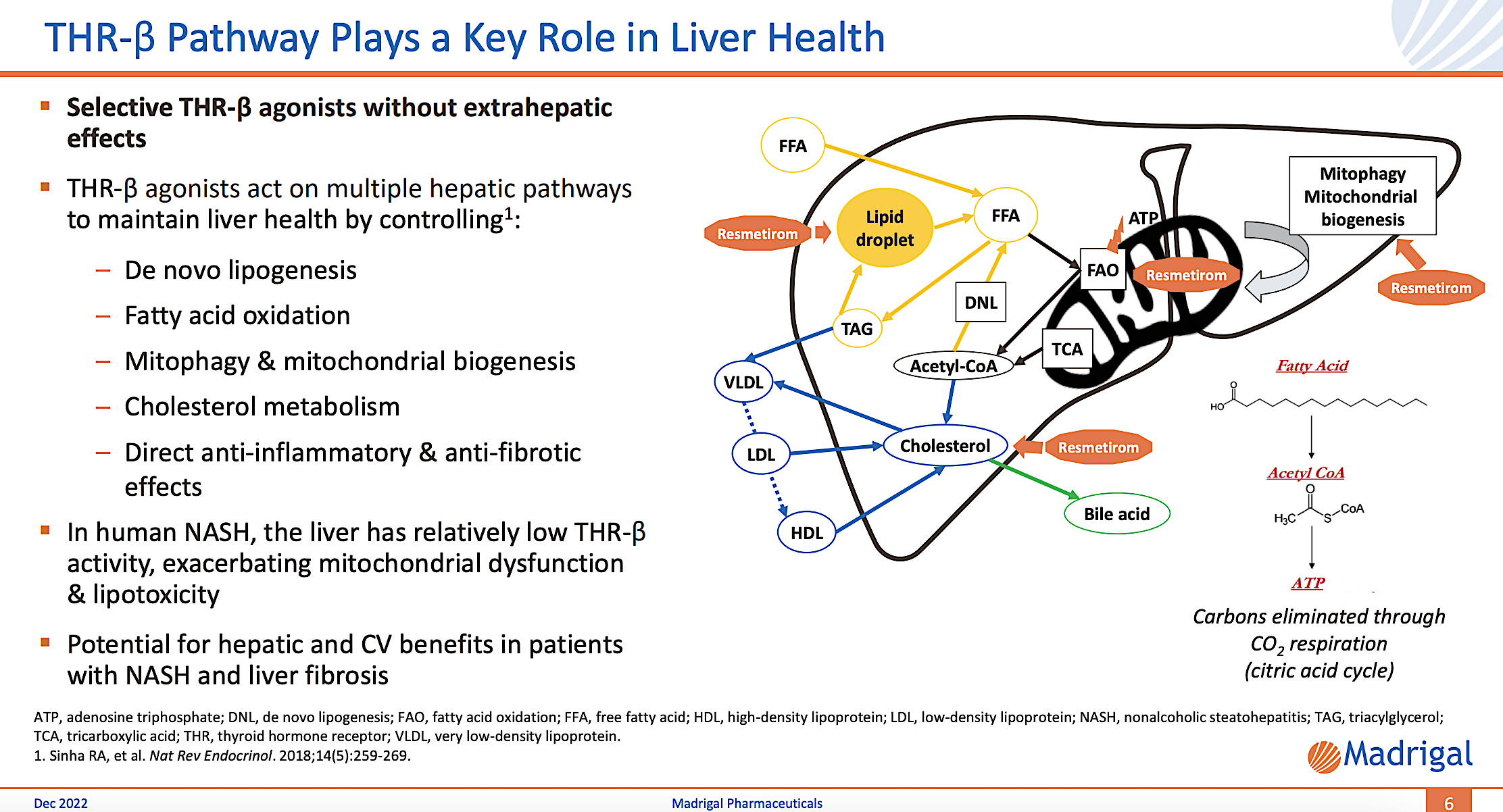

As you can appreciate, Resme is special because of its mechanism of action (i.e, MOA) that helps unlocks the liver’s natural healing capacity. Notably, the liver is the only organ in the body that can regenerate itself. Let’s say you cut part of it off, the liver will regrow the missing volume. Here’s where things get tricky. In the fatty liver, excessive fat and inflammation overwhelm the liver’s regenerative ability. As it loses its self-healing prowess, the liver spirals downward in the NASH disease continuum.

By ramping up the liver’s internal fat-burning furnace with Resme, its natural healing capability kicks into high gear. The ultimate result is NASH reversal. Unless the liver is already severely cirrhotic, you can bet that Resme would reverse the disease course. After all, the liver has unique self-healing power.

NASH pathology

Figure 4: Resme’s mechanism of action

Robust MAESTRO-NASH Efficacy Data

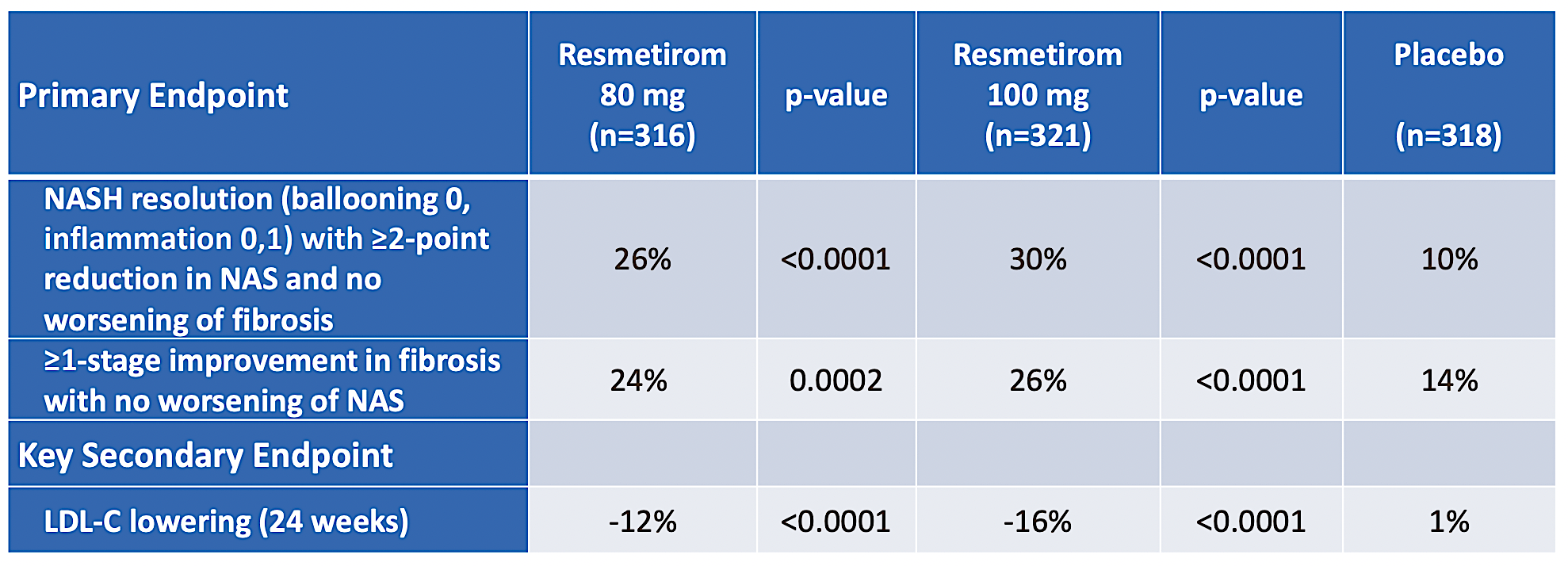

As you know, Madrigal posted extremely robust Phase 3 (MAESTRO-NASH) data on December 19. In the aforesaid high-quality 52-week serial liver biopsy study, Resme cleared both its primary endpoints (as shown below). In other words, both patients in the 80mg doses and 100mg doses groups experienced NASH resolution and fibrosis-stage improvement.

Moreover, there is a “dose-dependent” response. Specifically, 26% of the patients taking the 80mg doses enjoyed NASH resolution; whereas, 30% of the patients on the 100mg doses experienced a similar effect. As you can appreciate, a dose-rose response relationship supports strong efficacy. And given that the p-values are all far lower than 0.05, there is strong statistical significance. Simply put the results are real rather than random occurrences.

NASH pathology

Figure 5: Robust Resme’s efficacy

Additionally, Resme also cleared its secondary endpoints with flying colors. That is to say, there were clinically meaningful reductions in LDL as well as other liver enzymes like AST, ALT, and GGT. Taken all together, you can bet that if there is a silver bullet for NASH, this is it.

Superb Tolerability Profile

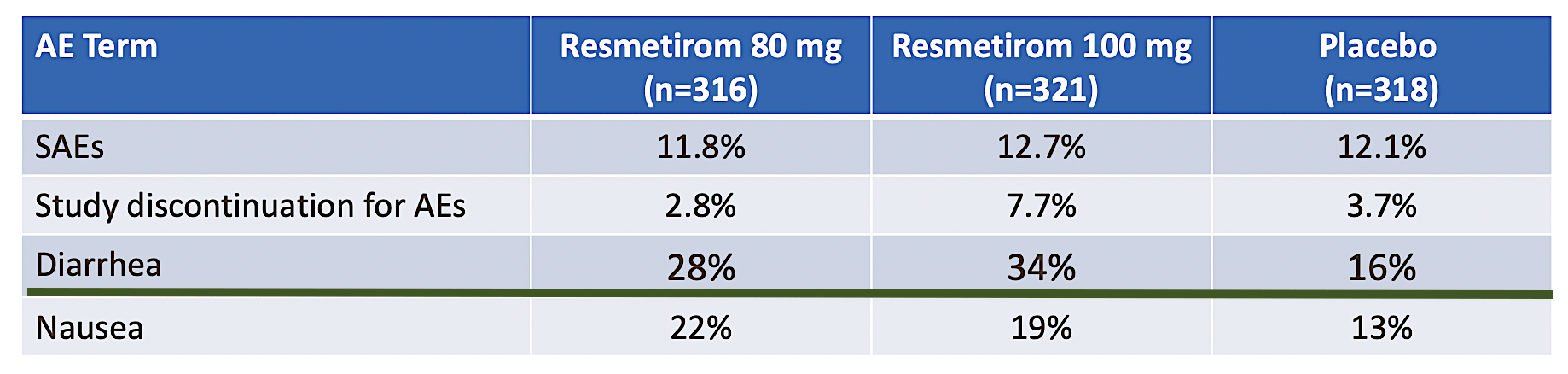

As you can see, other developing NASH drugs like OCA have been hit with significant side effects like pruritus (i.e., itching). On the surface, you don’t believe that itching is a big deal. Nevertheless, it can be quite significant for the patients and thereby limiting the drug’s utility. If the patient can’t tolerate the drug, it won’t be prescribed much even with approval.

Viewing the figure below, you can appreciate that Resme has a highly favorable safety profile. That is to say, its side effect is similar to the harmless sugar pill (i.e., placebo). Moreover, the study discontinuation due to an adverse event is also similar to a placebo. Therefore, you can tell the drug is quite safe.

Now, looking at the green highlighted line below, you can see that the proportion of patients on Resme who experienced diarrhea was much higher than those on the placebo. Moreover, the higher (i.e., 100mg) dosage experience even more diarrhea. As you can imagine, diarrhea is an indication that the liver is burning excessive fat. Which, those excessive fats that are not quickly metabolized in the body have to be rid of via diarrhea. Hence, the diarrhea side effect is actually great for the patients because it is proof that the drug works. Commenting on the development, the CMO (Dr. Becky Taub) remarked,

These pivotal Phase 3 results demonstrate the potential for resmetirom to help patients achieve improvement in both the underlying steatohepatitis that drives this disease and the resulting fibrosis that is associated with progression to cirrhosis and its complications. The topline data also reinforce our confidence in the safety and tolerability profile of resmetirom. We believe the Phase 3 MAESTRO clinical development program … provides a strong foundation for our new drug application and the potential accelerated approval of resmetirom for the treatment of non-cirrhotic NASH with liver fibrosis.

NASH pathology

Figure 6: Great safety profile

Capturing A Monopoly Market

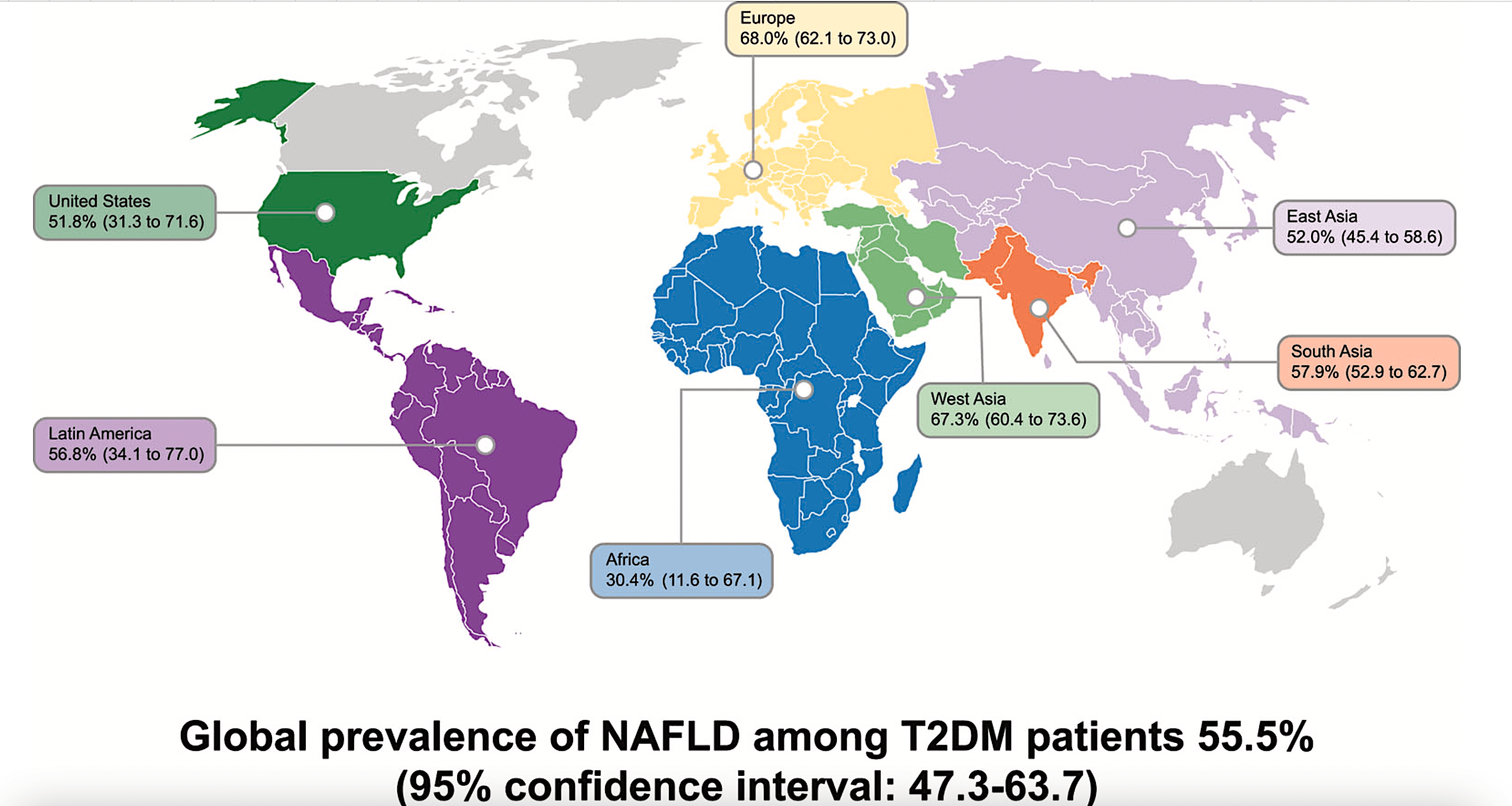

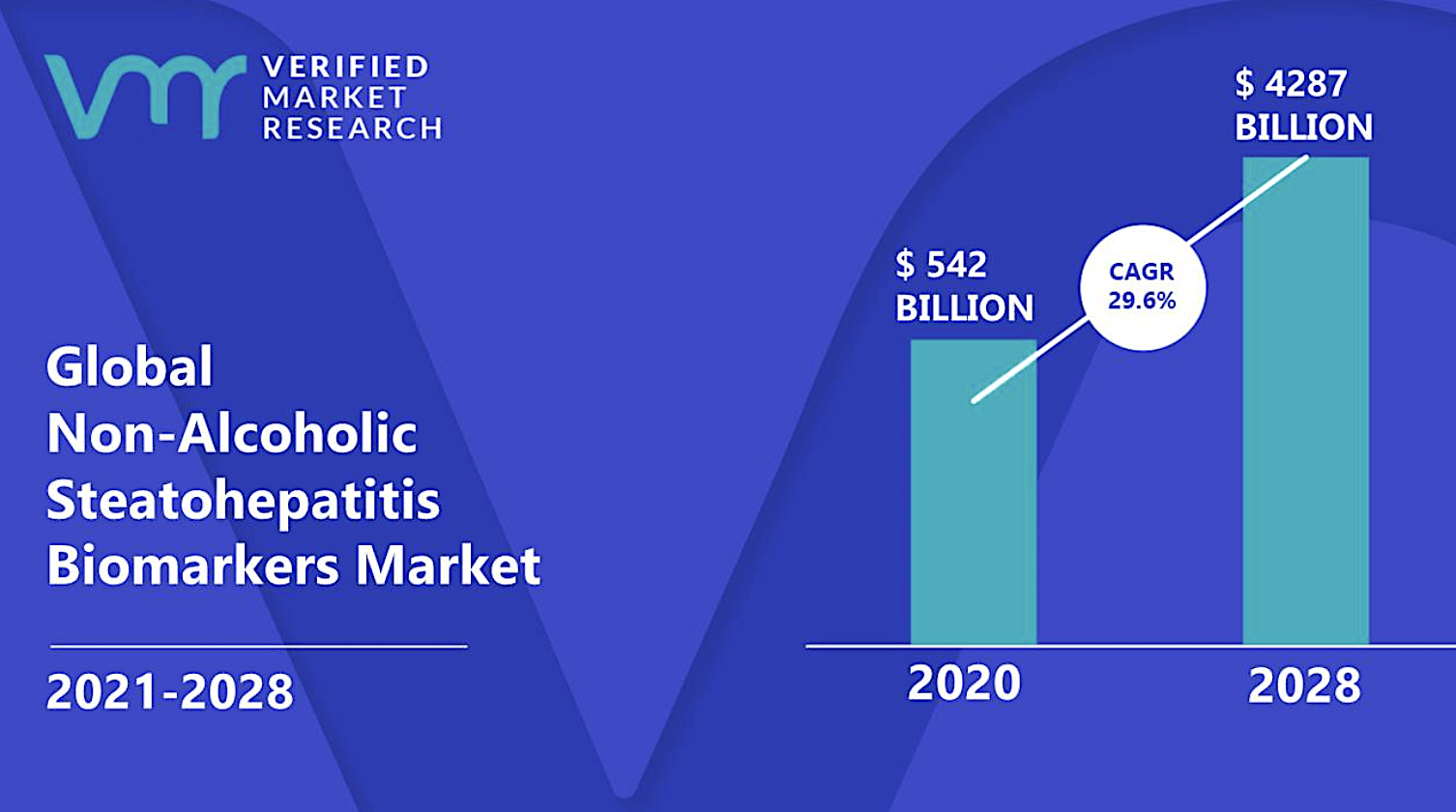

Though BioSpace valued the global NASH market at $180B, other sources like Verified Market Research have it a $542B in 2020. Growing at 29.6% CAGR, this market is expected to reach $4,287B. While the figure seems to be astronomical, you can imagine that NASH is as big as the obesity/diabetes market. After all, those conditions tend to occur together.

ScienceDirect

Figure 7: High global prevalence of NAFLD/NASH

If you imagine Resme capturing 1% of this market, that’ll be at least $5.4B in annual revenues. As you know, I tend to err on the conservative estimate. The most realistic scenario is that Resme would enjoy windfall profits just like how Moderna’s COVID vaccines are able to generate tens of billions of dollars. After all, their molecules are the early ones entering the untapped COVID market. Simply put, there is nothing more profitable than operating a monopoly market.

Verified Market Research

Figure 8: Estimated global NASH market

Financial Assessment

Just as you would get an annual physical for your well-being, it’s important to check the financial health of your stock. For instance, your health is affected by “blood flow” as your stock’s viability is dependent on the “cash flow.” With that in mind, I’ll analyze the 3Q2022 earnings report for the period that ended on September 30.

Given that I already went into great detail about the financials in the previous article, I’ll briefly go over the highlights here. Like other developmental-stage companies, Madrigal has yet to generate any revenue. The research and development (i.e., R&D) logged in at $68.2M compared to $54.8M for last year. For the bottom line, there were $81.1M ($4.75 per share) net losses versus $63.1M ($3.70 per share) declines.

Of the balance sheet, there were $153.2M in cash, equivalents, and investments. On top of the $300M recent capital raise today, the cash position is increased to over $453.2M. Against the $80.4M quarterly OpEx, there should be adequate capital to fund operations into 2Q204. Simply put, the capital position is now extremely robust.

Potential Risks

Since investment research is an imperfect science, there are always risks associated with an investment regardless of its strength. At this point in its growth cycle, the most imperative concern for Madrigal is whether Resme would gain approval for NASH by 2H next year. Though this is a concern, the said drug already cleared the most important data hurdle to approval. That aside, the other risk is that the safety study MASTRO-OLE might post subpar data. Notwithstanding, that is an extremely small risk.

Conclusion

In all, I upgraded my strong buy recommendation on Madrigal with a 5/5 stars rating. Madrigal is a stellar growth biotech story, one with tremendous innovation success. Though the pipeline is extremely narrow with tremendous risk, Madrigal cleared the extremely high hurdle to success recently. Precisely speaking, the early Christmas present came in the form of positive Phase 3 (MAESTR0-NASH) NASH data. Coupled with the prior strong MAESTRO-NAFLD-1 results, Resme is poised to become the first therapeutic approved for NASH. Due to its upcoming entry into a monopoly market, you can anticipate windfall profits for Resme. As such, you can expect Madrigal shares to rally further. In the coming years, it’s quite likely that Madrigal would become a giant of the future.

Be the first to comment