Walter Bibikow

Macerich (NYSE:MAC) just reported its fourth quarter and full year 2022 results, and we have to admit we were a little disappointed. It appears the market was not completely pleased with the results either, as shares traded down by several percentage points. It is not that the results were bad, but we were expecting the recovery to accelerate, and instead what we got was a relatively small improvement. For example, tenant sales were flat in the fourth quarter versus Q4 of 2021. Same center NOI growth of 2% in the fourth quarter was basically the same as that of the fourth quarter of 2021. This is a slowdown in NOI growth from the 7%+ levels achieved over the last 2 years. This is despite occupancy continuing to recover nicely. Unfortunately operational improvements are being counteracted by operating expenses that are growing, and higher interest expenses. You can read our previous coverage here and here.

This is not to say things are not improving, since there are several positives. For instance, trailing 12-month leasing spreads remained positive at 4%, even though it’s down from 6.6% last quarter. Also the company is making good progress on upcoming lease expirations, with commitments on 52% of its 2023 expiry square footage, and with another 27% in the letter of intent stage. The company sounds convinced that as they restore occupancy it will be easier to generate higher leasing spreads.

Q4 Results

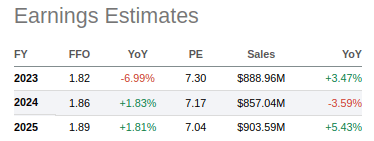

FFO per share for the quarter was $0.53 and $1.96 for 2022. The quarterly result was equivalent to FFO per share during the fourth quarter of 2021, again showing that FFO recovering is stalling a bit. Clearly some of the operational improvements are being counteracted by rising interest costs. Initial guidance for 2023 FFO is estimated in the range of $1.75 to $1.85 per share. It is disappointing to hear that FFO per share for 2023 is expected to be below that of 2022, but a big part of the reason is a $0.21 per share increase in estimated interest expense due to rising rates. Most of the FFO is expected in the fourth quarter, with Q1 and Q2 expected to be relatively weak.

There were some bright spots in the report as well. We particularly like that the company continues to make good progress in occupancy, which ended the year at 92.6%. That was a 50 basis point sequential improvement over the third quarter of 2022. It is getting closer to the pre-Covid level of ~94%, and the company believes it might get there by the fourth quarter. The company also continues to make progress converting temporary space into permanent leases, but temporary space remains elevated at about 7.5%. Another positive is that bankruptcies continue to be at a record low, leasing interest continues to be strong from a wide range of categories, and the company reported that retailers are starting to compete more for space in their higher quality centers, which bodes well for future leasing spreads.

The company has a big leasing pipeline that is expected to contribute meaningfully to NOI growth, but much of it will not have a cash impact until 2024 and 2025. This is because big leases such as the Arte Museum will take time to be ready to start operating and paying rent, so the benefit in 2023 is expected to be relatively small. Still, it is good to hear that roughly $55 million of NOI is expected to come online in the next couple of years, and that physical occupancy will start to pick up in the latter half of the year, setting up a good backdrop for cash flow and NOI growth in 2024. In other words, things are improving, but at a slower pace than many of us would like, and we will have to remain patient for some of these positives to start being reflected in FFO numbers.

Financing

Perhaps the best piece of news shared by the company is that the debt markets are opening to refinance their high-quality properties, and that they are getting deals done. This has been a big investor concern, as the company has meaningful amounts of debt that will have to be refinanced soon.

Some of the examples shared by the company include a 3 year extension of the $300 million CMBS loan on Santa Monica Place, which has a floating rate of LIBOR plus 1.48%. It also completed a $370 million 5 year refinance of the Green Acres Commons, with a fixed interest rate of 5.9%. The company’s joint venture that owns Scottsdale Fashion Square is also in the process of refinancing the existing $405 million mortgage loan and is expected to generate roughly $150 million of incremental liquidity to the company.

The company finished the year with $512 million of available liquidity and a net debt to forward EBITDA, excluding leasing costs, of 8.8x. This is still above the company’s target, and there was a mention during the earnings call of a potential small equity raise. This is what CFO Scott Kingsmore had to say regarding a question about the potential equity raise and getting back to their target leverage ratio:

We — if you look at that chart that we talked about on our Investor Day, we did have a placeholder for a nominal equity raise. That doesn’t mean we’re committed to raising equity at $13 a share. But that was a placeholder in there, if you look at the footnotes. In addition, NOI growth certainly is an important component to us, ultimately getting our target leverage below 8% — or excuse me, 8x over the course of the next year or 2. So those are the primary factors. We think that we’re certainly headed down the right path of achieving reasonable NOI and EBITDA growth between now and next year.

As we believe shares remain significantly undervalued, we believe it is in the best interest of investors that the company refrain from issuing shares at current prices.

Valuation

MAC shares remain very cheap, trading with a well-covered ~5% dividend yield, and based on the 2023 FFO guidance, they are currently trading with a forward P/FFO of ~7.3x. Needless to say, this is a cheap valuation for a REIT that is showing operational improvements, even if some of the operational improvements are being counteracted by the headwinds of increased operating costs and higher interest expenses. Still, we believe investors should look at the big picture. That is, things look set to continue improving operationally for the next 2-3 years and the valuation remains significantly below historical averages. If we look at analyst estimates, they are forecasting small improvements in the FFO per share for the next two years, but what it is critical to remember is that the ~7x multiple is roughly half of the historical average. Once the company reaches its ~8x leverage target and has restored occupancy to pre-Covid levels, we believe it will start raising the dividend in a more meaningful way.

Seeking Alpha

Risks

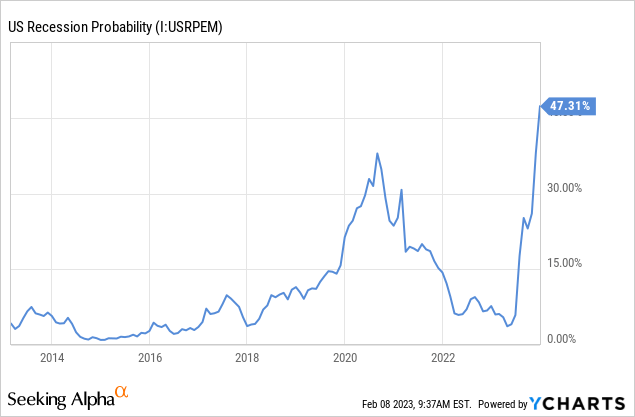

The company is still in the process of recovering from the enormous impact dealt by the Covid pandemic. Should another adverse event like that occur, it would certainly put the recovery in jeopardy and the share prices could decline very significantly. At this point the highest probability risk is probably that of a recession in 2023.

So far, the company continues to report low bankruptcies among its tenants, and a healthy leasing appetite, but that could change should the economy suffer a significant downturn. Some models are predicting with very high probability a recession in 2023, such as the Estrella Mishkin model.

Conclusion

We have mixed feelings about Macerich’s fourth quarter results. We were expecting faster progress on the recovery than what we got. Still, the company continues to make progress, and the operational recovery has not stopped, even if it is slower than we would like. Things to look forward include occupancy potentially recovering to the ~94% level by year end, and significant NOI scheduled to come online in 2024 and 2025. In the meantime the company will see some of the benefits from the operational improvements counteracted by higher operating expenses, and particularly higher interest expenses. When looking at the big picture, though, we believe shares remain significantly undervalued at a ~7x FFO multiple given the quality of many of Macerich’s properties.

Be the first to comment