RHJ/iStock via Getty Images

General Overview

In my last review of Lynas Rare Earths Limited (OTCPK:LYSCF), Australia’s leading exotic minerals player, I posited that geopolitical changes, technological shifts, and the electrification of the world grid provided the perfect storm for equity upside. Over the past quarter, there has been no seismic upside explosion in the equity.

Yet underlying themes remain – a virtual monopoly of rare earth gathering and processing technologies led by China, a requirement for Western allies to diversify the supply chain and hence sponsor project initiatives, and continued demand driven by advances in technology for exotic battery minerals.

Trading View

Over the past 6 months, Lynas (+5.86%) has tended to marginally outperform the S&P 500 (+1.43%).

That narrative remains. While this long-term trend may take time to bed-in, progress is being made by the Australian pioneering rare earths player at both its Kalgoorlie industrial complex and its Malaysian processing hub. Let us take the opportunity to detail those advancements made over the past several months.

Still bullish.

Lynas Rare Earths

Year-on-year revenue performance – Lynas Rare Earths.

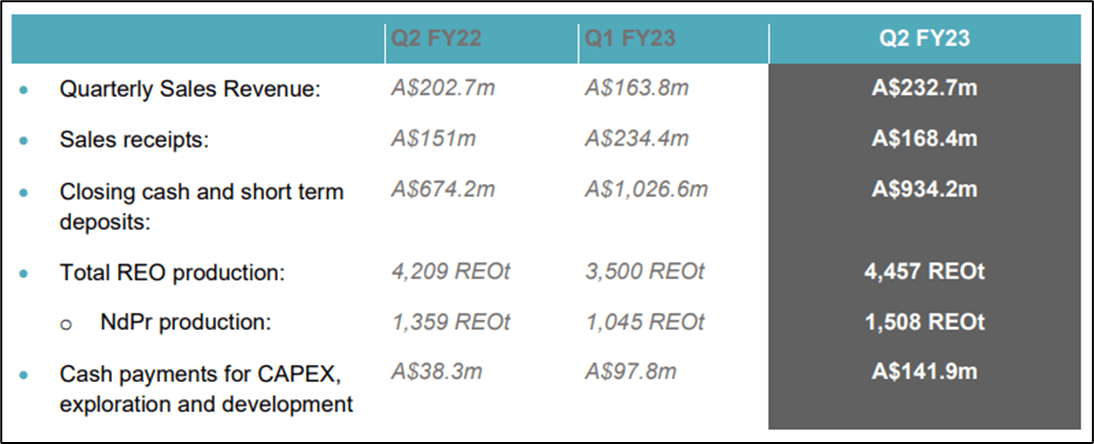

Latest Results – Key Highlights & Financials

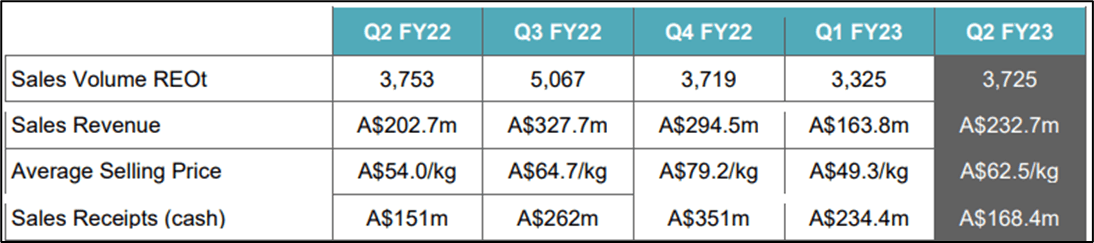

Results improved in the last quarter following recovery from water supply disruptions that had previously hampered output. Lynas Rare Earths’ top line improved, with the company posting A $232M during the quarter, roughly a $30M improvement (+13%) over the same period one year earlier.

Revenues hit A $168M, underscoring late quarter deliveries along with trade terms the company holds with its customers. Specialty products such as mixed heavy rare earths, lanthanum and Cerium, helped maintain robust average selling prices despite a flattish market. During the period, China Domestic prices for NdPr remained at US $83 per kilo.

The late January Lunar New Year in China was the likely catalyst for an uptick in prices during December. Over the quarter, the company posted production of ~1,500t of NdPr and total REO production of 4,457t, which was an increase on a year-over-year basis.

Lynas Rare Earths

Aerial photo of run of mine stockpiles with Campaign 4-1 ores.

Mining Campaign 4-1 continued at the Mount Weld operation, with ore being moved from the open cut mine to run of mine stockpiles. Upstream ore processing efficiencies allowed the site to deliver record volume of REO concentrate, translating into a ~5% improvement.

This was achieved due to characteristics of current ore body, combined with changes to ore processing parameters. Additionally, the lanthanide concentrate stockpile continued to make headway at the Kalgoorlie Rare Earth Processing facility. This stockpile is on schedule, as the operation juggles increased demand from the Malaysia facility and inventory build-up from the Kalgoorlie startup.

Lynas Malaysia benefited from capital dedicated to plant improvements in receiving and processing of rare earths from its sister Kalgoorlie processing facility. Construction works for a permanent disposal facility in Malaysia is also developing. These activities culminated in cash outflows underpinning project progress achieved thus far.

The Kalgoorlie Rare Earths Processing facility has witnessed the accomplishment of several project milestones, including construction of evaporation pond and embankments, kiln lining, and the installation of a kiln generator.

Construction works for workshops, warehousing and maintenance offices have also made sound progress. Pace is picking up on the construction front – operational leadership is now based at site, and close-out of several engineering work packages means the site is slowly taking shape.

Lynas Rare Earths

Several engineering work packages have been completed including soda ash silo, MgO outer concrete tank walls, and silo structures.

The Mount Weld project is developing nicely, with meaningful progress in detailed engineering and design, procurement of long lead items and award of select work packages. Over the past month, bulk earthworks have been undertaken by the dedicated contractor.

Additionally, the Chair of the EPA (Environmental Protection Agency) and the Director of EPA Services made a whirlwind tour to inspect progress. During this time, a briefing on current operations was completed and project progress was showcased.

By the end of October 2022, one of Lynas Rare Earths’ senior creditors – JARE – signed a letter of agreement deferring US $11.5M in historic interest payments until mid-2023, with no interest-bearing penalties. This emphasized the support the project is generating, particularly from Australian allies such as the United States.

Lynas Rare Earths

Average selling prices generated – Lynas Rare Earths.

Product demand remains solid, with the company continuing to focus on productivity improvements to meet a bloated order books. Request for information and pricing continues to be received from new perspective customers, particularly from automotive original equipment manufacturers and magnet manufacturing projects outside China.

Koyfin

Price action for the Australian rare earths’ miner has been positive over the past 6 months.

From a financial perspective, 2024 is likely to be the year we see meaningful change in company revenue streams and cash flows. As project progress at both at its Kalgoorlie mine site and its Malaysian industrial hub continues, capacity will come online. Revenues are expected to increase by roughly 30% by FY 2024.

In summary, the outlook for Lynas following a spate of earnings remains positive. Strong progress is being made on capex projects, and rare earth prices continue to provide a supportive environment.

Risk

State-sponsored subsidies provide somewhat of a hard floor to the commodity group Lynas has built its business around. That means despite a sapping of aggregate demand driven by a forthcoming 2023 recession, the rare earth industry is likely to thrive.

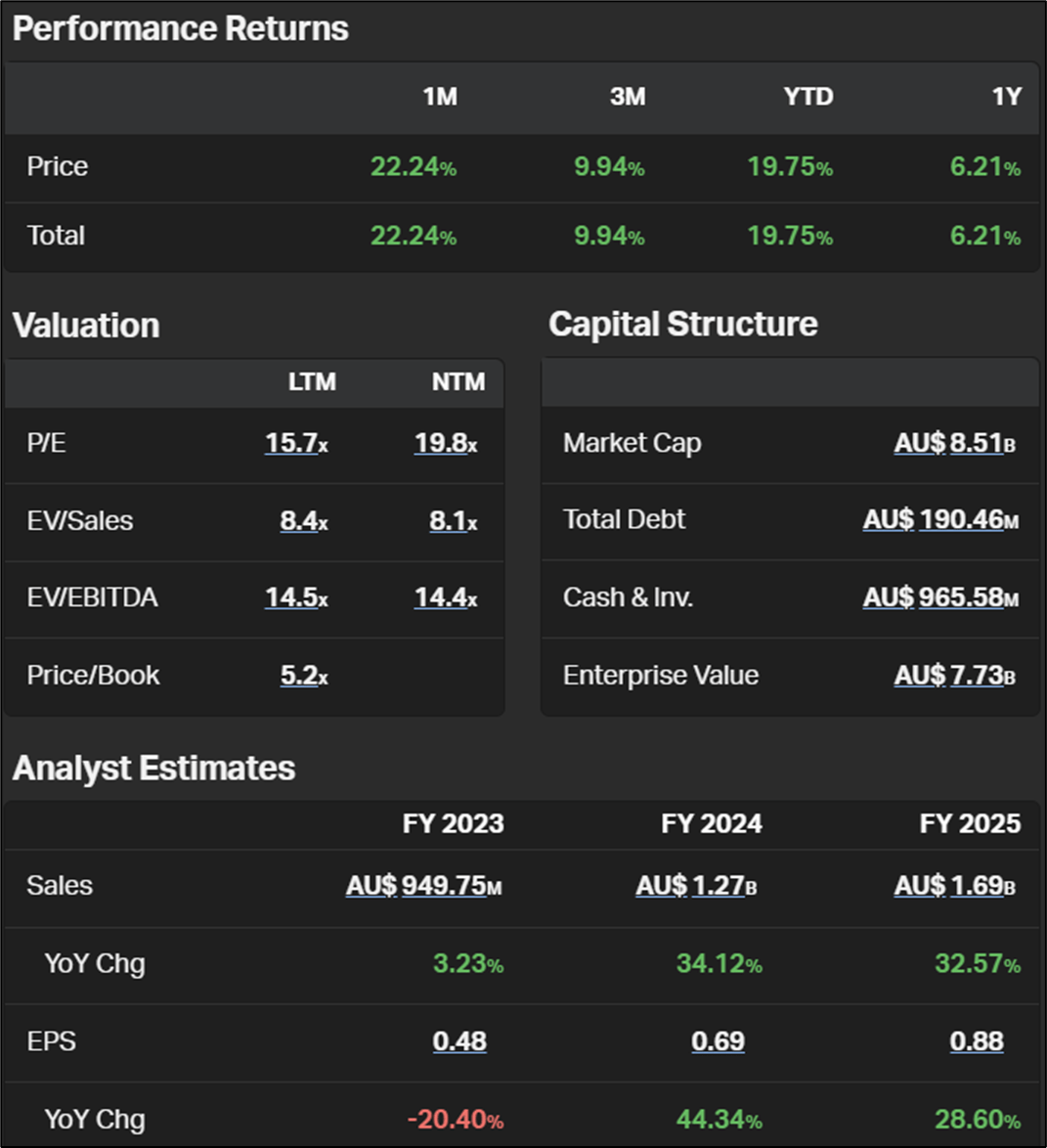

The stock’s recent run means it has an even loftier valuation – at around 19.8x forward earnings. World equity markets have opened up with a boom in 2023, which will likely spur additional inflation only to be met by renewed sovereign bank hawkishness.

Cranking up the monetary tightening narrative would surely impact short-term equity prices and possibly also have an effect on the company’s sources of funding.

Overall, while this is a risky mining venture – it remains supported by Western allies looking to decouple from China and a transition to clean energy that is not likely to deteriorate anytime soon.

Key Takeaways

In keeping with its project commitments, Lynas Rare Earths continues to make inroads into its Mount Weld mining operation along with sound progress at its Malaysian industrial hub.

That is why I am bullish on the firm’s outlook – even at 19x forward earnings over the next 12 months, a support price environment is likely to see rapid growth (~+60% by FY25) and additional capacity come online. All in, I rate Lynas Rare Earths Limited stock presently as a buy.

Capital continues to be prudently allocated while the same geo-political tensions remain – state sponsored development of the rare earths industry is an attempt to decouple from dependency on Chinese supply.

This theme, along with a clean energy transition, remain the catalysts for Lynas Rare Earths Limited to deliver lasting long-term value.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment