Man weighing whether to sell his last LUMN share to buy a bulb. JackF/iStock via Getty Images

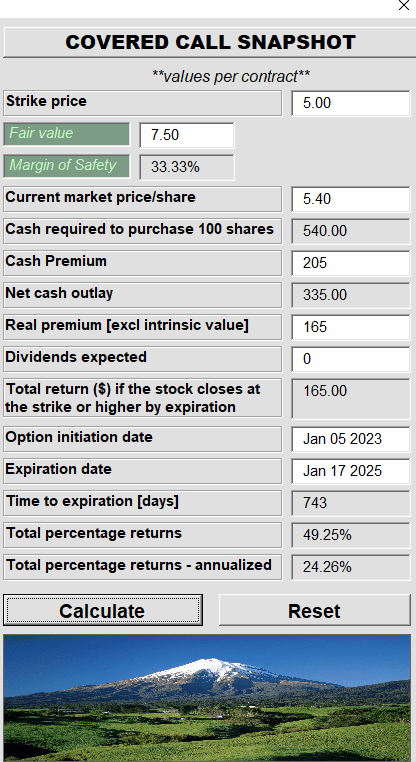

On every trade, you either become wealthier or you become smarter. Never both. In the case of Lumen Technologies, Inc. (NYSE:LUMN) while we want to take credit for our extreme patience before entertaining a long side play, the recent results certainly made us dial back the optimism. When we last wrote about it we came off the sidelines and gave it a cautious buy rating, but with the caveat that this was best played via options. Our suggested trade was a covered call with a higher buffer and a strong return profile should LUMN stay over $5.00.

CC Trade Idea From Previous Article

The company announced its Q4-2022 results yesterday and we took the opportunity to update our thesis.

Let’s see how things shook out.

I felt a great disturbance in the Force, as if millions of voices suddenly cried out in terror and were suddenly silenced. I fear LUMN has just reported.

Source: Star Wars, First Draft

Q4-2022

Q4-2022 was the first quarter with Kate Jackson at the helm and she certainly had her hands full.

LUMN Q4-2022 Presentation

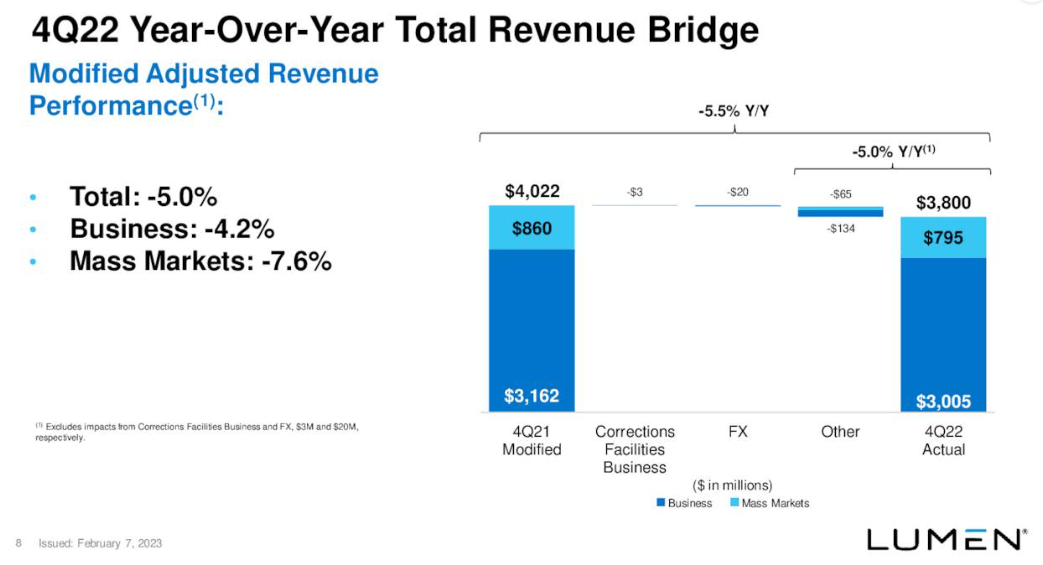

The revenue beat estimates by a smidge, even though it declined by 5.5% year over year. Keep in mind the comparative here is the adjusted revenue base from 2021 which strips out divestures to make it an apples to apples comparison.

LUMN Q4-2022 Presentation

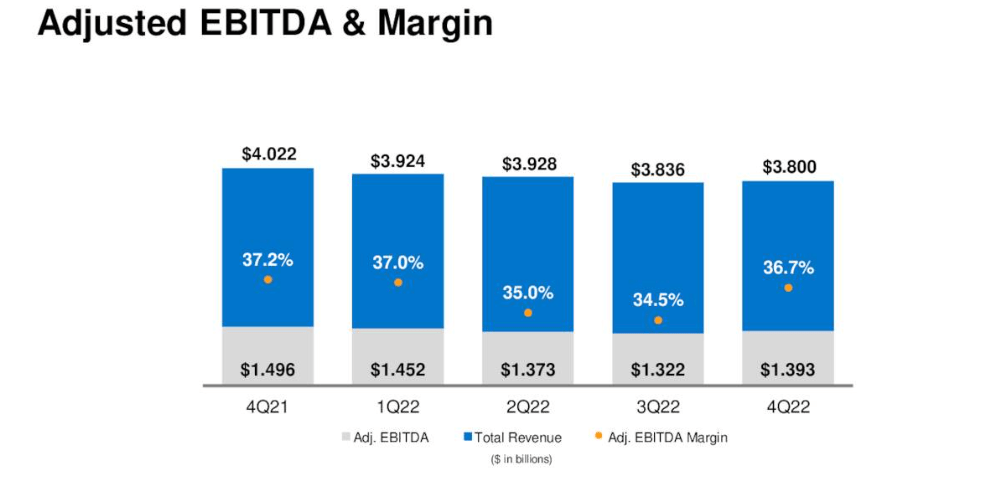

LUMN’s actual revenues in Q4-2021 were $4.85 billion and not the $4.022 shown above. That number goes to show just how rapidly LUMN the company (not just the stock price) has shrunk. GAAP earnings were influenced by a non-cash goodwill impairment charge of $3.271 billion but the more watched metrics, adjusted EBITDA ($6.858 billion) and free cash flow ($2.260 billion), did ok. Both metrics held up well despite LUMN going in full reverse with revenues. Generally, reverse economies of scale work to destroy margins on the way down but adjusted EBITDA margin continued to be impressive.

LUMN Q4-2022 Presentation

To some extent this was helped with LUMN selling off its lower margin businesses. Nonetheless that 36.7% number in a high inflation environment was excellent.

2023 Guidance

Our key reason to consider taking on this risky investment, even with the benefit of covered calls, was that we would see some stabilization in the base business. That hope was dashed. The adjusted EBITDA guidance was stomach churning.

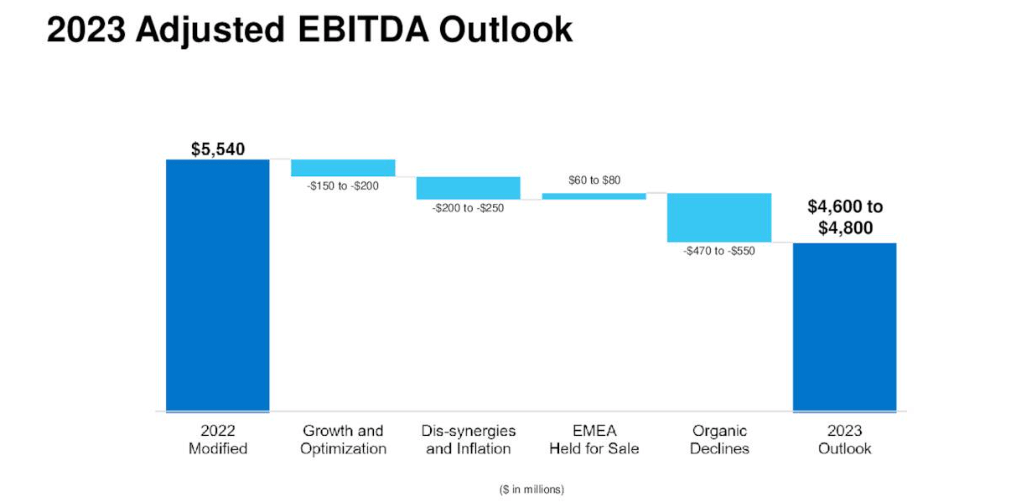

LUMN Q4-2022 Presentation

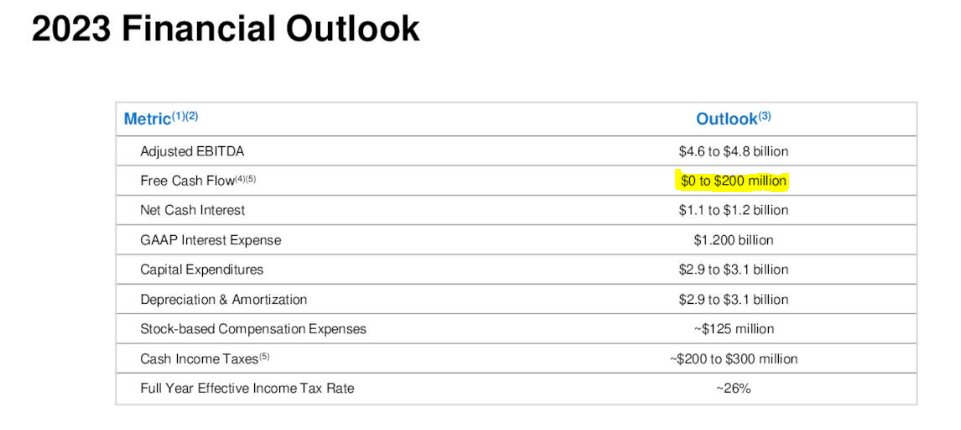

Sure a small part is due to the planned EMEA held for sale component and we think the EV to EBITDA multiples on that sale will do the company good. But the organic decline of $510 million (midpoint) was pretty bad. Interestingly enough, LUMN had two other categories for the adjusted EBITDA decline which added up to $400 million (midpoints). This is of course the problem that LUMN had avoided so far. Reverse economies of scale (dis-synergies in slide above). We would wager, “growth and optimization” is the same issue under a different name. Whichever way you slice it, this was far worse than our expectations and under the expectations of practically everyone on Wall Street. With the abysmal $4.7 billion of adjusted EBITDA things get even murkier as you move on to free cash flow. $100 million of free cash flow in 2023 after delivering $2.26 billion in 2022 is quite a shock.

LUMN Q4-2022 Presentation

The triple whammy here comes as revenues will fall more than expected, margins will drop at a faster clip and capital expenditures will rise to a $3.0 billion run rate. On top of that the cash income taxes shown above exclude the amounts payable for the recent transactions.

LUMN Q4-2022 Presentation

Leverage will rise as 2023 progresses and older quarters roll off.

Our expected estimated net debt reflects our utilizing cash on hand to settle the tax obligations related to the divestitures we closed in 2022, which totals $900 million to $1 billion. We anticipate paying these taxes during the first half of 2023. Given the investments that Kate identified, we anticipate leverage to rise to between 4.0 to 4.3x in the near-term. We expect leverage to peak as we approach year-end 2023 and decline thereafter.

Source: LUMN Q4-2022 Conference Call Transcript

This will be a tough setup for the bulls to defend and if a recession does materialize in 12 months, things get even worse.

Verdict

Was that a kitchen sink quarter? New CEOs are known to reset expectations and allow themselves some breathing room to deliver. On the conference call management highlighted how it would take them two years from here to start seeing growth.

As Kate discussed, over the next couple of years, we will be aggressively investing both OpEx and CapEx to position ourselves for long-term sustained success. The focus of these investments will be to enable growth, improve customer experience and simplify how we operate. These investments will include a number of items such as digitization, ERP, Network as a Service and IT simplification. These growth and optimization investments outlined in our EBITDA guidance waterfall chart are expected to total $150 million to $200 million. Importantly, we expect our revenue and EBITDA to stabilize as we exit 2024 with growth thereafter.

Source: LUMN Q4-2022 Conference Call Transcript

Perhaps it starts sooner, but these numbers are scary nonetheless. What makes this even more perplexing is that LUMN actually bought back shares during the past three months.

Repurchased 33 million shares of common stock for a total purchase price of $200 million.

Source: LUMN Q4-2022 Press Release

They must have some vision into that 2023 outlook as they frolicked around repurchasing shares at an average price of $6.06. That makes no sense. This is cash that they should have kept on hand. Especially since their bonds have still not been given the green light.

Based on everything we have seen here, we have to go the old quote route. When the facts change, you change your mind. We were wrong here. Not just slightly wrong, but really, really wrong.

The couple of pieces of solace here are the fact that we were not wrong for long and the suggested covered call approach would have dampened losses significantly. Nonetheless this was a horrible call and we failed at every level. We are downgrading this to a hold. We congratulate the vocal bears on this stock. They were not writing “hit pieces”, they were not biased, they were not “talking their book” as many commenters implied. They were just right and that must feel glorious today.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Be the first to comment