ThitareeSarmkasat

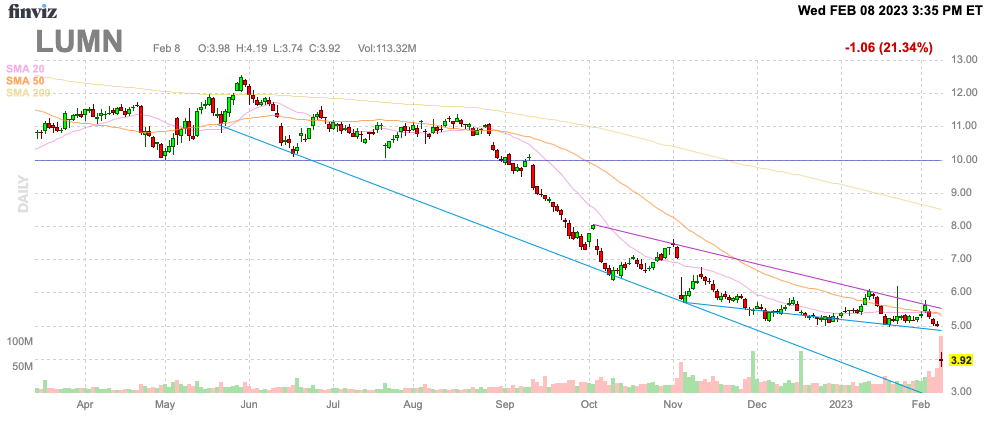

Lumen Technologies, Inc. (NYSE:LUMN) plunged 20% following their highly disappointing Q4 2022 earnings report. The telecommunications company got a new CEO and kitchen-sinked the 2023 guidance, while continuing the disastrous process of constantly cutting business versus building on the current profit base. My investment thesis is now Bearish on Lumen stock in a rare scenario where a beaten-down stock isn’t one to buy on dips.

Source: Finviz

Another Painful Rebuild

Kate Johnson took over the CEO role on November 7 following a tenure where Jeff Storey spent years working to transform the former CenturyLink business. The former CEO spent considerable effort removing low-calorie revenues to focus on the key growth drivers of the business.

Lumen Tech. just completed a couple of transformative divestitures where the company acquired large sums of cash to move the business focus to large enterprises and away from consumers. Now, the new CEO, Kate Johnson, came out in her first earnings report and reported plans for more streamlining when the telecom company is running out of sales and positive adjusted EBITDA to cut.

The telecom had reported some solid modified adjusted EBITDA over the last 3 quarters in a sign business was stabilizing as follows:

- Q4’22 – $1,393M

- Q3’22 – $1,322M

- Q2’22 – $1,373M.

On the Q4’22 earnings call, CEO Kate Johnson discussed another rebuild of the business (emphasis added):

Simplification will come in two major forms. First, we will focus on doing fewer things better. That means shutting down subscale or non-accretive businesses, which includes no longer selling products or services that don’t directly enhance our value to customers or benefit Lumen and its shareholders.

Lumen can’t afford to cut any more businesses after LUMN stock has slumped below $5 on the dividend cut and transitioned to stock buybacks. Instead, the company shocked the market with this 2023 adjusted EBITDA outlook.

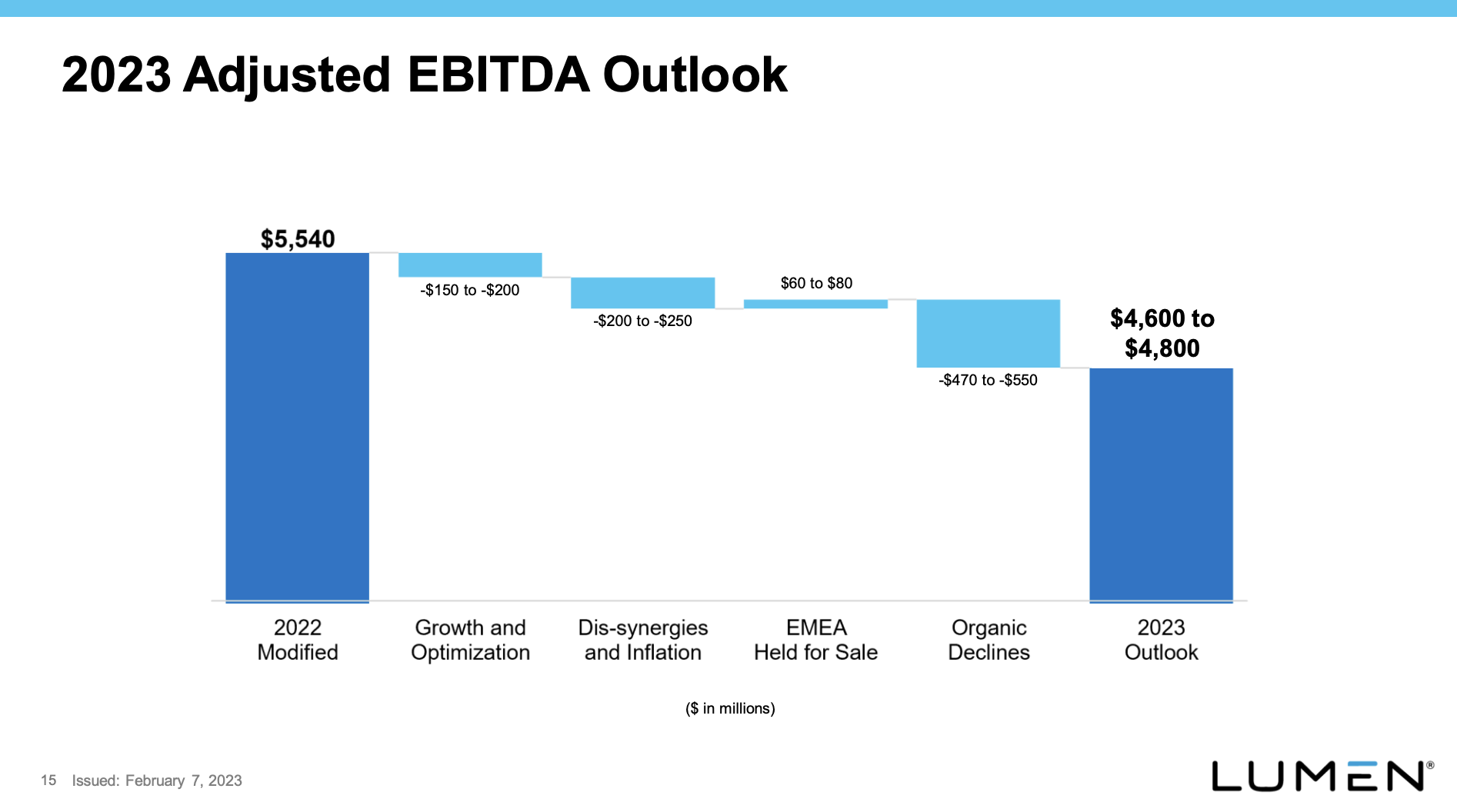

Source: Lumen Q4’22 presentation

The new guidance has Lumen getting hit by a whole host of financial problems in 2023, with adjusted EBITDA falling from a modified $5.54 billion in 2022 to only $4.7 billion, at the midpoint. The guidance for an ~$500 million organic decline is abysmal, and the company appears to be adding to this pain with growth investing costing up to $200 million in additional EBITDA on top of inflation impacting profits. The consensus analyst estimates were up at $5.15 billion in a sign of how minimal weakness was expected.

Even worse, the new CEO suggested the company would take up to 2 years to achieve just stability in revenues and EBITDA:

First, on EBITDA and CapEx, we are leaning into our growth and optimization priorities and Chris will provide financial details of these initiatives shortly. We believe these investments are critical to position Lumen for strong execution and scalable sustainable growth. And we expect revenue and EBITDA stability in less than 2 years.

Cash Flow Problems

The problem here is that no company with $20 billion in debt can afford to cut a business generating EBITDA profits for a replacement business that won’t stabilize for a couple of years. At the same time, Lumen Tech. plans to boost capital expenditures in 2023 to ~$3 billion.

Source: Lumen Q4’22 presentation

Again, the company could utilize some of the removed businesses to fund capital spending, but Lumen appears eager to pass on current cash flows to focus on potential new or expanded revenue streams down the road. Either way, Lumen no longer generates the positive free cash flows needed to repurchase shares on what once appeared a very cheap stock price below $5. In fact, the company faces a scenario now where missing financial targets leaves the company in a negative free cash flow position and requires a pullback on capital spending.

Lumen Tech. guided to 2023 free cash flows of $0 to $200 million. The company still spends up to $1.2 billion on interest expenses and the combination with $3.0 billion in capital spending leads to $4.2 billion in cash spending. Lumen only guided to adjusted EBITDA of $4.7 billion leaving limited cash from operations to cover these outflows considering the telecom still has cash income taxes of ~$250 million.

The problem facing the company is that Lumen used to have a business generating up to $2 billion in free cash flow and now such cash flows are next to breakeven after divesting several businesses. Also, the divestiture of the EMEA business in the next year will eliminate another $70 million from current adjusted EBITDA targets leading to the constant downward trend.

Takeaway

The key investor takeaway is that selling stocks based on kitchen-sink quarters can end up leaving a lot of profits on the table. Some times, the new management team aggressively lowballs guidance making for an easy hurdle.

The problem is this guidance is that Lumen Technologies, Inc. is on a dangerous path approaching negative free cash flows. Even worse, Lumen Technologies, Inc. was supposed to aggressively purchase cheap shares, and the original $200 million purchase was a waste of money, with this guidance suggesting management is out of touch with their financial reality.

Investors should dump Lumen Technologies, Inc. stock and watch from the sidelines.

Be the first to comment