hapabapa/iStock Editorial via Getty Images

Introduction

Lululemon Athletica Inc. (NASDAQ:LULU) stock fell 9% on Jan. 9, 2023 after the company updated its Q4 guidance with mixed forecasts. LULU raised the target range of their revenue to $2.66Bn-$2.7Bn billion from $2.605Bn-$2.655Bn. The company also narrowed their earnings per share range to $4.22-$4.27, which remained in line with previous guidance, while also reducing the gross margin target range by 115bps given extra discounting in the period due to slower retail sales in the holiday season. LULU provided these figures ahead of the ICR Conference, which is scheduled to take place in Orlando, FL from Jan.9-Jan.11, 2023. After reviewing the updated figures, I am comfortable with the progress LULU continues to make, and I re-iterate my previous Buy rating, while updating my price target to $360 given the broader market dynamics.

Implications from Updated Guidance

While initial reactions from investors were negative, I don’t foresee these results to materially stump the operational momentum that LULU enjoys. The company is yet again on pace to record another blockbuster revenue increase of 25-27% and the company continues to be a top performer among peers, even given a tough 2022. The long term growth plan remains intact, and the earnings range remains within the previously guided totals. It was shocking to see how much the gross margin forecast, which did decline, impacted the stock price. Management was explicit in highlighting that SG&A spend would be better leveraged to account for the dip, hence why the earnings range remained intact. Retail sales broadly struggled in the U.S. recently, while the company improved their revenue targets, which confirms brand strength remains a huge advantage for the firm. Overall, this update doesn’t change my opinion on LULU at all and represents another buying opportunity, similar to in the summer, when the stock dipped toward $260 a share. Before today’s drop, they were performing well versus peers over the past 6 months.

Seeking Alpha Quant Tool – 6M Performance

Model Shows Upside

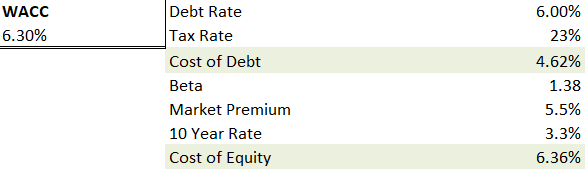

I anticipate positive momentum for LULU and expect the stock to bounce back over the medium to long term. The company’s cash position is stable and CAPEX spending seems controlled. The model forecasts a WACC of ~6.3%, with minor updates to the debt rate, the market premium and the 10-year paper. Given their strong quarterly performance, I don’t anticipate the cost of debt rising to 6% should they attempt to add leverage in this environment.

Author WACC Forecast

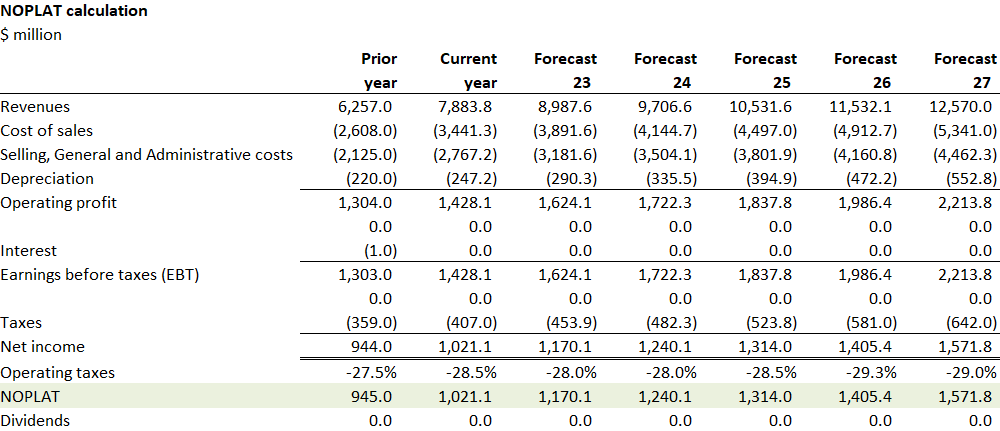

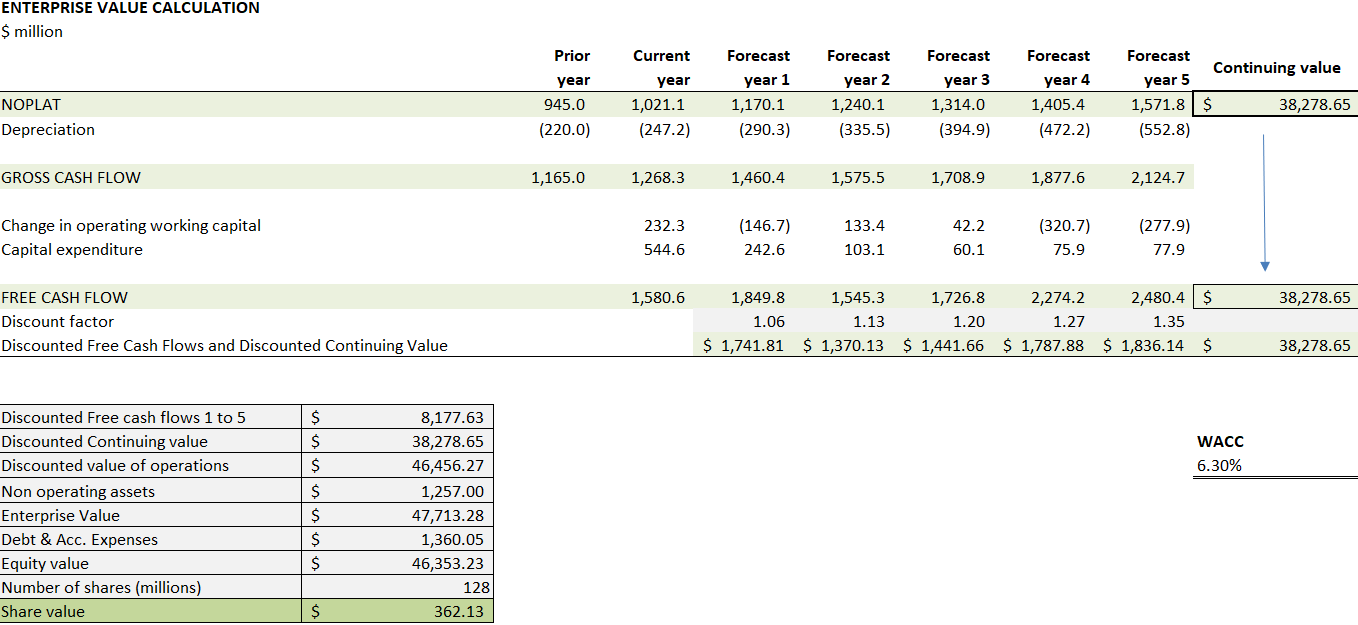

I forecast the continuing value above $38Bn, given a 26% revenue increase this year, in the mid-range of their new forecast, before reducing four future years to a blended 11% growth rate due to potential brand concentration and headwinds on international growth efforts. I project a continuing growth rate of ~3.5% & WACC of ~7.75%, given their ability to adapt in ever-changing environments. The model now projects revenue of $12.57Bn in 2026, just above their Power of Three revenue target of $12.5Bn. I now see COGS jumping about 100bps from my previous forecast and remaining in this range, given new guidance. I see SG&A staying flat at about 35% of revenue, as the company increases store counts and global advertising to achieve high growth. As operating profit almost doubles in five years, a $360 share price can be supported with reasonable fundamentals and a 2023 EV/EBITDA of 24.9.

Author Earnings Forecast Author EV & Share Price Forecast

Conclusion

LULU continues to be the leader in global large cap apparel. While the valuation remains a bit stretched, the current opportunity to buy the stock has value. Today’s press release didn’t change the outlook for the company, and the downward reaction is overblown. The company continues to increase revenue guidance, and earnings remain on track with their previously announced Power of Three targets for 2026. Management has proven that they have the foundation and track record to achieve success. LULU is worth a Buy at these levels, and I forecast a $360 share price within 18 months.

Be the first to comment