Robert Way

Lululemon Athletica Inc. (NASDAQ:LULU) stunned investors as it revised its FQ4’23 gross margins guidance downward, likely suggesting worse inventory adjustments. It also coincided with an upward revision in its revenue outlook, but investors likely focused on the impact of a higher promotional campaign across retailers during the recent holiday season.

LULU highlighted its confidence in improving supply chain dynamics in its FQ3’23 earnings commentary in early December. Therefore, the downshift in gross margins guidance from last year is certainly not welcomed by investors as they parse the company’s forward outlook.

Accordingly, Lululemon highlighted that its Q4 gross margin is likely to decline 100 bps (midpoint) YoY, compared to its previous outlook of a 15 bps (midpoint) adjustment.

As such, it indicates that LULU likely sees Q4 gross margin coming in at about 57.1%, against a gross margin of 58.1% a year ago. However, it’s still better than FQ3’s 55.9%, indicating the worst of its writedowns are likely over. Moreover, the company emphasized that it has OpEx levers to pull to mitigate the impact, with “general and administrative expenses 100 to 120 basis points compared to its previous expectation of 30 to 50 basis points of leverage.”

As such, we believe it’s credible for investors to consider that Lululemon remains in control of a potential recovery in FY24 as its China business improves further.

Notably, management narrowed its FQ4 adjusted EPS range to $4.22 to $4.27, implying midpoint guidance of about $4.245. It’s also just slightly below its previous guidance of $4.25. Hence, we believe investors’ focus is likely not on Q4 but on whether the outlook in FY23 could improve or deteriorate as macroeconomic conditions have worsened.

However, we believe there are reasons to be optimistic. Global container shipping spot rates have already collapsed through January, with a global freight index down to levels last seen in September 2020.

Furthermore, global supply chain headwinds that impacted retailers’ ability to forecast inventory accurately have also abated, as exports from Taiwan and Korea faltered, given the recessionary headwinds.

Therefore, we assessed that Lululemon’s supply chain dynamics and visibility should improve further through 2023.

Moreover, Lululemon has continued to perform admirably despite weaker consumer discretionary spending. Its upgraded revenue outlook suggests FQ4 revenue growth of nearly 26%, well above its previous guidance of 23.5%. Hence, Lululemon’s branding power and pricing leadership has continued to lift its outperformance against the industry.

Recent Mastercard (MA) estimates suggest that Lululemon seems to have outperformed its peers as “Online sales grew 10.6% year over year and in-store sales increased 6.8%” during the holiday season.

Moreover, investors should not understate the company’s solid performance in China despite its economic and consumer spending malaise over the past year. Back in December, management highlighted its confidence and momentum in China, despite its harsh COVID lockdowns, suggesting that LULU has been outperforming. CEO Calvin McDonald highlighted:

And on China, we remain very excited. Our new store openings, we opened 9 stores in [FQ3] in Mainland China. We have 88 now in [the] market. Their performance continues to exceed expectations. In markets where we don’t have constraints related to COVID, the store performance and online performance is very strong. So we remain very excited about the market. (Lululemon FQ3’22 earnings call)

As such, we believe Lululemon has significant branding power, coupled with its fast-growing direct-to-consumer segment that accounted for nearly 41.3% of FQ3’23 revenue (compared to FQ3’19’s 26.9%).

Therefore, we believe with China’s reopening from its COVID restrictions, LULU is well-poised to leverage its consumption recovery as China resumes its focus on meeting its GDP growth targets.

As such, we urge investors to evaluate the company’s commentary on its outlook and adjustments in its China market in 2023.

LULU is an expensive stock with an embedded growth premium in its valuation. Accordingly, LULU last traded at an NTM EBITDA of 17.2x, well above its peers’ median of 10.3x (according to S&P Cap IQ data).

Despite that, LULU trades at a discount against its 10Y average of 17.2x. As such, we believe Lululemon is at a critical juncture, as management needs to chart growth despite the threat of a global recession.

Investors need to assess whether China’s impending recovery after its COVID wave peaks could help mitigate the global macroeconomic headwinds. Moreover, consumer discretionary spending in the US could be hit further if the Fed keeps its rates high for an extended period. Therefore, it remains to be seen whether the US economy could dodge a recession. However, LULU’s growth premium suggests that it will not be immune if a recession turns out to be worse than expected, impacting forward earnings.

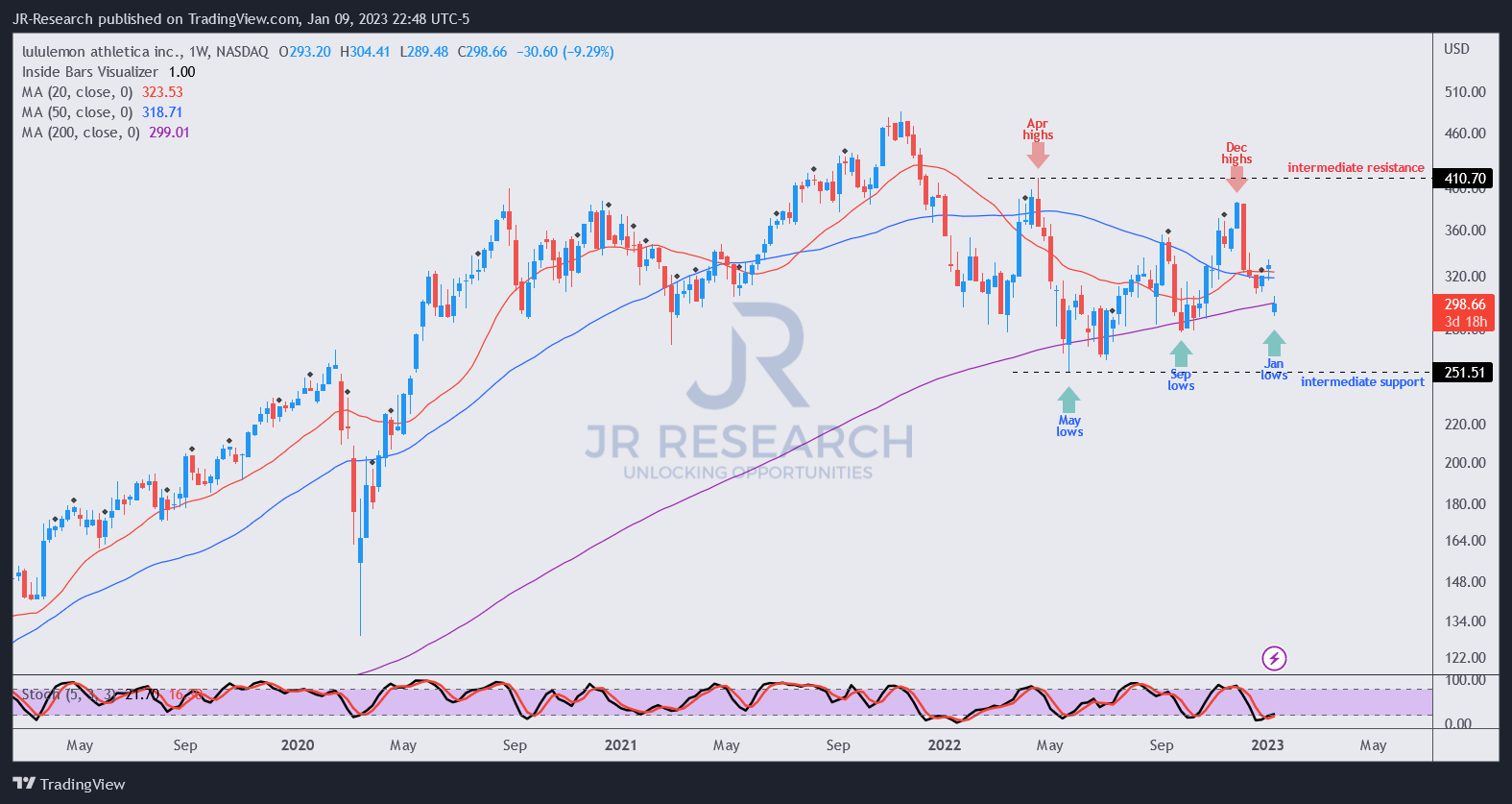

LULU price chart (weekly) (TradingView)

Still, we assessed that an opportunity to buy into LULU has likely appeared, given the gap-down from yesterday’s (January 9) pre-Q4 shocker.

We gleaned that LULU has fallen back to its 50-week moving average (blue line), which has undergirded its recovery from its May lows. As such, it implies that buyers have continued to support significant dips in its momentum, likely anticipating a recovery in 2023/24.

As highlighted earlier, LULU is well below its 10Y average, indicating that it’s no longer expensive. Hence, if the US or global economy could avert a disaster in 2023, this could turn out to be a savvy buyable bottom for long-term LULU investors.

Rating: Buy (Revise from Hold).

Be the first to comment