Looking for monthly income? LTC Properties (LTC) is a Healthcare REIT which pays $.19/month.

Like most other equities, LTC has had a rough time of it in the latest market pullback, falling from the high $40s, down to the mid-$20s:

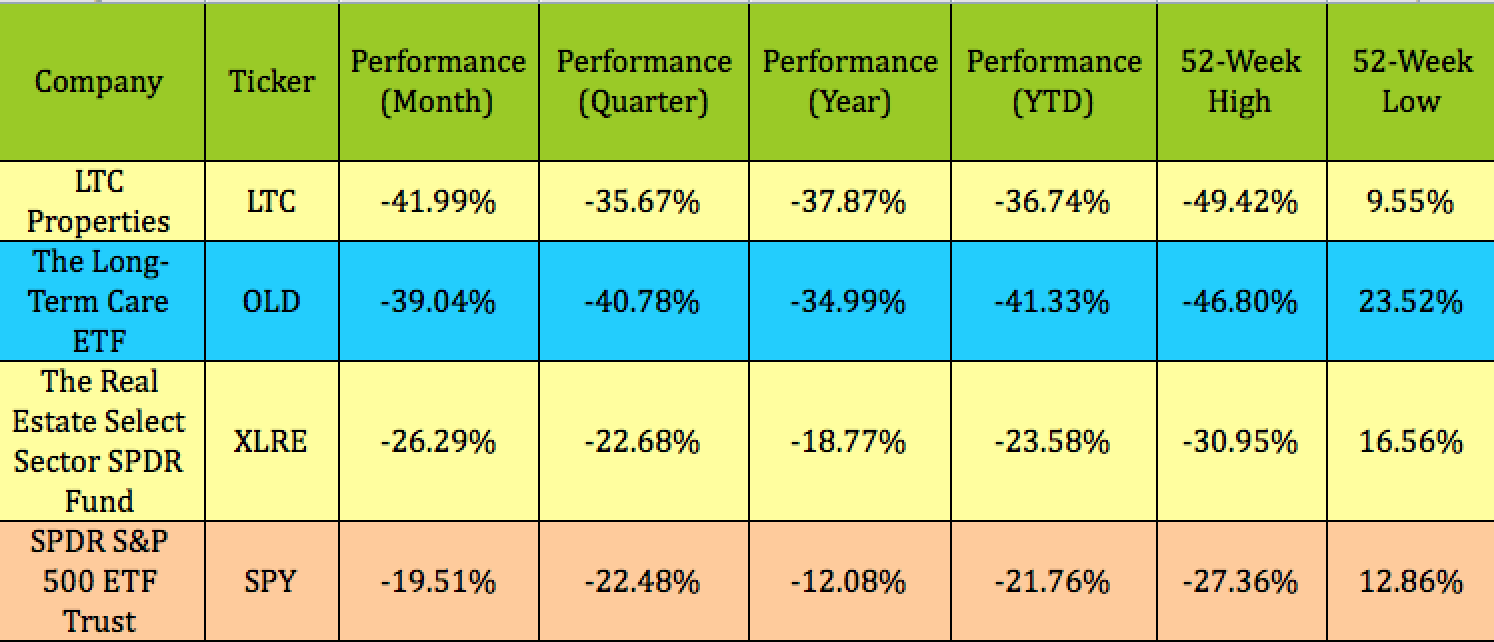

Comparing LTC to the Long Term Care ETF (OLD) shows LTC trailing over the past month and year, while outperforming a bit year to date. However, they’ve both lagged the broader Real Estate Selectp Sector SPDR ETF (XLRE) by a wide margin. XLRE has lagged the S&P over the past month, year, and year to date:

Profile:

Profile:

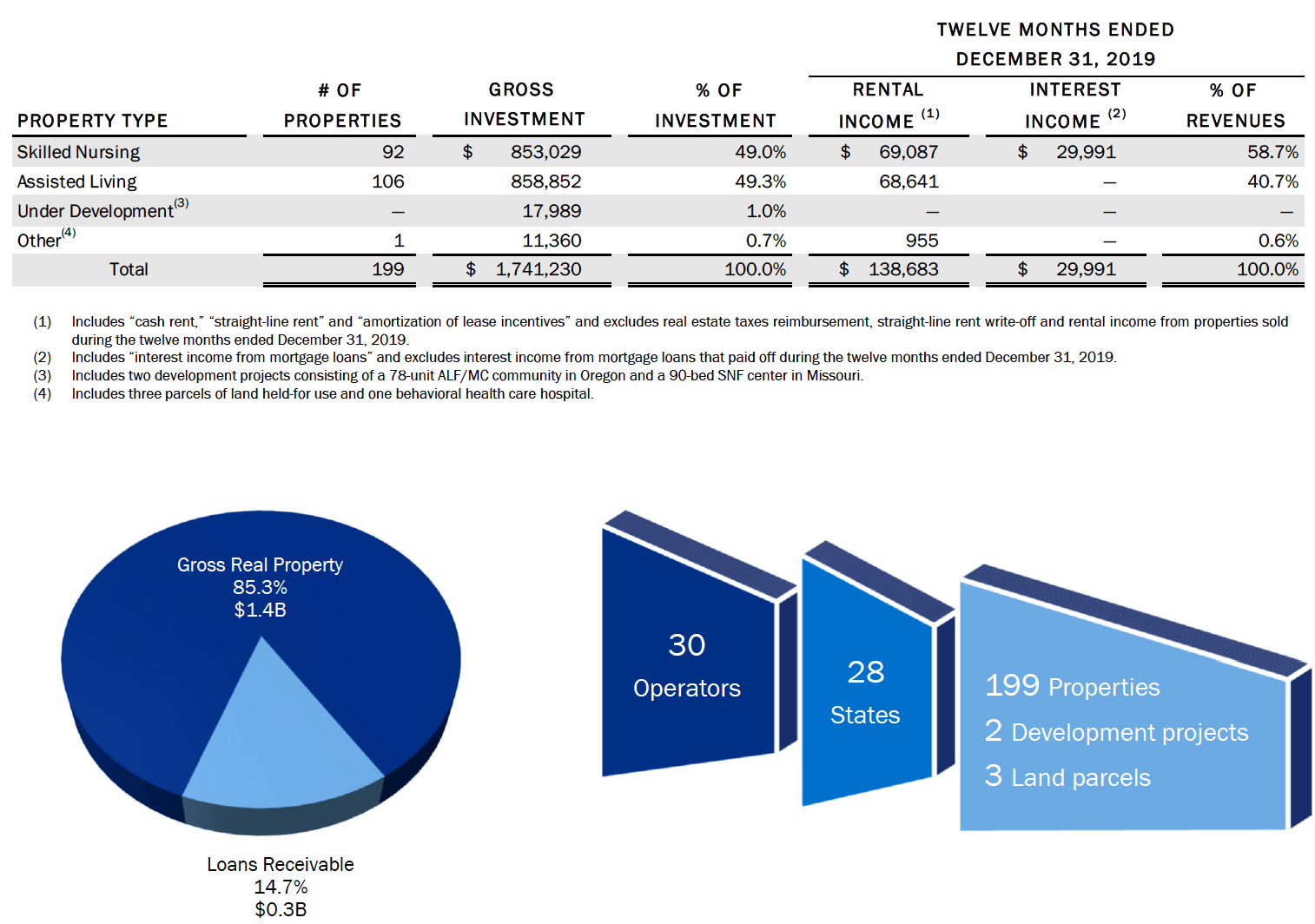

LTC invests in senior housing and healthcare properties primarily through sale leasebacks, mortgage financing, joint ventures and structured finance solutions including preferred equity and mezzanine lending. LTC holds more than 200 investments in 28 states with 30 operating partners. The portfolio is comprised of approximately 50% seniors housing and 50% skilled nursing properties. (source: LTC site)

(source: LTC site)

(source: LTC site)

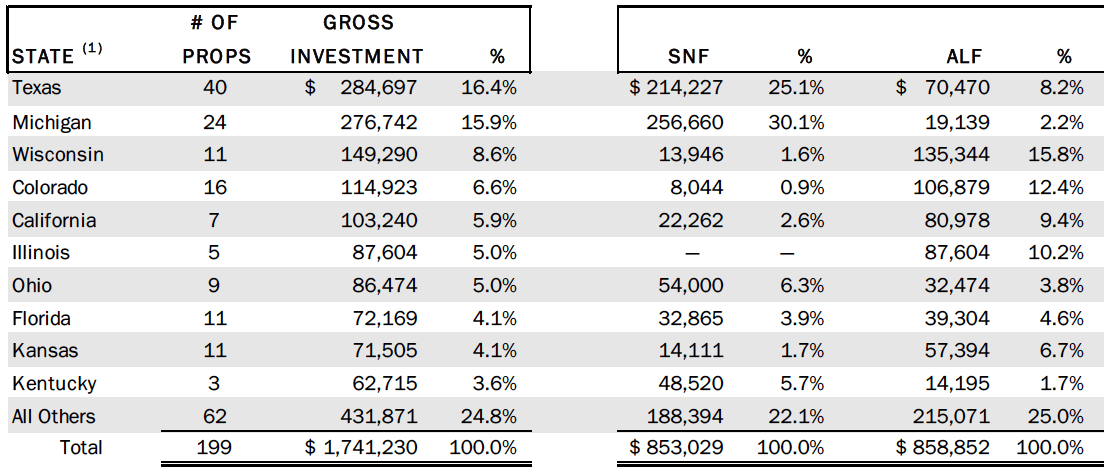

Management has concentrated on states with the highest forecasted rates for geezer growth over the next 10 years. Texas and Michigan top the list, comprising over 32% of total gross investment, and are heavily weighted toward skilled nursing facilities, forming over 55% of LTC’s SNF investments:

(source: LTC site)

(source: LTC site)

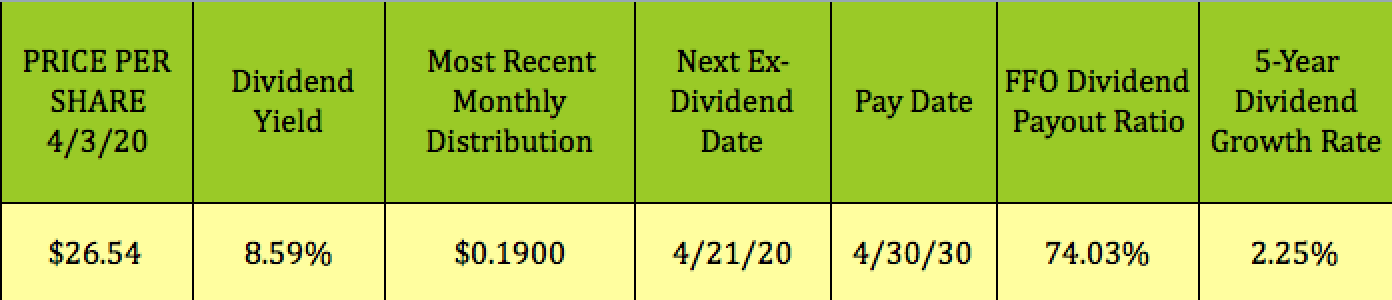

Dividends:

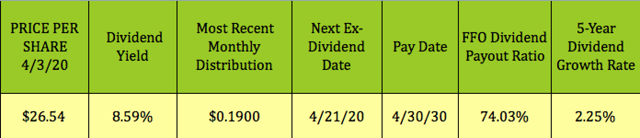

Like many of the income vehicles we’ve covered in our recent articles, the market pullback has pushed up LTC’s dividend yield to heights not seen in years.

It currently yields 8.59%, and goes ex-dividend next on 4/21/20. Dividend growth has been slight – LTC has paid $.19/month since Q4 2016.

Its trailing FFO dividend payout ratio is 74.03%.

Management typically pre-announces the dollar amount and the ex-dividend and pay dates for the upcoming quarter.

They did so this week, on 4/1/20, declaring a monthly cash dividend of $0.19/common share/month for the months of April, May and June 2020, payable on April 30, May 29 and June 30, 2020, respectively, to stockholders of record on April 22, May 21 and June 22, 2020, respectively.

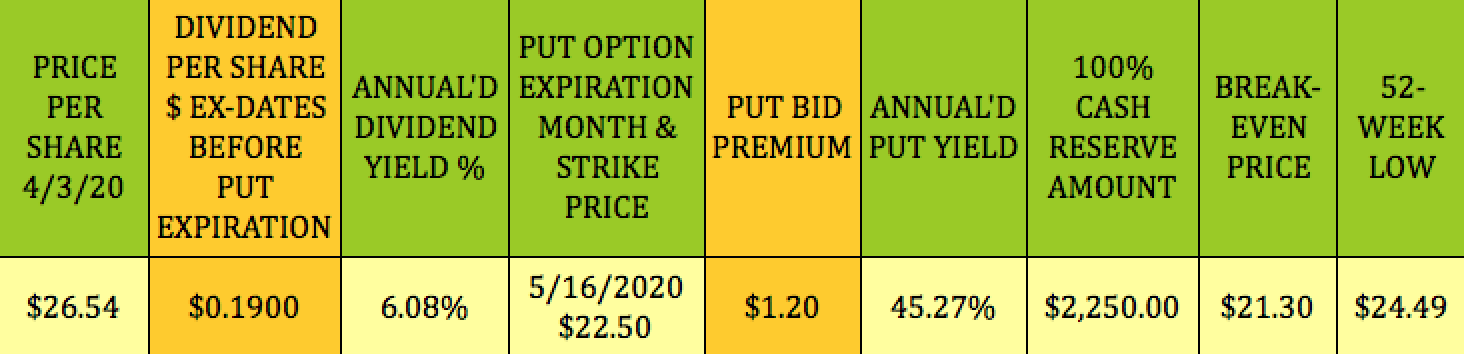

Options:

Options:

{kind=link}

Given LTC’s lagging performance during the pullback, an alternative to buying it outright would be to sell cash secured puts below its current price/share.

This short-term trade expires in mid May. LTC’s May $22.50 put strike, which is “out of the money,” i.e. further away from the price/share, pays $1.20. The nominal yield is 5.33% in ~6 weeks, or 45.27% annualized.

The breakeven is $21.30, which is 13% below LTC’s 52-week low.

NOTE: Put sellers don’t receive dividends – we include dividends in our tables, so that you can compare them to the option premiums. We use annualized yields in our options table, so that you can compare the yields from trades with different amounts of time.

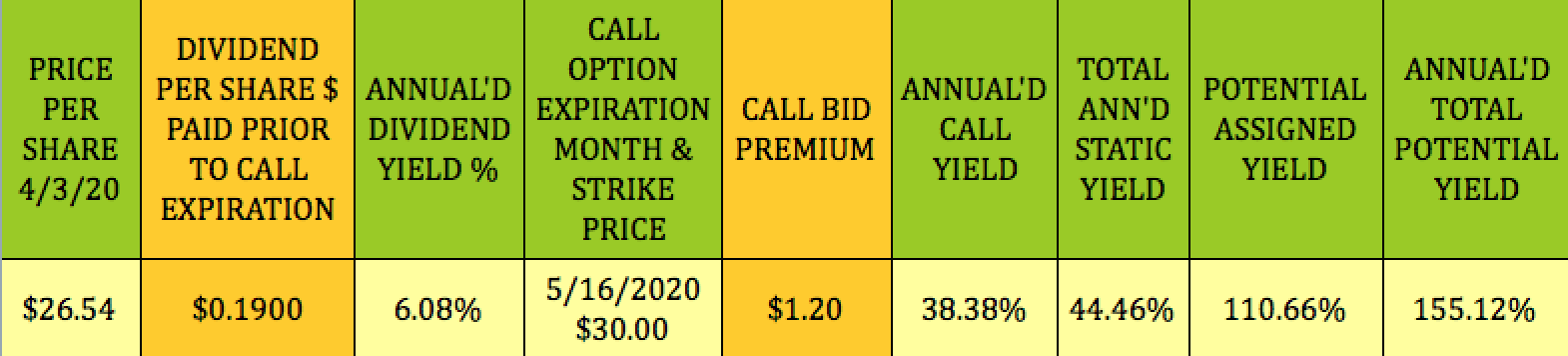

If you’re more bullish on LTC, and you think that the current low prices are going to last beyond mid May, there’s also a high-yield covered call trade which expires then.

If you’re more bullish on LTC, and you think that the current low prices are going to last beyond mid May, there’s also a high-yield covered call trade which expires then.

The May $30 call strike also pays $1.20. The combo of the one $.19 monthly dividend and the $1.20 option premium equals a nominal yield of 5.24% in six weeks, or 44.46% annualized.

You can see more details for these two trades on our free Covered Calls table and Cash Secured Puts table.

Earnings:

Earnings:

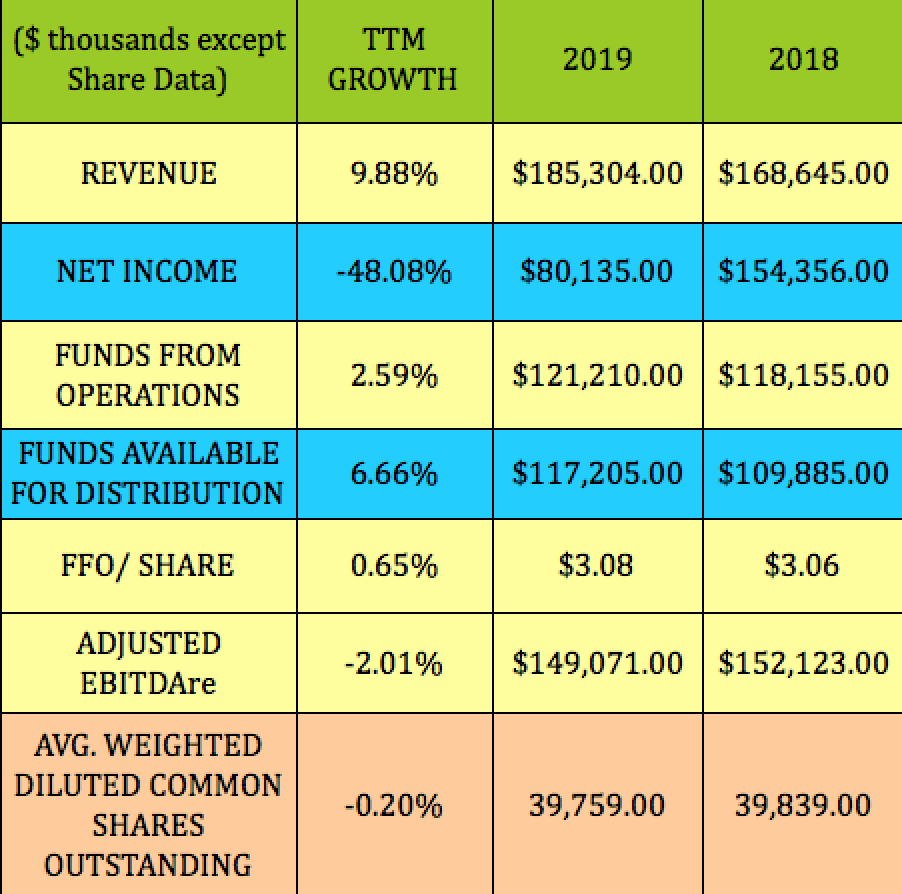

LTC’s revenue rose ~10% in 2019. Its Net income fell -48%, but, that’s due to an asset sale in 2018. Being a REIT, the more appropriate measure is Funds From Operations, FFO, which rose 2.59%.

Funds Available for Distribution rose by 6.66%, while FFO/Share growth was flat, at just .65%. Adjusted EBITDAre, (the “re” stands for real estate), slipped by -2%:

In February, management guided to FFO/share of between $3.01 and $3.03 for 2020, down ~-1.6% to -2.2% vs. 2019’s $3.08/share.

In February, management guided to FFO/share of between $3.01 and $3.03 for 2020, down ~-1.6% to -2.2% vs. 2019’s $3.08/share.

Recent Acquisitions and Asset Sale:

In January, LTC announced a $33M investment in three properties in Michigan and Texas with operators new to LTC. The two Michigan properties are located in Auburn Hills and Sterling Heights include a total of a 156 assisted living and memory care units and closed right at the end of 2019. LTC acquired them for $19 million with an additional capital improvement investment of approximately $2 million to be deployed in the first year of the lease.

The Michigan communities will be operated by Randall Residence and the Texas center will be operated by HMG Healthcare. Both regional operators are new to LTC. The properties will be on 10-year triple net master leases, escalating 2% annually starting in the second year of the lease, with five-year renewal options

– LTC just announced the completion of the sale of its largest holding this week – Preferred Care, which accounted for 19.4% of its income. LTC previously communicated that it anticipated concluding the sale during the second quarter of 2020 but finalized the transactions ahead of schedule.

The combined net proceeds for the Preferred Care portfolio, including one property sold in 2019 and 21 properties sold in the first quarter of 2020, was $77.9M, resulting in a total estimated gain on sale of $44M. The portfolio had a combined net book value of $35.6M.

The 21 properties sold in the first quarter of 2020, which included more than 2,500 beds across Arizona, Colorado, Iowa, Kansas and Texas, were sold through multiple transactions and generated net proceeds of $71.9M.

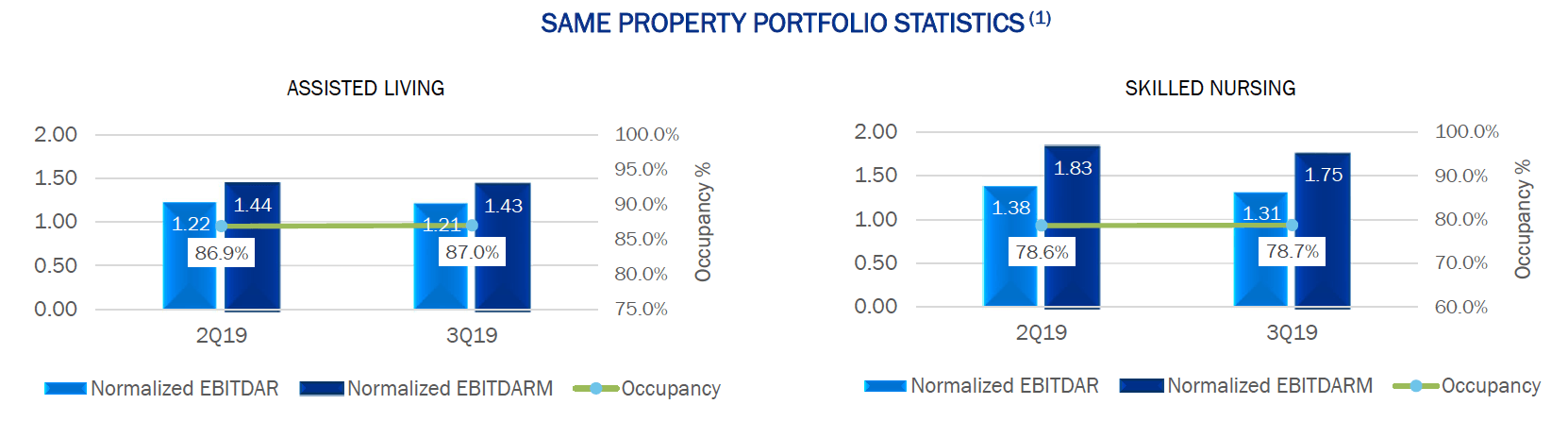

LTC’s quarterly same property stats are based on operator financial statements for the trailing periods ending 6/30/19 and 9/30/19. The occupancy rates for the operators appear stable in both segments, at ~87% for assisted living, and 80% for skilled nursing.

LTC’s quarterly same property stats are based on operator financial statements for the trailing periods ending 6/30/19 and 9/30/19. The occupancy rates for the operators appear stable in both segments, at ~87% for assisted living, and 80% for skilled nursing.

The assisted living segment had more stable EBITDAR and EBITDARM figures during these periods, whereas the SNF segment showed a -5.8% decline in EBITDAR and a -4.4% drop in EBITDARM:

(LTC site)

(LTC site)

Valuations:

LTC’s price decline has pushed its Price/FFO valuation lower than industry averages, at 8.62 vs. 10.64. It also looks cheaper on an EV/EBITDA basis, and slightly cheaper on a price/book basis, while its dividend yield is a bit lower than the group average.

Financials:

Financials:

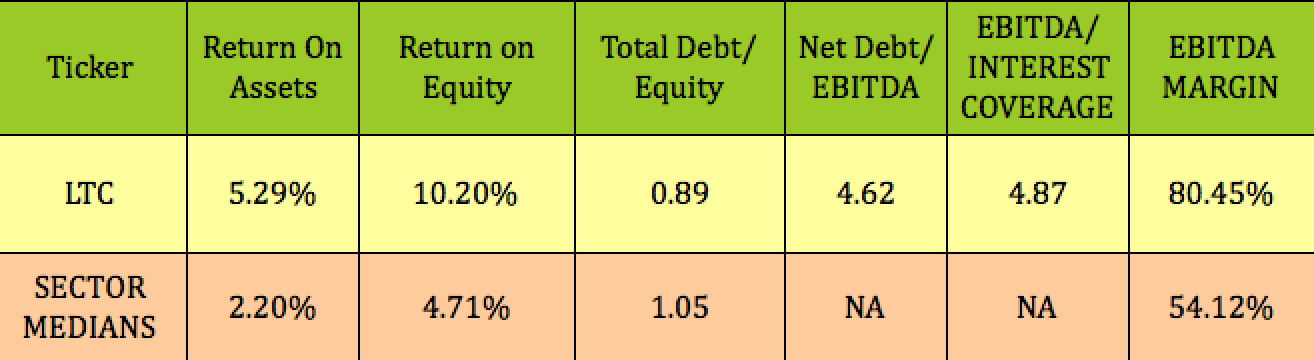

LTC’s ROA, ROE and EBITDA margin look stronger than sector medians, while its debt/equity leverage is lower.

Debt and Liquidity:

Debt and Liquidity:

LTC had $506.1M available on its $600M line of credit, as of 12/31/19. Its capitalization is comprised of 72% common stock and 28% debt.

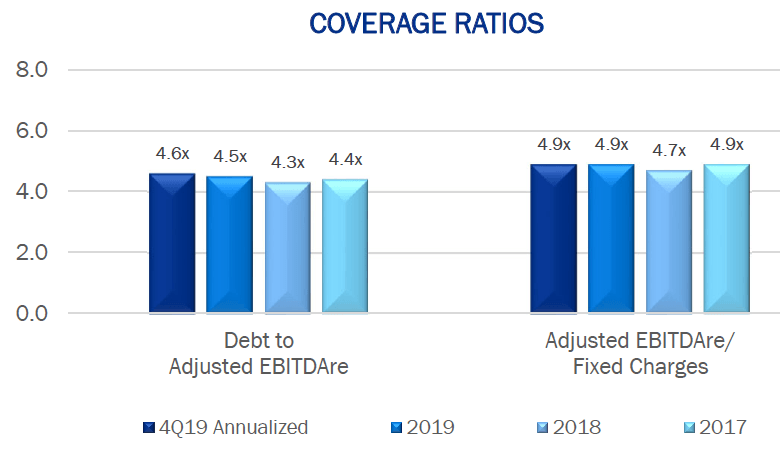

Its debt coverage ratios have been pretty steady over the past three years:

(LTC site)

(LTC site)

Risks:

Senior Housing operators have low margins, which could be further pressured by economic fallout in a recession. LTC’s management had to deal with operator delinquency issues in 2019, including Thrive, and Senior Care Centers. The bankruptcy court allowed Senior Care to assume their LTC lease over LTC’s objections, but LTC received all monies owed, including all past due rent and legal fees. Senior Care continues to get short extensions to emerge as they work to finalize their exit financing. As of late February, LTC’s management expected Senior Care to emerge from bankruptcy sometime in March.

When Thrive continued to not perform, LTC transitioned that portfolio to three separate regionally-based operators, which management feels are better capitalized. LTC’s triple net leases give them the power to vacate facilities which are occupied by non-performing operators, but this can be a lengthy process.

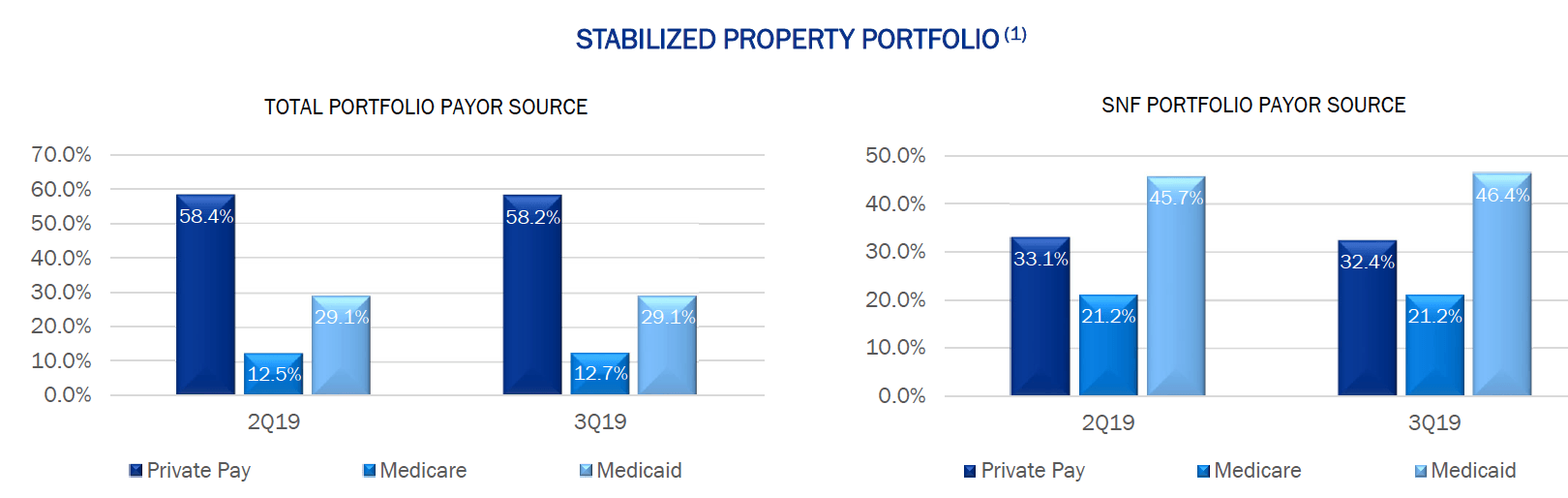

LTC’s total tenant portfolio averaged ~58% private pay, 29% Medicaid, and 12.7% Medicare in the trailing 12 months ending 9/30/19. The SNF segment had a much higher Medicaid amount, at ~46%. Regulatory issues can adversely affect operators’ already thin margins.

(LTC site)

(LTC site)

All tables by DoubleDividendStocks.com, except where noted otherwise.

Our Marketplace service, Hidden Dividend Stocks Plus, focuses on undercovered, undervalued income vehicles, and special high yield situations.

We scour the US and world markets to find solid income opportunities with dividend yields ranging from 5% to 10%-plus, backed by strong earnings.

We publish exclusive articles each week with investing ideas for the HDS+ site that you won’t see anywhere else.

We offer a range of income vehicles, which can offer you defense vs. this latest market pullback.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in LTC over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Our DoubleDividendStocks.com service has featured options selling for dividend stocks since 2009.

It’s a separate service from our Seeking Alpha Hidden Dividend Stocks Plus service.

Disclaimer: This article was written for informational purposes only, and is not intended as personal investment advice. Please practice due diligence before investing in any investment vehicle mentioned in this article.

Be the first to comment