ivanastar

Sometimes, market conditions can have a significant role to play in determining how a company will perform moving forward. In a typical market, you might expect a gradual amount of growth in business from year to year. This makes investing easier since you don’t anticipate any significant fluctuations, economically, that could impact the firms you are invested in. But during times of rapidly changing conditions, the picture becomes more complicated and investments that might otherwise have been fundamentally robust may not be all that great for investors to pursue. One company that this scenario may describe is home improvement retailer Lowe’s Companies (NYSE:LOW). Despite enjoying some rather attractive gains in recent years, the company does seem to be taking a step back from a fundamental perspective. Shares do still look cheap at the moment. But in the event that we see some return to normal, the stock would be, at best, fairly valued. The good news for investors is that this does create a favorable risk-to-reward scenario that, in my opinion, justifies a ‘buy’ rating, but not one that is as enthusiastic as the fundamentals initially indicate.

The picture is changing

Truth be told, Lowe’s Companies is not a firm that I keep track of as regularly as I would like to. In fact, the last article that I wrote about the business was published in May 2020. In that article, I talked about the robust financial performance of the company that was being generated in light of the pressures associated with the COVID-19 pandemic. I called the company a quality operator and I concluded that its future would likely be favorable for investors. At the end of the day, I ended up rating the business a ‘buy’ to reflect my view that shares should outperform the broader market for the foreseeable future. And outperform, they did. While the S&P 500 is up 39.3% since the publication of that article, Lowe’s stock has seen an upside of 88.4%.

This massive outperformance can be attributed to an unprecedented increase in demand for the company’s offerings. According to management, the global economic slowdown and social distancing created by policies in response to the COVID-19 pandemic resulted in individuals paying even more attention to the state of their homes. This led to some significant investment from consumers, investment that otherwise might not have come to pass. To illustrate, I need only look at financial data covering the past few years.

Author – SEC EDGAR Data

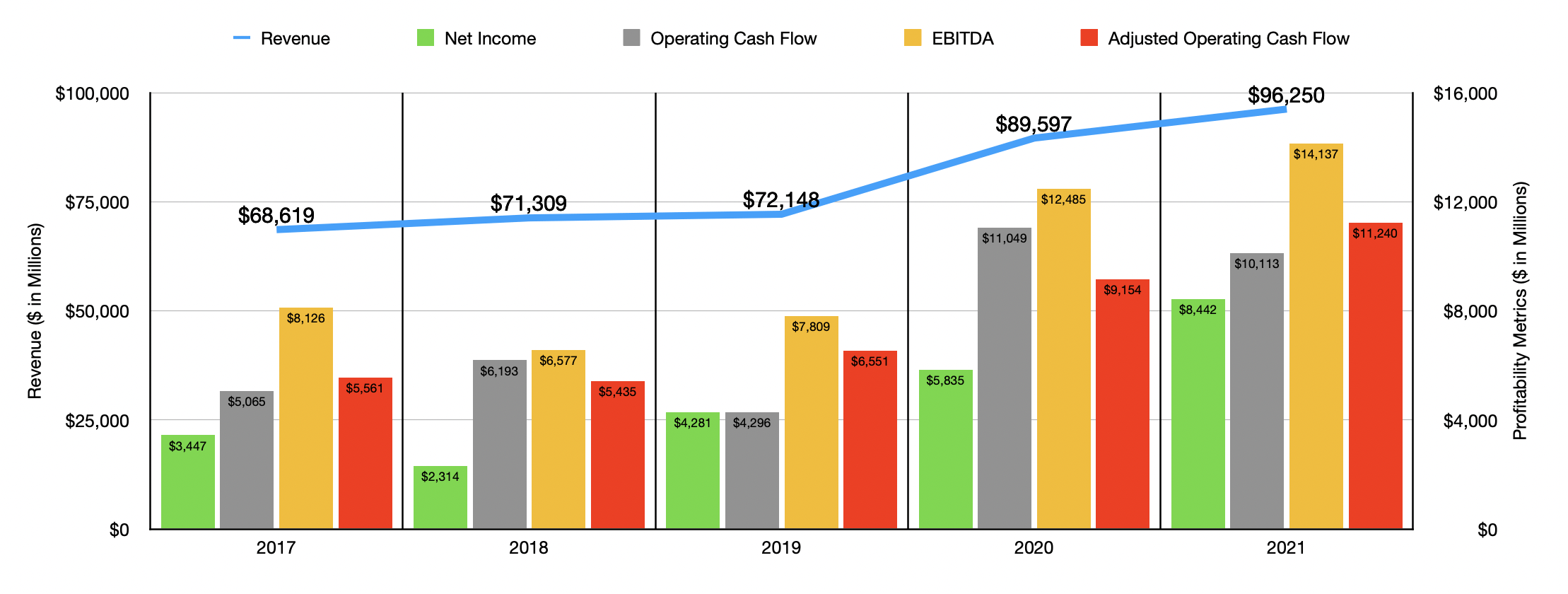

Between 2017 and 2019, revenue generated by Lowe’s Companies increased modestly from $68.6 billion to $72.1 billion. But then, in 2020, revenue surged 24.2% to $89.6 billion. This increase, management said, came even at a time when the company closed some of its stores. Comparable sales skyrocketed 26.1%, driven by a 14% rise in the number of comparable transactions and a 12.1% increase in comparable average ticket size of each transaction. Sales increased even further in 2021, hitting $96.3 billion for the year. Even though the number of stores the company operates dropped during this time, falling from 1,974 to 1,971, it benefited from a 6.9% increase in comparable sales. Unfortunately, total customer transaction volume during this time dropped by 4.2%. But this was offset by 12.2% rise in average ticket size.

The rise in revenue that Lowe’s experienced during this time also had a positive impact on its bottom line results. You see, whenever comparable sales increase, the company gets to spread out more of its fixed costs across more dollars of revenue generated. This helps earnings improve drastically, even relative to sales. For instance, after seeing that income climb from $3.4 billion in 2017 to $4.3 billion in 2019, it then surged 36.3% to $5.8 billion in 2020. In 2021, it jumped another 44.7% to $8.4 billion. Other profitability metrics followed a similar trajectory. In 2019, operating cash flow for the company was only $4.3 billion. This shot up to $11 billion in 2020 before ticking down modestly to $10.1 billion in 2021. If we adjust for changes in working capital, the metric would have continued rising, going from $6.6 billion in 2019 to $9.2 billion in 2020 before ultimately hitting $11.2 billion in 2021. A similar trajectory can be seen when looking at EBITDA, with the metric climbing from $7.8 billion in 2019 to $14.1 billion in 2021.

Author – SEC EDGAR Data

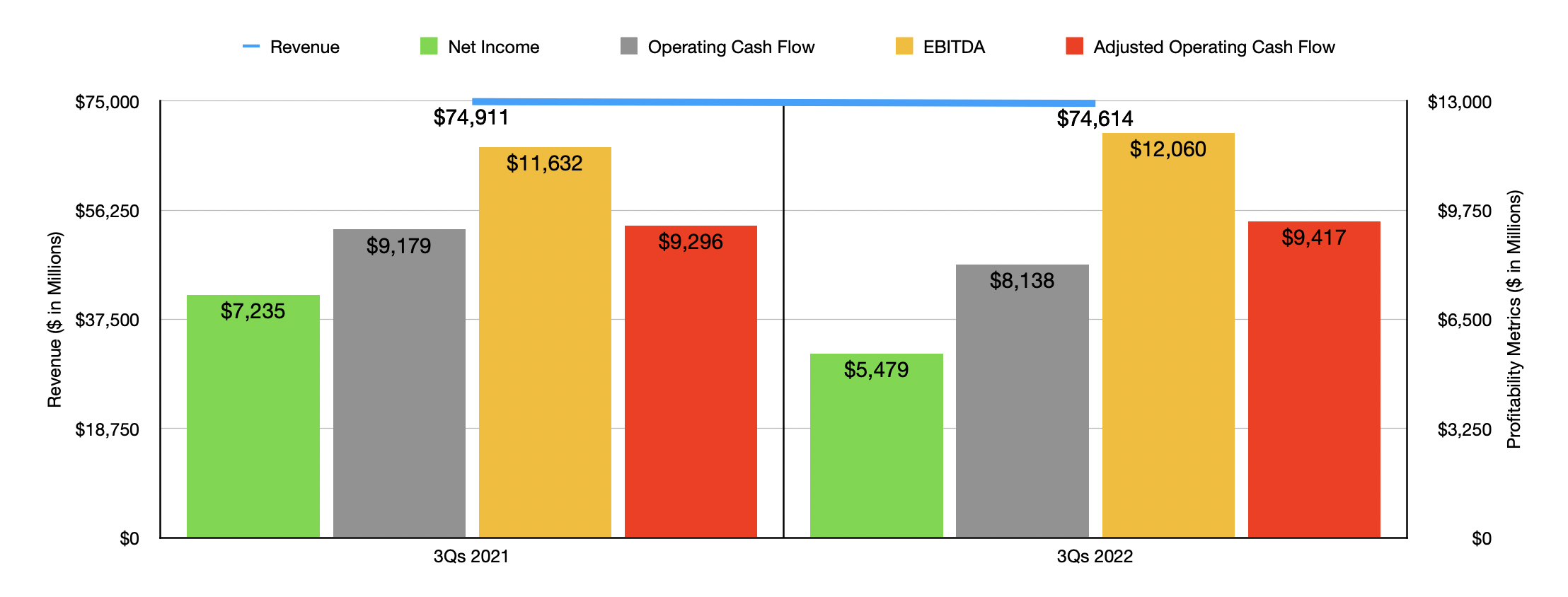

The decline in transaction volume seen during the 2021 fiscal year should have been the first indicator to investors that some weakness was arising. The higher pricing that management was charging for their goods, largely as a result of inflationary pressures, ended up reducing how many purchases consumers were making. Throughout the 2022 fiscal year, the business saw this picture worsen. Revenue during this time dipped 0.4% year-over-year, falling from $74.9 billion in the first nine months of 2021 to $74.6 billion the same time of the 2022 fiscal year. Overall comparable sales for the company actually fell during this time to the tune of 0.8%, plus the company saw a reduction in store count from 1,973 to 1,969. The sales decline for the company came in response to a plunge in customer transactions of 8.4%. The only reason why sales didn’t decline further is because the average ticket size jumped 8.8% from $95.40 to $103.76.

On the bottom line, Lowe’s Companies experienced some pressure. Net income dropped from $7.24 billion to $5.48 billion. While the decrease in sales played a part in this, the biggest hit came from selling, general, and administrative costs rising from 18.1% of revenue to 20.4%. Although this may not seem like much of a change, when applied to the revenue the company generated in the first nine months of 2022, it translated to $1.70 billion of missed pre-tax profits. The rest of this gap was made-up by higher depreciation and amortization costs, and a rise in interest expense. Other profitability metrics were somewhat mixed. For instance, operating cash flow fell from $9.18 billion to $8.14 billion. On the other hand, if we adjust for changes in working capital, it would have risen from $9.30 billion to $9.42 billion, while EBITDA jumped from $11.63 billion to $12.06 billion.

For the 2022 fiscal year in its entirety, management said that revenue should be between $97 billion and $98 billion. While this is higher than what the firm generated in 2021, it’s important to note that the existence of a 53rd week in the year is expected to result in between $1 billion and $1.5 billion of revenue that the company wouldn’t have if it were a typical year. Comparable sales would be somewhere between flat and down 1%. Management said the earnings per share, on an adjusted basis, will be between $13.65 and $13.80. At the midpoint, that would translate to net income of $8.51 billion. According to my own estimates, adjusted operating cash flow should be around $11.39 billion, while EBITDA should total around $14.66 billion.

Author – SEC EDGAR Data

Fundamentally, this looks great. But we need to keep in mind that these good times are not exactly here to last. The decline in the number of transactions the company is experiencing will eventually cause it to lower prices. In the event that the company was to revert back to the levels of profitability seen prior to the pandemic, during the 2019 fiscal year, shares would look a bit lofty. This much can be seen in the chart above. By comparison, if we use data from the 2022 fiscal year, shares look quite cheap when you consider how high-quality the business is. The price-to-earnings multiple in this case would be 14.8. The price to adjusted operating cash flow multiple would be 11.1, while the EV to EBITDA multiple would be 10.7.

It’s also worth noting that management is making some rather bold moves that may not make the most sense in the long run. During the first nine months of 2022, the company repurchased $12.13 billion in shares while simultaneously paying out $1.73 billion in the form of distributions. If the company was just using the cash it generates to do this, that would be fine. But this is not exactly the case. Operating cash flow during that window was only $8.14 billion. In fact, the company had to issue debt, on a net basis, of $8.84 billion during this time. In fact, from the end of the third quarter of 2021 to the end of the third quarter of 2022, net debt for the company jumped from $19.56 billion to $29.86 billion. Using data from 2022, Lowe’s Companies has a fairly respectable net leverage ratio of 2.04. But that ratio does worsen to 3.82 if we eventually revert back to the levels of profitability experienced in 2019. If management were to keep the debt situation where it is now, then things would probably be fine. But late last year, they announced a new $15 billion share buyback program on top of the $6.4 billion that they still have remaining under their old authorization. This suggests that the share buybacks aren’t done yet. To help cover this, though, the firm did recently sell off its Canadian retail business in exchange for $400 million in cash, plus potential contingency payments.

| Company | Price/Earnings | Price/Operating Cash Flow | EV/EBITDA |

| Lowe’s Companies (LOW) | 14.8 | 11.1 | 10.7 |

| The Home Depot (HD) | 19.5 | 25.3 | 13.4 |

I know a lot of what I’m saying now may look like I am bearish about the company. Fundamentally, I’m not. I do think that the fundamental picture will worsen from here, perhaps not in the next quarter or two, but certainly by the end of 2023. I’m wary of management buying back additional stock at current prices, especially with the run-up in net debt that we have seen. But again, even a return to the levels of profitability seen prior to the pandemic would result in shares being perhaps just a bit lofty. Of course, those who are bullish about the company could look at an interesting scenario with a pair trade. The largest home improvement company in the world, The Home Depot currently trades at a price-to-earnings multiple of 19.5, a price to adjusted operating cash flow multiple of 25.3, and an EV to EBITDA multiple of 13.4. Given this pricing disparity, going long Lowe’s Companies while going short Home Depot could result in some attractive returns.

Takeaway

Based on the data provided, I must say that I’m no longer as bullish on Lowe’s as I was previously. This does not mean that I am bearish. Long term, I suspect that this quality operator will do just fine. Those who have a long-term investment horizon should be less concerned about near-term fluctuations. Having said that, I do think some additional pain is around the corner and I think that shares might come to look more or less fairly valued as a result of that. This does still create a favorable risk-to-reward opportunity where, in the event that fundamentals don’t deteriorate, upside could be attractive, while in a scenario where they do deteriorate, downside would be limited or nonexistent. Simply going long the stock could be sensible here as a result. But for those who like something a little more exotic, a pair trade where one goes long Lowe’s Companies while going short the more expensive Home Depot could also be advantageous.

Be the first to comment