Torsten Asmus

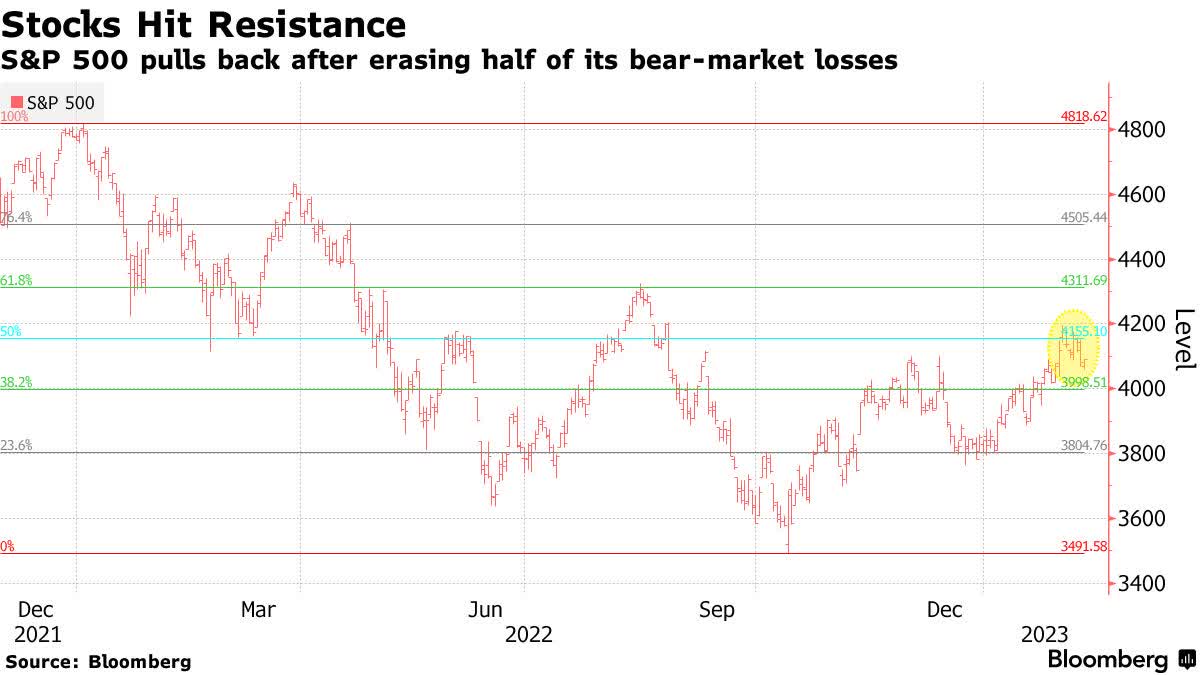

One week ago I wrote that we were likely to see a pullback in the major market indexes after their outsized year-to-date gains, which would serve as a pause to refresh a new bull market rather than resume the bear market that appears to have ended last October. That pullback looks to be underway, and it was instigated by a strong labor report for January and followed with warnings from central bankers that short-term rates could rise higher for longer than the consensus expects. As a result, markets are now pricing in a modestly higher interest-rate scenario. Yet the correction from the recent highs has been relatively modest, which tells me we need a little more red meat to feed the bearish narrative, clear out the weak shareholders, and find a higher bottom in the S&P 500 that refreshes the new uptrend. Tuesday’s inflation report may be it.

Edward Jones

Typically, once a bear market retraces 50% of its losses, it is an indication that a new bull market has started. In fact, each of the prior 13 bear markets since 1946 ended after the S&P 500 recovered 50% of its losses, but the latest retracement comes with a caveat. This is the second 50% retracement, as the first occurred last August, but it was followed with a new low in October. That ended a perfect score for this indicator, but I am chalking it up as another “first” in a long list of firsts that have become the norm in this unprecedented post-pandemic economic expansion. Surely, the second time will be the charm, but the end to the perfect score for this indicator is another factor breathing life into skeptics.

Bloomberg

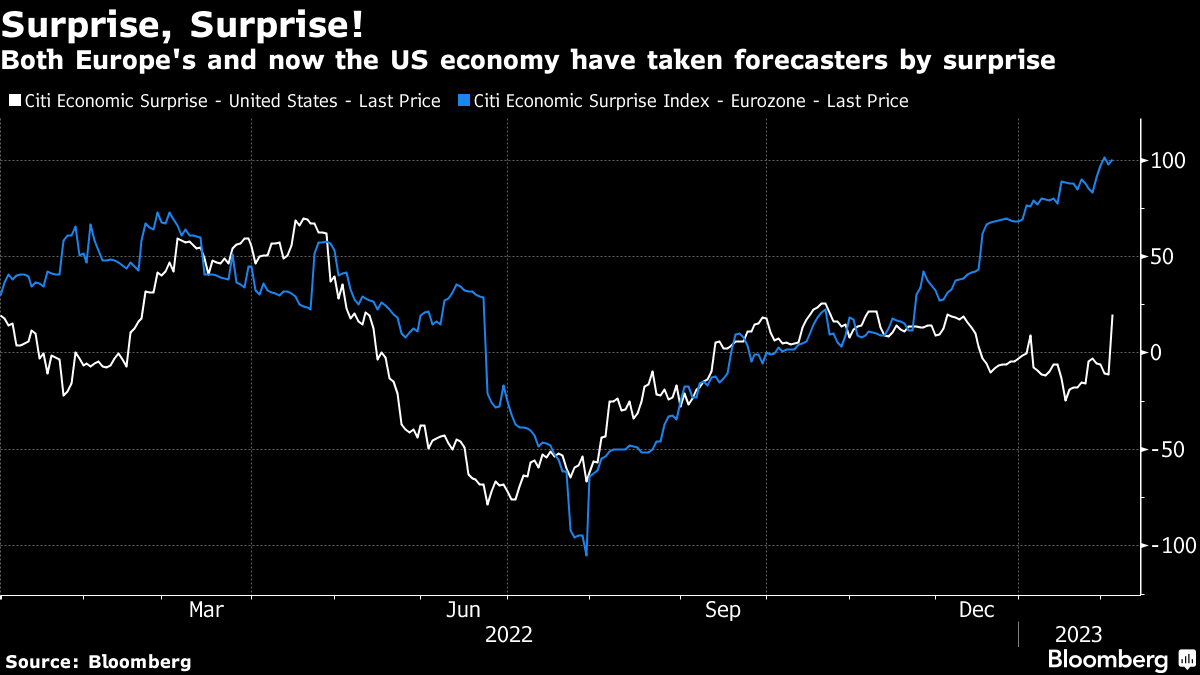

I have been encouraged by the economy’s resiliency this year in light of Fed policy. We continue to be warned by the bearish consensus that the Fed’s tightening campaign will have dire consequences for the economy and markets. To that point, it does take several months for rate increases to work their way through the economy and have their full impact, but the Fed started raising rates nearly a year ago, and the high frequency economic data is again starting to surprise to the upside.

Bloomberg

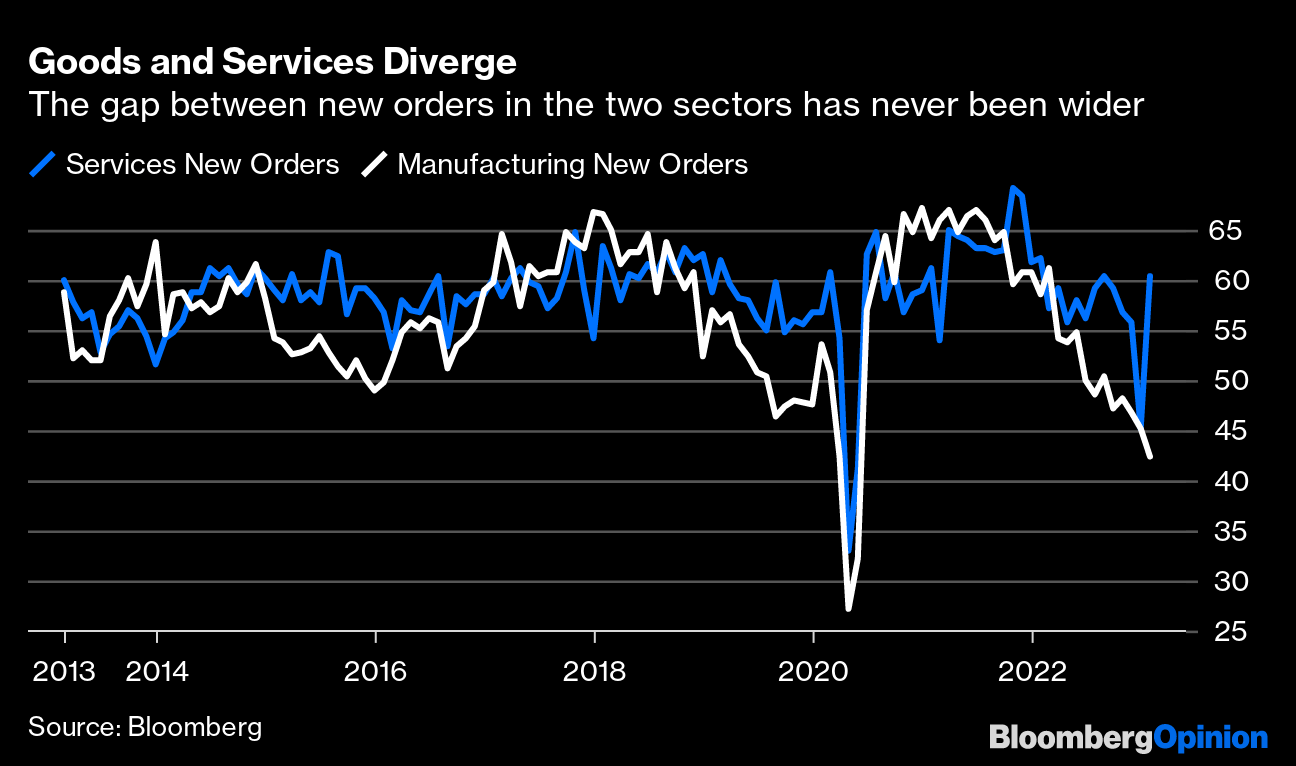

This resiliency is largely due to the strength of the service sector, as consumer savings and wage growth fuel spending on experiences at the expense of goods, resulting in one of the largest disparities between goods and services spending on record. I think this is another post-pandemic anomaly that will adjust over the coming year, but for now it is keeping the current expansion alive.

Bloomberg

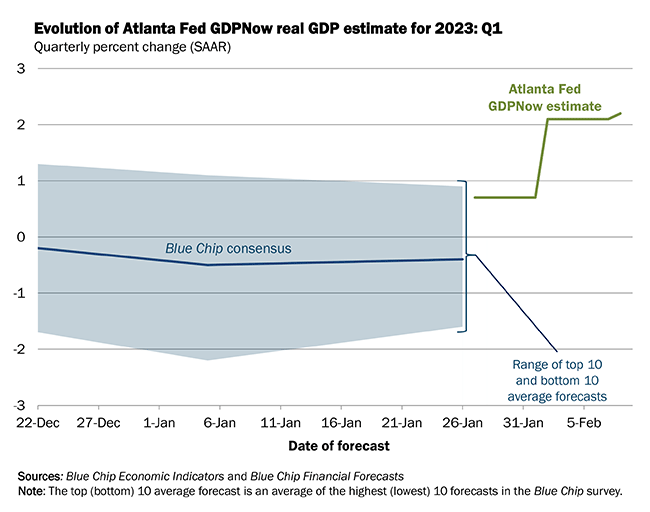

In fact, the Atlanta Fed’s GDPNow model is forecasting growth in the first quarter of 2.2%, which is a real-time estimate that has been increasing over the past three weeks, but not at the expense of disinflation.

Atlanta Fed

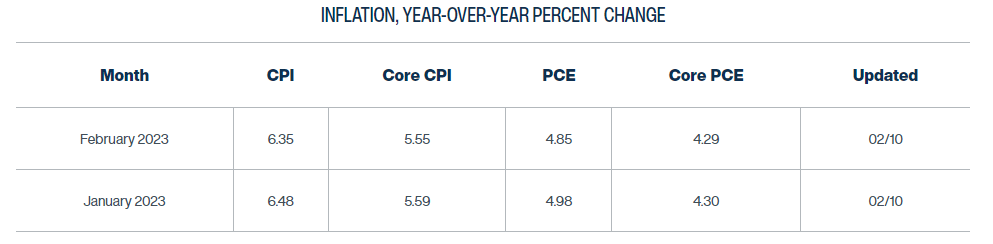

The Cleveland Fed’s Inflation Nowcasting model shows the annualized run rate for price increases in the first quarter of this year at 3.86%, which is moving ever closer to the 2-handle that the Fed is targeting for its preferred measure of inflation—the personal consumption expenditures price index (PCE). Tuesday’s focus will be on the Consumer Price Index (CPI), and any deviation from what has been a steady decline in prices over the past six months will likely be met with an increase in volatility and decline in risk asset prices.

Cleveland Fed

The consensus is forecasting a 0.4% increase in the January CPI, which would bring the year-over-year rate down from 6.5% in December to 6.2%. The core CPI is expected to rise 0.3%, bringing the year-over-year rate down from 5.7% to 5.4%. An uptick in used-car prices might result in a slightly hotter number than expected. Additionally, a new weighting system to be implemented for the first time in January by the Bureau of Labor Statistics will place more emphasis on goods than services, which runs counter to current spending trends.

Cleveland Fed

These two factors may lead to a hotter monthly number than expected, which is what the Cleveland Fed’s model now shows. If we see no decline in the year-over-year rate at 6.5% and a downtick in the core from 5.7% to 5.6%, it will not disrupt the steady disinflationary trend that started last July. Still, the bears will undoubtedly assert that disinflation was transitory, and stocks are likely to sell off further. I think the S&P 500 has downside to 3,900. So be it, as that will be the excuse to complete the correction this market needs and resolve the overbought short-term condition.

Be the first to comment