“There’s one more terrifying fact about old people: I’m going to be one soon.” – P. J. O’Rourke

Today, we revisit a ‘Tier 4‘ microcap biotech concern. The company had a horrid year in 2019 but has made some significant progress so far in 2020, even as its stock remains a roller coaster. We update the investment case on this volatile name to incorporate all recent events in the paragraphs below.

Company Overview:

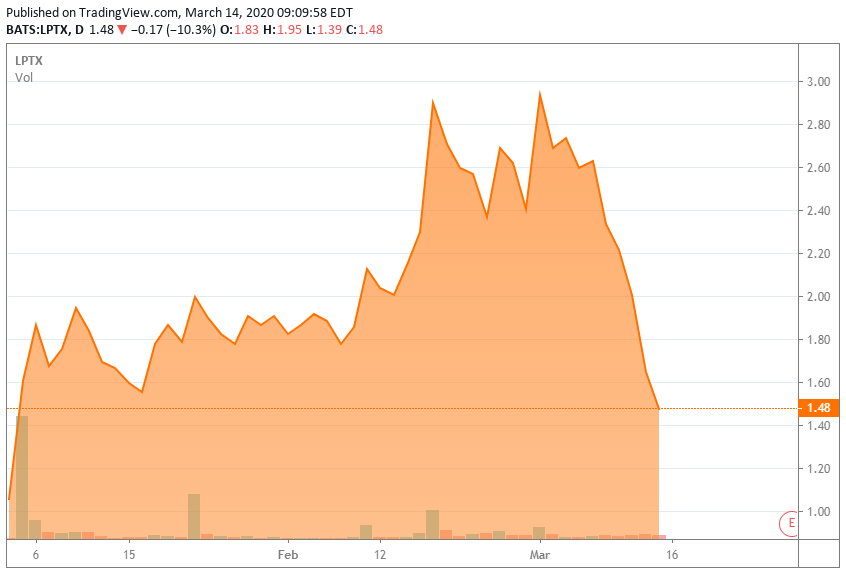

Leap Therapeutics, Inc. (LPTX) is a Cambridge, Massachusetts based biotech focused on the development of targeted remedies for various forms of cancer. The company effectively has one asset (DKN-01) in the clinic after de-prioritizing solid tumor candidate TRX518 in November 2019. Leap was founded in 2011, later going public when it executed a reverse shell merger in January 2017 while concurrently transacting a private placement at $9.90 a share. After trading below $1 a share for the final seven weeks of 2019, two press releases in 2020 – one announcing a collaboration deal and concurrent dilutive financing, and the other updating positive clinical news regarding DKN-01 – propelled the shares to over $2.50 a share, which the stock has given back during the recent market meltdown.

{kind=link}

DKN-01

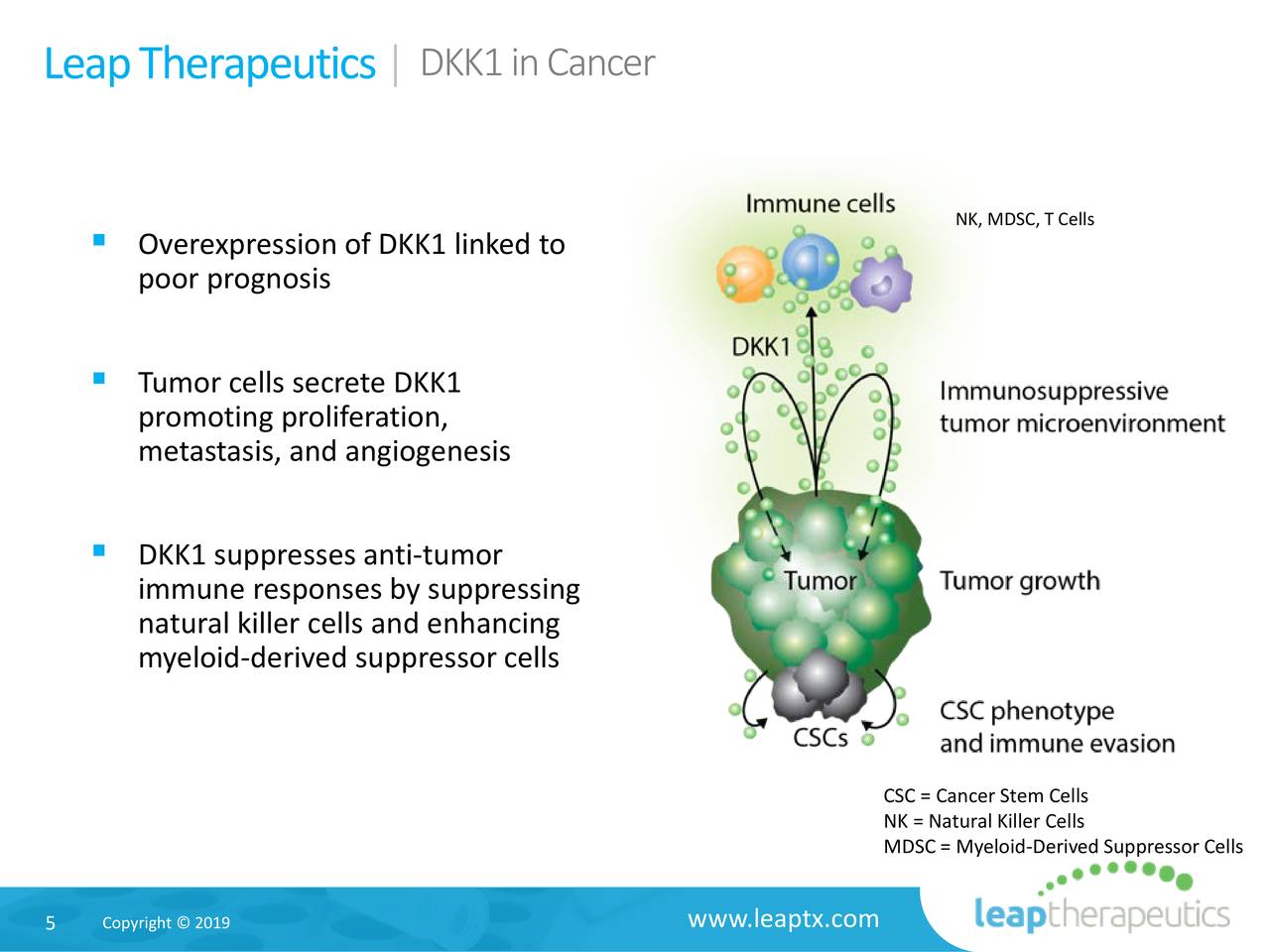

The company is hanging its hat on DKN-01, which it developed after identifying a set of signaling pathways in cancer cells known as canonical and non-canonical Wingless/Integrated (Wnt) pathways. The Dickkopf-related protein 1 (DKK1) has been identified as an inhibitor of the canonical Wnt pathway and a modulator of the non-canonical Wnt pathway. Tumor cells secrete DKK1, thus promoting cancer cell growth and metastasis while curbing immune response by suppressing natural killer cells and enhancing myeloid-derived suppressor cells.

Source: Company Presentation

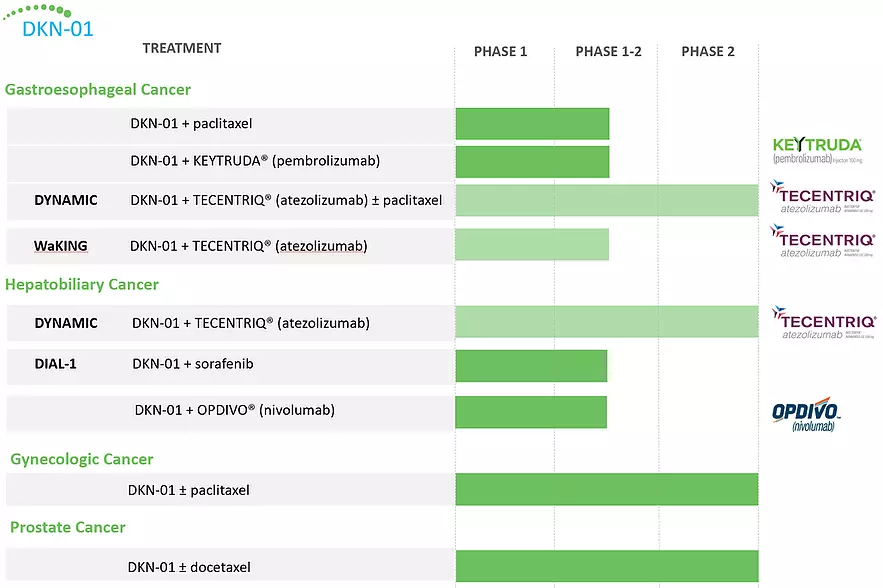

DKN-01 is a humanized IgG4 monoclonal antibody (MAB) for DKK1 that is being assessed as a monotherapy, and in combination with chemo and/or immunotherapy for the treatment of esophagogastric, gynecologic, hepatobiliary, and prostate cancers.

Source: Company Presentation

Esophagogastric Cancers (EGCs). The most recent DKN-01 update is from a multi-part Phase 1/2 trial evaluating it as a monotherapy, in combination with Merck’s (MRK) immunotherapy drug KEYTRUDA (pembrolizumab), and in combination with chemo agent paclitaxel in advanced ECG patients who have progressed after previous lines of therapy.

On January 23, 2020, Leap updated data (from August 2019) on a subgroup of 25 patients with anti-PD-1/PD-L1 naïve gastric/gastroesophageal junction adenocarcinoma treated with DKN-01 plus KEYTRUDA. Of the ten whose tumors expressed a DKK1 H-Scores greater than 31 (DKK1-high), 22 weeks median progression free survival (PFS) and 32 weeks of median overall survival (OS) were observed. Overall response rate (ORR) was 50% and the disease control rate (DCR) was 80%. That compared favorably to the 15 DKK1-low patients, who only achieved median PFS of 5.9 weeks, OS of 17.4 weeks, and a DCR of 20%. Owing to this correlation, Leap will use tumoral DKK1 levels to prospectively identify patients in subsequent studies with new collaboration partner BeiGene – more on that later.

In an earlier readout, the DKN-01/paclitaxel combo achieved OS of 14.1 months, PFS of 19.6 weeks, overall response rate (ORR) of 46.7%, and DCR of 73.3% as a second-line treatment in 15 patients with esophagogastric malignancies. Overall, the DKN-01/chemo combo achieved a 25% ORR, a 59.6% DCR, median PFS of 13.4 weeks, and median OS of 27.9 weeks in 52 previously treated patients expressing esophagogastric tumors. As a benchmark, paclitaxel monotherapy in patients who have received prior chemotherapy has only demonstrated ORRs of ~7% in esophageal cancer and ~16% for gastric cancer.

There is a significant need for upgrading the current treatment paradigm of esophagogastric cancers with ~46,000 new cases diagnosed annually in the U.S. and ~1.4 million worldwide. Most people diagnosed have late-stage disease, owing to the fact that symptoms don’t generally manifest until the tumor is fairly large. Esophageal patients and gastric cancer patients have 5-year survival rates of 18.8% and 30.6%, respectively.

Gynecological Cancers. DKN-01 is also being assessed as a monotherapy and combination with paclitaxel in a Phase 2 basket study for the treatment of advanced gynecological cancers. In the monotherapy cohort, of the 16 evaluable patients with relapsed/refractory epithelial endometrial cancer (EEC) and Wnt signaling mutations, one complete response, one partial response (PR), and seven stable disease (SD) were observed for a 12.5% ORR and 56.3% DCR. In the six evaluable patients devoid of Wnt signaling mutations, none had clinical benefit. The study is being expanded to include cohorts of patients with carcinosarcoma.

In 14 evaluable relapsed/refractory endothelial ovarian cancer (EOC) patients, seven had stable disease (50% DCR).

Overall, irrespective of cancer (EEC or EOC), mono or combination therapy, patients with Wnt activating mutations have demonstrated a longer PFS (n=21, 175 days) versus patients without Wnt activating mutations (n=67, 63 days). And as was the case with the EGC studies, patients whose tumors are DKK1-high have prolonged PFS (n=13, 168 days) as compared to patients with tumors that are DKK1-low (n=41, 63 days). Also, median OS has not yet been reached for the patients with Wnt activating mutations as compared to 321 days OS for patients without Wnt activating mutations.

Hepatobiliary Cancers. Leap is also studying DKN-01 in combination with Bristol Myers’ (BMY) OPDIVO in previously treated patients with advanced biliary tract caner. The ~36-patient trial’s primary endpoint will be ORR. Bristol is providing both OPDIVO and partial funding for the study. Enrollment, which began in 3Q19, is ongoing.

In a prior study that was readout in 2018, DKN-01 in combination with chemo agents gemcitabine and cisplatin demonstrated median OS of 12.4 months and median PFS of 8.7 months in 47 evaluable patients with advanced biliary tract cancer. Ten patients (21.3%) had a PR and 31 patients (66.0%) achieved SD, representing a DCR of 87.2%. The one-year probability of OS was 51%, and the six-month probability of PFS was 58%.

The common theme through these studies is that patients with Wnt signaling mutations or high DKK1 levels respond to DKN-01. As a result, DKN-01 is being further investigated in biomarker-enhanced studies, including as a monotherapy and in combination with protein kinase inhibitor sorafenib in patients with hepatocellular carcinoma, and as a monotherapy and in combination with chemo agent docetaxel in patients with advanced prostate cancer.

BeiGene Partnership

With DKN-01 demonstrating some promise in these early stage trials, Leap has attracted a partner in BeiGene (NASDAQ:BGNE). Under the agreement announced on January 3, 2020, BeiGene will receive a license to develop and commercialize DKN-01 in Asia (ex-Japan), Australia, and New Zealand. Leap will receive $3 million upfront and be eligible to receive development and commercial milestones of $132 million and tiered royalties. This partnership makes a lot of sense as the biggest source of cases of Esophagogastric Cancers are in China.

Recent Financing:

In addition to the $3 million upfront, BeiGene made a $5 million investment as part of a contemporaneous and complicated $26.1 million financing that involved two other institutional investors: Baker Brothers and Perceptive Advisors. Without going into all the convertible preferred stock, accruing dividend, forced convertibility, and pre-funded warrant machinations, as the lead investor, Baker Brothers is essentially investing $15 million at $1.055 per share and is receiving a seat on the board of directors. BeiGene and Perceptive ($7 million) are investing the balance. In total and on a pro-rata basis, the three investors are also receiving ~25.6 million warrants struck at $2.11 a share. This transaction not only raised needed capital for Leap, but also had the effect of regaining compliance with NASDAQ listing requirement of minimum stockholders’ equity of $10 million. It also marked the third and largest equity financing for the company in eleven months.

Balance Sheet & Analyst Commentary:

On September 30, 2019, Leap held $10.1 million of cash and no debt. With a burn rate of ~$8 million a quarter, it is safe to assume that the coffers were nearly empty at the time of the early January financing, forcing the de-prioritizing of solid tumor mAb TRX518. With the focus strictly on DKN-01, Leap has essentially ‘bought’ itself a cash runway to YE20.

The financing news prompted Raymond James, which had downgraded Leap in November 2019, to raise its rating from a hold to a outperform with a twelve-month price target of $2.50. HC Wainwright also follows the company, currently recommending a buy with a price target of $3.25. Robert W. Baird is the most optimistic analyst firm on Leap, reissuing its Buy rating and $6 price target on February 11th.

Verdict:

News of the financing gave the company a much-needed shot in the arm. Shares of LPTX soared 52% to $1.61 as 16.9 million shares exchanged hands over the subsequent trading session. The momentum continued with the January 23rd update on DKN-01 in the treatment of EGCs. Even though it won’t show up on its financial statements for a while, with the financing, Leap essentially doubled the number of its shares outstanding to just shy of 50 million. There are also ~35 million additional warrants, not counting the ones with a conversion price of $0.01 – equity in disguise – with conversion prices between $1.75 and $2.11. The stock got up to over $2.50 a share in early March, but has sold off some 40% in the past two weeks as the market has tanked.

Having two big institutional investors on board certainly helps, and with Baker getting a seat on the board, investors should be confident. And with close working relationships with Merck and Bristol Myers, there is always a possibility of another BeiGene-like collaboration for DKN-01.

In summary, after a disappointing 2019, the company seems headed in the right direction so far in 2020. Obviously, our outlook is not as rosy as when the company had two main assets in its pipeline and before it had to line up some dilutive financing. We are not adding to our holdings of Leap Therapeutics but are hanging on to our existing stake.

“Family love is messy, clinging, and of an annoying and repetitive pattern, like bad wallpaper.” – P. J. O’Rourke

Bret Jensen is the Founder of and authors articles for the Biotech Forum, Busted IPO Forum, and Insiders Forum

I present and update my best small-cap biotech stock ideas only to subscribers of my exclusive marketplace, The Biotech Forum. Try a free 2-week trial today by clicking on our logo below!

Disclosure: I am/we are long LPTX. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment