Tippapatt/iStock via Getty Images

A Quick Take On LiveRamp Holdings

LiveRamp Holdings, Inc. (NYSE:RAMP) recently reported its FQ1 2023 financial results on August 7, 2022, beating revenue estimates.

The company provides identity resolution software and related capabilities for online marketing activities.

Given uncertainties about the firm’s mid-market customer base spending slowdown and its increasing operating losses, I’m on Hold for RAMP over the near term.

LiveRamp Overview

San Francisco-based LiveRamp was founded to offer a suite of audience identification and data tools for online marketing purposes.

The firm is headed by Chief Executive Office Scott Howe, who was previously president and CEO of marketing services company Acxiom.

The company’s primary offerings include:

-

Identity resolution

-

Data activation

-

Measurement

-

Data collaboration

-

Marketplace

The firm acquires customers via its direct sales teams as well as through partners and cloud provider channels.

LiveRamp’s Market & Competition

According to a 2021 market research report by MarTech referencing a report by Winterberry Group, the global market for identity resolution services is forecast to reach $2.6 billion by the end 2022.

As marketers lose access to some forms of data such as via ‘cookies’ from major mobile platforms from Apple and Google, data from alternative sources is becoming more valuable.

Different industries are more or less reliant on third-party cookies for their online marketing efforts, with the financial services and travel industries reporting the greatest reliance on cookies.

Major competitive vendors or other industry participants include:

-

Intent IQ

-

Saint-Gobain S.A Tapad

-

Amperity

-

Merkle

-

Zeta Global

-

Throtle

-

Xoriant Katch

-

Signal

-

Neustar

-

BounceX

-

NetOwl

-

Informatica

-

Infutor

-

Criteo

LiveRamp’s Recent Financial Performance

-

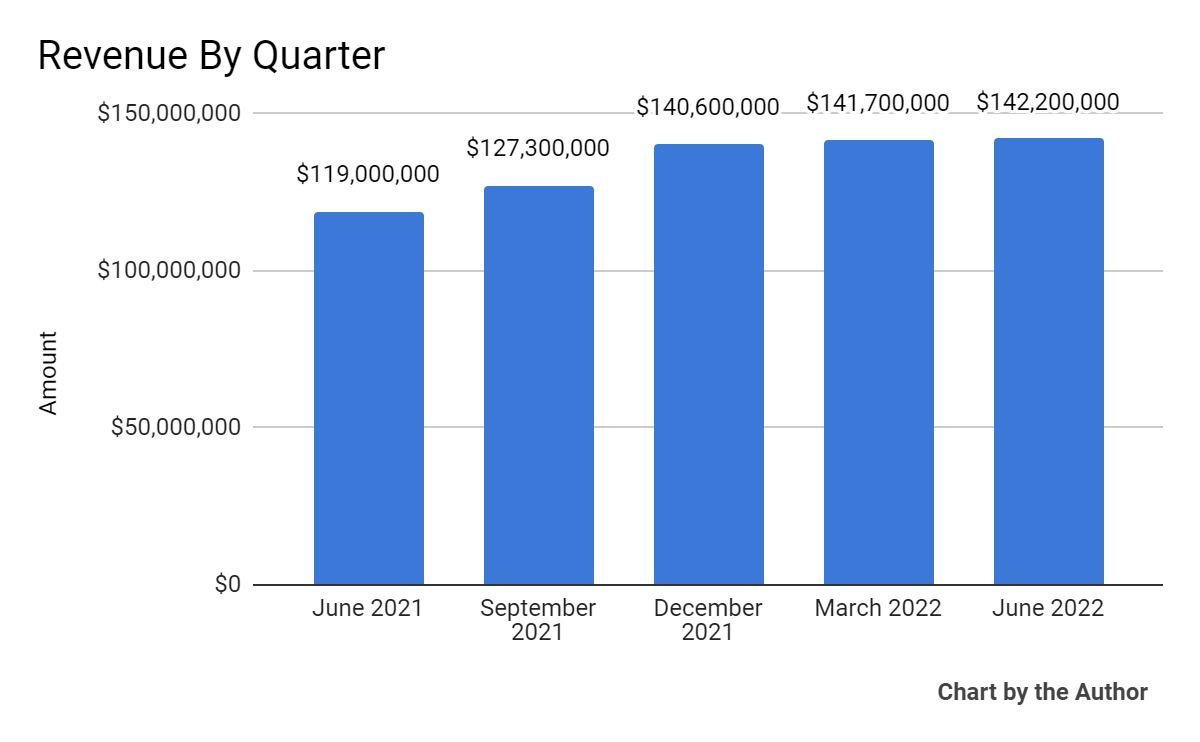

Total revenue by quarter has plateaued in recent quarters, as the chart shows here:

5 Quarter Total Revenue (Seeking Alpha)

-

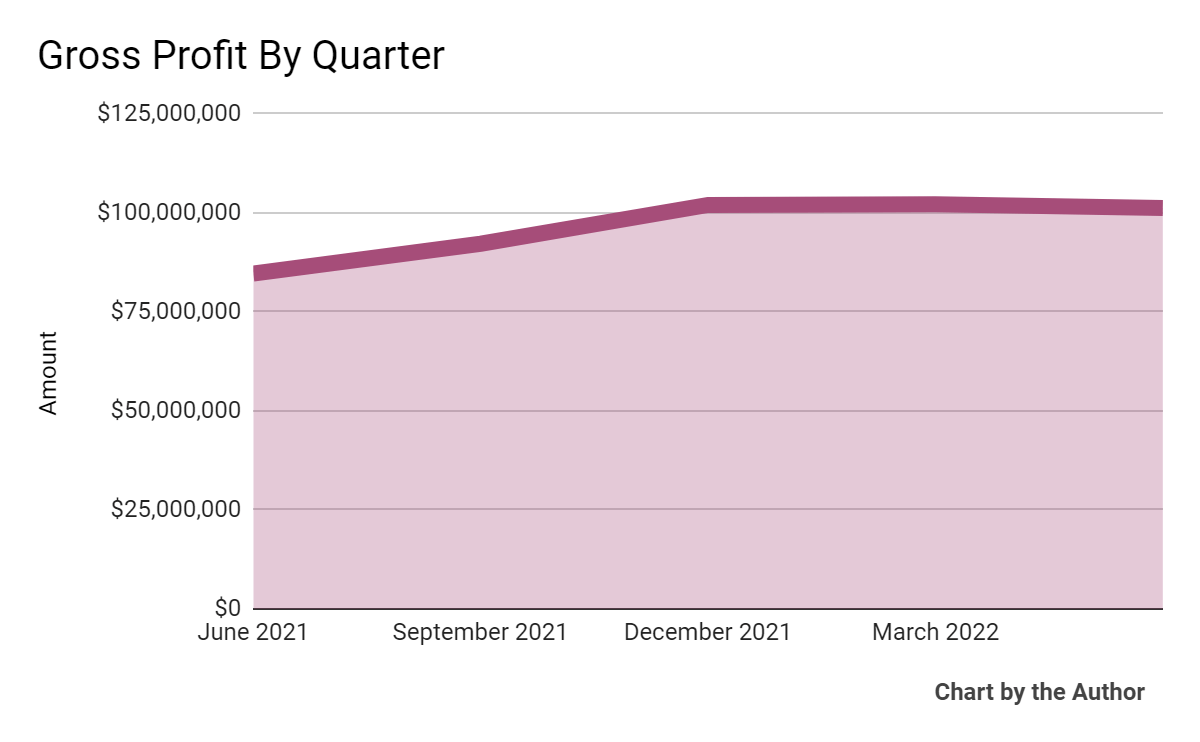

Gross profit by quarter has also flattened recently:

5 Quarter Gross Profit (Seeking Alpha)

-

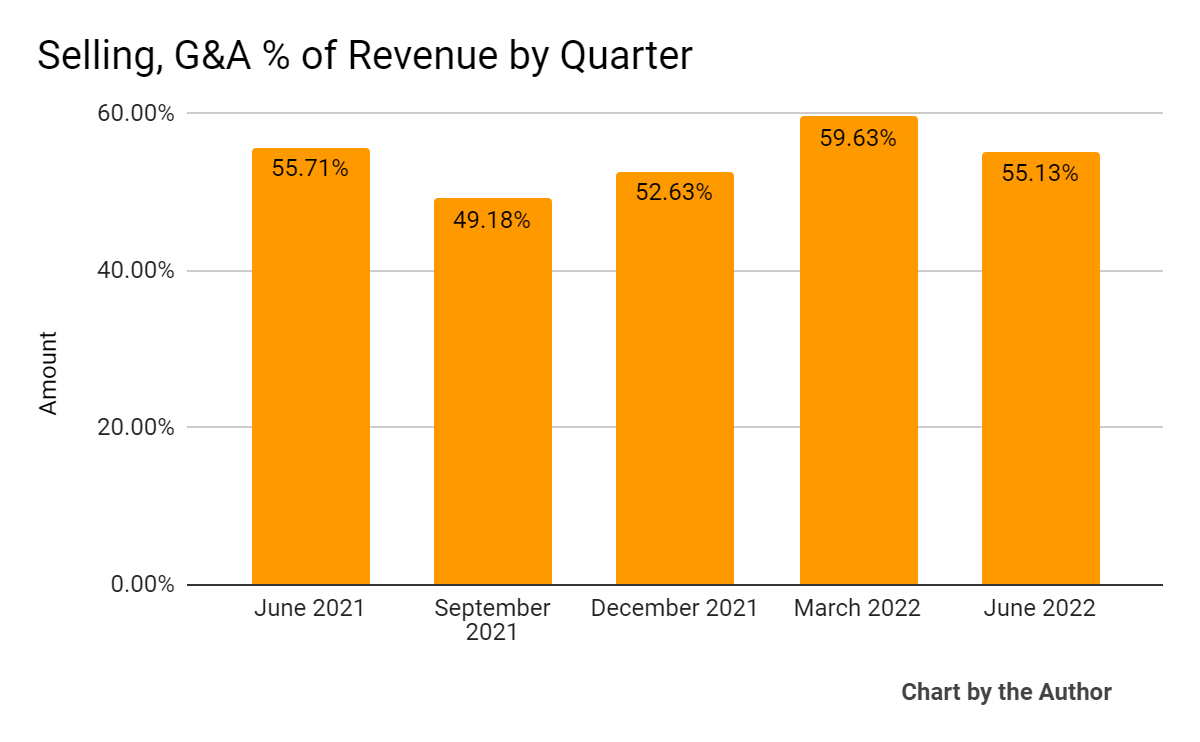

Selling, G&A expenses as a percentage of total revenue by quarter have varied within a relatively tight range over the past 5 quarters:

5 Quarter SG&A % Of Revenue (Seeking Alpha)

-

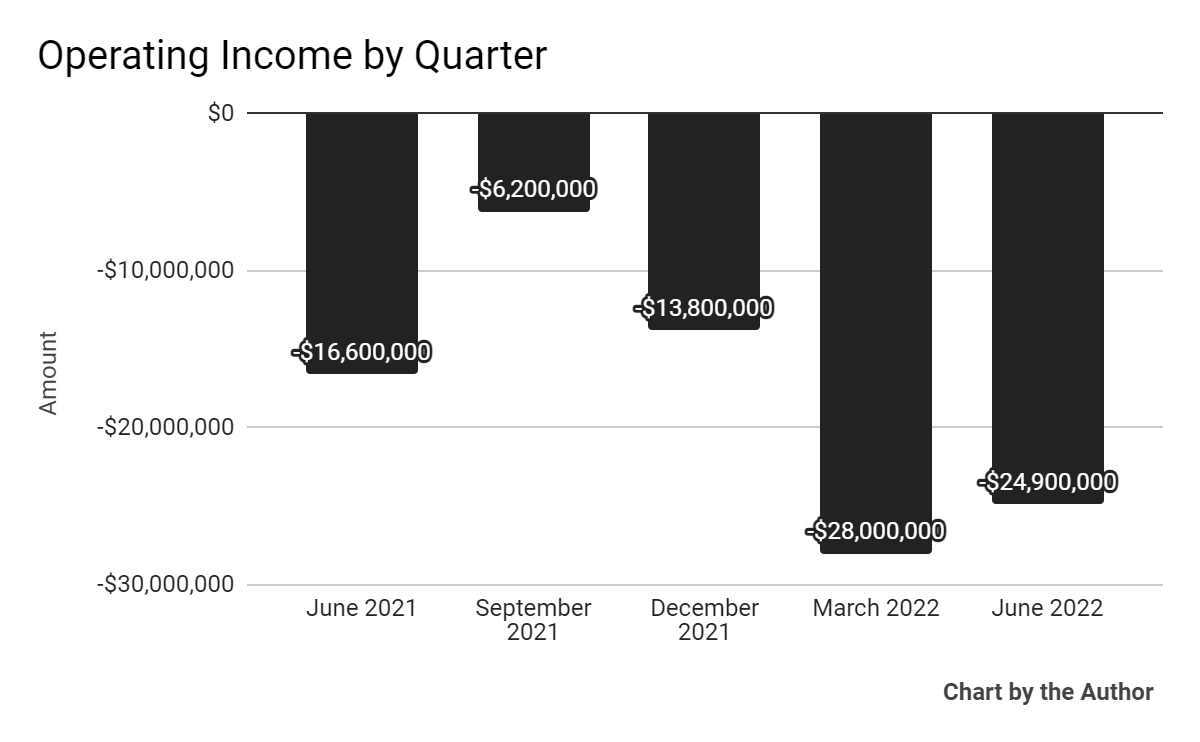

Operating losses quarter have worsened markedly in recent quarters:

5 Quarter Operating Income (Seeking Alpha)

-

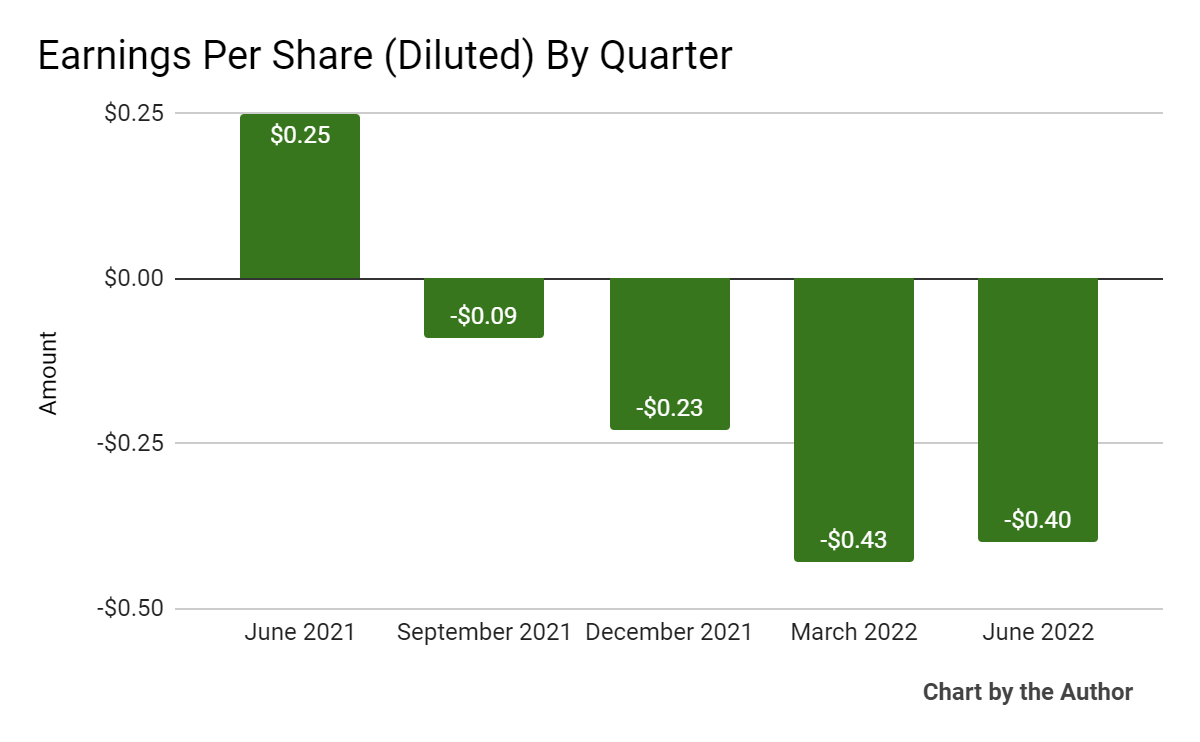

Earnings per share (Diluted) have also turned increasingly negative, as the chart shows below:

5 Quarter Earnings Per Share (Seeking Alpha)

(All data in above charts is GAAP)

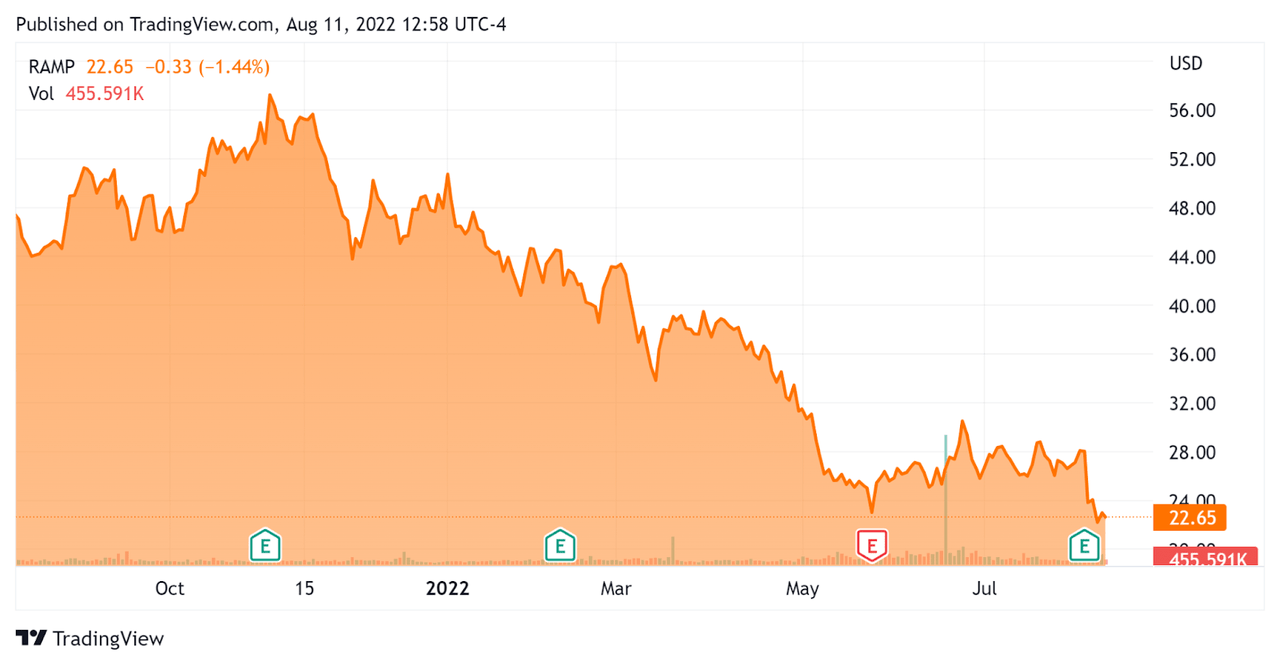

In the past 12 months, RAMP’s stock price has dropped 52.3% vs. the U.S. S&P 500 index’ fall of around 4.5%, as the chart below indicates:

52 Week Stock Price (Seeking Alpha)

Valuation And Other Metrics For LiveRamp

Below is a table of relevant capitalization and valuation figures for the company:

|

Enterprise Value |

$1,090,000,000 |

|

Market Capitalization |

$1,540,000,000 |

|

Enterprise Value / Sales |

1.97 |

|

Revenue Growth Rate |

19.3% |

|

Operating Cash Flow |

$61,950,000 |

|

Earnings Per Share (Fully Diluted) |

-$1.15 |

|

Net Income Margin |

-14.2% |

(Source – Seeking Alpha)

As a reference, a relevant partial public comparable would be Zeta Global Holdings Corp. (ZETA); shown below is a comparison of their primary valuation metrics:

|

Metric |

Zeta Global |

LiveRamp |

Variance |

|

Enterprise Value / Sales |

3.82 |

1.97 |

-48.4% |

|

Operating Cash Flow |

$66,940,000 |

$61,950,000 |

-7.5% |

|

Revenue Growth Rate |

22.8% |

19.3% |

-15.5% |

|

Net Income Margin |

-56.1% |

-14.2% |

-74.7% |

(Source – Seeking Alpha)

A full comparison of the two companies’ performance metrics may be viewed here.

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

RAMP’s most recent GAAP Rule of 40 calculation was 10% as of FQ1 2023, so the firm needs significant improvement in this regard, per the table below:

|

Rule of 40 – GAAP |

Calculation |

|

Recent Rev. Growth % |

19% |

|

GAAP EBITDA % |

-9% |

|

Total |

10% |

(Source – Seeking Alpha)

Commentary On LiveRamp

In its last earnings call (Source – Seeking Alpha), covering FQ1 2023’s results, management highlighted notable large deals but also said that it is seeing ‘recessionary concerns’ with customers which may put downward pressure on client decision processes related to data-enabled marketing spend and slow down sales cycles.

The company’s subscription net retention rate was 113% for the quarter, indicating negative net churn and efficient sales and marketing efforts to grow business within customer cohorts.

As to its financial results, the firm bettered guidance with total revenue growth of 19% but the quantity of net new additions were a disappointment.

However, operating losses remained elevated and management has grown cautious about the future, especially with its mid market clients where it is seeing increasingly lengthy sales cycles and lower conversion rates.

For the balance sheet, the firm finished the quarter with cash, equivalents and short term investments of $515.8 million with no long-term debt and it used $35.1 million in free cash flow [GAAP], although the quarter is historically a negative cash flow quarter.

Looking ahead, management lowered guidance due to reduced expectations on customer spend.

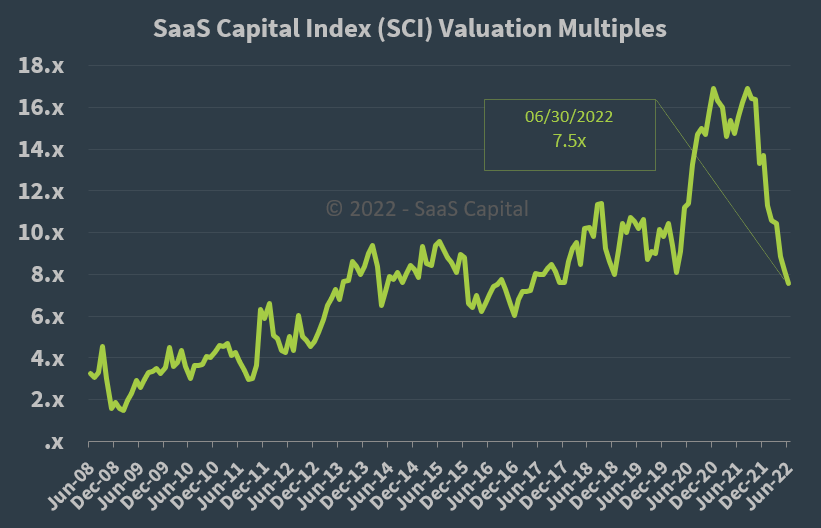

Regarding valuation, the market is valuing RAMP at an EV/Sales multiple of around 1.97x.

The SaaS Capital Index of publicly held SaaS software companies showed an average forward EV/Revenue multiple of around 7.5x at June 30, 2022, as the chart shows here:

SaaS Capital Index (SaaS Capital)

While RAMP is only partially a subscription company, it is currently valued by the market at a significant discount to the SaaS Capital Index, at least as of June 30, 2022.

A potential upside catalyst would be a ‘short and shallow’ economic downturn and the potential for a tapering of interest rate hike increases, reducing pressure on both its valuation multiple and negative earnings.

However, given uncertainties about the firm’s mid market customer base and its increasing operating losses, I’m on Hold for RAMP over the near term.

Be the first to comment