Mario Tama

Introduction

Live Nation Entertainment (NYSE:LYV) is a global entertainment company that operates in the live events and concert promotions industry. The company owns, operates, and partners with venues, promotes live events, and manages the careers of musicians. Live Nation Entertainment was formed in 2010 by the merger of Live Nation and Ticketmaster.

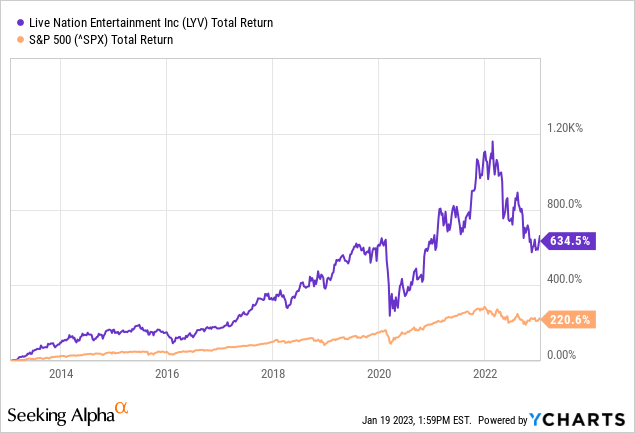

The stock has performed well, with a 10-year total return of 635% (22% annually on average), compared to only 221% for the S&P500 (12.4% annually on average).

The stock is declining as a result of potential headwinds such as the Department of Justice’s investigation. The recent pullback presents a buying opportunity, but I prefer to wait until the DoJ risk is reduced.

Earnings Are Recovering

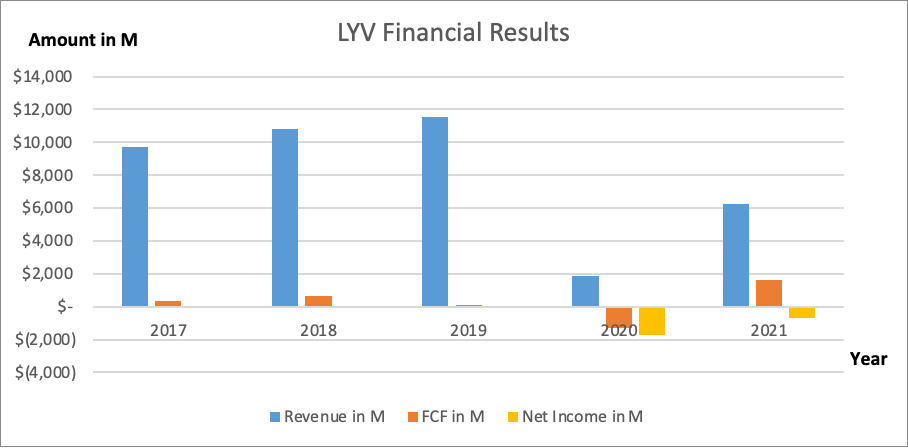

Revenue and earnings were rapidly recovering from the Corona crisis, with revenue increasing 128% in the third quarter of 2022. Operating income increased to $506 million in the third quarter, up from $137 million the same quarter in the previous year.

Looking at the big picture, Live Nation generated 9.2% annual revenue growth from 2017 to 2019. The reduction in revenue that occurred in 2020 was caused by corona measures, but it was followed by strong revenue growth in the years that followed. The company currently has a free cash flow margin of 9.4%.

Live Event’s Financial Figures (SEC and author’s own graphical representation)

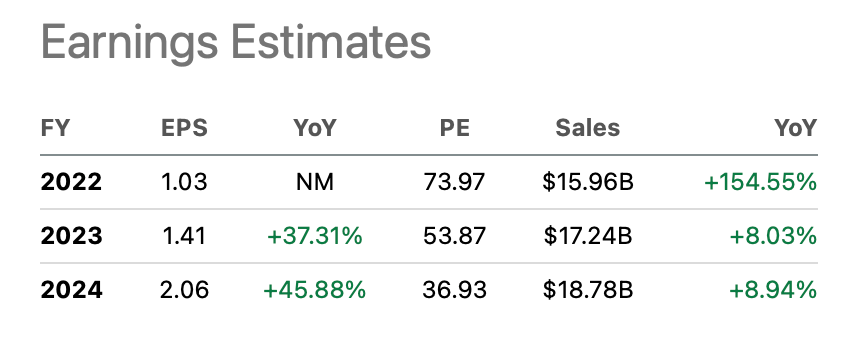

When we take a look in the crystal ball, we find that a number of analysts anticipate significant growth in earnings per share in the years to come. It is anticipated that there will be an 8% rise in sales over the next few years. But as can be seen in the figure below, forward PE ratios appear to be rather pricey.

Earnings Estimates (Seeking Alpha LYV Ticker Page)

Investors worry that Live Nation’s growth will be hindered by headwinds like higher cost of capital and the potential fallout from the Department of Justice’s inquiry, which could increase costs due to dis-synergies. Department of Justice officials have expressed interest in separating Live Nation and Ticketmaster.

The following is an excerpt from a letter sent to the DOJ by the Senate Judiciary Committee’s subcommittee on Competition Policy, Antitrust, and Consumer Rights:

Reports about system failures, increasing fees, and complaints of conduct that violate the consent decree Ticketmaster is under suggest that Ticketmaster continues to abuse its market positions.

Analysts’ reactions to the result were varied. Jason Bazinet gave the stock a buy recommendation and an $82 price target, or a 12% gain from current levels. It is only 20% likely, according to Jason Bazinet, that the company will split up.

The analyst estimated a $90 per share value for the company if it were to remain unchanged, but only $48 if it were forced to split. Jason Bazinet estimates that the firm would lose $100 million in dis-synergies after the split.

Stock’s Valuation Is Favorable

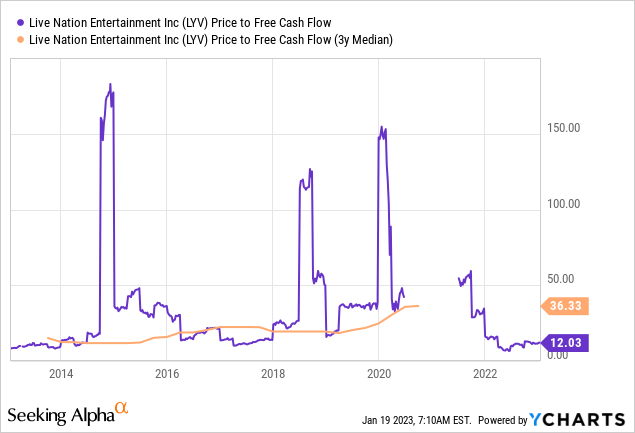

What most investors forget is to look beyond the PE ratio. Looking beyond the PE ratio, the stock appears to be cheaply valued based on the price to free cash flow ratio. Currently, the ratio is 12, which is low both in comparison to its historical valuation and in terms of its general attractiveness.

While it has a healthy free cash flow position, the company’s earnings performance has lagged behind. The current price-to-earnings ratio of 74 indicates that the stock is being valued at more than it is worth. Revenue and EPS are anticipated to grow rapidly over the next few years. The P/E ratio looking forward to 2024 is 37, which is quite high.

If we evaluate the stock price in light of cash flow metrics, the company appears to be undervalued. Live events, however, are vulnerable to economic risks. Now that a recession appears likely, I am putting Live Nation on hold.

Conclusion

Live Nation Entertainment is a global entertainment company that operates in the live events and concert promotions industry. The company was formed in 2010 by the merger of Live Nation and Ticketmaster. The stock has performed well, with a 10-year total return of 635% (22% annually on average) compared to only 221% for the S&P500. Live Nation’s stock is undervalued relative to its historical valuation. While it has a healthy free cash flow position, the company’s earnings performance has lagged behind.

Live events, however, are vulnerable to economic risks, and now that a recession appears likely, I am putting Live Nation on hold.

Be the first to comment