proxyminder/E+ via Getty Images

The major market averages were green across the board yesterday on news that a downtrend in the rate of inflation is firmly in place, which fueled a rise in the S&P 500 above its long-term moving average to test 4,000. Interest rates fell across the yield curve, as market participants reduced their expectations for additional rate increases. The light at the end of the inflationary tunnel is looking more and more like a soft landing. Yet a disgruntled bearish consensus continues riding on hopes that the Fed will follow through on its hawkish rhetoric by raising short-term rates above 5% and driving the economy into recession to bring down a rate of inflation they expect to remain stubbornly elevated. If that doesn’t doom the market, then eroding margins and earnings shortfalls are bound to drag stock prices down.

Finviz

I have consistently counseled investors to focus on what the Federal Reserve does rather than what Fed officials say they will do for two reasons. The first is that they have a horrible track record in predicting their own actions, much less developments in the real economy, and the second is that they have been fighting a battle with expectations as much as with inflation over the past year. It is a conundrum for the central bank in its attempt to navigate a soft landing for the economy by tightening financial conditions without its incremental achievements evoking enthusiasm for risk assets, which thereby loosens financial conditions before its job is done.

Bloomberg

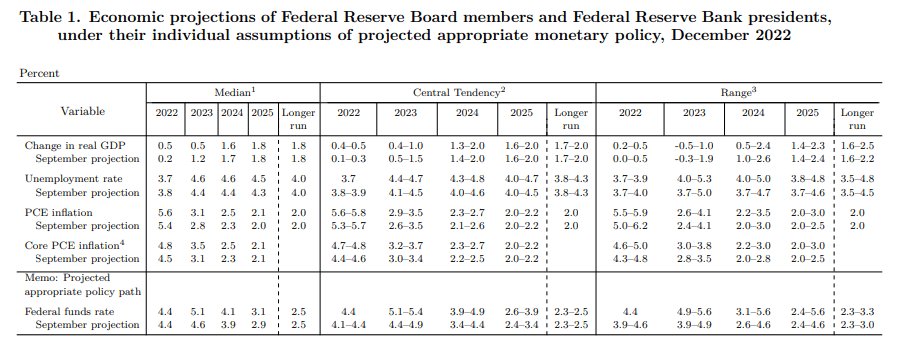

This is why I continue to listen to the market for direction when it comes to short-term interest rates, economic growth, and stock prices. Chairman Powell may continue to express concern about a tight labor market and still strong wage growth, but if the Fed’s preferred rate of inflation falls within the 2-3% targeted range without a significant rise in the unemployment rate, which is my expectation, then those are misplaced concerns. I think he is trying to jawbone the market. By the same token, Fed officials are likely to continue asserting that short-term rates will rise above 5% and stay there all year long, but that rhetoric is designed to cap risk asset prices. I also think this is why the Fed increased its forecast for the year-end rate of inflation (PCE core) for 2022 from 4.5% to 4.8% last month, despite a CPI report the day before that suggested a much lower number was possible. That was confirmed by the PCE report later in December, as well as yesterday’s CPI report. In its next Summary of Economic Projections update, the Fed will have to lower that 4.8% back to 4.5%, which should force it to lower its year-end 2023 target as well from 3.1% to 2.8% or lower.

Federal Reserve

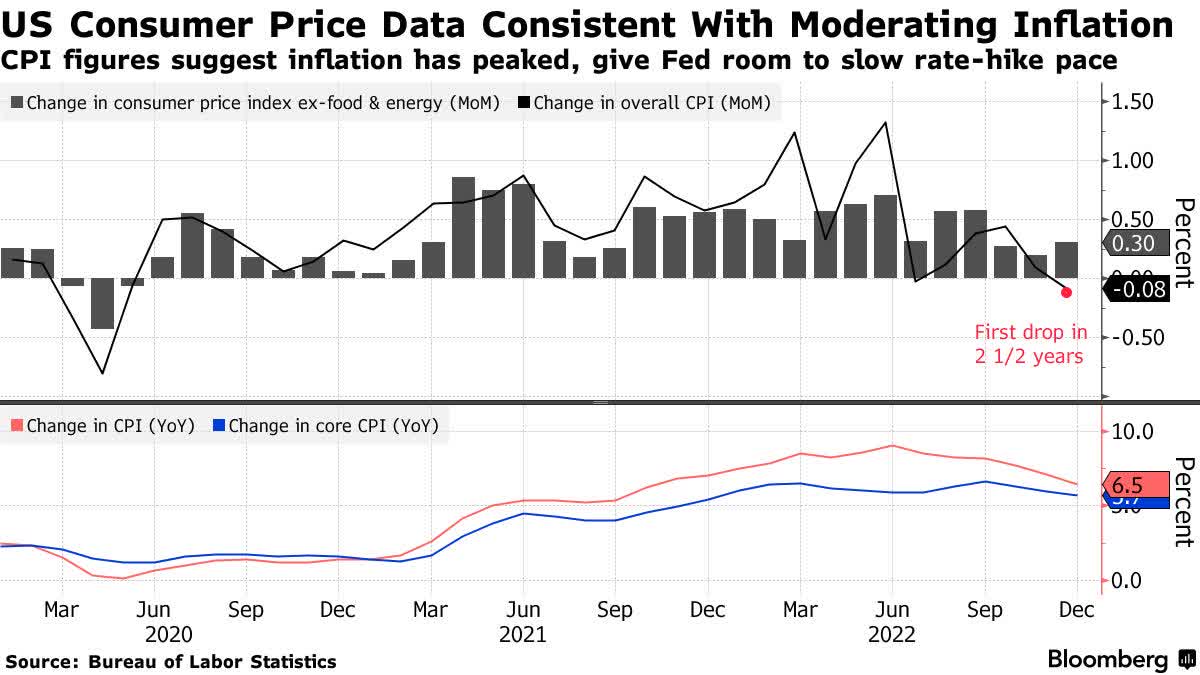

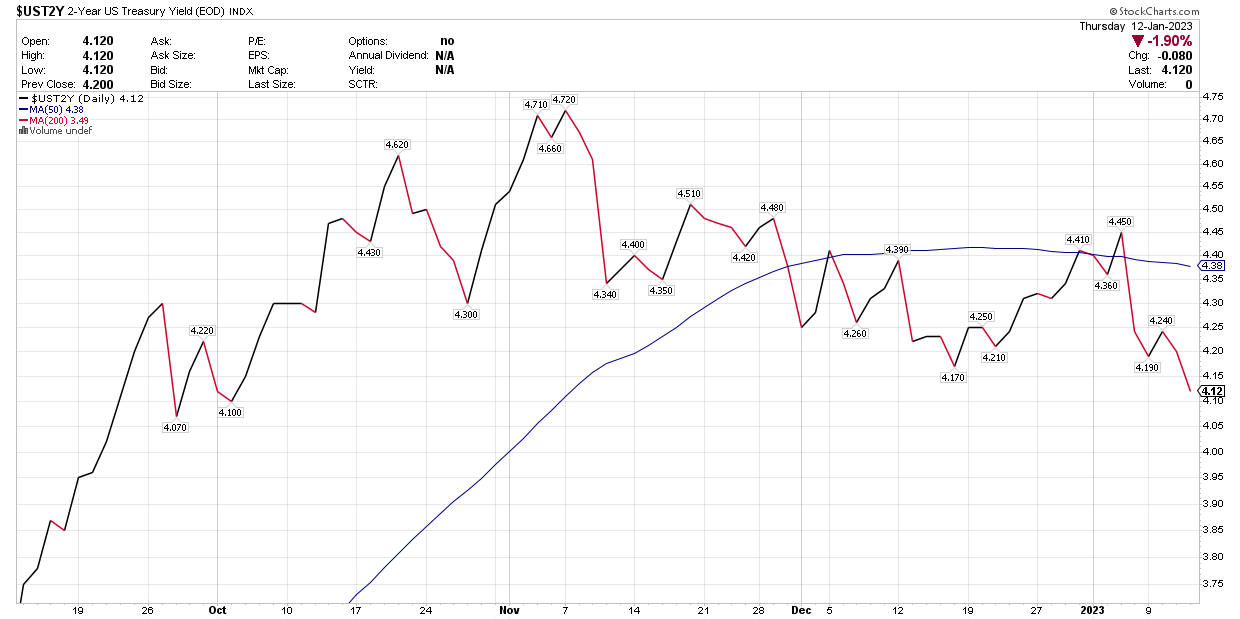

The reason yesterday’s report was received so well by investors, despite the Fed rhetoric that followed, is that the monthly increases for the headline and core rates of inflation have fallen back within their pre-pandemic range of -0.1 and +0.4. The peaks for both in 2022 were 1.3% and 0.9%. This is why the bond market is saying that the Fed does not need to keep raising interest rates and that they are likely to be no higher a year from now than they are today. The 2-year yield has been in a downtrend since November, falling to a new low yesterday of 4.12%. A Fed Funds rate of 5% is increasingly unlikely.

Stockcharts

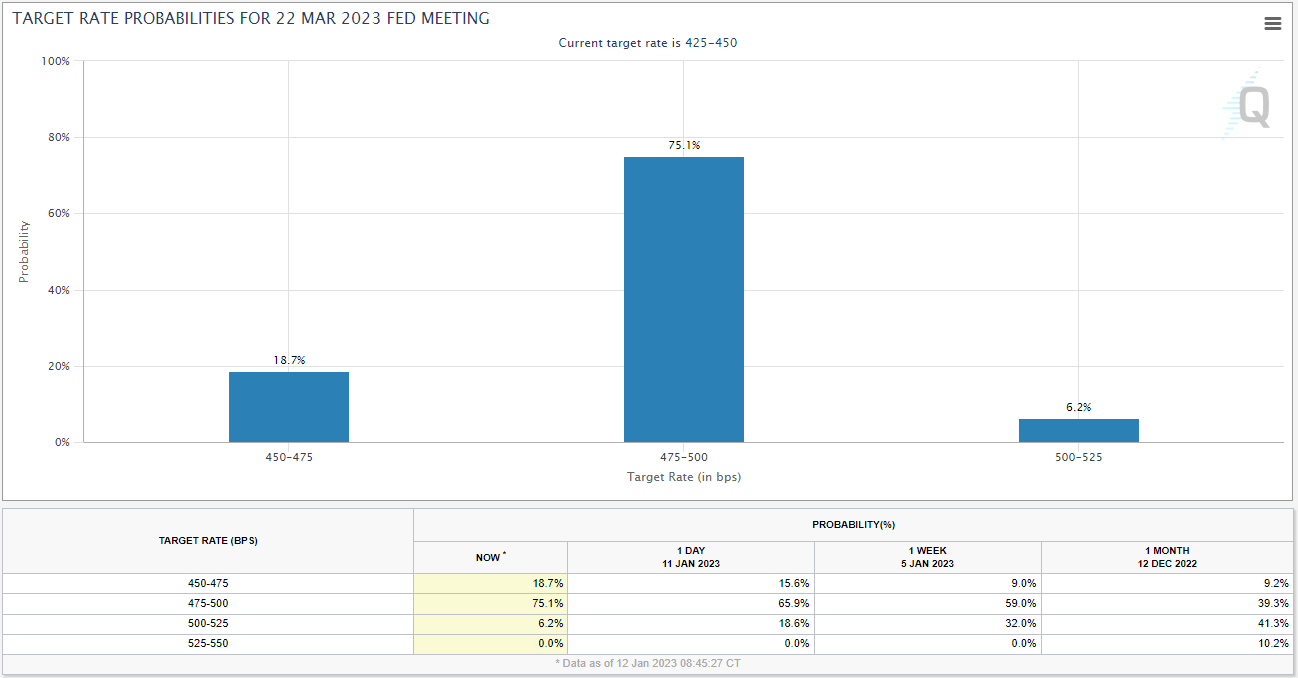

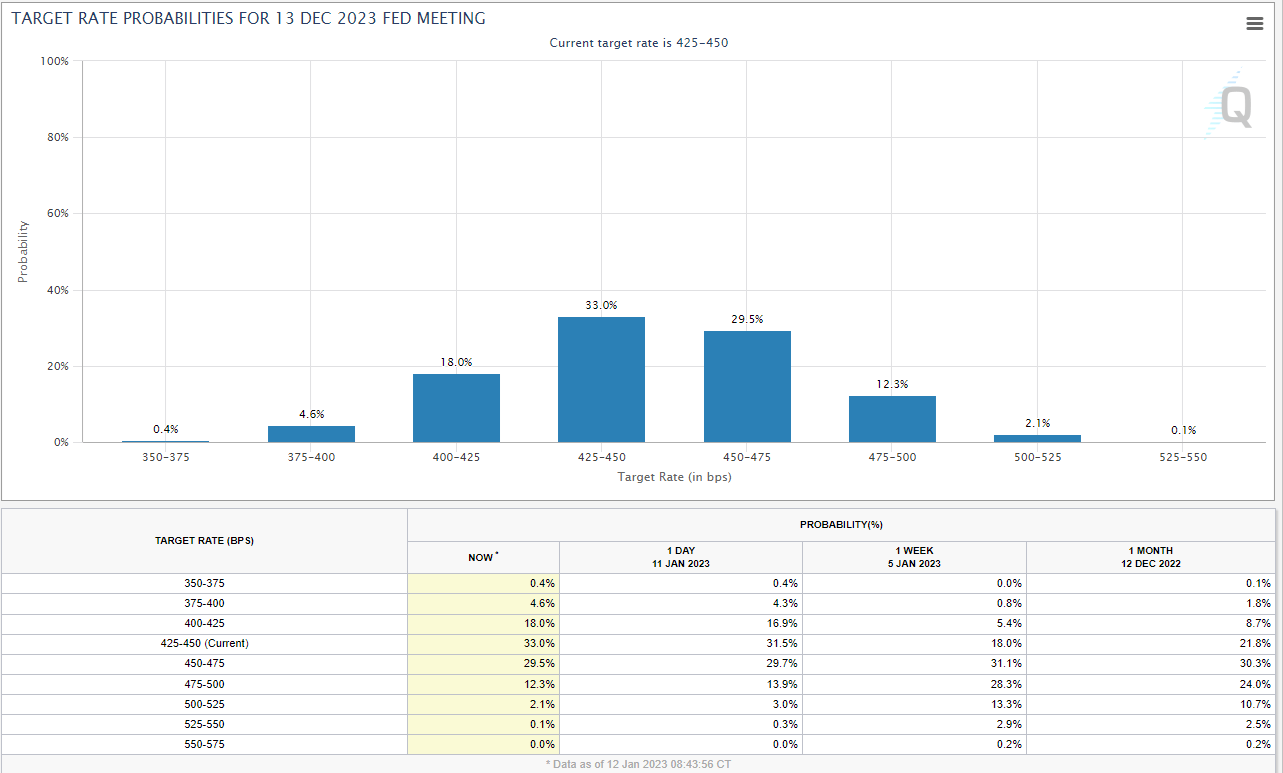

Prior to November’s Consumer Price Index report, the consensus was expecting another 100 basis points of short-term rate increases with 50 to come in February and 50 in March. It was my expectation that the Fed was done raising interest rates, which is what fueled my optimism for the economy and markets at that time. Those numbers were cut in half to 25 basis points at each meeting after the November report. The Fed has tried to battle those expectations ever since, but after yesterday’s CPI report those probabilities have only grown and there remains a near-20% chance that February’s 25-basis-point hike will be the last.

CME

Additionally, the probability that short-term rates are no higher at year end than they are today continues to grow and be consensus. This suggests that the Fed will be reversing any additional rate hikes later in the year.

CME

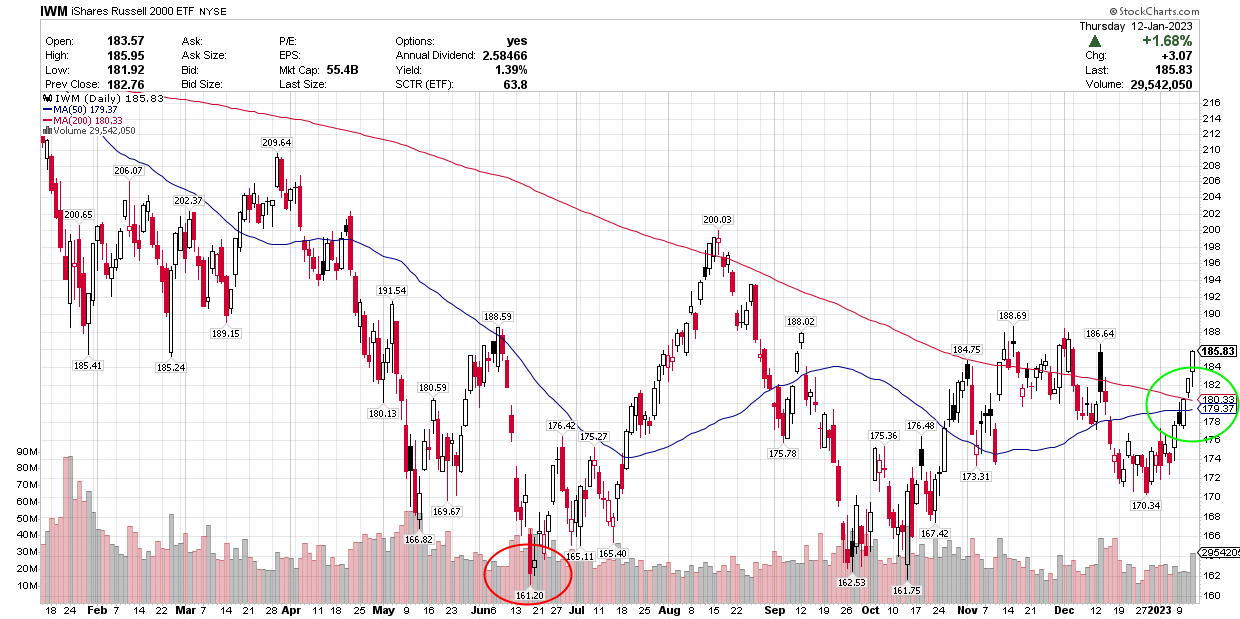

This explains the S&P 500’s outperformance over the past three months off its October low, but there were signs earlier than that suggesting we were on the mend. I think the more domestically-focused Russell 2000 small cap index has been telling us as far back as last summer that the macroeconomic landscape was becoming less bad month after month. The Russell bottomed last June, which coincided with the 9.1% peak in the rate of inflation. I don’t think that is a coincidence. It has been outperforming ever since and climbed above its 200-day moving average this year with two higher bottoms behind it. The 50-day moving average is close to climbing above its 200-day, which would be a very positive development for the longer term. This is not what you typically see when the economy is on the cusp of a recession and new bear-market lows are approaching. I think I am going to keep listening to the market.

Stockcharts

Be the first to comment