Gary Yeowell

Liberty TripAdvisor Holdings Amid Challenging Outlook for Travel and Leisure Tourism Industry

Many companies in the travel and leisure tourism activities sectors have not fully recovered from the crisis caused by the COVID-19 virus infection amid a highly uncertain outlook due to skyrocketing fuel prices coupled with inflation and an economic slowdown.

With that in mind, investors should reconsider some of their holdings in companies involved in travel and leisure, starting with Liberty TripAdvisor Holdings, Inc. (NASDAQ:LTRPA).

This stock represents a company with a weak balance sheet that has little chance of improving as the company is far from being sufficiently profitable while growth prospects are hampered by a challenging outlook.

Overall, investors should consider softening their position in Liberty TripAdvisor Holdings. But if the sale of shares of Liberty TripAdvisor Holdings involves a significant loss, investors may also want to know that the alternative of holding the position still offers the opportunity to take advantage of a possible, albeit low probable, scenario.

About Liberty TripAdvisor Holdings, Inc.

Headquartered in Englewood, Colorado, Liberty TripAdvisor Holdings operates a travel advisory platform that connects travelers with travel partners.

Liberty TripAdvisor Holdings’ travel platform provides content and the ability to compare prices and make online reservations. Prospective travelers can also use various related services for travel destinations, accommodation, travel activities and experiences, and restaurants.

Liberty TripAdvisor Holdings also owns and operates online travel advisory brands and companies that provide travel planning and travel resources in the travel industry.

The company offers click and display-based advertising services in addition to subscription-based advertising services.

In order to sum up, Liberty TripAdvisor Holdings operates through the TripAdvisor Core segment, which includes sub-segments, Hotels, Media & Platform, and Experiences & Hospitality, as well as through the Viator and TheFork websites segment.

Viator is a website that offers search and booking services and experience activities in addition to attractions in travel destinations, while The Fork is an online restaurant reservation platform.

TripAdvisor Core accounted for 58%, while Viator and TheFork together accounted for the remaining 42% of total revenue for Q3 2022. While Hotels, Media & Platforms accounted for 78% of the total TripAdvisor Core segment, Experiences & Hospitality accounted for 22.2% of the total TripAdvisor Core segment.

How Liberty TripAdvisor Holdings Is Performing

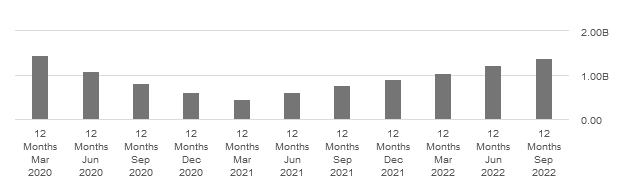

At first glance, Liberty TripAdvisor Holdings’ platform appears to be performing well, with revenue up 51.5% year over year and 10% sequentially for the third quarter of 2022 to $459 million.

However, when comparing the data for the third quarter of 2022 to a corresponding period before the pandemic, the growth does not represent a large improvement in revenues. That probably doesn’t please analysts, who would likely have instead hoped for a significant increase in revenue to boost the profitability of Liberty TripAdvisor Holdings’ business.

In fact, Q3 2022 revenue of $459 million is only slightly higher than Q3 2019 revenue of $428 million while close to Q3 2018 revenue of $458 million.

The chart below, which compares sales over 12 months, is a much better indication of a trend that likely still does not fully reassure shareholders, as pressured by an economy with low growth prospects and high inflation, it struggles to gain momentum after the COVID-19 crisis.

Source: Seeking Alpha

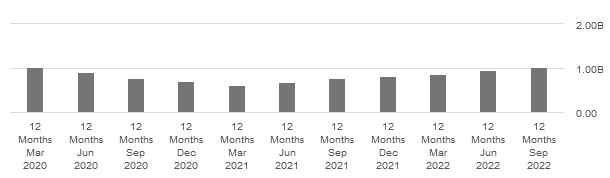

So while revenue is being challenged by shrinking consumption due to high inflation and massive job cuts, particularly in the tech industry, Liberty TripAdvisor Holdings’ total operating expenses appear to be increasing dramatically, and the combination of these two factors certainly cannot be positive, as it affects the company’s ability to generate profits.

The TTM total operating expenses for Q3 2022 were $1.03 billion, a year-on-year increase of 33.55% and an 8.7% increase sequentially, as the graphic below illustrates.

Source: Seeking Alpha

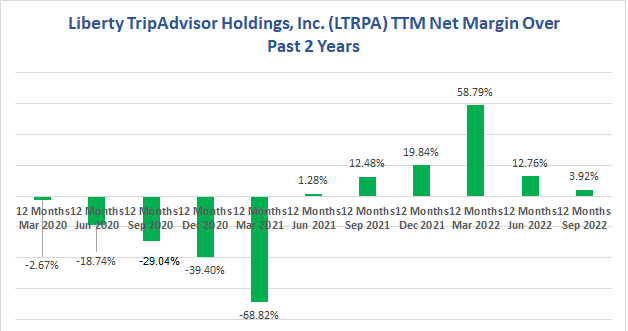

In terms of net income, Liberty TripAdvisor ended the third quarter of 2022 with a loss of $0.39 per common share compared to a net income of $0.95 per share in the third quarter of 2021.

Liberty TripAdvisor Holdings’ TTM net margin, which is an indicator of profitability, has declined significantly in the past two quarters following the strong recovery due to the lifting of restrictions on activities to contain the spread of the COVID-19 infection.

Data Source: Seeking Alpha

That level of profitability does not help to improve the financial situation that is currently plaguing shareholders.

The Financial Condition

As of September 30, 2022, the balance sheet showed cash and cash equivalents of $1.1 billion against total debt of $1.35 billion.

Approximately 97% of the total cash is held by the company’s subsidiary, TripAdvisor, and this cash can only be made available to the consolidated company if approved by TripAdvisor’s minority shareholders as well. This is because the consolidated company’s economic interest in TripAdvisor does not currently result in any power of control over the subsidiary.

Instead, as a result of the outstanding debt, Liberty TripAdvisor Holdings incurred $66 million in TTM interest expense as of Q3 2022. TTM interest expense versus TTM operating income of $50 million gives a TTM interest coverage ratio of 0.76. This is below the widely accepted threshold of 1.5, suggesting that the company may struggle to meet its financial obligations as they mature on outstanding debt.

Two other indices are worrying Liberty TripAdvisor Holdings shareholders. One is the Altman Z-Score of 0.44, meaning the company’s balance sheet is in serious financial difficulties with a risk of bankruptcy to occur within 2 years, and the second is the comparison between the weighted average cost of capital (WACC) of 3.6% and the return on the invested capital (ROIC) of 0.84%.

The WACC to ROIC ratio implies the following consideration.

The investment entails financial costs that are currently barely covered by the returns achievable on the investment, so any attempt to grow the business at this point does not create value for the shareholder but arguably destroys it.

If the company wants to expand the business while making it significantly more efficient, it needs capital to upgrade its portfolio of operations.

Currently, this situation faces two major obstacles, namely the high cost of borrowing in the markets and the uncertain economic outlook, which will likely weigh on travel and holiday bookings.

The near-term perspective presents challenges that appear to be beyond Liberty TripAdvisor Holdings, Inc.’s actual capabilities, thus weighing on the company’s growth plans.

As such, any potential setback in the company’s strategy to evolve into a more profitable operation currently carries a significant risk that the stock price could be materially impacted.

The Stock Valuation

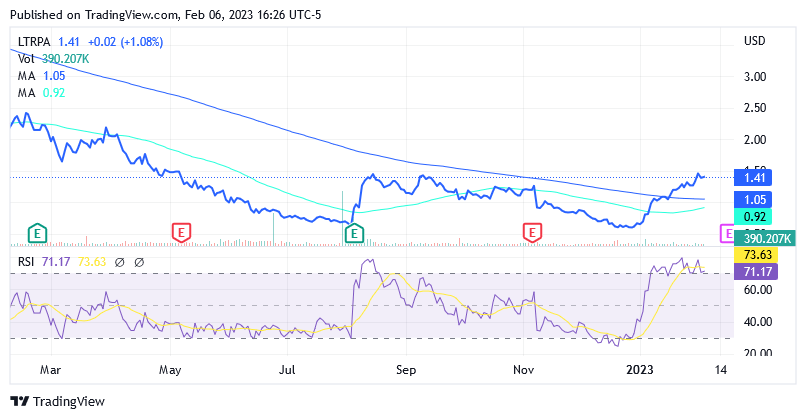

Shares of class A common stock of Liberty TripAdvisor Holdings, Inc. traded at $1.41 for a market cap of $191.25 million as of this writing.

Source: Seeking Alpha

Shares are not cheap as, following a 110% increase so far this year, they are trading above the 200-, 100- and 50-day simple moving average lines. Shares are still below the middle point of the 52 Week Range of $0.57 to $2.47.

The 14-day relative strength indicator of 71.17 suggests that stocks have reached an overbought level and could be ready to pull back.

The class B common stock traded at $26 per share for a market cap of $180.09 million. Shares are slightly below the 50-Day Moving Average of $26.56 but above the 200-Day Moving Average of $23.33. The class B common stock has a 52-week range of $8.43 to $93.67. However, class B common stock has a very low volume of shares traded daily.

Liberty TripAdvisor Holdings’ class A common stock, which is more likely to underperform than improve from current levels, represents a significant investment risk that should guide an investor’s decision not to further add to the position given a possible future scenario of economic slowdown, persistent inflation and expensive borrowing.

It is not out of this world to speculate that the negative impact of a probable recession and other unfavorable macroeconomic factors could impact Liberty TripAdvisor Holdings’ future share price. So, it wouldn’t hurt if the investor, along with owning shares of this company, also considers the possibility to lighten his position and focus on assets that currently offer better prospects.

Liberty TripAdvisor Holdings’ stock has not received any ratings for a while, which could mean that analysts are very undecided about what to recommend and this situation will not help anyone who needs to make an investment decision on this stock today.

Liberty TripAdvisor Holdings is traded on the NASDAQ Global Select Market, one of the three tiers of NASDAQ, the index of America’s leading technology stocks and the premier US stock exchange.

Yahoo Finance states that Liberty TripAdvisor Holdings has a 5-month beta of 1.98x, suggesting the stock is positively correlated with the NASDAQ Global Select Market and is more volatile than the market.

Analysts don’t expect this market to perform well into 2023, and this forecast combined with the 1.98x beta could provide further insight into the future performance of Liberty TripAdvisor Holdings’ share price.

As a benchmark for the NASDAQ Global Select Market, investors should consider the US Tech 100 Index, which summarizes the performance of the 100 largest publicly traded US technology stocks.

From current levels, the US Tech 100 index is set to fall another 2% by the end of this quarter and another 11.5% by the end of 2023, according to Trading Economics global macro models and analyst forecasts.

This means Liberty TripAdvisor Holdings could start a quick decline as it tends to double the impact of changes in the technology stock market based on the 5-month beta. So unless it is a loss that is difficult to recoup through other deals in the financial markets, investors might also consider selling shares of Liberty TripAdvisor Holdings.

Otherwise, investors may choose to Hold the stock and bet on the upside potential that could emerge, should the following bullish scenario for the NASDAQ Global Select Market occur. Contrary to Trading Economics’ forecasts, the market could potentially be positive about Wall Street’s downward revision of corporate earnings for big tech companies as growth plans were scaled back due to higher borrowing costs. As big tech companies make dramatic staff cuts, which is relevant since labor costs account for a significant portion of total operating expenses, they should stand a better chance of beating Wall Street analysts, who have since lowered their future earnings estimates.

The beat should be positive for market valuations of NASDAQ Global Select Market stocks, generating tailwinds for Liberty TripAdvisor Holdings’ shares as well.

This event is of course not certain and the risk that it will not occur is not small given the heightened market volatility due to geopolitical issues and tensions between countries, as well as known macroeconomic factors.

Still, it would be worth owning shares of Liberty TripAdvisor Holdings if the alternative is to take a heavy loss by selling this stock with shaky finances and uncertain growth prospects.

However, the investor, who may choose to keep Liberty TripAdvisor Holdings in his portfolio, is urged to heed the monetary policy decisions of the US and European central banks.

This is highly recommended given the latest updates showing the US economy added 517k jobs (vs 188k est.) and the first expansion in Germany’s services sector after seven months of contraction.

If central banks aggressively raise borrowing costs based on this data, which indicates anything but an economic recession, it could hurt market sentiment towards technology companies like Liberty TripAdvisor Holdings. And the resulting headwinds of concerns that the stocks’ net present values might be below market valuations would reduce the chances of success for the decision to Hold the stock in the portfolio.

On the other hand, a Hold rating would be more likely to succeed if upcoming speeches from policymakers caused central banks to consider cumulative monetary tightening and the lags with which the hawkish policy affects economic activity and inflation. In that case, the US Federal Reserve and the European Central Bank will make further rate hikes, but with more muted increases.

Conclusion

Liberty TripAdvisor Holdings is in a precarious financial situation that urgently needs to be improved, but neither its operating activities from a profitability perspective nor today’s growth prospects provide favorable conditions for achieving the goal. With that in mind, shareholders might want to sell the shares, but if that couldn’t be done without incurring huge losses, there is still a small possibility of taking advantage of a favorable scenario by holding the position.

Be the first to comment