Henrik Sorensen/DigitalVision via Getty Images Levered Insight

Suspended Disbelief

“To allow oneself to believe things that cannot be true” according to Websters. 2022 was a great reminder of the cyclicality of human nature toward this idiom and the frauds and bubbles that are perpetrated during feverish periods. We witnessed the unraveling of the $10 billion fraud at Sam Bankman-Fried’s cryptocurrency empire, FTX, and the long-awaited sentencing of Elizabeth Holmes, CEO of Theranos, the fraudulent blood testing company. One does not have to go back very far to remember Bernie Madoff’s Ponzi scheme (2008) or the Enron scandal (2001). Or one can be reminded of the housing bubble (2008), dot-com bubble (2000), Nifty 50 bubble (1969) or go way back to the Dutch Tulip Bulb bubble (1637), South Sea bubble (1720) as evidence for the durability of suspended disbelief and the ingenuity of fraudsters and those with a vested interest in promoting bubbles. For an excellent podcast from the Financial Times of the South Sea and Mississippi bubbles, John Law, and their parallels to today, click here.

This consistency in human nature is no doubt one of our flaws. Greed comes to mind, of course, but it is envy that is the more deadly. We simply cannot stand it when our neighbors and friends appear to be making easy money in the “future’s obvious winners”. After all, we’re as smart or smarter than them. We are also being whispered to by friends and family, along with celebrities and fraudsters, about these amazing opportunities. “Fortune Favors the Brave” according to actor Matt Damon. “I’m in! You in?” says NFL quarterback Tom Brady and model ex-wife Gisele Bundchen (referring to buying crypto with FTX). Some other great closing investment lines include “housing prices always go up”, or “crypto will protect you from the Fed debasing our currency”.

Of course, as Warren Buffet quipped, “Only when the tide goes out that you discover who’s been swimming naked”. Fraud and bubbles are usually exposed when the investment tide goes out. Collateral values fall and force leveraged investors to reckon with their capital holes. Well, the tide went out in 2022! The Federal Reserve aggressively raised the Fed Funds rate, and many are expecting no pause until it reaches at least 5%. Long duration assets took a beating this year as higher interest rates pummeled values through the discounting process. For the first time in 15 years, fixed income now actually competes with equities in asset allocation frameworks.

As for Levered Insight, we sidestepped most of the market’s mayhem and eked out a positive return for the year. Our heavy weighting in the energy space was rewarded and short selling was a profitable exercise this year. We also believe the new reality for investors will be lower P/E’s and more free cash flow certainty as the price of money is now dearer than it has been over the past 15 years. “What is your path to profitability or exit” will likely be the operative phrase for some time to come. Simply put, business models will have to prove themselves. This backdrop should continue to reward value-based investment strategies on a relative basis. Howard Marks, the legendary investor and commentator with Oaktree Capital Management, recently penned an excellent letter to this effect entitled Sea-Change. I implore you to read this memo!

Musings on Inflation

Vats of ink, traditional and digital, have been spilled on the topic of inflation. Since it is a pivotal issue for asset values, here are my thoughts. I lean toward the camp that most of the increase in the rate of inflation over the past two years will prove transitory. The global Covid pandemic did a few things. First, it slowed or halted existing supply chains. This created a panic among purchasing managers to get raw materials “at any cost” and led to double-ordering (semiconductors) and overpaying for goods (logistics costs also jumped exponentially). Within a year of the outbreak, Western societies, which had abruptly closed businesses and schools, discovered and produced vaccines to slow the spread and lethality of the disease. This led to the eventual reopening of economies and resulted in huge swings in demand, first downward, and then massively upward compared with supply lines that have been more sluggish to return to pre-pandemic levels. Adding fuel to the fire was government stimulus money in the form of the Payment Protection Program of the Cares Act which put money in businesses pockets as well as direct payments to individuals. As business came back, employees did not. The unemployment rate (3.7%, near an all-time low) and JOLTS data – which peaked back in March and is down 13% from that peak – continue to suggest both a very tight labor market but also signs of improvement in the logjam as the economy slows. Noted economist Paul Krugman wrestles with the data and leans toward a similar conclusion in a recent NY Times Op-Ed.

Wall Street Journal

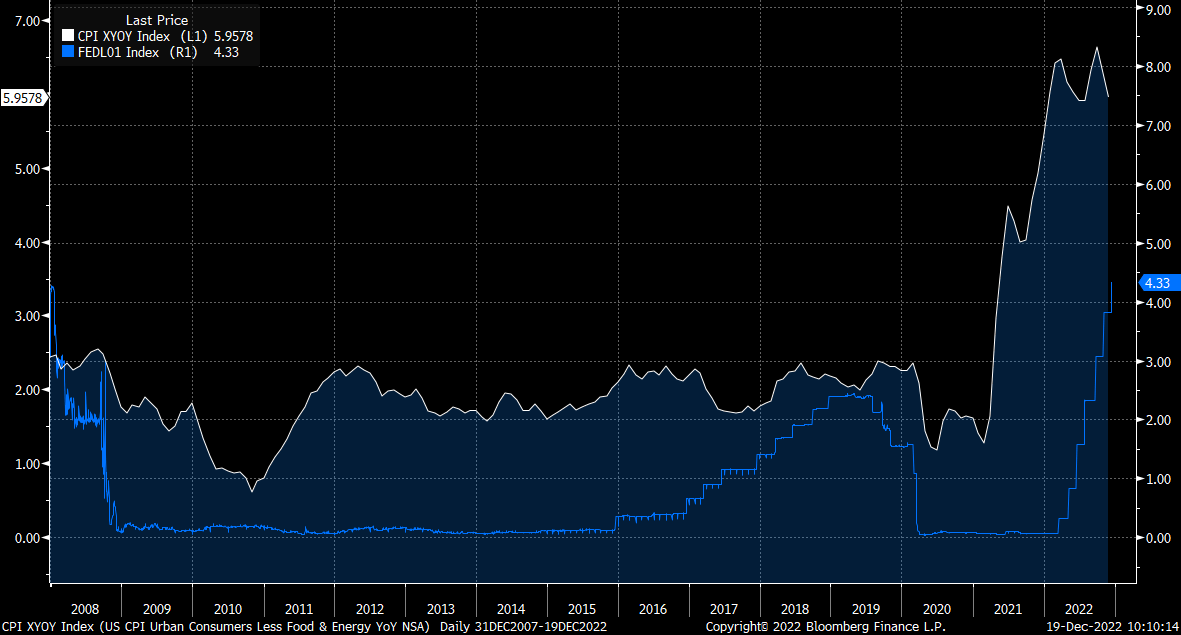

Going forward, the stickier portions of the economy, namely wages and service inflation, rather than the goods side, are going to take more time to recede back and contribute to the Fed’s goal of 2% inflation. However, along with the rise in interest rates, low birth rates, aging demographics, and slowing productivity will work to undermine rampant service cost inflation. One countervailing force is de-globalization that will continue to create higher costs for businesses. It feels to me that a 0.2% growth in the prime working population growth + 1.0% productivity + 2.5% to 3.0% inflation rate gets us to a 3.7% – 4.2% nominal GDP growth and a similar 10-Year US Treasury yield. The fixed income markets appear to have recognized and largely priced these structural changes. Any dramatic decline in yields from current levels – due to recessionary fears or a Fed pivot would be a reason to lighten up on bonds. The equity markets have started to normalize to the new reality except for a few mega-cap tech companies.

Inflation, and more importantly, inflation expectations, operate with long lags relative to monetary policy and financial exuberance. Chairman of the Fed, Jerome Powell, has been right to not give any oxygen to softening his stance of inflation. Past Chairman Paul Volcker raised rates to over 19% to slay the inflation dragon in 1981! It is the most insidious and corrosive of problems that undermines capital formation and valuation. We’ll see whether inflation can come under control. My two cents – let’s make that three cents (inflation!) – is that it will subside.

CPI Non-Food and Energy v. Fed Funds Rate

Bloomberg

Top 2022 Contributors

Office Depot (ODP +16%)

ODP proved resilient in 2022 despite its mid-year swoon. The company fended off a low ball $40/share offer from Sycamore Partners (owner of Staples – a competing office supply store chain and better organized its businesses into its retail office supply store fleet, corporate office supply business, and two supply chain and purchasing divisions serving broad end markets. Taking advantage of its tremendous balance sheet, management announced over $1.0 billion in share buybacks over the next few years, including $300 million in accelerated share repurchases. ODP also announced a three-year earnings projection of $7-$8/share by 2025 in its Investor Day Presentation. It remains one of our largest positions.

Energy Transfer (ET +56%)

ET is one of the largest natural gas, LNG, and oil pipeline and storage companies in the U.S. The stock correlated with strong oil and gas prices even though 85%-90% of revenues are contracted at fixed margins without reference to the underlying commodity price. ET cut its dividend late in 2020 as it digested large acquisitions and associated debt. ET has since substantially cut its growth capital spending in favor of debt reduction. They have increased the dividend 70% since February as free cash flow accelerates. With a dividend yield of 9% and free cash flow continuing to accrue toward debt reduction, ET’s equity value continues to look attractively valued.

New Fortress Energy (NFE +77%)

NFE’s historical business of creating offloading liquefied natural gas (LNG) facilities in countries that import dirtier fuels to run their electricity services was turbocharged after Russia invaded Ukraine. Suddenly, European countries dependent on Russian gas turned their efforts to secure LNG from other sources. NFE stands to benefit from its Fast LNG program. Fast LNG is a constructed sourcing, cleaning, and liquefaction facility that sits on top of a floating or fixed offshore rig. Cryogenic ships can onload LNG cargo and sail to their destinations in a more timely and lower cost manner. As China opens from its Covid lockdowns, the global competitive demand for LNG will be substantial, with Russia remaining a pariah on the energy stage for decades to come. NFE’s CEO Wes Edens has grown NFE at an aggressive clip and is now shifting some of its capital allocation toward dividends ($3/share in January and a 40% of adjusted EBITDA payout ratio over time). The stock price is volatile given the lack of history at the company, allowing us to effectively trade around our position.

Top Detractors YTD

Intel (INTC -47%)

We sold our Intel position at a large loss earlier this year but repurchased the company after the associated wash sale period had cleared. There is no doubt that CEO, Pat Gelsinger, is undertaking a herculean task in ramping up spending on new fabs with cutting edge technology as well as taking on Taiwan Semiconductor (TSM) as the supplier of choice for fabless semiconductor designers. INTC had no choice. They lost share in the PC and graphics markets to AMD and Nvidia as well as the technology poll position in nanometer wafers to TSMC. There are several “green shoots” that are underemphasized, in my opinion. Namely, their 95% interest in automotive sensor company Mobileye, co-funding opportunities from private equity partner Brookfield Infrastructure Partners, and outright grants under the Chips Act passed in 2022. While a potential recession looms near term, INTC is solidifying its position as one of the top 3 global semiconductor manufacturing companies while the long-term demand and ubiquity for semiconductors should continue for decades.

Lumen Technologies (LUMN -56%)

“First loss, best loss” is a trader’s maxim that would have saved a boat load of money for the Fund. Lumen announced its long-expected dividend elimination to fund growth initiatives. We were enamored with the idea that its fiber backbone, so well placed for edge-computing, would yield more revenue traction and asset value protection. Watching revenues fall and fall again, despite management’s guidance, should have tipped us off earlier. The CEO transition to Kate Johnson, a seasoned executive from Microsoft, cemented the capital allocation pivot and dividend elimination. We will keep our eye on her progress, but from the sidelines for now.

Citigroup (C -22%)

C remains the most undervalued money center bank in the U.S., trading at 54% of tangible book value per share ($80.34/share at 3Q 2022). It didn’t gain this notoriety without trying. Most recently, it was the only bank of the 8 majors to fail a regulatory “living will” analysis that cited its inability to produce financial data in periods of distress. This after being exonerated from a “fat finger” mistake that forked over $500 million in principle to Revlon bond holders rather than just a quarterly interest payment (Revlon is in bankruptcy). To be sure, technology spending at C will remain high for years to come. New CEO Jane Frazier has committed as much. Further, C is retrenching from many of its money losing or poorly positioned international markets. The biggest prize will be the sale of its Mexican assets early next year. C’s capital position overall remains strong and tangible book value could be an intermediate stopping point to bigger gains.

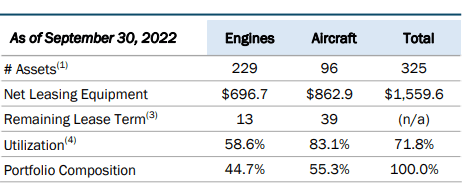

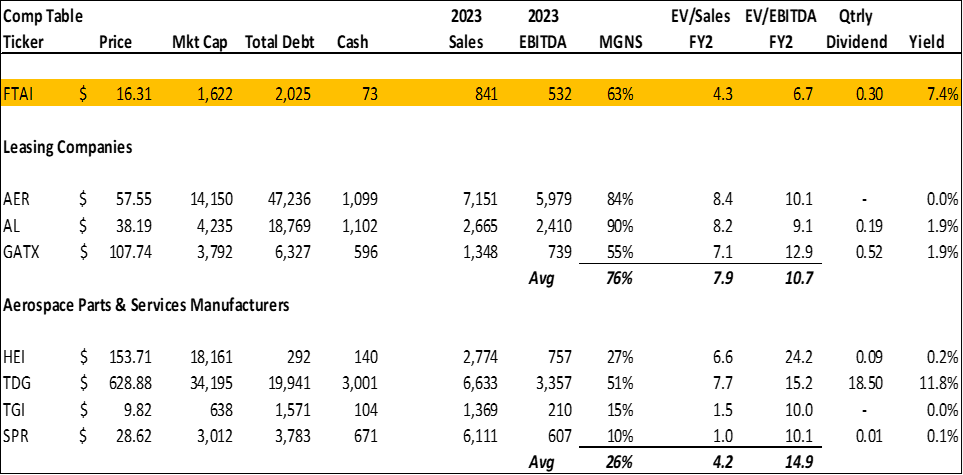

Stock in the Spotlight – FTAI Aviation Ltd. (FTAI)

FTAI Aviation Ltd., formerly Fortress Aviation and Infrastructure, commenced operations in 2014 as an aircraft and engine lessor for older vintage equipment. It is focused on the CFM56 engine, the work horse of the commercial aerospace market with over 50% of the market. FTAI makes money by owning the aircraft and engines and leasing them to commercial airlines globally. FTAI also offers FAA certified repair and servicing of engines after the OEM warranty period expires at a much lower price. This is a valuable alternative for airlines facing double digit price increases on servicing and parts from the OEMs (GE/Safran are 50/50 partners on the CFM56).

FTAI 3Q 2022 Earnings Supplement

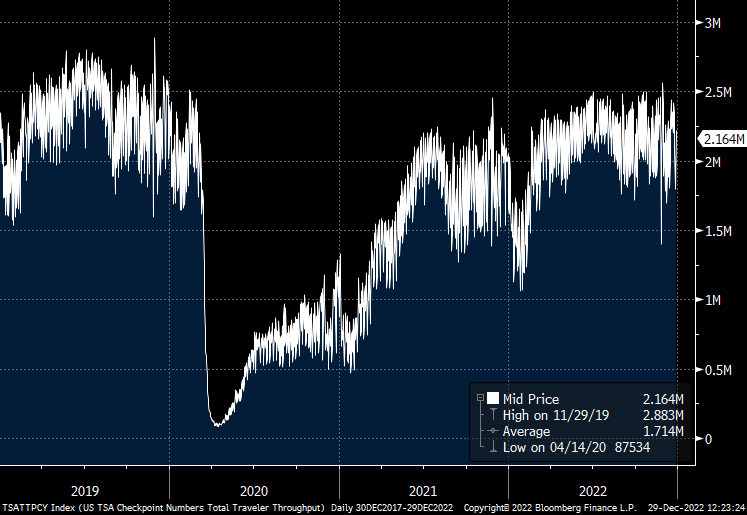

Air travel has largely recovered to pre-pandemic levels while more aircraft are demanding increasing levels of shop visits as new aircraft orders plummeted during Covid. FTAI’s aerospace parts and service business is expected to generate over $100 million in EBITDA in 2023, a high margin complement to the $400 million in leasing EBITDA. FTAI also benefits from consistent gains on portfolio assets sales, which are lumpy and can be substantial. FTAI pays a $1.20/share dividend (7%+ yield) and recently changed its corporate structure from an LLC to a Cayman based corporation.

TSA Checkpoint Passenger Volume

Bloomberg

Given its history as an LLC until recently and being externally managed by Fortress Investment Group (a subsidiary of Softbank), FTAI has been somewhat ignored by Wall Street. Its valuation is noticeably lower than its peers. We expect the change from LLC to Incorporation (some investors can’t own companies that generate K-1s) and growth in sales and EBITDA to support a re-rating upward in the shares over time.

Bloomberg

Tax Update

We managed to end the year in a small taxable capital loss position (although we did receive dividend income and partnership distributions throughout the year). I am aware that I have not distributed capital back to most of you since your initial investment (myself included). Thank you for your confidence! If you desire a distribution for taxes or any other reason, please let me know. Contributions are always encouraged! In the immortal words of Dean Martin, “It’s your world, I just live in it”! K-1’s will be out in early April based on experience in prior years.

Final Ruminations

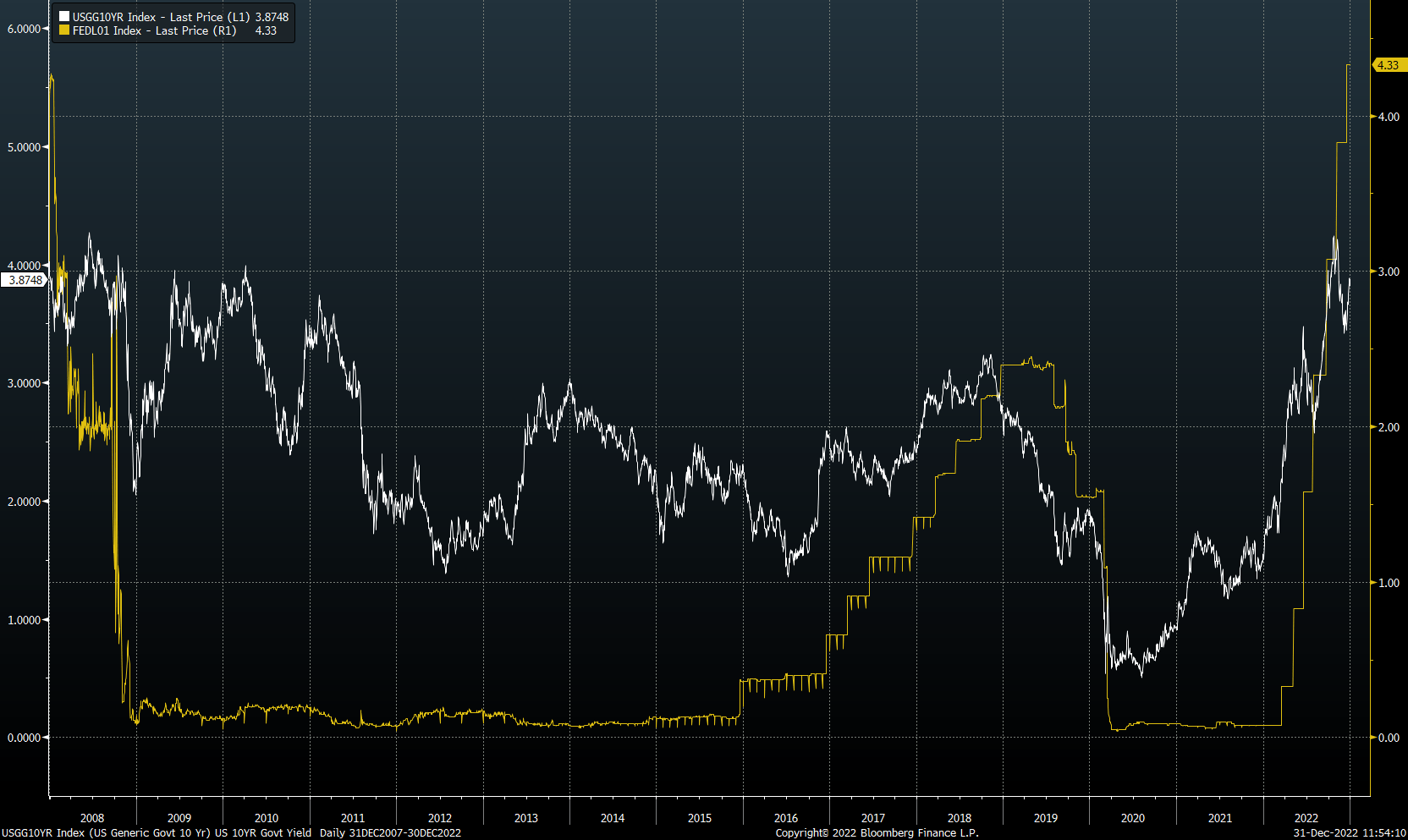

About 12 years ago, when I was managing large institutional accounts, I joined the litany of voices that believed there would be a snap back in interest rates after the Fed cut rates to zero following the housing crisis in 2008. There was a period from 2016-2019 when the Fed attempted to begin normalizing the Fed Funds rate. Then Covid hit – driving rates to rock bottom levels for an additional two years. Overall, the market benefited from 15 years of low long-term interest rates and an explosion of technological innovation – much of it lacking an investor’s requirement for profits or positive cash flow.

Fed Funds v. 10 Yr. Treasury (2007-2022)

Bloomberg

The trouncing that value-focused investing strategies took on a relative basis was staggering and lead to an asset reshuffling toward growth-based strategies. A difficult but valuable learned lesson through this period was humility. The future is unpredictable, although CNBC will interview legions of market commentators who will try. After 35 years of professional investing, I believe there are a couple of investment maxims to go by. First, know who you are. We are not all technologists, financial engineers, salespeople with the gift of gab, or serial entrepreneurs. For me, discounting free cash flows and attempting to buy securities with a margin of safety between share price and intrinsic value resonates. Levered Insight is the imprimatur of my investing soul. There are other ways to make and lose money and I can’t know them all. Being envious of how others make money is a really bad investment strategy! Being disciplined and staying in one’s wheelhouse seems much more lucrative. Thomas Watson Sr., founder of IBM, once quipped “I’m no genius. I’m smart in spots – but I stay around those spots”. And second, “get rich slowly” seems like a solid catchphrase. You will enjoy the journey far more, take fewer stupid and envy-based risks, and not feel compelled to use leverage, except when the odds are significantly in your favor – like buying a reasonably priced home with a 30-year mortgage. 2022 put a big shiny nail in the coffin of rampant speculation. As I referenced on my website at the start of the Fund in 2017, “Interest rates are the ultimate fulcrum”.

Warmest Regards,

Eduardo A. Brea, CFA

Managing Partner

1/16/2023

Be the first to comment