AsiaVision

We recommend initiating a long position in Lesaka Technologies (NASDAQ:LSAK) at the current stock price of $4.28. We have a 12/31/23 price target of $8.00, reflecting 87% upside to the current share price of $4.28 and an increase from our prior $7.00 price target issued in December 2020. We are raising our price target given several positive developments described below.

Executive Summary

-

Background: In December 2020, we recommended an investment in Lesaka Technologies (LSAK) at a share price of $3.36. At the time, Lesaka was named Net 1 UEPS Technologies and traded under the ticker UEPS. Subsequent to our recommendation, the share price reached a high of $6.45 in November 2021 and has since declined to roughly $4.28. Despite a total transformation in the company’s story and fundamentals, the stock price remains at similar levels.

-

Investment Thesis: Lesaka Technologies (“Lesaka”, “LSAK”, or “the Company”) offers investors a compelling mix of high growth and deep value. The story begins in mid-2020 when Value Capital Partners acquired a significant minority stake in Lesaka, and together with board member Ali Mazanderani, set about completely resetting the vision and strategy around building the leading financial technology (“fintech”) provider in Southern Africa. Heretofore there was no fintech ecosystem in South Africa akin to the likes of PagSeguro (PAGS) or Fawry (FWRY), despite South Africa displaying many of the same characteristics as markets such as Brazil and Egypt. South Africa is a highly cash-based economy, and many consumers and merchants in the informal sector suffer from a lack of access to any traditional financial services, let alone the digital economy.

A high-quality new management team and Board of Directors was appointed to oversee the company’s turnaround, which culminated in the transformative acquisition of the Connect Group, a profitable, high-growth and leading provider of financial technology solutions to 44,000 micro, small and medium enterprises (“MSMEs”) in Southern Africa. For the management team, the mandate was immediate and clear: fix the consumer business and integrate the merchant business into the dual-sided ecosystem. The opportunities and synergies this presents are tremendously exciting, in our opinion.

The acquisition of the Connect Group significantly advanced Lesaka’s vision, adding substantial scale to Lesaka’s Merchant business segment, bringing established and highly respected brands such as Kazang, Cash Connect, Capital Connect and Kazang Connect, and more than doubling total revenues. These complementary product offerings create a business with significant scale across all tiers, offering further growth opportunities to service small and medium enterprises in South Africa.

Today, Lesaka is positioned as the leading provider of end-to-end fintech solutions to underserved consumers and merchants in Southern Africa with a large total addressable market opportunity that is underpenetrated. Lesaka delivers financial services to consumers (B2C) and merchants (B2B) in Southern Africa through its proprietary banking and payment technologies, which include banking, lending and insurance solutions to consumers, and cash management solutions, bill payment technology, value-added services, business funding and card acquiring solutions to formal and informal retail merchants.

We believe the inevitable digitization of the Southern African economy provides the company with a secular tailwind for revenue growth of roughly 20% annually, which combined with very favorable unit economics and management’s cost reduction initiatives should enable Lesaka to further expand margins and increase EBITDA. However, the market has yet to recognize Lesaka’s transformation, and shares of LSAK currently trade at a fraction of the EV/EBITDA multiples afforded to peers. These dynamics should appeal to growth, value and special situation investors alike, in our opinion, resulting in stock price appreciation driven by both earnings growth and multiple expansion over time. Meanwhile, a stock buyback program is already in place, and achieving any of the catalysts listed below could also help close the gap between LSAK’s public valuation and those of its peers.

Catalysts

-

Consumer Business Turnaround: The consumer business reported an EBITDA loss of $22 million in the fiscal year ended 6/30/22. Management has stated that the consumer business will be EBITDA breakeven in the quarter ended 12/31/22. Over time, we expect EBITDA margins in the consumer business to reach roughly 25%, which in turn should drive positive net income for the company as a whole.

-

Winning Business with SASSA: Lesaka has a strong relationship with the South African Security Agency (SASSA), which has indicated its need for better support and service in executing on the distribution of social grants in South Africa. Approximately 19 million social grants are paid to 12 million grant recipients every month, of which approximately 7 million grants are paid by Post Bank (post office) of South Africa. In each of the past three months, Post Bank has failed to do this effectively and acknowledged its inability to do so, citing operational challenges. Lesaka has an immediate opportunity to assist in grant distribution in South Africa, which could result in growth of its EPE customer base and cross-selling opportunities, thereby increasing revenue.

-

Sale of Non-Core Assets: Lesaka still holds stakes in several non-core assets made by prior management. Current management has indicated these assets will be sold as soon as practicable with the cash used to pay down debt and grow the operating business. We value these at roughly $40 million while the company values these at roughly $83 million.

-

Expanding Investor Relations Efforts: Lesaka has renewed its focus on investor engagement, which we expect to drive greater market awareness of the company’s attractive growth and margin expansion prospects. Within the past year, Phillipe Welthagen joined as Head of Investor Relations, and the company recently retained FNK IR to further support its investor relations initiatives. Worth noting, Lesaka is only covered by B. Riley Securities, and we believe the company’s efforts to re-engage with the sell-side could translate into additional research coverage. The company also just issued annual guidance for the first time in years.

-

Note: all currency figures will be USD, in which LSAK both trades and reports, unless otherwise noted. LSAK’s operational currency is South African rand (ZAR), and the company therefore analyzes its performance in ZAR. The company’s results reported in USD can be significantly affected by the currency fluctuations between USD and ZAR.

Company History

Lesaka has been publicly traded on the Nasdaq and based in Johannesburg for over 10 years. At one point, when it held a large payments contract with SASSA, the company had a market capitalization of over $2 billion. In 2018, Lesaka lost SASSA as a customer, which in turn reduced its consumer account base by 90% in one fell swoop. As a result, the company laid off half of its workforce. In the aftermath of the SASSA loss, Lesaka was essentially a holding company with a subscale B2C payments business, a portfolio of non-core international payments and fintech assets, and roughly $200 million in cash.

Re-Involvement of Value Capital Partners (“VCP”): In 2020, VCP, one of the best-known private equity funds in South Africa, acquired an approximately 18% position in Lesaka. VCP’s founder, Antony Ball, knows the business very well, as he led an investment in LSAK in 2004 and served on the company’s Board when it went public on the Nasdaq. Prior to VCP, he founded and built Brait, a private equity firm in South Africa with an enviable track record. His background and involvement leaves us confident that VCP is focused on value creation over the long-term. VCP has been the driving force behind the company’s turnaround since acquiring its position and continues to buy stock on the open market, most recently on 12/30/22 with the purchase of another 199,871 shares at an average price of $4.49. The firm now owns roughly 25% of LSAK. We view their involvement as a major positive.

Recent Developments

Connect Group Acquisition: In November 2021, Lesaka announced the acquisition of Connect Group, a profitable, high-growth provider of B2B fintech solutions in Southern Africa for an enterprise value of $264 million, or roughly 10x EBITDA. The purchase price was financed with cash and debt of $160 million (five-year term loan) and $24 million in an equity earn-out, which was structured as follows: 3 million LSAK common shares valued at $7.50 per share payable in three equal tranches on the first, second and third anniversaries of the deal closing. Worth noting, the stock price on the day of the announcement was $5.71, so $7.50 per share was a 31% premium to the stock price, and is still a 75% premium to today’s stock price.

The deal was transformative as Connect Group’s sales exceeded those of Lesaka’s legacy revenues. Connect Group had also grown EBITDA at a three-year compound annual growth rate in excess of 30% through the year ended February 28, 2021, which includes the impact of the COVID-19 pandemic. ConnectGroup is also generating free cash flow. Post-transaction, Lesaka now has significant scale as evidenced by the $125 million in revenues and $3.6 million in EBITDA generated in the quarter ended 9/30/22.

Strategically, the acquisition diversifies Lesaka’s business, expands its addressable market opportunity, and creates potential revenue synergies. Whereas Lesaka’s legacy business focuses on underbanked consumers and enterprise-level businesses in the “formal” market (e.g. a chain of stores), Connect Group focuses on micro, small and medium enterprises (MSMEs) in the “informal” market (e.g. a single shop on the corner). Connect Group has roughly 44,000 merchant clients, comprised of 8,600 “formal” merchants and 35,000 “informal” MSMEs, and their addition enhances the stickiness of Lesaka’s customer base as merchants have higher switching costs and lower churn rates than consumers. Although Connect Group conducts business primarily in South Africa, the company also has a presence in Botswana, Namibia and Zambia, setting up Lesaka for further expansion across Southern Africa. In terms of revenue synergies, the combined company now boasts a dual-sided ecosystem (merchant and consumer), creating more opportunities for cross-selling. Adoption of multiple product offerings by customers should lead to lower churn, higher transaction volumes and take rates, and greater customer lifetime values. Additionally, Connect Group’s loan business, one of the faster growing products, will no longer be capital constrained and could accelerate growth. Finally, this acquisition gets the company to a size and scale where their cost of capital is lower than most competitors.

New Management: As mentioned earlier, the whole executive team has been revamped. We believe each of the executives listed below is an upgrade and boasts significant large-company experience, which we think speaks to Lesaka’s greater ambitions.

-

Chris Meyer: Group CEO. Appointed in June 2021, Chris has over 20 years of relevant experience, most recently serving as the Head of the Corporate & Investment Bank at Investec, a GBP 100Bn+ asset management and investment banking firm. He has bought stock on the open market.

-

Steven Heilbron: CEO of Connect Group. Steve is a very capable and entrepreneurial executive who was the primary driver behind Connect Group’s success and now leads Lesaka’s merchant division. He has also joined the Board of Directors and previously worked at Investec with LSAK Group CEO Chris Meyer. His contract was recently extended through 2025.

-

Lincoln Mali: CEO of South Africa. Lincoln has over 25 years of experience in various financial services roles, including his most recent position as Head of Group Card and Payments at Standard Bank in South Africa. Lincoln is in the midst of turning around the consumer division and is also focused on improving relationships with SASSA.

-

Naeem Kola: Group CFO. Naeem joined the company in February 2022, and has over 25 years of experience in various accounting and CFO roles, but most pertinently, he spent six years as Group CFO of Emerging Markets Payments Group (EMP), an EMEA-focused fintech business that made several acquisitions and was backed by Actis, a well-known European private equity firm. Of note, Lesaka board member Ali Mazanderani was the partner at Actis that led the EMP investment.

-

Basie Kok: CTO. Basie previously served as CTO at SaltPay, a fintech company founded by LSAK board member Ali Mazanderani.

Importantly, management’s interests and compensation are well aligned with shareholders. For instance, CEO Chris Meyer has a three-year incentive compensation plan in place in which half of his compensation only vests if LSAK’s share price is $8.14 or higher on June 30, 2024. Many of the top executives and Board members have also bought stock on the open market over the last year and a half at prices higher than the current stock price. Finally, the company is in the process of introducing an employee stock ownership plan representing 5% of the company’s stock in order to attract and retain talent.

Refreshed Board: Value Capital Partners has changed the board dramatically since its re-involvement. Although the entire Board is impressive, two specific board members merit mention: Antony Ball, Chairman of Value Capital Partners, and Ali Mazanderani, a highly regarded fintech expert who made a number of successful emerging markets payments investments at Actis, including StoneCo (NYSE: STNE) in Brazil, Network International in Dubai (trades in London) and Fawry in Egypt (trades in Cairo).

Operational Turnaround: New management wasted no time in making changes after parachuting into the company, demonstrating their ability to execute well and providing us with comfort that they can seize the opportunity. Key changes include the following:

-

Simplified financial reporting: LSAK now reports revenue and adjusted EBITDA for two clearly defined segments: merchant and consumer. Management has also begun to disclose more KPIs and metrics applicable to each segment, providing investors with a greater understanding of the company’s underlying performance.

-

Resumed guidance: In September 2022, management issued guidance for the fiscal year ended 6/30/23, calling for revenue between $565 million and $600 million, and adjusted EBITDA between $31 million and $34 million; these numbers have come down slightly due to the change in the ZAR/USD exchange rate. This was the first time guidance has been issued to Wall Street since August 2020.

-

Cost reduction initiatives: Late last year, management launched “Project Spring,” a cost reduction plan expected to cut $19.5 million in costs on an annualized basis. Approximately 75% of the savings pertain to SG&A expenses, including a 20% reduction in operating expenses in the consumer division, with the balance in COGS. As part of the plan, headcount was reduced dramatically, all contracts were renegotiated, and Connect’s office in Johannesburg was consolidated into Lesaka’s main office. Management also exited businesses and regions that were not profitable, and merged Easypay and Kazang under a single management team in the merchant division.

-

Investments in sales and marketing: Management has moved the company to a sales and data-focused culture. In the consumer division, EPE previously lacked a sales force and now has 900 sales reps, many of whom are in the field signing up new customers. Importantly, every sales rep within the consumer division is now trained to sell all products, which should lead to greater cross-selling opportunities. Sales leadership has also been upgraded in eight of the nine provinces in South Africa. Incentive compensation programs have been tweaked, and advertising recommenced after years of underinvestment. Efforts are also underway to retarget former EPE customers, many of whom are among the 11 million current recipients of SASSA distributions. Investments have also been made in software to measure performance more rigorously.

-

Adopting an asset-lite model: Within its consumer division, Lesaka has closed 800 ATMs and sold 400 mobile ATMs, leaving approximately 900 remaining at present. Half of its ATMs have been moved into formal retailers, producing greater foot traffic and eliminating the need for security, in addition to being open longer. Despite the reduction in overall ATMs, transactions per ATM have increased 60% Y/Y. Additionally, Lesaka has also shut down over 100 unprofitable retail branches and sold 200 vehicles.

New Product Introductions: LSAK has recently introduced several new products. The pace of innovation is accelerating, albeit from a low base.

-

EPE Lite card: Targeted at 18 to 50-year-olds, EPE Lite features a low membership fee of R5 per month.

-

SmartOne: An insurance product in the consumer division, offering a payout of up to R30 000.

-

EPE Moneyline short-term loan: A one-month loan product, offering up to R500.

-

EZE Money Market product: In partnership with retail chains in the formal market, EPE kiosks are opened in their stores to sell VAS and other financial products to consumers.

Total Addressable Market

Merchant division: South Africa has an estimated 1.4 million informal micro, small and medium enterprises (MSMEs) and 700,000 formal merchants. The formal SME sector includes traditional merchants with revenues in excess of R150 000 per month, who can accept various forms of payment and have access to the formal banking market. In terms of market penetration, we estimate Lesaka currently has less than 1% market share of the formal market and less than 4% in the informal space, as the company has roughly 6,500 traditional formal merchant clients and 45,500 MSME clients, respectively. According to the company, South Africa’s informal economy is estimated at over R300 billion, or $17.3 billion, and independent estimates indicate the informal market contributes around one-third of the country’s GDP. Worth noting, 60% of total transactions in South Africa are cash-based, but in the informal sector, we estimate approximately 90% of transactions are cash-based. As merchants and consumers continue to shift from cash to digital payments, we believe this will provide a secular tailwind to growth.

Consumer division: South Africa’s population is segmented into ten different levels of Living Standard Measures (LSM), with ten being the highest living standard level (wealthiest) and one being the lowest (poorest). Lesaka’s consumer business targets individuals in levels one to six, almost all of whom are underbanked. Competition for customers in these segments is lower while demand is fairly inelastic.

Lesaka’s EPE product currently targets the 11.6 million permanent social grant recipients who receive cash distributions from SASSA via the Post Office. However 19 million of the 60 million people in South Africa receive some form of SASSA payout, and we expect LSAK to expand their target market accordingly. Today, Lesaka has just over 1.1 million EPE customers, or roughly 10% of its current target market, and generates a monthly average revenue per user (ARPU) of just above R70. Assuming a consumer utilized all of the company’s products, monthly ARPU could potentially reach R135, implying a serviceable addressable market opportunity for the consumer business in excess of $750 million based on Lesaka’s current target market.

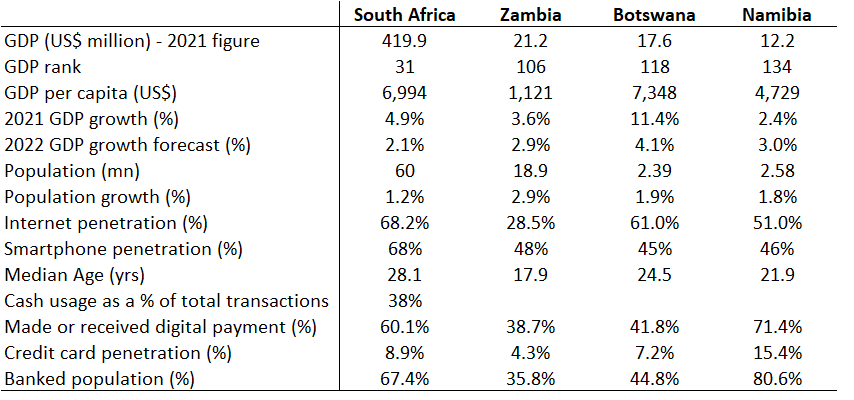

As previously mentioned, the vast majority of Lesaka’s revenues are in South Africa, but Kazang also conducts business in three other adjacent countries: Botswana, Namibia, and Zambia. Below is a chart of some relevant statistics for South Africa and the other countries in which LSAK conducts business. We also believe it is important to note that South Africa has an increasingly robust startup ecosystem, and several South African universities have highly regarded computer and data science programs. These dynamics produce a strong pool of engineering talent at relatively inexpensive rates. Given its prominence and strong balance sheet, we think Lesaka is likely considered an employer of choice and will be able to attract the best talent in the region.

Important Metrics of Southern African Countries

Source: public domain

Source: Created by author with the help of data from Wikipedia/public domain.

Products & Services

Lesaka offers a broad array of cash, credit card, capital/loans, payment and value-added services (VAS) to merchants, and also targets consumers with a comprehensive set of financial products. We review these offerings below:

Merchant division: This B2B division comprises the legacy Easypay business plus the acquired ConnectGroup. Sales by product line have not been disclosed:

-

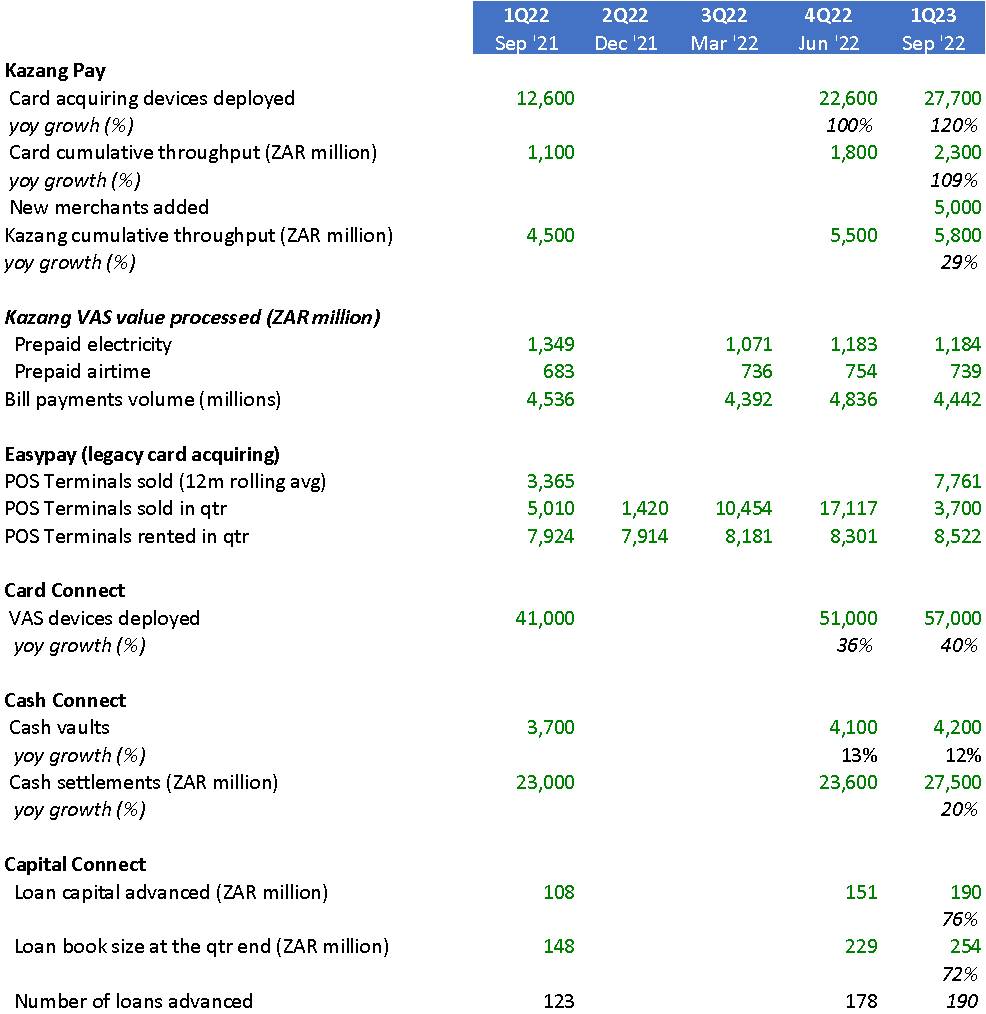

Kazang VAS: We think this is the crown jewel inside ConnectGroup. Kazang is a prepaid, micro-payment VAS platform sold through a mobile POS device/terminal (MPOS) to MSME’s in the informal market. Kazang enables merchants to sell the following to consumers: mobile phone airtime, electricity, digital TV, bill pay, sports betting, lotto tickets, local and international cash transfers, gaming, money transfer services, and ATM-like services. We note that in many developing countries, including South Africa, most consumer services are prepaid in small increments. Typically, qualified merchants are provided with a Kazang MPOS device free of charge, but those that fall short of a minimum monthly revenue number must pay a rental fee. Lesaka negotiates either a take rate (1% to 3%) or small fixed fee for each bill paid with the service provider, and receives about R4.50 per bill on average. Merchants also receive a portion of every VAS sale. As Lesaka purchases each MPOS device for roughly R1 500 and receives R125 per terminal in monthly average revenue, breakeven is typically reached after 12 months but may be achieved in as little as four months. In the quarter ended 9/30/22, approximately 57,000 devices were deployed, representing an increase of 40% Y/Y. We estimate that EBITDA margins at scale in this business will be roughly 20%-25%.

-

CashConnect: A digitized cash management platform for merchants. Lesaka provides in-store “smart safes” to formal SME merchants and also offers financial products and services to the merchant. The company charges a monthly fee for the vault as well as a percentage take rate for money that flows through the vault. Lesaka also leverages its deployment of “smart safes” as a means to persuade merchants to sell more profitable products and services. Servicing of the vaults is outsourced and switching costs are generally high. In the quarter ended 9/30/22, approximately 4,200 vaults were deployed, an increase of 12% Y/Y. We estimate that EBITDA margins at scale in this business will be roughly 25%-30%.

-

Capital Connect: Provides unsecured short-term working capital loans to merchants who are CashConnect customers under the brand name “Click & Borrow.” Based on the merchant’s sales and amount of cash flowing through the merchant’s vault, loans are approved within 60 minutes and cash provided within 24 hours. Loan sizes range from R200 000 to R2.5 million but tend to average R800 000 with terms ranging from 90 to 360 days. Lesaka charges an 18% flat rate fee, or an effective interest rate of 37%. Bad debt is less than 1%. In the quarter ended 9/30/22, R190 million of loans were advanced (roughly $11 million), reflecting an increase of 77% Y/Y. We estimate that EBITDA margins at scale in this business will be roughly 15%-20%, assuming conservative provisioning for write-offs.

-

CardConnect, including KazangPay: Merchant acquiring solutions targeted at MSMEs in the informal market. Lesaka sells or rents desktop and handheld/mobile point of sale (POS) devices to merchants, enabling them to accept credit cards. Traditional POS terminals are too expensive for these merchants but our checks have found that KazangPay’s device is sold at the lowest price point in the market. Merchants using KazangPay receive cash immediately after a customer uses a card i.e. instant settlement, whereas those using competitive products typically wait 24 to 48 hours for funds to be made available. Chargebacks are covered by the card issuer, not Lesaka. In addition, merchants may be offered working capital loans based on their card volumes. Thus far, only a small percentage of Kazang merchants have been penetrated, so we see a lot of upside potential and believe investors will assign a high multiple to this business. In the quarter ended 9/30/22, approximately 27,700 devices were deployed, an increase of more than 100% Y/Y. We estimate that EBITDA margins at scale in this business will be roughly 35%-40% but may be lower over time as competition increases.

-

EasyPay: Lesaka’s legacy B2B payment switch and bill and supplier payments business, enabling formal merchants to facilitate bill payments and sell VAS to consumers. EasyPay is one of the largest bank-independent card transaction processing services (i.e. switch) in South Africa and is also one of the largest bill payment companies. We believe this scale as both a large payment processor and aggregator is a competitive advantage. Throughput through the switch per month is approximately R15 billion via 50 million transactions.

Merchant Division KPIs by Quarter

Source: company SEC filings

Source: Created by author with the help of data from Lesaka SEC filings.

Consumer division: This B2C division comprises the EasyPay Everywhere (EPE) business, which offers four products:

-

EasyPayEverywhere (EPE): EPE is a low-cost transactional banking solution that is structured for underserved consumers in a lower income market. The EPE banking solution is available through the use of a bank card, USSD, internet banking and mobile app. EPE functionality includes cash withdrawals and deposits, balance enquiries and debit orders with simple and transparent pay-as-you-transact pricing. The account also includes 3% interest on credit balances per annum.

-

With EPE, banking clients are able to receive cash distributions from the South African government’s social grant program and build up a financial profile that opens a range of financial opportunities, including access to fixed or variable loans, device lending and access to standalone insurance products.

-

EPE is available and serviced through a widespread network of EPE branches, in-store retailer branches and ATMs to broaden financial access for customers.

-

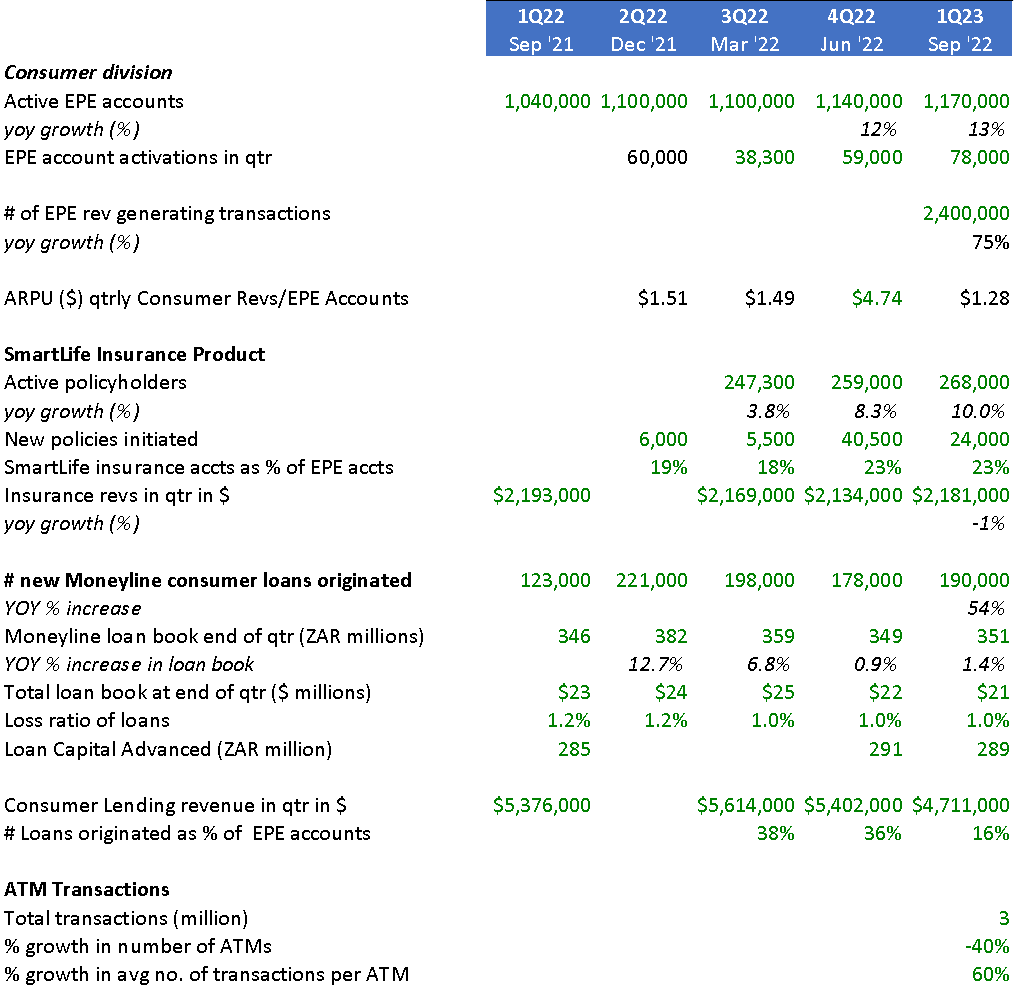

As EPE has been in the market for over 20 years, the product has strong brand recognition and operating expertise. Each month, SASSA pays approximately 19 million grants. EPE is the cheapest product in the market with a transparent fee structure. EPE charges monthly transactional and account fees of approximately R7.50. As of the quarter ended 9/30/22, Lesaka had 1.17 million EPE customers, representing an increase of 13% Y/Y.

-

-

EasyPay Insurance (previously named SmartLife): This business holds a Long-term Insurance License and offers consumers access to Smart 1 and the Pensioners Plan insurance plans. These are distributed through Lesaka’s widespread sales and distribution network in Sub-Saharan Africa. Smart 1 offers coverage that is flexible, affordable and easy, with benefits that can be extended to include:

-

Family income protection

-

Funeral assistance

-

Accidental death

-

This funeral insurance product is sold to EPE account holders. Funeral insurance is very popular in South Africa and pays out upon the death of the policyholder. For a monthly premium starting at R26 per month (roughly $2.50), policyholders receive coverage ranging from R5 000 to R30 000 (roughly $1,000). The penetration rate of active EPE accounts is currently averaging around 18%. As of the quarter ended 9/30/22, Lesaka had 267,000 active policies, up 10% Y/Y.

-

EasyPay Loans (previously named Moneyline): This is a short-term, unsecured loan offered to existing (and qualifying) EPE customers through Lesaka’s established and widespread EPE distribution network. Loans are either fixed or variable in amount and repayment tenure, up to a maximum of R2 000 (approximately $125) over a maximum term of six months. EasyPay loans also offers device lending for mobiles phones, providing customers with access to more affordable smart technology. There is a three-month lag before new EPE customers may take out a loan. The average loan size is roughly ZAR 1 500. In lieu of interest, Lesaka charges an initiation fee equal to 0.4x the loan amount and a monthly service fee. On average, this has yielded revenues of approximately 1.3x to 1.5x the loan amount. The portfolio loss ratio is consistently around 4% per annum.

-

ATM Network: Lesaka operates over 800 ATMs across all nine provinces in South Africa and processed over R11 billion in transaction value during FY 2022. Lesaka has made significant progress in implementing its ATM optimization program, which is also benefiting from its retailer partnership strategy whereby more ATMS have been shifted out of branches and into retailers. To date, 40 through the wall ATMs have been deployed, increasing the number of available hours due to optimal positioning within the stores or malls accepting more customer traffic. As such, volumes have increased, especially in terms of transaction counts. Lesaka earns about R12 ($0.80) per ATM withdrawal transaction. In the quarter ended 9/30/22, the ATM business processed over 3 million transactions through its ATMs. The productivity of the ATM network has increased significantly despite the number of ATMs in the field decreasing by 40% compared to a year ago, and the average number of transactions per ATM is up 60%. Lesaka has also made progress integrating its ATM business into Cash Connect and has begun the rollout of new ATMs and recyclers as part of a holistic cash management solution. This integration will also increase traffic across Lesaka’s ATM network.

Consumer Division KPIs by Quarter

Source: company SEC filings

Source: Created by author with the help of data from Lesaka SEC filings.

Competition

Given that Lesaka has a wide breadth of B2B and B2C products, the company has a long list of competitors. That said, Lesaka is significantly larger than most of its direct competitors in terms of scale, revenues, and reach, and therefore has a lower cost of capital. The company has over 68,000 touchpoints in South Africa, including branches, retailer pay points, ATMs, satellite kiosks and merchant devices, and is the only company able to reach all citizens within a three-mile radius in South Africa. Although banking penetration in South Africa is very high in the middle class and is dominated by five big banks, those banks do not cater to the underbanked consumers and merchants served by Lesaka. South African banks also will not lend to consumers lacking a salary. Finally, we note that Lesaka is unique in that it has products on both the consumer/issuing side and the acquiring side. We believe this could potentially lead to Lesaka having one of the lowest customer acquisition costs on the acquiring side over time.

Merchant competition: Lesaka’s ConnectGroup is the leading player in the informal market. Flash, owned by the retail chain Pepkor, is the largest competitor in this space. Like ConnectGroup, Flash targets the informal sector but does not have its own in-house card-acquiring platform. As such, Flash offers only VAS and supply payments, which is a narrower set of products than Lesaka’s. While Pepkor does not break out numbers for Flash, we know that Pepkor has 200,000 merchants. In the formal market, the company competes with Yoco, a VC-backed MPOS player. In our checks, we have found that merchants have to buy Yoco’s device, whereas Lesaka’s Kazang offers devices for free. Additionally, Yoco does not have a core VAS solution. As of 2020, we know that Yoco had roughly 120,000 merchants and revenue of approximately $35 million. In July 2021, Yoco raised a Series C round of $83 million. For EasyPay, competitors include BankservAfrica, UCS, eCentric and Transaction Junction.

Consumer competition: Competition for the EPE Moneyline loan business is primarily from unregulated lenders who charge high interest and deliver a poor customer experience. Capitec Inc, a large public South African bank, also offers a competitive product to the underbanked. Lesaka’s ATM business competes against South African banks, ATM Solutions and Spark ATM Systems, which collectively have a market share in excess of 90%.

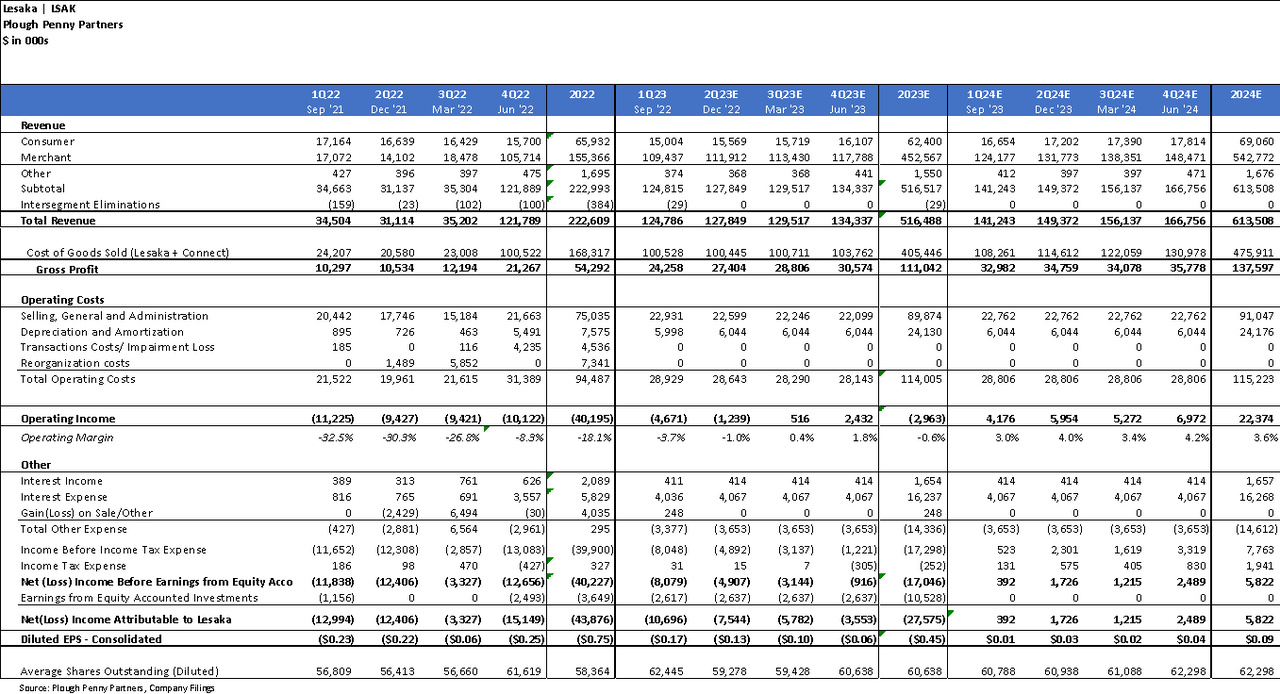

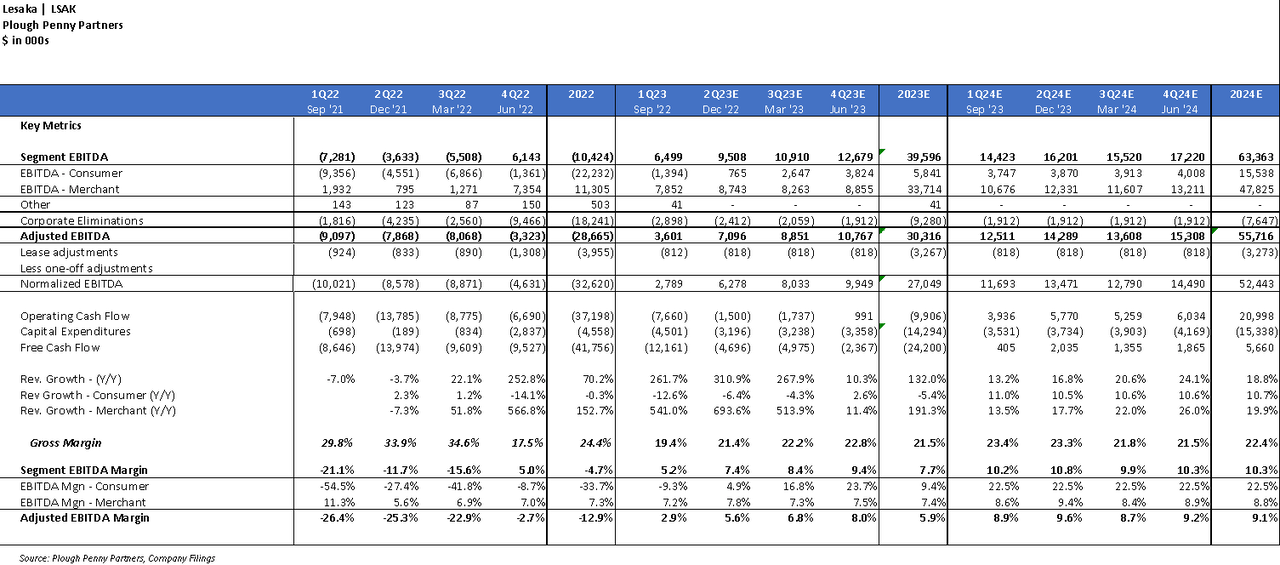

Financial Summary

Although Lesaka’s functional currency is the South African Rand, the company’s financial statements are reported in U.S. dollars and it’s financial statements follow GAAP. Additionally, Lesaka is incorporated in Florida and is therefore not a “Foreign Issuer” that files 6-Ks and 20-Fs with the SEC. The company files 10-Ks and 10-Qs. Unless otherwise noted, all currency figures will be USD.

Recent Results: Lesaka has reported two quarters of results since closing its acquisition of ConnectGroup. In its quarter ended 9/30/22 (fiscal Q1 ‘23), total revenue was approximately $125 million, up from $122 million in the prior consecutive quarter and an increase of 262% Y/Y. Of course, much of the increase from the prior year was attributable to the acquisition. Although details regarding legacy Lesaka’s and ConnectGroup’s organic growth rates for Q1 ‘23 are not available, we believe the combined business is capable of sustaining annual revenue growth of roughly 20% going forward. Adjusted EBITDA increased to $3.6 million, a marked improvement from $(3.3) million in the previous quarter and $(9.1) in the same period last year. By segment, revenue from the merchant division was $109 million and the consumer division contributed $15.0 million, while segment EBITDA was $7.9 million and $(1.4) million, respectively. Corporate eliminations of $(2.9) million comprise the difference between segment and adjusted EBITDA.

Guidance: Given that the South African Rand is Lesaka’s primary operating currency, management’s guidance is provided on a Rand basis. We have assumed a USD/ZAR exchange rate of 17.0 in the conversion of guidance to U.S. dollars. For its fiscal Q2 ‘23, group revenue is expected to be between R2.0-R2.3 billion ($118-$135 million), while segment adjusted EBITDA is expected to range from R157-R164 million ($9.2-$9.6 million) and group adjusted EBITA is expected to be R116-R123 million ($6.8-$7.2 million). For FY ‘23, management’s guidance includes total group revenue of R8.7-R9.3 billion ($512-$547 million), segment adjusted EBITDA of R645-R675 million ($37.9-$39.7 million) and group adjusted EBITDA of R480-R525 million ($28.2-$30.9 million).

Balance sheet: As of 9/30/22, Lesaka had outstanding debt of just under $200 million, largely due to the acquisition of ConnectGroup, and $93 million in cash. Considering management’s guidance for adjusted EBITDA of roughly $30 million, that is a manageable Net Debt/EBITDA ratio of approximately 3x. Management recently refinanced its acquisition debt to extend the maturity by several years. Lesaka has relatively modest working capital requirements as evidenced by its DSO of 21 days and its DPO of 17 days in the quarter ended 9/30/22. That said, Lesaka entered into an agreement on 11/29/22 that increased its revolving credit facility from R150 million to R300 million. The expanded revolver will be used solely to fund the merchant lending business, which requires more capital to accelerate growth but provides good ROI.

Low capital intensity: Capital expenditures are expected to range from $3.0-$3.5 million per quarter going forward, or roughly 3% of revenues. The majority of these expenditures are for the purchase of Kazang’s MPOS devices and CashConnect’s vaults.

Share repurchases: Lesaka has a legacy $100 million stock buyback in place, which has not been used. Although we think the company’s excess capital should be used to grow and take market share, we also acknowledge share repurchases would produce favorable returns for shareholders at current levels.

M&A strategy: Although the company is still digesting the acquisition of ConnectGroup, management has stated that smaller, accretive acquisitions will be a part of the future growth strategy. We think that Lesaka’s Nasdaq listing will prove beneficial once the stock is more reasonably valued, providing the company with additional access to capital and acting as a potential currency. The company recently hired an employee whose sole focus is evaluating acquisitions and M&A opportunities.

Non-Core Assets

Lesaka still maintains a small portfolio of investments made by prior management. The current leadership intends to exit these investments as soon as practicable, yet responsibly, and plans to utilize the proceeds to pay down debt and invest in marketing. Management values these assets at roughly $83 million as of the end of the last quarter, but we more conservatively value them at $40 million.

Our Non-Core Assets Valuation Methodology

Source: internal estimates.

-

Source: Created by author with the help of data from Lesaka SEC filings and investor relations websites of respective companies.

-

MobiKwik: By far the most significant of Lesaka’s non-core assets is the company’s non-controlling stake in MobiKwik, a private fintech company operating in India. Lesaka owned 6,215,620 common shares, or 10% of MobiKwik as of 6/30/22. For the year ended 3/30/22, MobiKwik grew its revenues 80% Y/Y to ₹5.4 billion ($72 million), although its losses have increased. Of note, MobiKwik has been EBITDA positive since the quarter ended 12/31/21. Per Lesaka’s 10-K filing, management values its stake at $76.3 million, based on MobiKwik’s latest fundraising round in June 2021. That said, multiples of publicly traded fintechs around the world have dropped dramatically over the past 18 months. As such, we apply a 50% discount to management’s valuation, implying an EV/Sales multiple of 5.3x on a historical basis and an even lower multiple on projected revenue, assuming MobiKwik sustains its strong growth trajectory. After accounting for a 21% tax rate on any gains, we estimate a sale will net the company $35.8 million.

-

FinBond Group: FinBond is a publicly traded consumer bank operating in South Africa. Lesaka has been selling its position in FinBond over time. During its latest earnings call, management stated that its stake is currently valued at $5 million. We apply a 20% haircut and value the position at $3.9 million, which also reflects estimated net proceeds from a sale of the remaining shares given Lesaka’s higher cost basis. We note that in the event shares rise above the company’s cost basis, we would assume a 22% tax rate on any gains.

-

Cell C: Cell C is the fourth largest mobile network operator in South Africa. Lesaka owns 75,000,000 class “A” shares, or a roughly 5% stake in Cell C. We note that Cell C recently emerged from bankruptcy and has roughly 12 million subscribers. Lesaka has reduced the value of its equity stake to zero, but that occurred when Cell C was bankrupt. We believe Cell C’s equity is valuable as the company owns as much spectrum as the top two mobile network operators in the market. In addition, Lesaka also owns roughly $15 million of Cell C air minutes and has an agreement requiring Cell C to repurchase $588,000 of air minutes per month from Lesaka if the company is unable to sell that much to its users. Management values its stake in Cell C at zero and we do too. That said, Cell C generated R6 516 million in revenue and R366 million in EBITDA in the first half of 2022 and ended the period with R9 460 million in debt. Applying median peer group multiples for EV/Sales and EV/EBITDA of 1.5x and 3.3x, respectively, to these annualized figures implies a potential valuation of $35 million to $85 million for Lesaka’s 5% stake.

Valuation

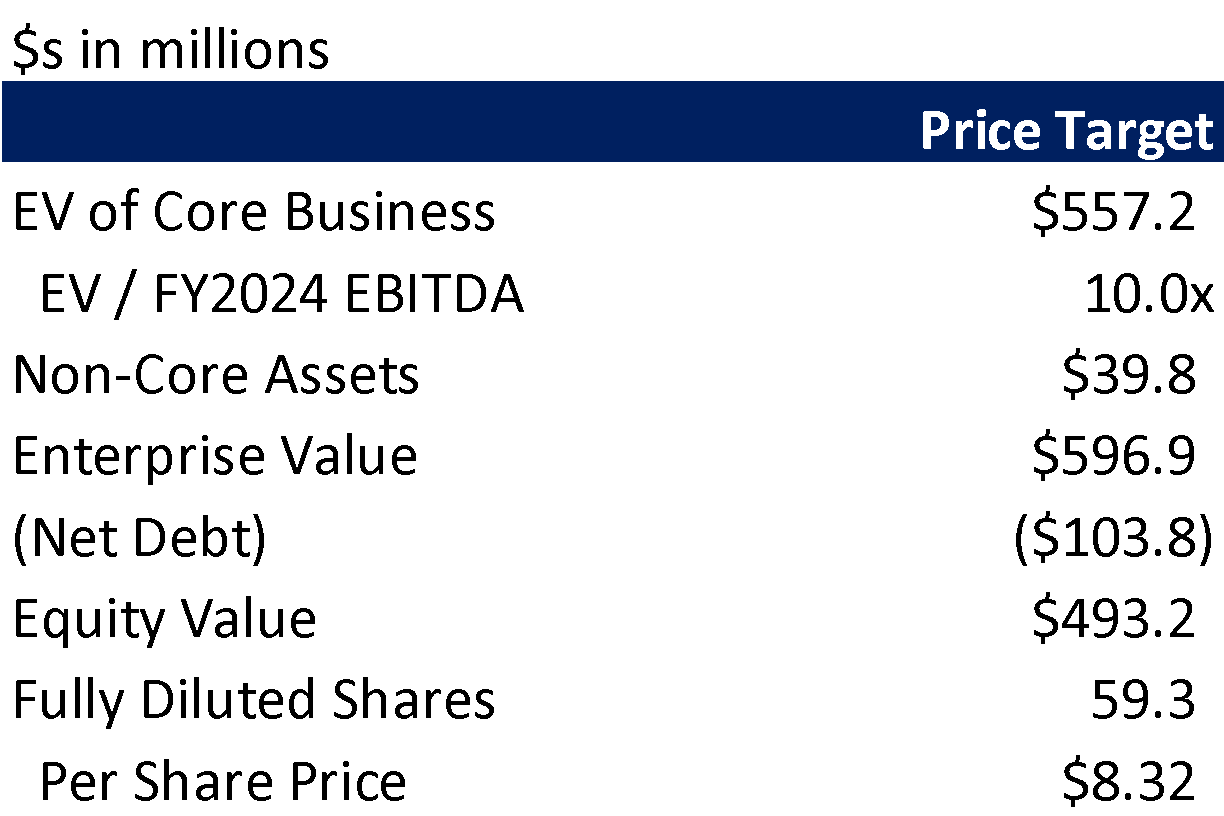

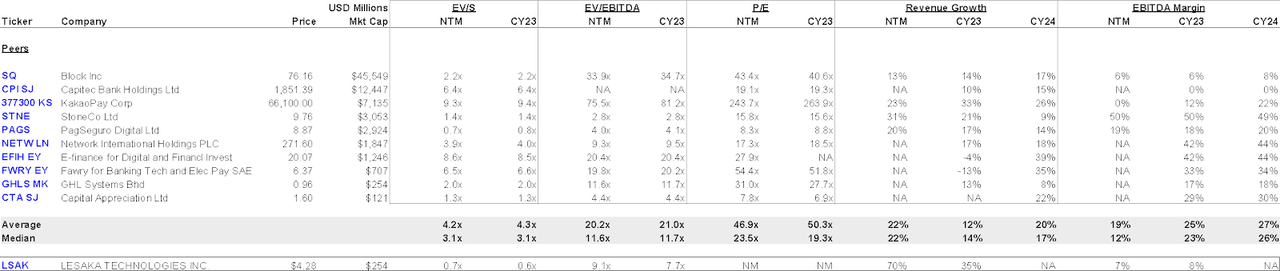

We value the core business based on 10x FY 2024E EBITDA (YE 6/30/24) of $56 million and add the value of non-core assets to derive an Enterprise Value of $597 million. The average peer CY 2023 EV/EBITDA multiple is 21x (see Appendix Public Comparables). We give a 25% discount for LSAK’s small size and another 25% discount due to the fact that LSAK is in South Africa, for a total multiple discount of 50%, which gets us to the 10x multiple we use below.

Adjusting for net debt of $104 million yields an equity value of $493 million, reflecting a per share price of $8.32. We note that a 10x EBITDA multiple is consistent with the median multiple garnered by Lesaka’s peer group, which includes a mix of legacy payment processors and high-growth fintech companies (see Appendix Public Comparables), and is in line with the multiple Lesaka paid for ConnectGroup.

Valuation Methodology

Source: internal estimates

Key Risks

-

Illiquid Stock: LSAK stock is thinly traded, with an average daily volume of 0.2mm shares. In addition, there is significant ownership concentration (Value Capital Partners owns 25% and International Finance Corporation owns 13%).

-

Macroeconomic Risks: South Africa has several structural economic issues that predate COVID. GDP growth has been below 2% since 2013, which is exceptionally low for a developing economy. Unemployment has lingered between 25%-30%. However, the current commodity up-cycle should be positive for their balance of payments.

-

Currency Risk: The vast majority of Lesaka’s revenue is generated in South Africa and is therefore denominated in ZAR (RAND). If the U.S. Federal Reserve continues to hike interest rates, the U.S. dollar may drop, negatively affecting the ZAR/USD exchange rate. Should the ZAR depreciate relative to USD at a rate greater than its historical average, the share price would fall. However, we expect the growth in the company’s revenues and EBITDA to offset this.

-

Loan Defaults: An important and growing part of Lesaka’s business is lending. Typically, we would be concerned if the South African economy were to slip into a recession; however, most of Lesaka’s loans are based on the amount of funds inside a customer’s bank account, which should limit defaults.

-

Execution Risk: Our thesis is contingent on operational improvement within the core business and less so on further liquidation of the non-core investments. As such, strong execution is required.

-

Regulatory Risk: As the consumer division operates in a highly regulated economy, Lesaka faces numerous regulatory risks, including potential new regulation as well as ongoing matters from existing regulation. In 2019, South Africa passed the National Credit Amendment Bill, which provided credit relief to consumers and could have significant adverse effects on Lesaka’s Moneyline business if promulgated by the President. South Africa has made significant investments in “Postbank”, a bank subsidiary of the South African Post Office that uses post office branches as bank branches. In 2017, Postbank took over the SASSA contract from UEPS, which led to the loss of SASSA revenue in 2018. However, we note that recent public news suggests SASSA is beginning to decrease its dependence on Postbank. Finally, the Protection of Personal Information Act (“POPI”) went into effect in South Africa in 2020. POPI provides various consumer data privacy restrictions, similar in spirit to GDPR in Europe.

-

Partner Risk: As Lesaka lacks registration as a retail bank and engages in banking activities in its consumer division, the company has partnered with Grindrod bank, a registered bank in South Africa. Lesaka therefore faces risks from both the partnership itself as well as the risk that Grindrod bank remains a solvent, going concern in good standing with the South African regulatory agencies.

Appendices

Appendix A: Financial Performance and Outlook

Source: internal projections

Source: internal projections

Appendix B: Public Comparables

Source: Bloomberg

Data as of 1/22/23

Be the first to comment