JoeGough/iStock via Getty Images

Given the state of the economy, you might think that buying into food producers may not be exactly the best idea. After all, they tend to be fairly low margin in nature and they are susceptible to significant amounts of competition. One player that has done surprisingly well recently, however, at least from a revenue and share price perspective, is Lancaster Colony Corporation (NASDAQ:LANC). This producer of frozen breads, refrigerated dressings, dips, croutons, and a variety of other offerings, has held up quite well in this environment. But what’s really surprising is that this improvement came even at a time when profitability has declined. Given this weakening in profits and cash flows, and factoring in how pricey shares are, I do think that the company is an illogical play at this time. Although I wouldn’t go so far as to become bearish on the company entirely, I do think that the ‘hold’ rating I assigned to it previously is still justifiable.

Not tasty

Back in November of 2021, I wrote my first article about Lancaster Colony. In that article, I talked about how excellent the company is thanks to the market-leading positions that it holds for many of its brands. I felt as though the long-term outlook for the company was positive, with investors likely to see continued value creation down the road. At the same time, however, I also felt as though shares were too expensive to make sense for value investors, a conclusion that led me to rate the firm a ‘hold’ to reflect my view that it would likely generate returns that more or less matched the broader market moving forward. Since then, the company has significantly outperformed expectations. While the S&P 500 is down by 24%, shares of Lancaster Colony have generated a return for investors of 6.7%.

Author – SEC EDGAR Data

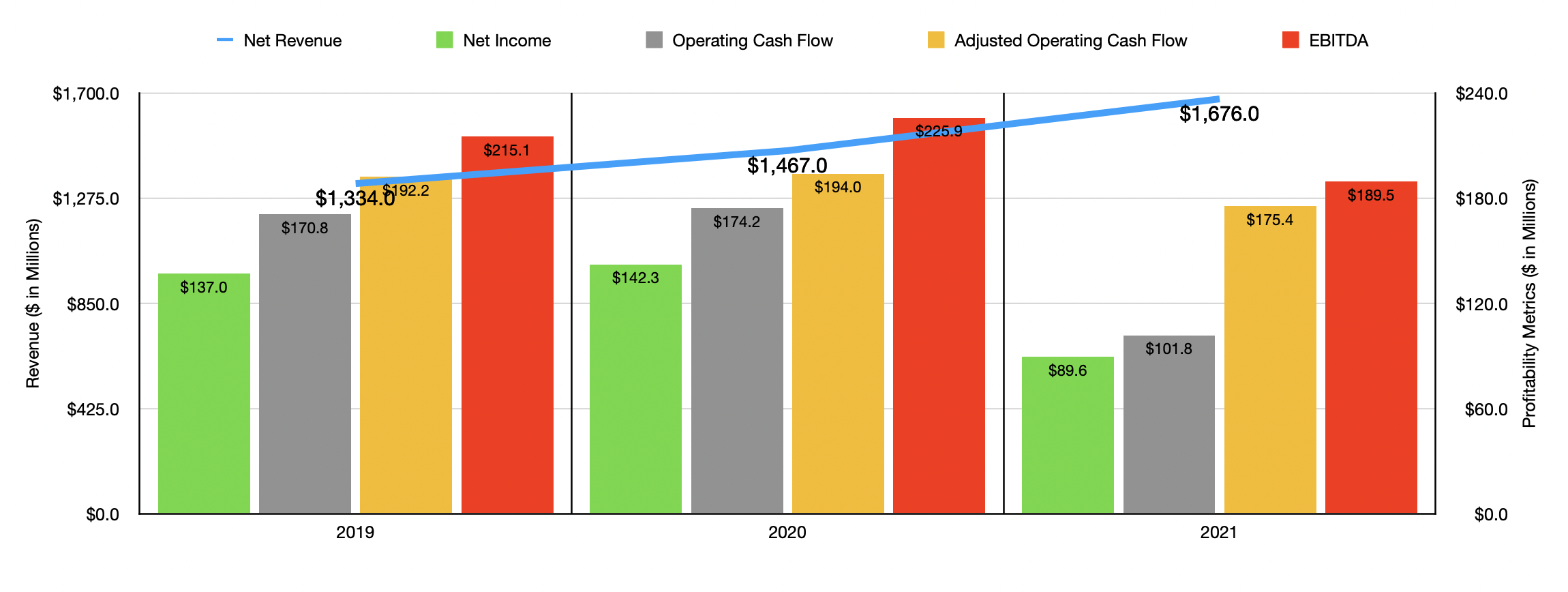

My prior article on the enterprise only covered data through the first quarter of its 2022 fiscal year. Fast forward to today, and we now have data covering the rest of that year as well. During 2022 as a whole, revenue came in strong at $1.68 billion. That’s 14.2% higher than the $1.47 billion generated during the 2021 fiscal year. As can be expected in this current inflationary environment, the vast majority of the increase the company experienced was as a result of price increases. Having said that, the firm still managed to increase the volume of product shipped, on a total pound basis. This number grew by 2% year over year, which was not much different than the 3% increase recorded from 2020 to 2021.

With revenue rising, you might think that profitability has followed suit. Unfortunately, this has not been the case. Net income actually fell year over year, declining from $142.3 million to $89.6 million. A big contributor to this was an 8% decline in gross profit, driven by what management referred to as ‘unprecedented inflationary costs’ associated with commodities, packaging, freight, warehousing, and labor. The company also saw other expenses impact this, such as those associated with the company’s increased reliance on co-manufacturers in order to satisfy demand. Restructuring and impairment costs were also an issue, totaling $35.2 million for the year compared to the $1.2 million reported for the 2021 fiscal year. Other profitability metrics followed suit. Operating cash flow, for instance, dropped from $174.2 million in 2021 to $101.8 million in 2022. If we adjust for changes in working capital, it would have declined still from $194 million to $175.4 million. And over that same window of time, we also saw EBITDA decline, dropping from $225.9 million to $189.5 million.

Author – SEC EDGAR Data

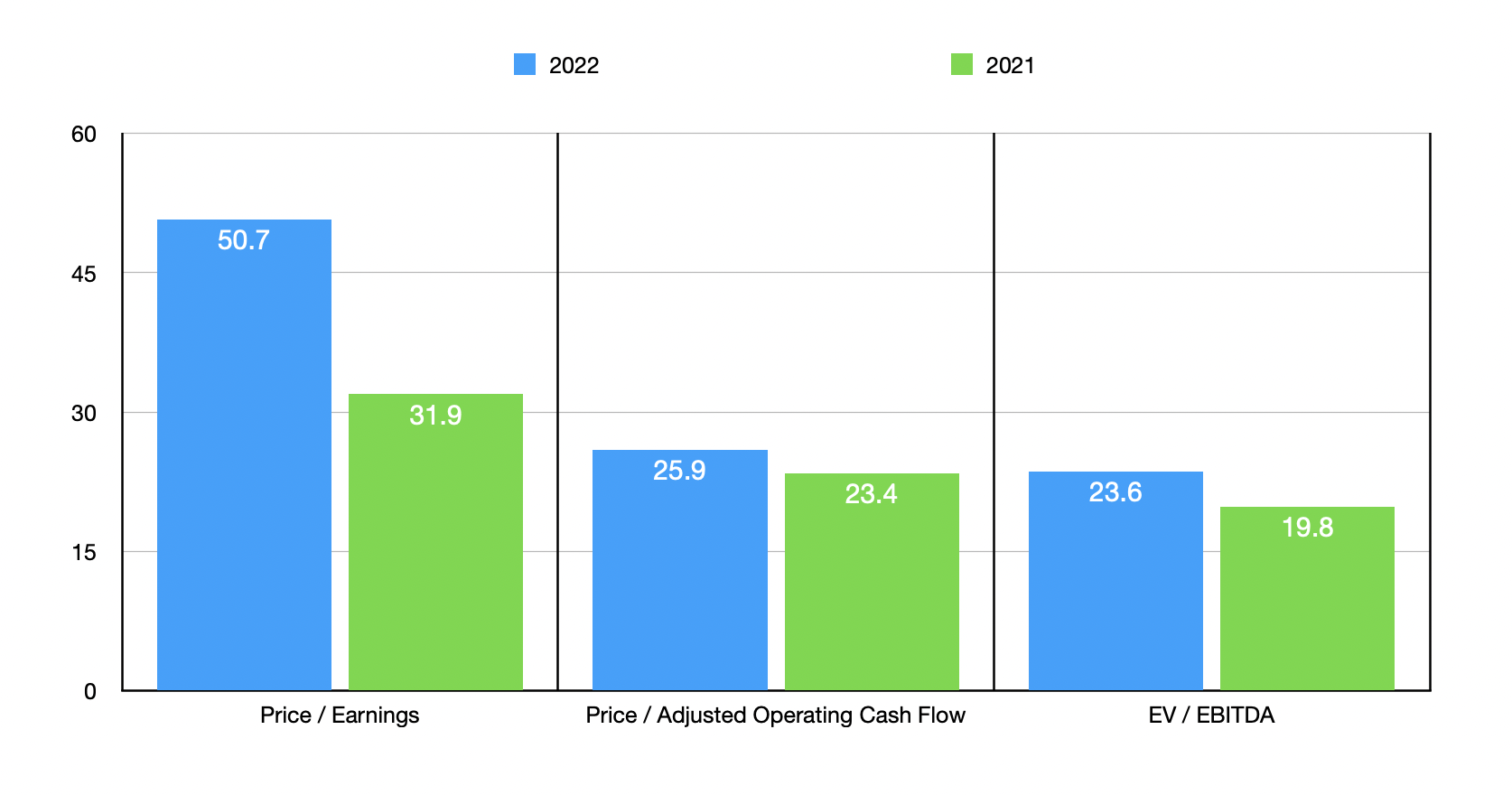

Given all the evidence we have today, we don’t really know what to expect for the 2023 fiscal year. And even if we did have guidance figures, the uncertain economic environment would likely make those irrelevant. Instead of focusing on the future then, I decided to value the company based on data from both its 2021 and 2022 fiscal years. Using the 2022 figures, we can calculate that the company is trading at a price-to-earnings multiple of 50.7. The price to adjusted operating cash flow multiple is lower, but still high, at 25.9. And the EV to EBITDA multiple should come in at 23.6. Using, instead, the data from 2021, we would get multiples of 31.9, 23.4, and 19.8, respectively.

To complete this analysis, one thing I decided to do was to compare the firm to five similar businesses. Given the nature of the company, I do believe that the cash flow figures are more important than the earnings one. On a price to operating cash flow basis, these five companies ranged from a low of 9 to a high of 29.7. In this scenario, four of the five companies were cheaper than our prospect. Using the EV to EBITDA approach, the range was between 6 and 18.8, with our target coming in as the most expensive of the group.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| Lancaster Colony | 25.9 | 23.6 |

| Flowers Foods (FLO) | 18.4 | 14.0 |

| Hostess Brands (TWNK) | 16.6 | 15.8 |

| The Simply Good Foods Co. (SMPL) | 29.7 | 18.8 |

| Cal-Maine Foods (CALM) | 9.0 | 6.0 |

| The Kraft Heinz Company (KHC) | 10.7 | 15.3 |

Takeaway

The data available right now tells me that while Lancaster Colony continues to grow nicely, the firm has not yet adjusted fully to the inflationary environment. Until something changes on this front, there will be some pain for shareholders. But even if the firm were to see the levels of profitability it experienced during the 2021 fiscal year, shares would look rather lofty. Considering this, I do believe that there are better opportunities to be had on the market, both in this space and elsewhere. Yes, Lancaster Colony does have cash of $60.3 million with no debt on hand. But while that provides some degree of protection in this environment, It’s not enough to warrant material upside for investors. In all, I still do believe that the company represents a ‘hold’ prospect at this time. But if shares get any more expensive than they are today, I could see myself ultimately downgrading it to a ‘sell’.

Be the first to comment