DNY59

(This article was co-produced with Hoya Capital Real Estate)

Introduction

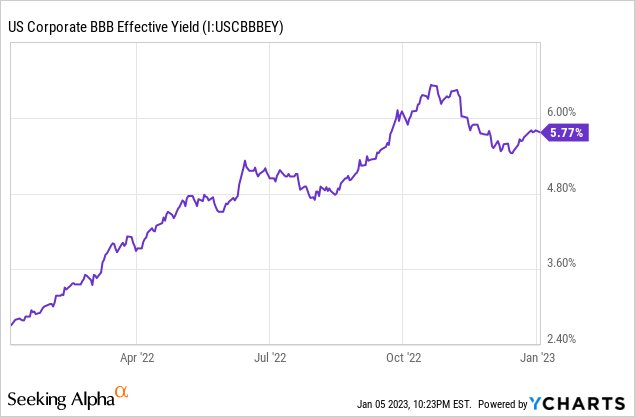

The question facing Fixed Income investors seems to be: “Is the year-end uptick going to continue or have rates peaked?”. Most experts believe the FOMC has anywhere from 75-125bps additional rate hikes in the pipeline before next fall; and that assumes inflation is more than just trending down. If the preverbal “soft landing” explodes, any rate decrease help to bonds could be more than offset by recession fears driving up default concerns.

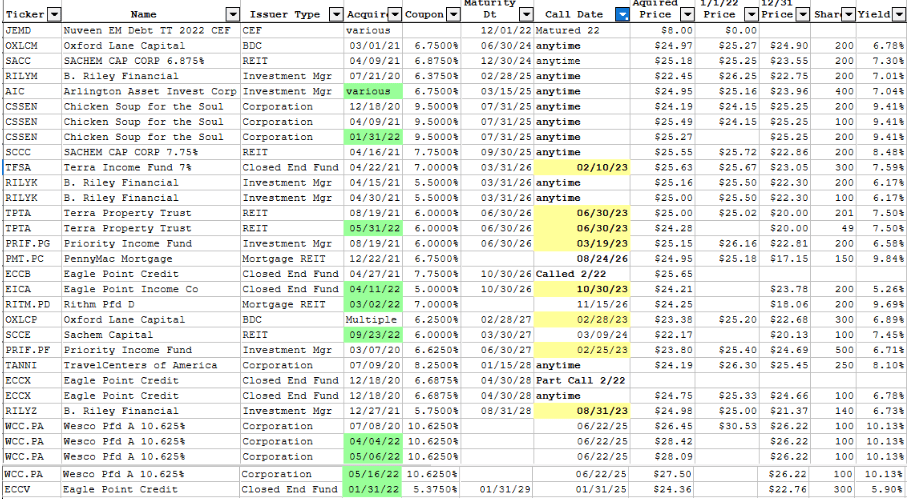

Current Ladder portfolio

Author’s Laddering XLS

The Green indicates assets acquired in 2022, which now account for 25% of the portfolio. The Yellow indicates that asset becomes callable in 2023.

Some basic statistics about the portfolio:

- Weighted Average Yield: 7.6%

- Weighted Average YTC/YTM: 10.3%

- Callable anytime: 45%; in 2023: 35%

- Maturities schedule: 24: 8%; 25: 25%; 26: 25%; 27: 17%, later: 14%

- No maturity date: 10%

- Three largest Issuer types: Investment Mgrs: 33%; Corporations: 24%; Closed-End-Funds: 17%

Assets no longer held

There was only one asset that “matured”, actually terminated, and that was the Nuveen Emerging Markets Debt 2022 Target Term Fund (XJEMX). Eagle Point Called all of the 7.75% Series B Cumul Term Preferred, and a 50% partial Call of their Eagle Point Capital 6.6875% Notes (ECCX). With so many assets becoming Call eligible in 2023, turnover could jump back to what I saw in 2021.

Assets added in 2022

Additions fall into three classifications:

New Issuer/New Issue

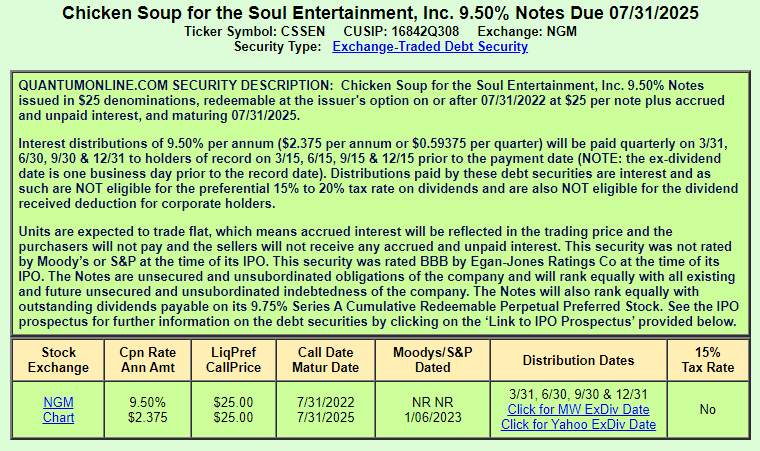

quantumonline.com

I have faith that asset managers are a safe bet and pick this up at a yield of 6.76%.

quantumonline.com

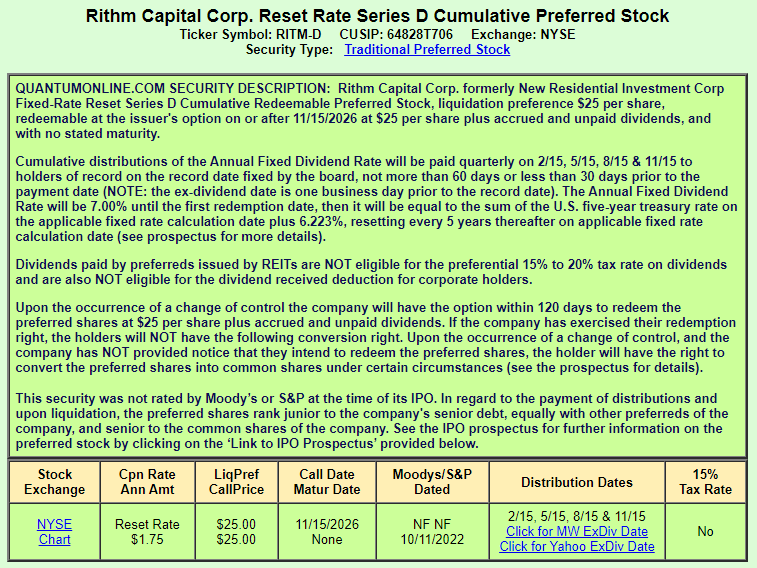

I did an article on this mREIT and its various Preferreds, and chose “D” as it has the longest time to Call and its floating rate is very attractive if it is not. This is my second mREIT exposure. Author’s note: The company changed its name since that article was published. The YTC was about 7.7% at time of purchase.

Existing Issuer/New Issue

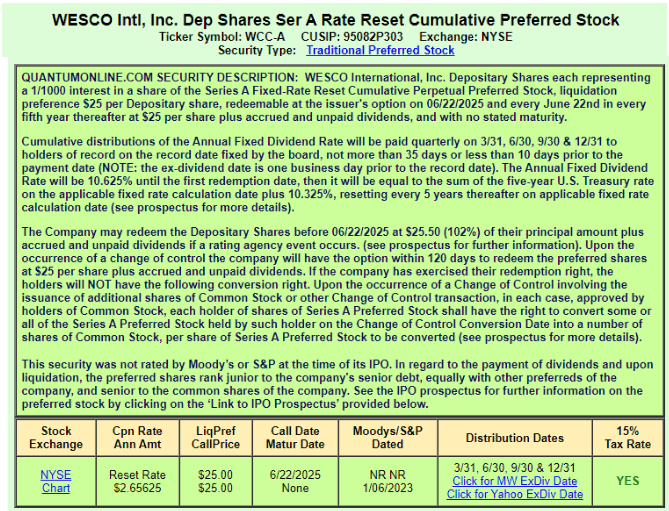

quantumonline.com

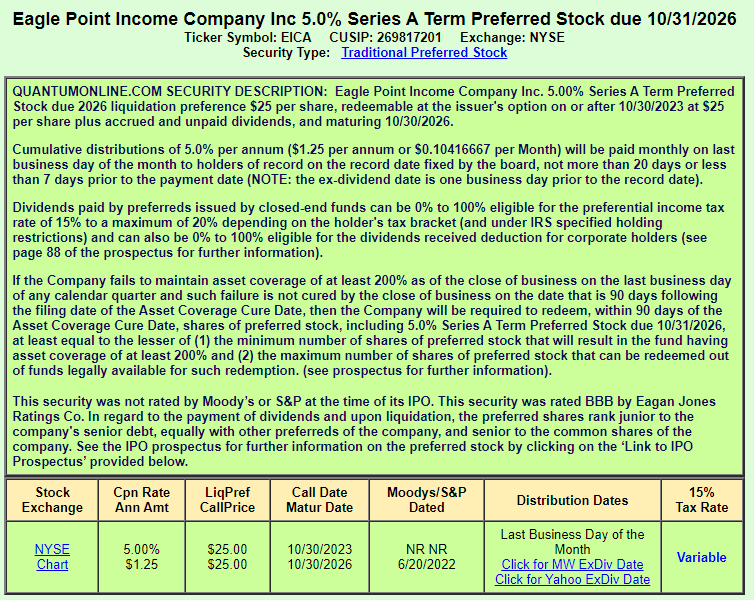

I added this as a replacement for ECCB that was Called and the partial Call of ECCX. With a YTM under 5.5%, it was one of the lowest in the portfolio. Their ability to call and replace made accepting the lower YTC okay, since I took that as a safety sign.

I also added ECCV as a replacement from Eagle Point.

quantumonline.com

While this has the longest time to maturity, if history repeats, it could get called much sooner.

quantumonline.com

I already held the Sachem Capital Corp. 7.75 NT 25 (SCCC) and the depressed price made adding more mREIT exposure worth the risk.

Position expansion

quantumonline.com

A year ago, there were high hopes that this issue would be called, even with rates rising. Not only did that not happen, I believe the company issued more of these Notes. While not Called as hoped for, the YTM was close to 9.5% at purchase.

quantumonline.com

This is a lightly trade Note, as many of these are, and I rounded up my position to 250. YTC at that time was just over 6%. Remember, CDs were still yielding almost nothing at the time.

quantumonline.com

Last June I did an article on WCC.PA about waiting for a good YTC. This preferred has traded above Par since being issued as part of a merger agreement. There are lots of opinions about buying above Par, mostly negative, but the measure to know is the YTC/YTM. If memory serves me right, I believe I added at YTCs around 7%. With the 10.625%, with possibly a higher floating rate, I cannot imagine this issue not being Called.

Portfolio strategy

As a retired couple whose only inflation adjusted income comes from two Social Security checks, one purpose of the ladder is to generate more income with minimal interest-rate risk than our other fixed income assets. The second purpose is holding some in our IRA accounts to generate the cash needed to make or RMD or QCD payments, which we now do quarterly using the QCD option.

The strategy has two components to reduce interest-rate risk. First, is the laddering itself so the assets do not all mature at the same time. Since most also have a Call feature, 100% certainty is not there. The more important part of the strategy is mostly using assets that actually have a maturity date. We have added a couple of Preferreds that do not, though the WCC.PA, because of its coupon, I assume will be Called in 2026 so I look at as having a maturity date.

Overall, this is a minor part of our overall investment portfolio, and with rates up, the worry about replacing a part because it was Called seems to have dried up for now and I suspect for the rest of 2023.

There, of course, is another risk when owning lower-rated fixed income assets; that being the default risk. While it hasn’t happened to us since Lehman Brothers went under (we still get small recoveries each year), that concern can drive down the prices of what we own, though that is immaterial if held to maturity and no default actually occurs. Our strategy to help reduce that risk is limiting exposure we have to an issuer and type of issuer.

What now?

This strategy, designed to enhance our income and return at a time when my broker was paying us 1bps, now has alternatives, though with risks. Baby bonds and preferreds can always stop paying interest, as some of these did in 2020; or worst, their issuer doesn’t make them good. My broker is now paying 3.85% on idle cash and 4.6+% on CDs maturing between 2-5 years. Since that second option comes with both interest penalties and selling difficulties, they do have a different type of risk. This translates to me as requiring 7+% YTC/YTM to expand this strategy. Assets with 6+% fixed, plus a floating component will be looked at closer too.

Final thought

Most of these preferreds and baby bonds are thinly traded and occasional move of up to $.50 occur. Also, wide bid/ask spreads are common so consider using limit orders and maybe below market bids with a GTC order.

Be the first to comment