DNY59

Market volatility is a value investor’s best friend, as this creates buying opportunities. This can be especially beneficial on high yielding stocks, such as those in the commercial mortgage REIT space. Such I find the case to be with Ladder Capital (NYSE:LADR), which is again trading below $11 on fears of higher interest rates from the Federal Reserve. This article highlights why this creates an opportunity on this high yielding stock.

Why LADR?

Ladder Capital is an internally-managed commercial mortgage REIT that’s focused on generating senior secured loans collateralized by high-quality properties in the middle-market. Since inception in 2008, LADR has made $45 billion of investments, including $30 billion of loans originated. At present, its portfolio carries $5.8 billion of assets across CRE loans, securities, and equity.

Ladder Capital carries a safe investment profile, as 98% of its loan investments are senior secured by first mortgage loans, with an average loan to value ratio of 68%, implying that the underlying properties would need to lose substantial equity value before LADR begins to take on losses. This also ensures that borrowers have significant skin in the game, and 82% of its balance sheet loans were originated post-COVID.

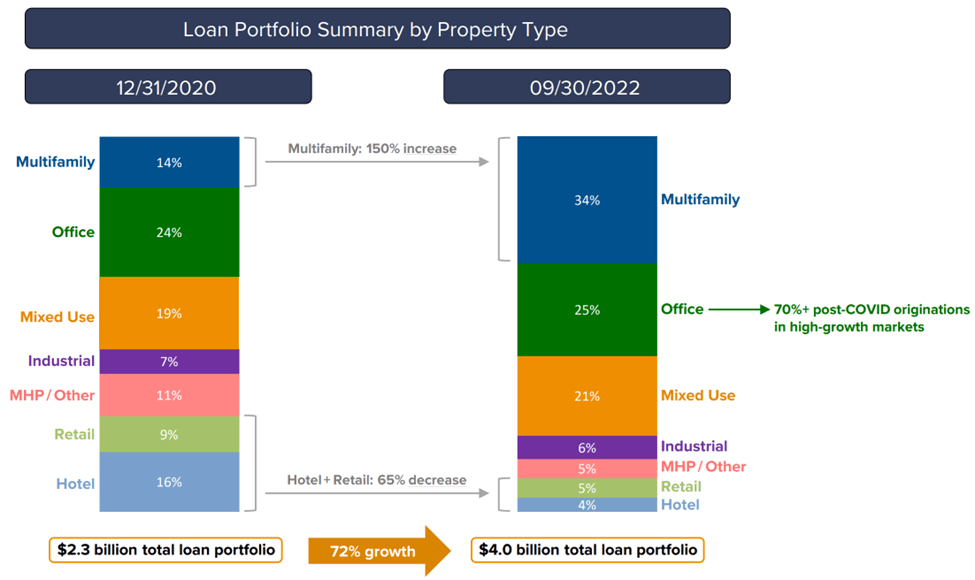

Importantly, unlike peers such as Broadmark Realty (BRMK), LADR has no exposure to riskier construction loans. While LADR has origins in New York City, its loans are well diversified by geography, with the rest of the U.S. beyond the Northeast comprising two-thirds of the portfolio. Also, over the past 2 years, LADR has greatly reduced its exposure to riskier hotel and retail segments, while increasing its exposure to the safer and growing multifamily segment, which now makes up 34% of the portfolio.

LADR Portfolio Transition (Investor Presentation)

Moreover, LADR is diversified with its own portfolio of physical real estate, 65% is landlord-friendly net leased. At present, the net lease portfolio has a gross asset value of $660 million spread across 157 properties in necessity based tenants such as Walgreens (WBA), Sam’s Club (WMT), and Bank of America (BAC). Over 68% are leased to investment grade rated tenants. They carry a long-weighted average remaining lease term of 10 years, similar to that of Realty Income Corp. (O), LADR is seeing 100% rent collection (over 98% on non-net lease properties).

Meanwhile, LADR is seeing strong operating fundamentals, generating a 9.1% return on equity, driven by strong net interest margin and rental income. It’s also has relatively low leverage compared to peers, with an adjusted debt to equity ratio of 1.8x, and has over $750 million in total liquidity. LADR is also seeing a healthy demand environment, as it originated $159 million of balance sheet loans, 86% of which were in either multifamily or manufactured housing.

The market has reacted negatively to a strong jobs report with higher wages, based on fears of rising rates. This is, however, a good thing for Ladder, as low unemployment is beneficial to its borrowers, and higher rates spell higher profitability for LADR, as 89% of LADR’s balance sheet loans are floating rate with interest rate floors.

Importantly for income investors, LADR currently yields a high 8.6% after the recent drop in share price, and the dividend is well covered by an 85% payout ratio based on $0.27 per share in distributable EPS during the third quarter. Notably, LADR’s undepreciated book value increased to $13.63 in the latest quarter, and at the current price of $10.71, it trades at a 21% discount to book.

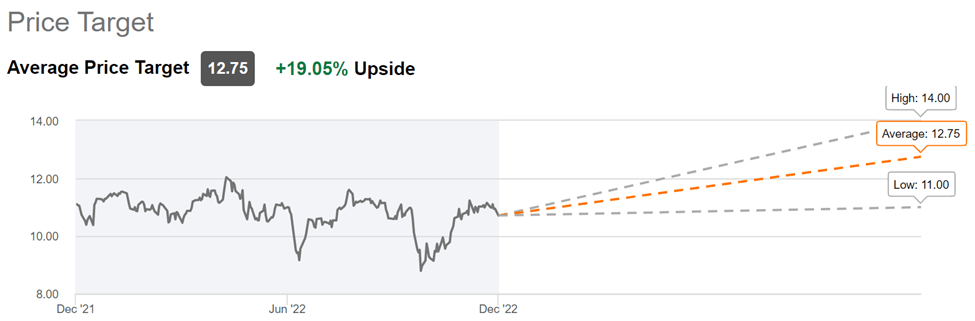

I believe this makes LADR rather cheap, especially considering its strong operating fundamentals and high insider ownership of 10%, more than 2x that of peers. Analysts have a consensus Buy rating on LADR with an average price target of $12.75, implying potential for strong double digit total returns including dividends. As shown below, LADR’s current share price sits even below the low end of its price target range.

LADR Price Target (Seeking Alpha)

Investor Takeaway

Ladder Capital carries a diversified portfolio of loans, securities, and net lease investments. It carries no exposure to riskier construction loans and has reduced its exposure to hotel and retail segments over the past two years. It’s seeing strong operating fundamentals and is positioned to benefit from higher interest rates amidst strong economic indicators such as low unemployment rates. I view LADR as being attractively priced at the moment with a discount to book value and a high and well-covered dividend yield.

Be the first to comment