South_agency/E+ via Getty Images

Summary

I see a 46% upside to Kura Sushi USA (NASDAQ:KRUS). The thesis is fairly simple. KRUS is akin to a quick-service restaurant [QSR] that has significant growth opportunities across the entire nation. Given the low base (42 units in 1Q23) and strong payback period, I believe KRUS can continue to expand in a very profitable manner.

Company overview

KRUS is a chain of sushi restaurants based in the United States. The concept revolves around a revolving conveyor belt filled with various small plate items, such as sushi, nigiri, and desserts, that diners can choose from on their own or have delivered to their tables via digital ordering screens.

Plenty of space available to grow

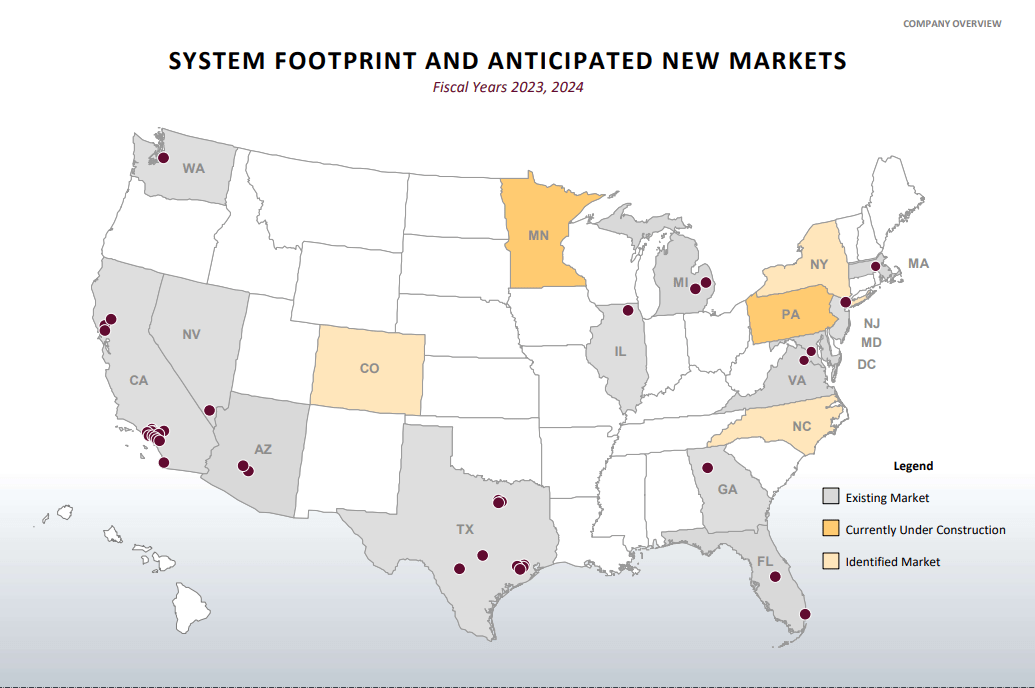

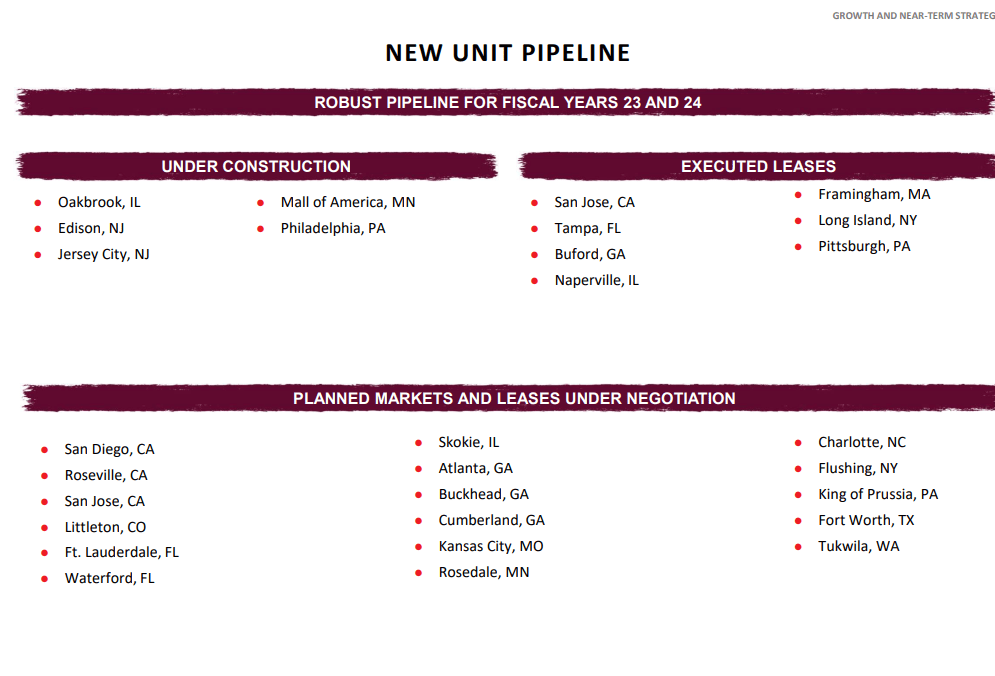

Given its early stage of development, I believe there is great potential for further expansion of the unit. I have no doubt that the KRUS concept can rapidly scale up to encompass many more units across the country. The growth potential can be visualized by comparing it to that of other QSRs like Shake Shack (SHAK), Chipotle (CMG), and Domino’s (DPZ). Personally, I think KRUS is just like any other QSR in that its model can be ported to other locations with little effort. In addition, KRUS’ current small size of 42 units in 1Q23 indicates that the company has significant room for expansion. To put this into perspective, a 15% increase in revenue can be easily achieved by opening four new units per year and increasing the average number of units by five percent (likely due to inflation today). I am aware of the difficulties inherent in expanding a restaurant chain beyond a regional footprint, but I am confident that KRUS model, impressive unit metrics, and global success will help it overcome these obstacles.

Considering the population density, target demographics, and higher seafood consumption rates on the East and West Coasts, I believe that KRUS’s executives would be wise to focus on expanding their presence there. Taking a look at the existing system footprint and the upcoming opening pipelines suggests this to be the case. Overall, I think KRUS has enough room to grow in its current West Coast markets and into new East Coast markets without having to expand into areas where seafood supply is more difficult or expensive.

Stephens Annual Investment Conference Presentation Nov 22 Stephens Annual Investment Conference Presentation Nov 22

Restaurant concept built for efficiency

KRUS top-tier sales productivity is a key indicator of its popularity among consumers and a positive sign for the company’s bottom line. Based on KRUS average unit size, which is approximately 3,600 square feet, I estimate that it is bringing in approximately $1,062 per square foot in sales. This is relatively good when compared to the sales productivity of Chili’s (EAT), Red Robin Gourmet Burgers (RRGB), Texas Roadhouse (TXRH), and Olive Garden (DRI). KRUS’s advantage, in my opinion, stems from the fact that its units are relatively small, and its business model is predominately self-service, both of which give patrons more say over how long they spend in the restaurant and thus likely lead to quicker table turns.

Assuming a check average in the high teens, I calculate that KRUS sees about 60 transactions per square foot, which is higher than other casual dining concepts like Cheesecake Factory and TXRH and on par with CMG. CMG’s make-line service model, which places a premium on throughput, and the fact that more than half of orders are eaten outside the restaurant make KRUS achievement all the more remarkable. This high transaction productivity, in my opinion, is evidence of robust customer demand and lends credibility to the concept, making it possible to expand into additional restaurants. On the flip side, I worry that restaurants’ low peak-time capacity is stifling future growth in foot traffic because of their high productivity. Gains in foot traffic will likely need to come from off-peak hours, which is challenging for casual dining, or from off-site sales. Most, if not all, KRUS eateries, in my opinion, are already swamped during peak lunch and dinner hours, so increasing sales at existing locations will have to come from raising prices or increasing the average check size.

Strong unit economics

KRUS’s one-of-a-kind restaurant layout and business model result in steadily rising unit economic metrics. On average, each KRUS will bring in close to $4 million in sales during FY22, with an operating margin of 21.2%. This equates to close to $840,000 in operating profits. Given that a new unit’s development costs around $1.6 million, this equates to a payback period of about twice as long, which is very appealing to me. If you’re an investor, that’s like seeing your money double every two years, or a CAGR of 41%. I think management should keep putting forth maximum effort into introducing brand-new units given the enticing returns they’re currently receiving. Here, the payback period makes sense even if operating margins drop by 33% due to factors like lower population density ($1.6 million / $560k = 3 years).

Other growth opportunities

Since KRUS has such high unit and transaction volumes, I think the two biggest sales opportunities at existing restaurants are off-premises sales and alcohol sales. Once accounting for less than one percent of KRUS’s revenue, off-premises sales have grown steadily in recent years, according to company management’s remarks at the 2022 Stephens Annual Investment Conference. Given consumers’ increasing preference for convenience, I anticipate that off-premises sales growth will continue to be the primary driver of casual dining same-store sales growth in the foreseeable future. In my opinion, KRUS is well-positioned to take advantage of this development because the concept’s emphasis on tech-enabled ordering gives it a leg up on digital ordering. Furthermore, I believe that making this ordering platform available to customers via website or mobile ordering could prove to be a natural extension and probably present fewer integration issues.

KRUS, in my opinion, is missing out on a huge opportunity in the alcohol industry, particularly in on-premise sales (alcohol currently represents a small portion of sales at Kura). Given the higher profitability of alcohol sales, increasing this mix could improve average check, sales, and restaurant margins. Given the concept’s commitment to traditional Japanese cuisine and culture, I think it would benefit from putting more focus on and promoting its carefully selected alcohol offering, including sake.

Valuation

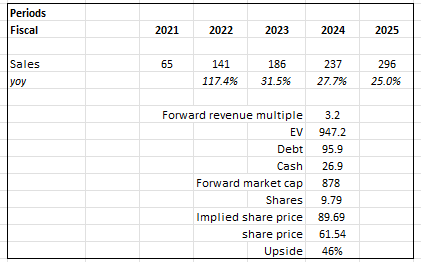

I believe KRUS there is 46% upside. Based on my estimates, I expect KRUS to generate $296 million in revenue in FY25. The growth algorithm is clear: new stores + SSS = revenue growth.

As mentioned earlier, I believe there is significant whitespace for KRUS to continue expanding the number of stores across the nation. In terms of momentum, KRUS did not show any signs of slowdown either – revenue grew 30% in the latest quarter. As KRUS is still in the growth phase, which it should be, I believe investors are not valuing through the lens of profitability but instead on growth (revenue).

Using the current forward revenue multiple of 3.2x, it implies that KRUS is worth $950 million in enterprise value, which translates to $89.69 per share.

Own calculations

Risks

Expansion into other states

While the above illustration shows a lot of white space, there is a possibility that some of it could be used to transport an entirely new idea. What has been successful in one area or state may not be applicable in another. If this holds true for the majority of the white space we’ve identified, it could severely limit KRUS capacity for future expansion.

Another Covid-like situation

The lack of customers during the Covid period was devastating to KRUS’s business, as it is primarily a sit-down restaurant. KRUS’s financials and valuation would likely be severely impacted by another pandemic of similar severity.

Conclusion

There isn’t much complexity to the thesis. Similar to QSRs, KRUS has great potential for expansion throughout the middle of the United States. KRUS has a low starting point (42 units in 1Q23) and a very good payback period, so I expect it to continue expanding in a highly profitable way.

Be the first to comment