RHJ

Incorporated in 1989, Kronos Worldwide (NYSE:KRO) is one of the top five global titanium dioxide (TiO2) pigment producers. With its broad customer base, the company markets its products in over 100 countries. The company’s sales Primarily come from Europe, North America, and Asia Pacific regions.

Also, because of its exceptional durability, impart whiteness, and opacity, TiO2 has been a critical component for coasting, plastic, paper, and the food industry. Although various substitutes are available in the market, their effectiveness compared to TiO2 has been considerably low.

Furthermore, the company operates in an industry that poses a high barrier for new entrants; therefore, over the period, the industry has not seen any increased capacity, and most of the players prefer to expand their production through debottlenecking. Therefore, the risk of capacity addition seems low which provides significant safety to the business. But investors must consider that the business operates in a slow-growing industry where demand is considerably unstable.

Valhi owns a significant stake in Kronos, partially through direct shareholding and partially through a stake in the NL industry (NL industries own a 30% interest in the company through its subsidiary). A family trust indirectly owns a significant stake in Valhi. Such a shareholding structure might affect investors’ sentiments about the stock.

Although the business performance seems considerably stable, the volatile market prices for TiO2 might affect the profitability and financial position of the business. Therefore, I believe investors must take seek substantially discounted valuation while holding a position in such a cyclical stock. Also, cyclical stocks provide significant downside risk; therefore, buying at a substantially discounted price remains the best option to achieve desirable returns.

Currently, the company has been trading for $1.27 billion, whereas it has produced over $124 million in the last nine months, which gives it a PE of 10. Earnings multiple of ten (Last nine months’ earnings) for the cyclical stock seems fair in its cyclical uptrend. From this price point, the stock may not produce considerable returns for the shareholder but can bring a substantial risk of a cyclical downturn.

Historical performance

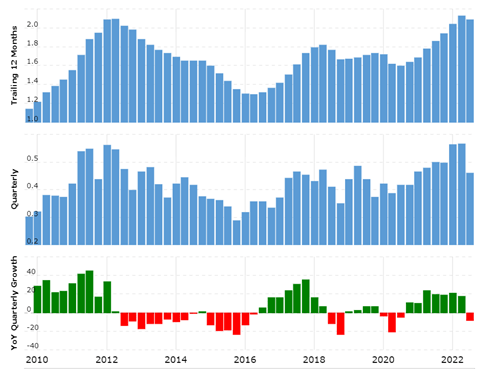

Revenue (Macrotrend.net)

In the last ten years, revenue has remained significantly volatile; after reaching a low of $1.3 billion in 2015, it has increased considerably to date; in the last year, revenue touched $1.9 billion. Also, the net profit margins have seen huge fluctuations over the underlying period. Such significant ups and downs in business performance might be attributed to the industry’s cyclical nature, where the company doesn’t have pricing power over its customer.

Also, in the last few years, the company’s liquidity profile has improved considerably; the company ended the recent quarter with $338 million in cash and over $1.2 billion in current assets, whereas it has long-term debt of about $390 million. Having such a strong financial position can improve business sustainability if a cyclical downturn hits the industry.

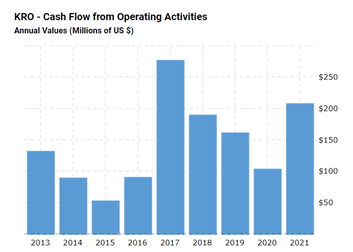

cash flow from operations (macrotrends.net)

It should be appreciated that over the last ten years, cash flow from operations has been positive and has produced significant cash for the business, which has been used to pay dividends.

As the business performance fluctuates widely, it becomes difficult to find out the actual earning power of the business; therefore, buying the share during its cyclical downturn can only provide the best results.

Also, after falling to $4.2 per share during the 2015 downturn, the stock has remained volatile and has reached $11 per share. Although the stock has lost nearly $41% of its value from the 2022 high, the price might drop further if the business performance starts deteriorating.

Strength in the business model

Having a substantially stable financial position provides significant safety to the business model. If the downturn hit the industry, the company has considerable liquidity to cope with the situation. In contrast, its competitors, such as Venator Materials (NYSE:VNTR), may face trouble because of high debt.

Also, it should be appreciated that despite the economic downturn in the last nine months, the business has maintained its profitability. Therefore, as the economy starts recovering, the company might see higher demand with higher profitability.

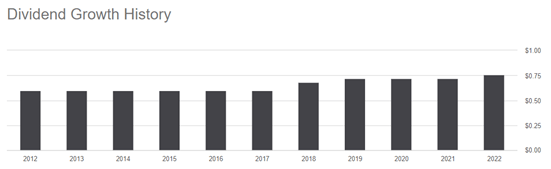

Dividends (macrotrends.net)

Furthermore, the company has distributed considerable dividends to the shareholders over the period, which seems a very healthy sign of business operation.

Risk factors

Due to competitive pressures, our Chemicals Segment’s average TiO2 selling prices decreased throughout 2014 and 2015. Our Chemicals Segment’s average selling prices at the end of 2015 were 17% lower than at the end of 2014, with lower prices in all major markets, most notably in North American and certain export markets. Our Chemicals Segment’s average selling prices in 2015 were also impacted by a higher percentage of sales to lower-priced export markets in 2015 compared to 2014.

Annual report Valhi (holding company of Kronos inc.) – 2015

It should be noted that the business performance is significantly dependent on the price and demand of TiO2; in 2015, due to a drop in prices, the company had to incur losses. Therefore, as the business performance fluctuates significantly, such a situation might affect the business in the upcoming years.

Also, Exceptional performance in 2018 was attributed to reduced capacity from a Chinese manufacturer (related to environmental issues). Therefore, the business performance can get affected if the new capacity is entered again. Although there seems to be a very low chance of new capacity entrance, existing players can ramp up production through debottlenecking during higher demand, which may again create pricing pressure. Chemours (NYSE:CC) states in its recent annual report that it can increase its production by 10% during high demand. Such an increase in production can drive down margins. Any reduction in net profit margins from this point might affect the share price significantly; In such case, the stock price might see a substantial correction.

Recent development

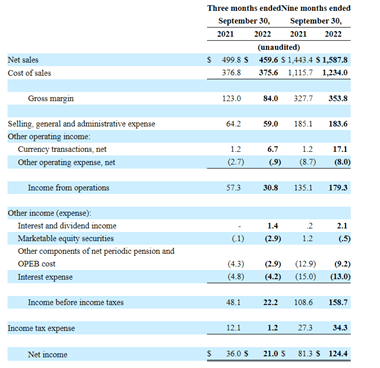

Quarterly result (Quarterly report)

In the recent quarter, the company posted revenue of over $459 million against $499 million in the same quarter last year. As a result, net profits have dropped to $21 million. In my view, such performance seems considerably attractive because the company has maintained its profitability even in the inflationary environment.

Also, sales and net profit have increased considerably over the last nine months. Although the cash flow has reduced due to higher inventory, the company has maintained its dividend payment.

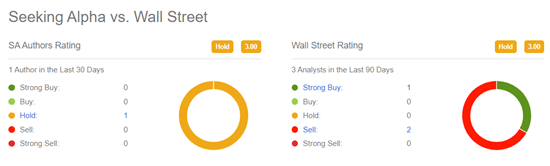

Seeking Alpha ratings (Seeking Alpha)

Currently, the stock is trading for ten times its last nine months’ earnings. Such a valuation seems fair for a cyclical stock; from this point, the stock may not give considerable returns; instead, there comes the risk of a cyclical downturn; Therefore, I assign sell ratings to the stock.

Be the first to comment