WendellandCarolyn/iStock Editorial via Getty Images

Investment Thesis

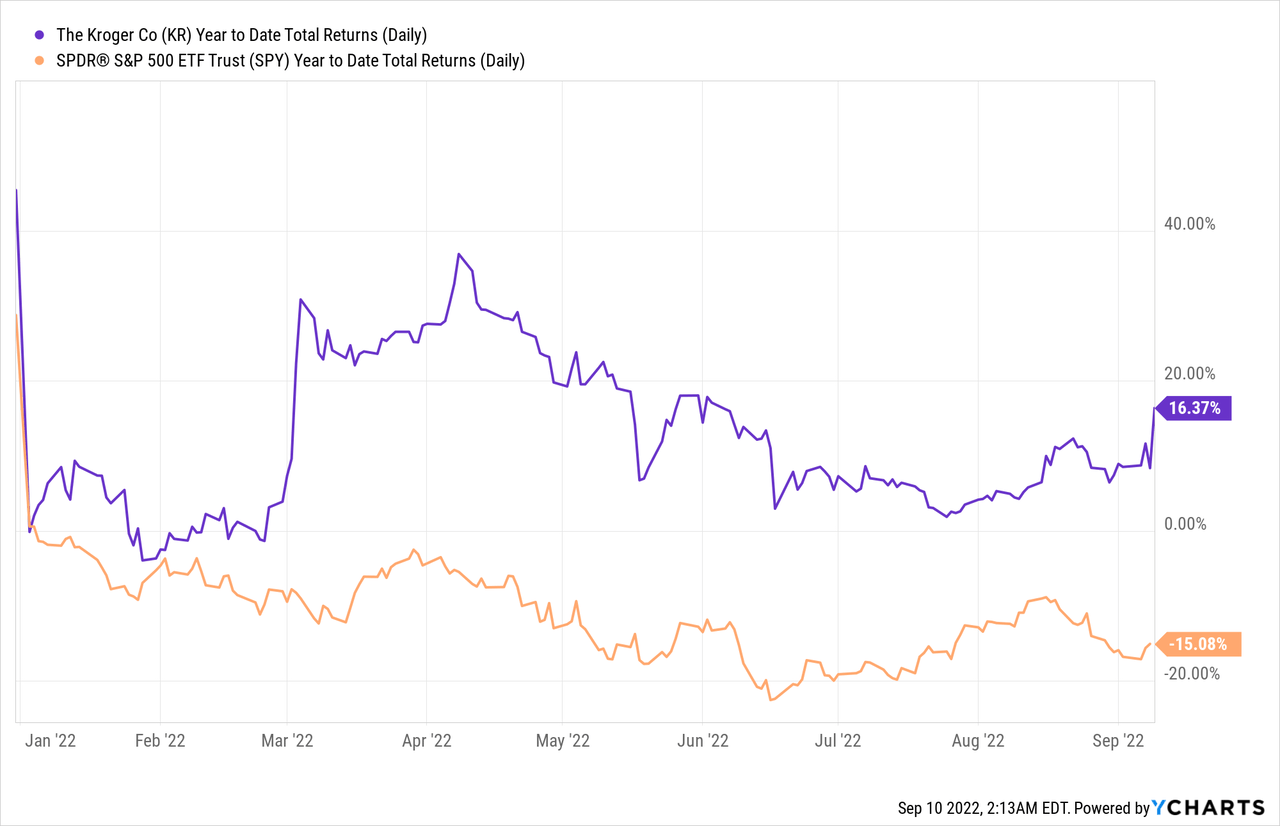

Kroger (NYSE:KR), founded back in 1883, is one of the largest grocery companies in the US. Thanks to the nature of its business, the company has been performing really well this year, up 14.9% year-to-date, significantly outperforming the S&P, which is currently down 15.2% year-to-date. Kroger reported its earnings last Friday, and shares popped over 7% as the company posted yet another beat and raise.

Despite the recent pop, the FWD P/E ratio is only around 12.2, which is very compelling. The company also has growth catalysts such as the increased adoption of digital sales and in-house brands. I believe Kroger is a good defensive investment during volatile times like these as it continues to show strong resilience. Therefore, I rate the company as a buy at the current price.

Multiple Growth Opportunities

While Kroger has been around for decades, it is still seeing new growth opportunities. The company’s growth strategy currently revolves around digital sales, in-house brands, and its new membership program.

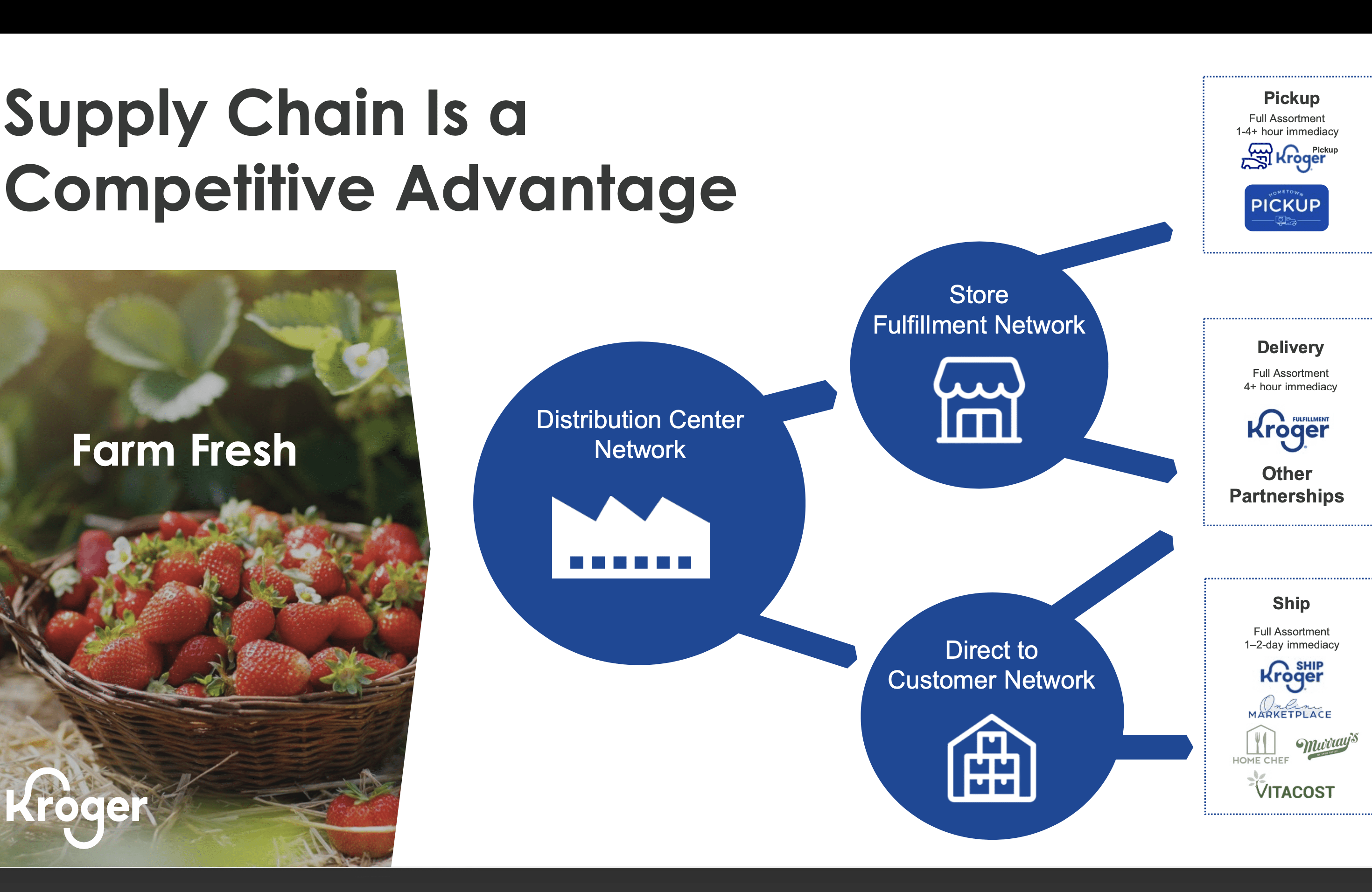

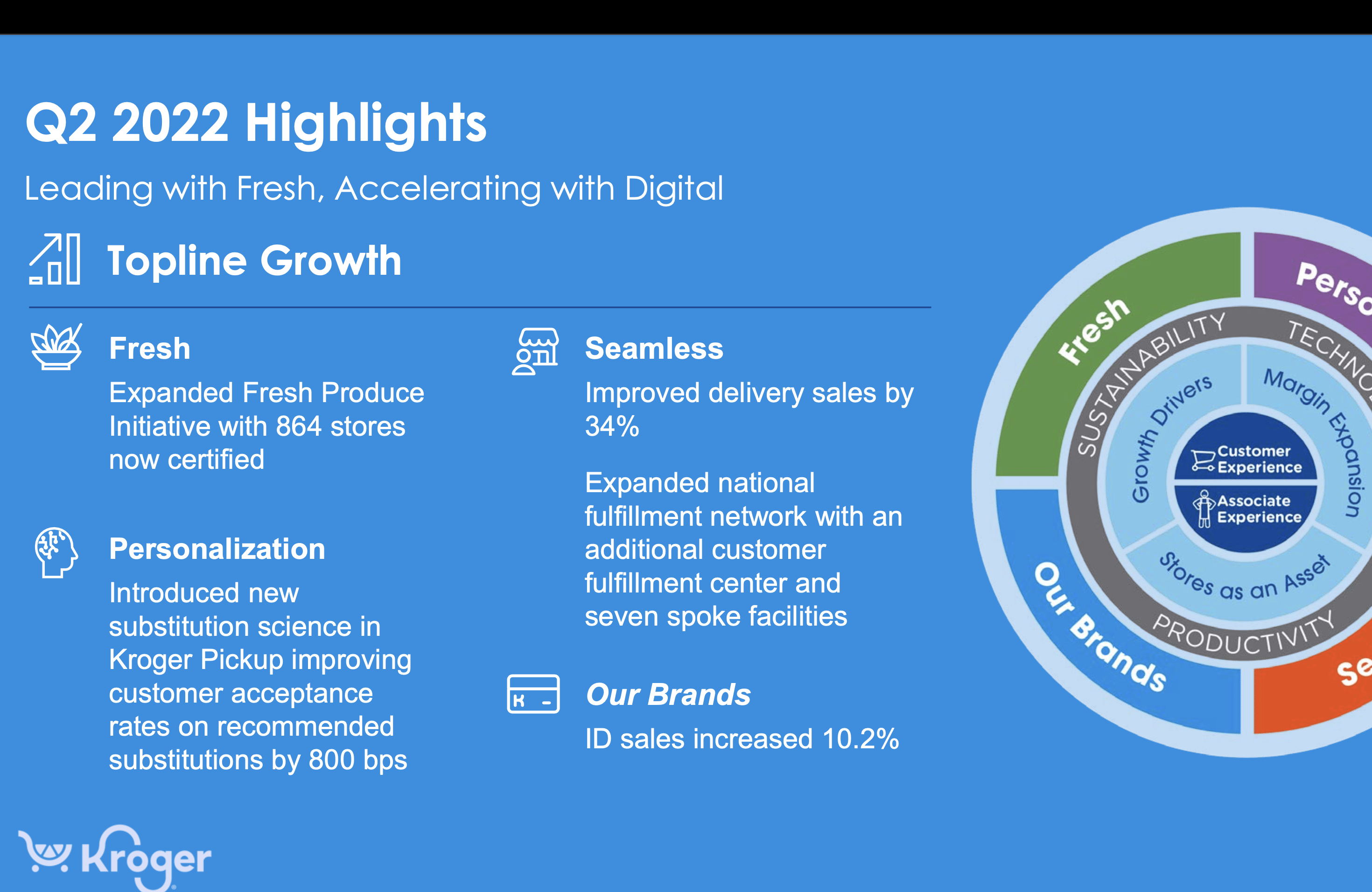

Back in 2020, COVID and lockdowns significantly boosted the adoption of digital sales as consumers are forced to stay at home. While we are getting past this phase, the trend is continuing to see strong traction. Unlike other players that suddenly emerged during COVID such as Boxed (BOXD), Kroger has a significant competitive advantage as it owns one of the largest fulfillment and distribution networks in the country. This results in a reduction in delivery time and an increased reach to more rural areas. The company is not planning to stop and it recently expanded its footprint into new geographies like Austin, Oklahoma City, and San Antonio. It is also increasing digital adoption through digital coupons. In the recent quarter, over 750 million digital offers are downloaded, representing an all-time high engagement rate.

Kroger

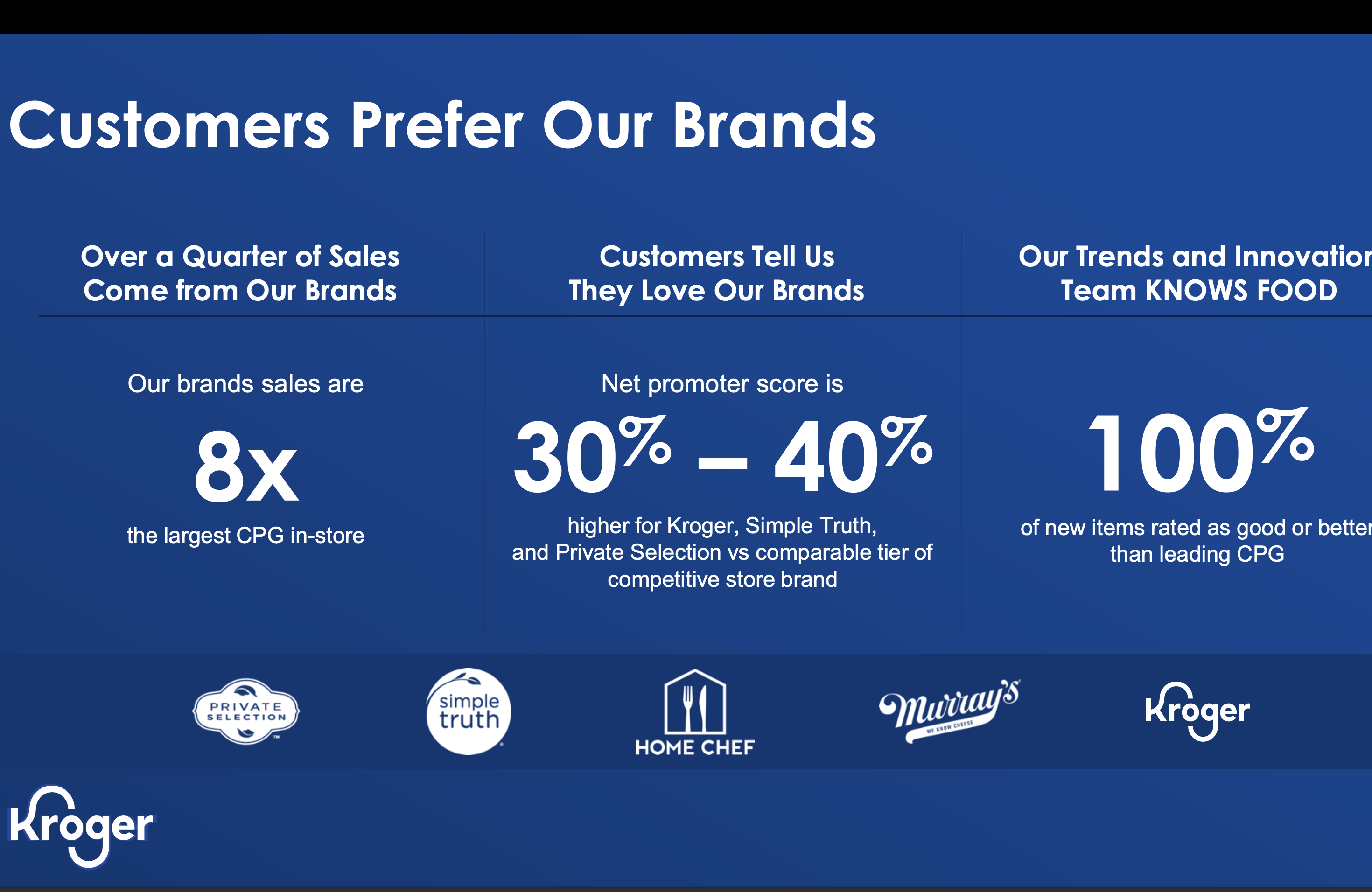

In-house brands are also seeing strong traction. As inflation persists, consumers are now turning to more affordable products. Compared to other external brands, Kroger’s in-house brands are competitively priced and meet the needs of customers on a budget. As more families are now eating at home, Kroger’s brands are able to offer a budget-friendly alternative. According to Kroger, the NPS score for its product is also 30%-40% higher than other store brands, indicating strong competitiveness on quality. During the last quarter, the company launched 150 SKUs for its own brands and is expected to roll out additional products throughout the second half of the year. This will likely increase the wallet of shares for in-house brands. In-house brands also have better profitability compared to external brands which benefits the company’s bottom line.

Rodney McMullen, CEO, on in-house brands

We saw incredible engagement in Our Brands during the quarter with identical sales growth of 10.2% compared to last year. This increase was led by our Kroger and Home Chef brands. Convenience remains a priority and Home Chef is meeting that need by providing high-quality family meals as a budget-friendly alternative to eating out at restaurants.

Kroger

Earlier in July, Kroger launched its Boost membership for customers nationwide, the latest loyalty program from the company. The annual membership provides customers with unlimited free grocery delivery on orders of $35 or more, fuel discounts of up to $1 per gallon, and additional savings on in-house brand products. The annual membership comes in two tiers which are priced at $59 and $99. I believe the membership program is likely going to improve engagement and retention rates over time, driven by free delivery and discounts. This is also going to improve the company’s bottom line as the margins on the membership program are much higher than retail. The adoption of Boost will likely be a strong catalyst in the near term.

Rodney McMullen, CEO, on Boost membership

Early in the second quarter, we introduced our Boost membership nationwide, and it’s already showing promising results including an increase in overall household spending among members. We remain focused on adding new members and are encouraged that enrollment is in line with our internal expectations and projections.

Dividend and Buybacks

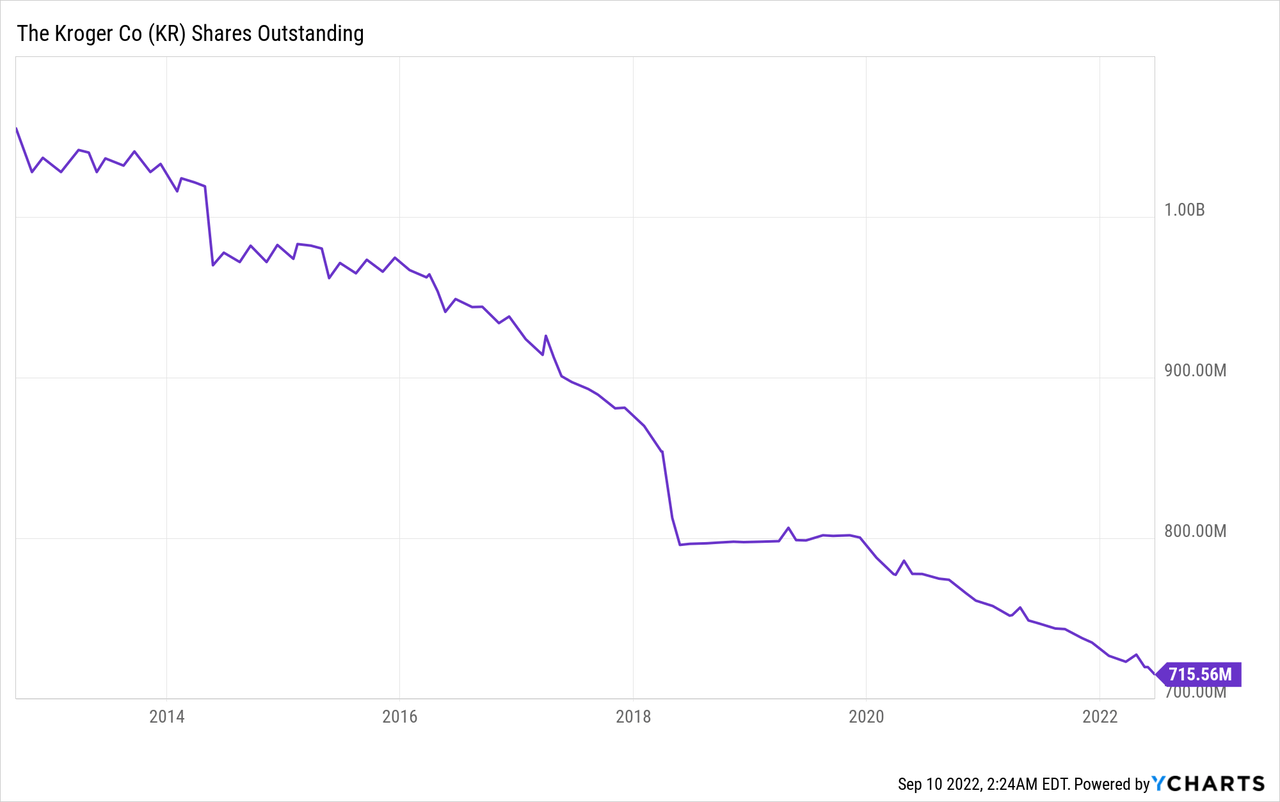

Another reason to invest in Kroger is shareholder-friendly policies. The company has been very committed to returning cash to shareholders. From 2017 to 2020, it returned over 7 billion to shareholders through dividends and stock repurchases. In the latest quarter, the company repurchased $309 million in shares and announced that it authorized a new $1 billion share repurchase program. From the chart below, you can see that the number of shares outstanding had been trending down steadily. Besides, dividends have also been growing. From 2006 to 2021, the company reported a dividend CAGR of 13%. Earlier in June, the board announced that it is raising its quarterly dividend by 24%, marking the 16th consecutive year of dividend increases. Despite the recent increase, the current payout ratio is only roughly 22%. I believe the company will continue to authorize larger-than-expected increases in dividends in the future.

Second Quarter Earnings

Kroger reported its second quarter earnings last Friday and it easily breezed past expectations. The company reported sales of $34.6 billion compared to $31.7 billion, up 5.8% YoY (year-over-year) excluding fuel. The growth is driven by strong in-house brand sales and digital sales, which increased by 10.2% and 8%, respectively. While the company does not disclose the sales figures, revenue for delivery solutions grew by 34%. Kroger mentioned in the latest report that in-house brand and digital sales now present a $28 billion and $10 billion opportunity. The expansion of its delivery network into new geographies is likely to provide further growth moving forward.

Rodney McMullen, CEO, on second quarter earnings

Kroger delivered strong second quarter results propelled by our Leading with Fresh and Accelerating with Digital strategy. Our consistent performance underscores the resiliency and flexibility of our business model, which enables Kroger to thrive in many different operating environments.

Kroger

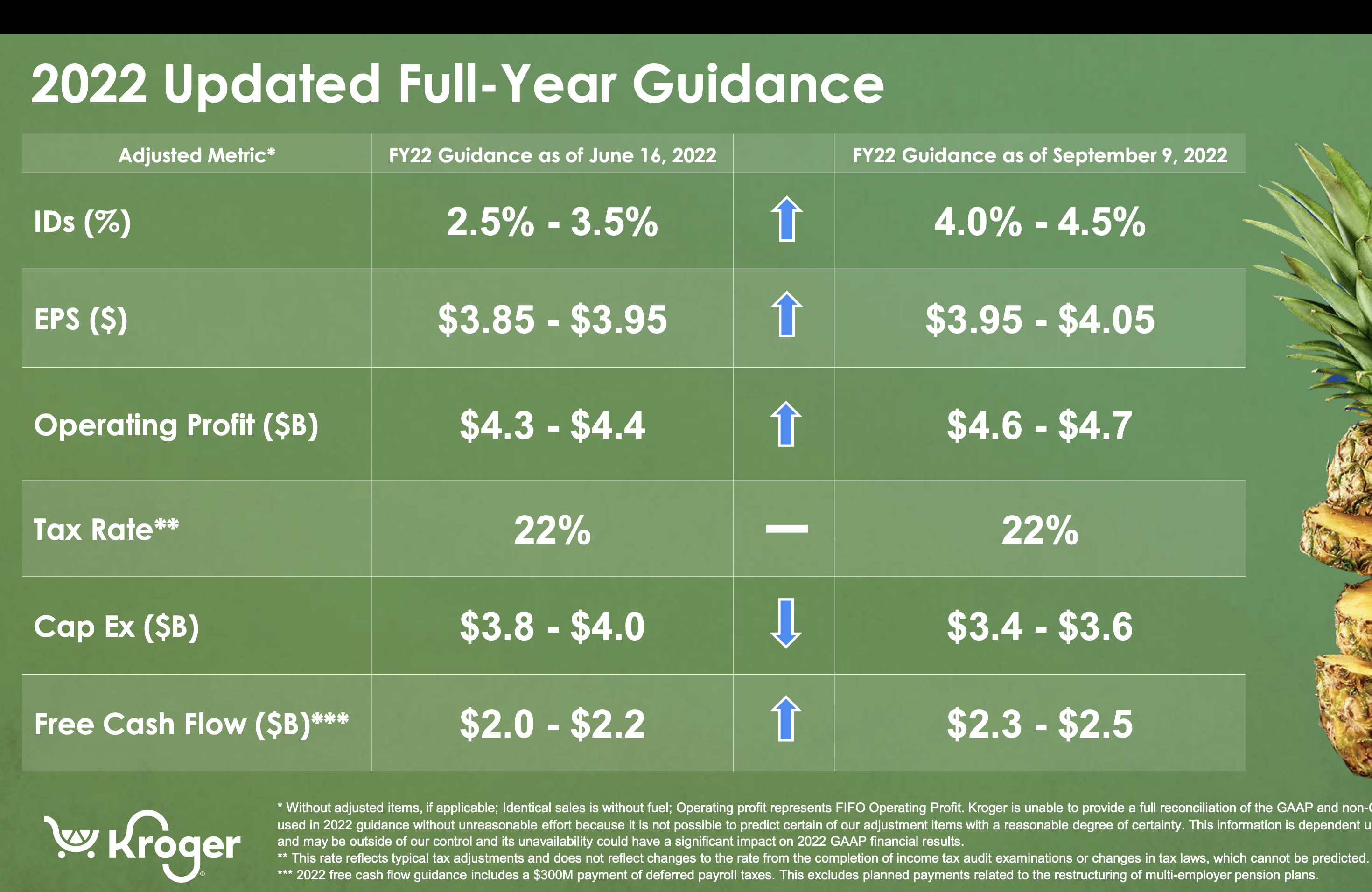

The company’s bottom line for the quarter was superb. Operating profit increased 13.4% YoY from $839 million to $954 million. The growth is due to the increase in profit margins, which were up 2 basis points to 2.8%. Adjusted EPS was $0.9 compared to 0.8, representing an increase of 12.5%. It is continuing to see success in cost-cutting efforts, currently on track for $1 billion in annual savings. Given the strong backdrop, Kroger announced that it is raising the full-year guidance. Identical sales growth is expected to be between 4%-4.5%, up from 2.5%-3.5%. EPS target range increased from $3.85-$3.95 to $3.95-$4.06, while the target range for free cash flow also increased from $2-2.2 to $2.3-2.5.

Kroger’s current balance sheet also remains very healthy. It currently has a net total debt to adjusted EBITDA ratio of 1.63, down from 1.78 a year ago. This is way below the company’s target range of 2.30 to 2.50, giving it a lot of room for further dividend increases and share repurchases.

Kroger

Valuation

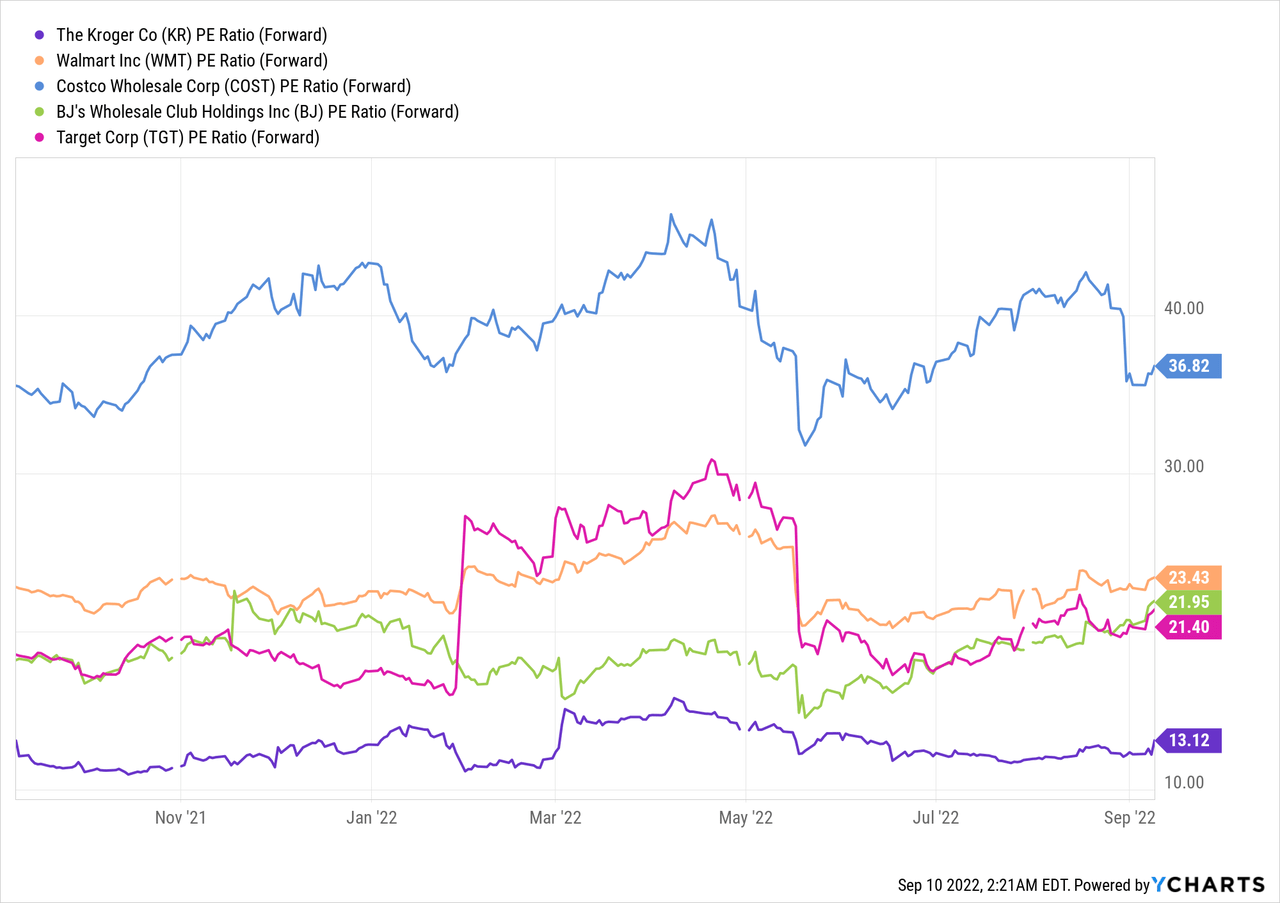

Kroger is currently trading at an FWD P/E ratio of 13.1, which is very compelling in my opinion. From the chart shown below, you can see that the company is valued at a significant discount compared to other big retailers such as Walmart (WMT), Costco (COST), Target (TGT), and BJ’s (BJ). These companies are all trading at an FWD P/E ratio of around 22, with Costco being the only outlier, trading at 36.8 times forward earnings. This is a 67.9% premium we are talking about. While Kroger’s sales growth has historically been around mid single-digit compared to high single digits from others, the premium is still too much in my opinion. The company is continuing to beat and raise earnings while buying back shares constantly, which will further boost its EPS growth. I believe the valuation gap between Kroger and other retailers is unjustified and will eventually contract. This will revise Kroger’s valuation upward and boosts its share price.

Conclusion

One of the few risks I see in regards to Kroger is a severe recession happening, which results in broad demand destruction. This happened during the great financial crisis, resulting in a large contraction in EPS. However, the chances of it happening is low, as the Fed will likely provide strong support if it were to happen. Competition is another potential risk, but the new membership program and products are likely to improve customer loyalty.

In conclusion, I believe Kroger will be one of the few stocks that continue to show resilience in a very volatile market. The company is seeing strong growth opportunities in areas such as digital sales, in-house brands, and the new Boost membership. Thanks to these catalysts, it posted a beat and raise once again, showing no sign of deterioration despite facing a tough macro environment. The company is also actively returning cash back to shareholders, recently authorizing a dividend raise and a new buyback program. While fundamentals continue to be strong, Kroger is still being valued cheaply compared to other retailers. The current valuation is attractive as a revision in multiples will offer meaningful upside in share price. Therefore, I rate Kroger as a buy at the current price.

Be the first to comment