Editor’s note: Seeking Alpha is proud to welcome William Madsen as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

ImagineGolf

Kolibri Global Energy (OTCQX:KGEIF)(TSX:KEI:CA) has a long runway for growth, with a relatively undeveloped oil play in southern Oklahoma. The company was inactive in the area from 2019 to 2021, with no drilling program due to the low commodity price environment and an inability to raise further financing. Average production in 2021 was only 975 BOEPD. A recent equity rights offering in late 2021 allowed Kolibri to resume drilling in the area, and the company announced a 2022 exit rate of over 4000 BOEPD in their latest press release. The success of the 2022 drilling program should lead to large upward year-end reserves adjustments on proved developed producing (PDP) reserves and proved undeveloped (PUD) reserves. This could in turn lead to access to further financing, and a potential acceleration in the development of the play. The market might also give more value to the company’s current reserves in place based on these recent results.

Kolibri is a junior oil and gas producer operating in southern Oklahoma in the Tishomingo field. As of Q3 2022, Kolibri had a production weighting of 74% oil, 16% NGLs, and 10% gas. The company has approximately 17,000 net acres of land in the Caney shale formation.

As previously mentioned, the company performed an equity rights offering in late 2021, raising C$8.6M. These funds were used to drill and complete the first two wells of the company’s five-well 2022 drilling program. While this caused heavy share dilution (increasing share count by 53%), this was the only option available at the time as the company’s credit facility with the Bank of Oklahoma was already fully drawn.

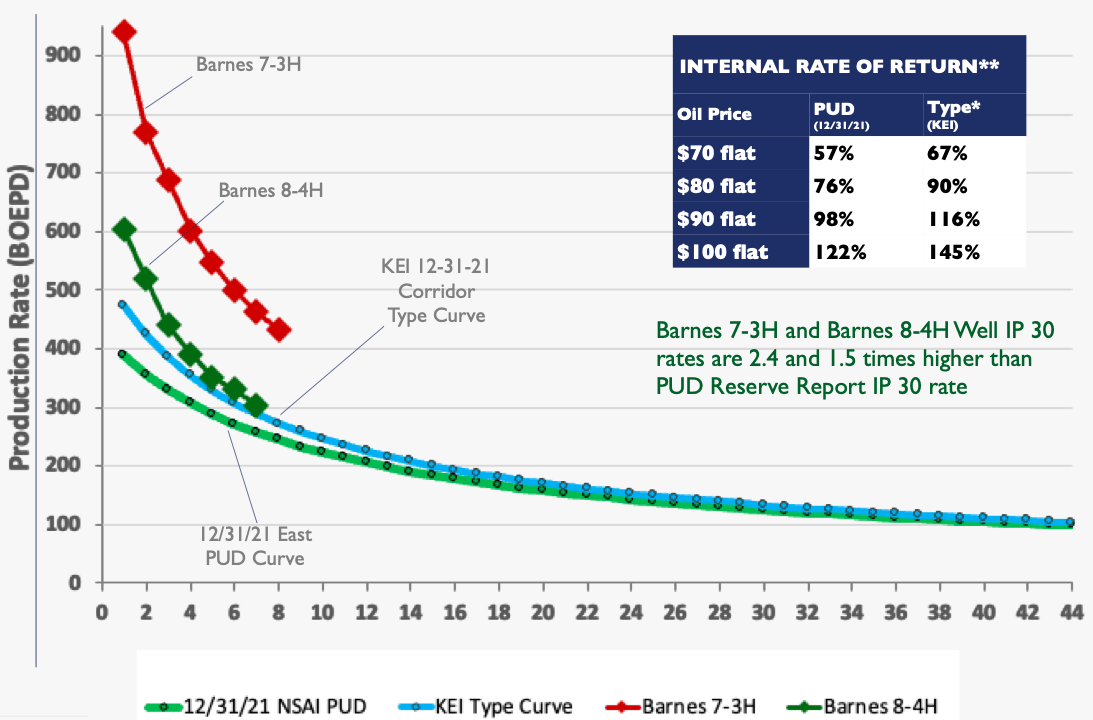

These first two wells (Barnes 7-3H and 8-4H) came online in March and April and were very successful, producing well above both third-party reserves estimates and internal management type curve estimates as outlined in the December 2022 corporate presentation.

KEI Presentation Dec 2022

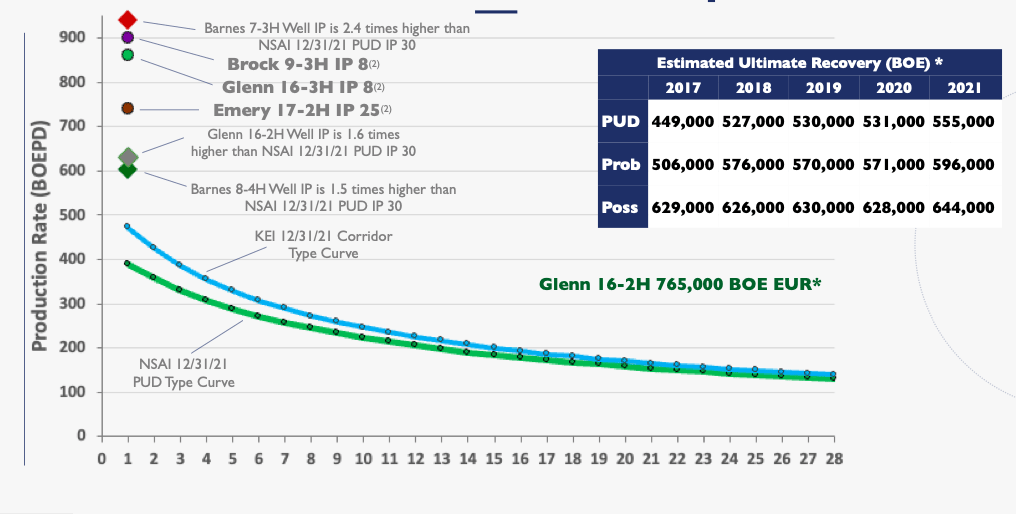

The other three wells in the 2022 drilling program were completed and brought online in November (Emery 17-2H) and December (Brock 9-3H and Glenn 16-3H). As of the most recent press release, these wells are also performing very favorably so far as compared to type curve estimates.

KEI Presentation Dec 2022

Management gives credit to a change in completion design that was first implemented in 2018, in which a high viscosity friction reducer (HVFR) is used to improve near wellbore stimulation and reduce fracture length. The Glenn 16-2H well completed with this technique in 2018 has also performed significantly above type curve estimates. These results seem to indicate that the company has optimized completion designs for the area and could lead to more consistent drilling results going forward.

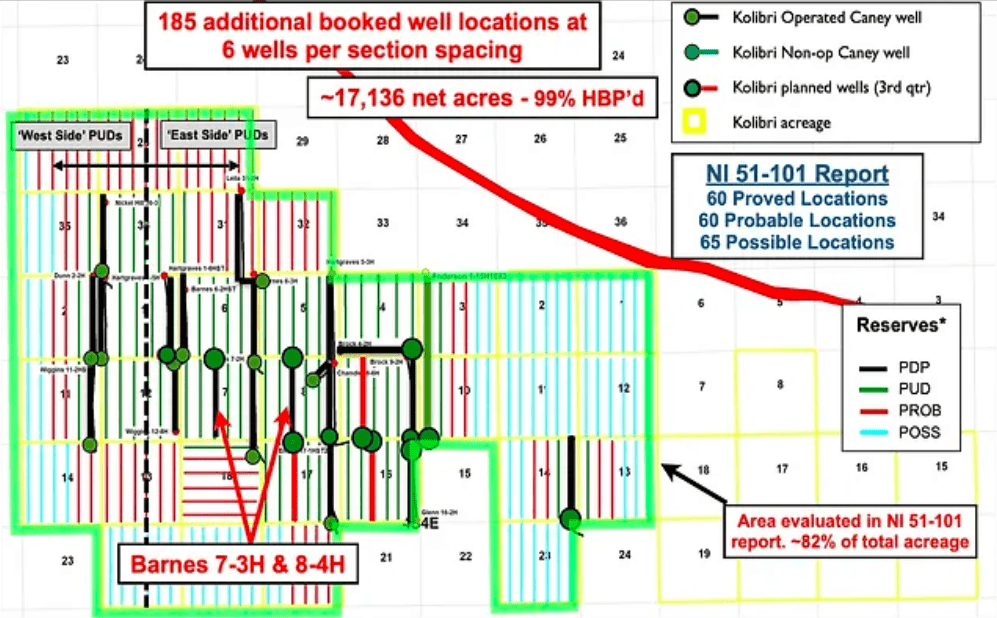

As of year-end 2021, Kolibri had 60 proved undeveloped locations (PUDs), shown as green lines on the land map below. Based on the outperformance of the five wells drilled this year vs. type curves, it is reasonable to assume that there will be a fairly significant increase in both proved developed producing and proved undeveloped reserves when the 2022 reserves report is released. As the 2022 program consisted of infill wells, the impact on proved reserves should be larger than the impact on probable reserves, as no step out drilling was conducted to further derisk probable and possible locations.

Kolibri Global Energy Website

Compelling Valuation

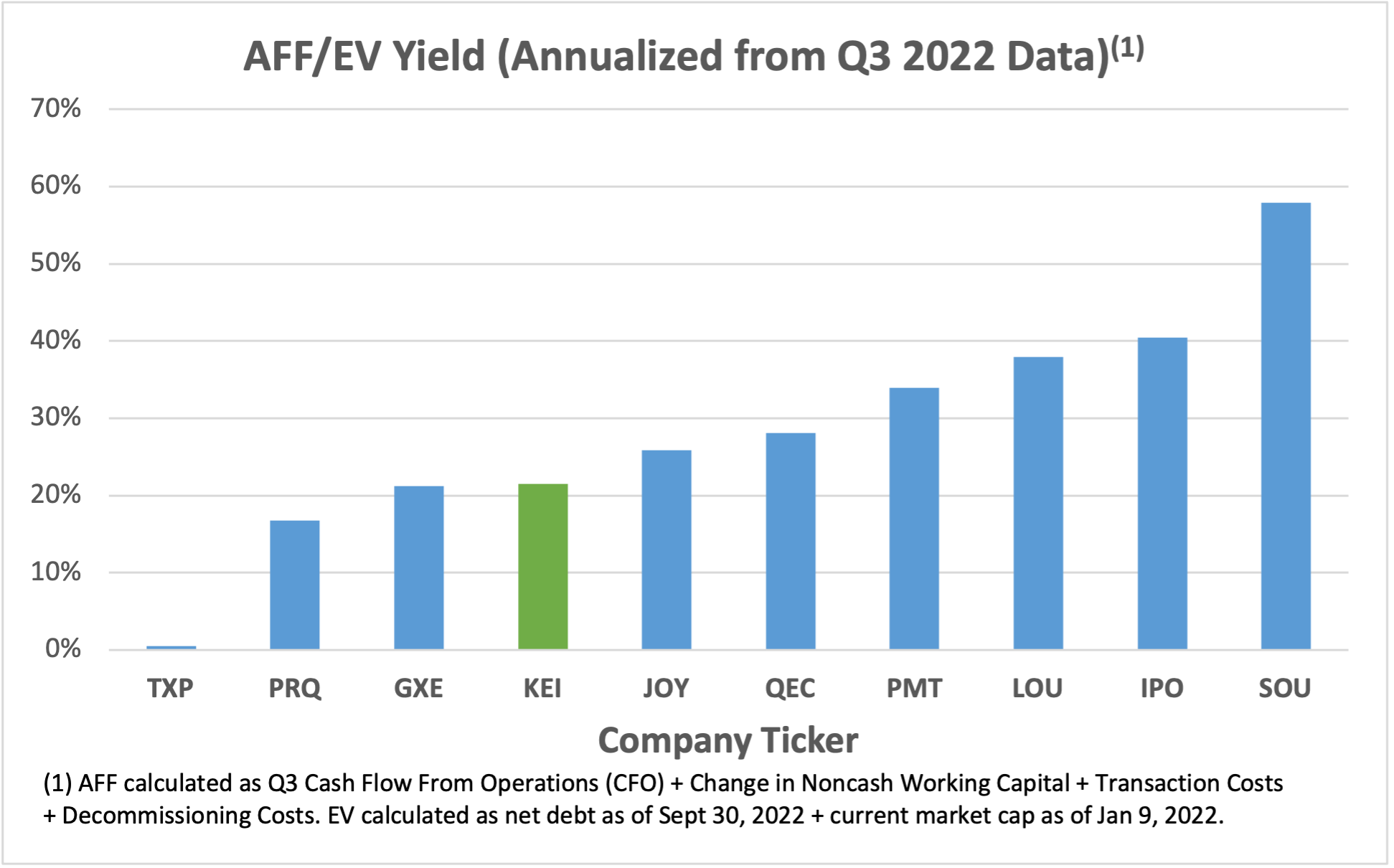

Kolibri is growing cash flows rapidly as they develop their proved reserves. Based on corporate guidance, the company is expected to grow adjusted funds flow (AFF) by 270% YoY, from C$8.9M in 2021 to C$32.5M in 2022. Due to this rapid growth in adjusted funds flow and early development of the field, Kolibri trades at a premium to most of its similar market cap Canadian traded peers on an AFF yield (annualized using Q3 2022 results) to enterprise value basis, with a yield of 22%. For example, other producers such as Lucero Energy (LOU:CA) (OTCQB:PSHIF) and Southern Energy (SOU:CA)(OTCQX:SOUTF) had much higher funds flow yields of 38% and 58%, respectively. With the three wells brought online in Q4, Kolibri should likely move closer to or exceed many of its comparable peers on this metric as cash flows increase.

Author using Q3 2022 financial statements and company presentations

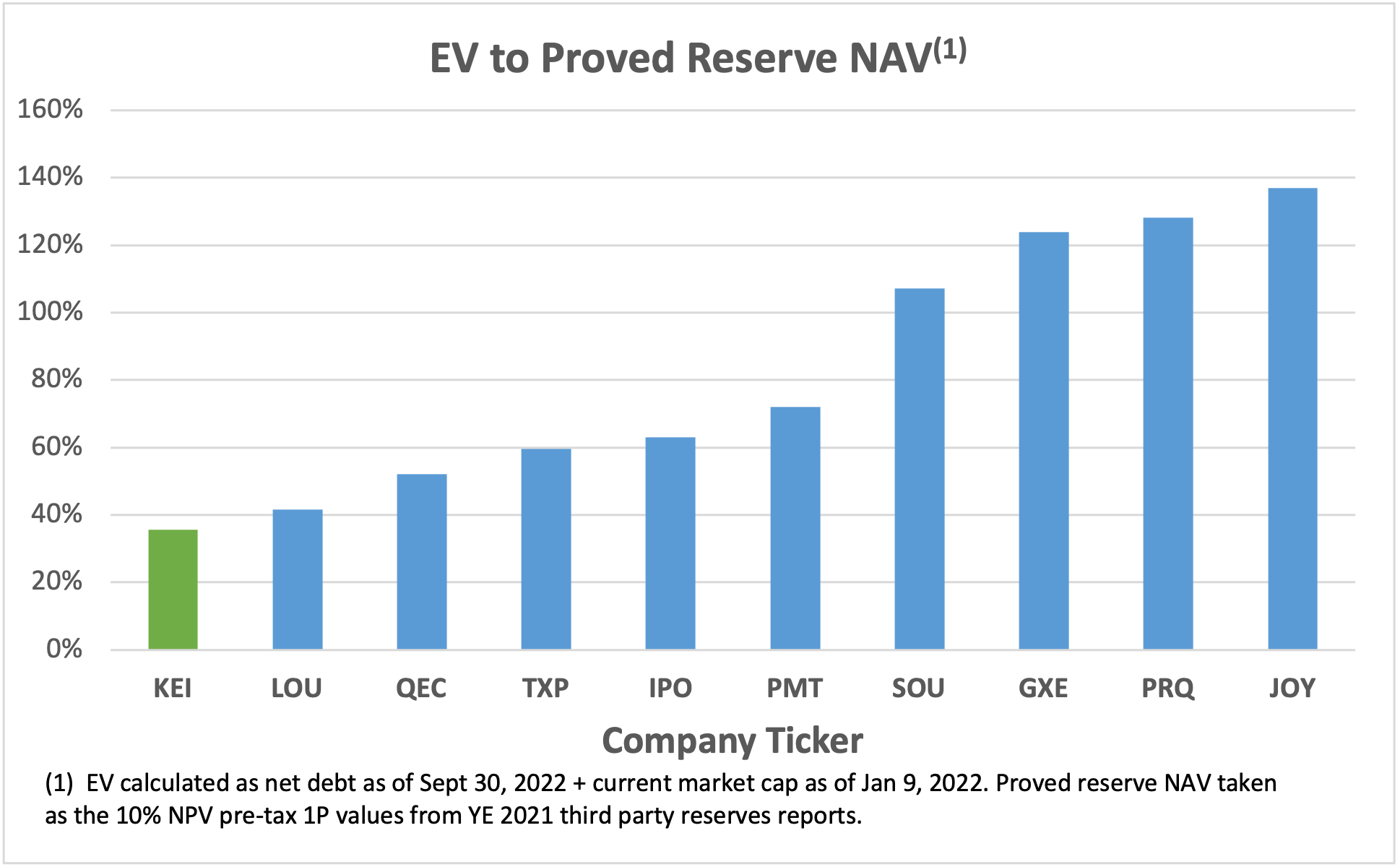

On a proved (1P) reserves basis, Kolibri is undervalued relative to its peers. Kolibri is currently trading with an enterprise value that is only 36% of its proved reserve valuation. A few of Kolibri’s peers, including Gear Energy (GXE:CA)(OTCQX:GENGF), are trading at over 100% on this metric.

Author using Q3 2022 financial statements and YE 2021 reserves reports

As of the YE 2021 reserves report, Kolibri had proved reserves of C$13.50/share. While they only had C$2.15/share of proved developed producing reserves at YE 2021, this number should increase substantially on the 2022 report with this year’s drilling results and associated increased production.

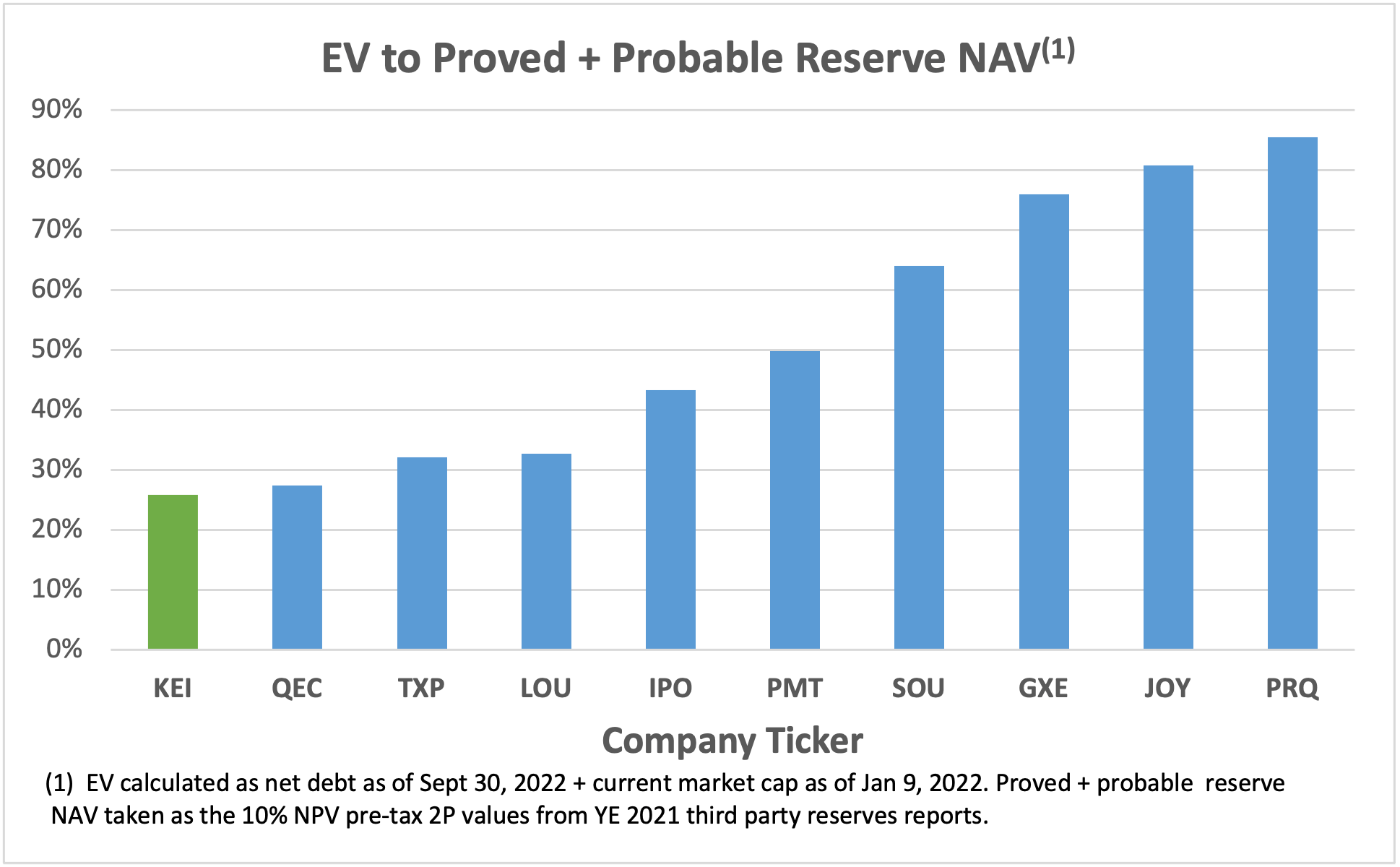

On a proved plus probable (2P) reserves basis, the company again trades favorably as compared to peers. In addition to the 60 proved undeveloped locations as of YE 2021, the company had 60 booked probable locations. As of YE 2021, Kolibri had proved plus probable reserves of C$18.51/share.

Author using Q3 2022 financial statements and YE 2021 reserves reports

Despite the increased pace of drilling in 2022, Kolibri is maintaining a healthy balance sheet. As of Q3 2022, the company had a debt to adjusted funds flow (annualized based on Q3 results) of 0.58 and a debt to equity ratio of 0.17. The company had C$21.3M in debt at the end of Q3. Kolibri currently has a credit facility in place with the Bank of Oklahoma, which was raised from $C26.8M to $C33.4M in October 2022. This will likely be increased further when the 2022 reserves report is released, which could allow for a larger drilling program in 2023.

Operating Efficiency

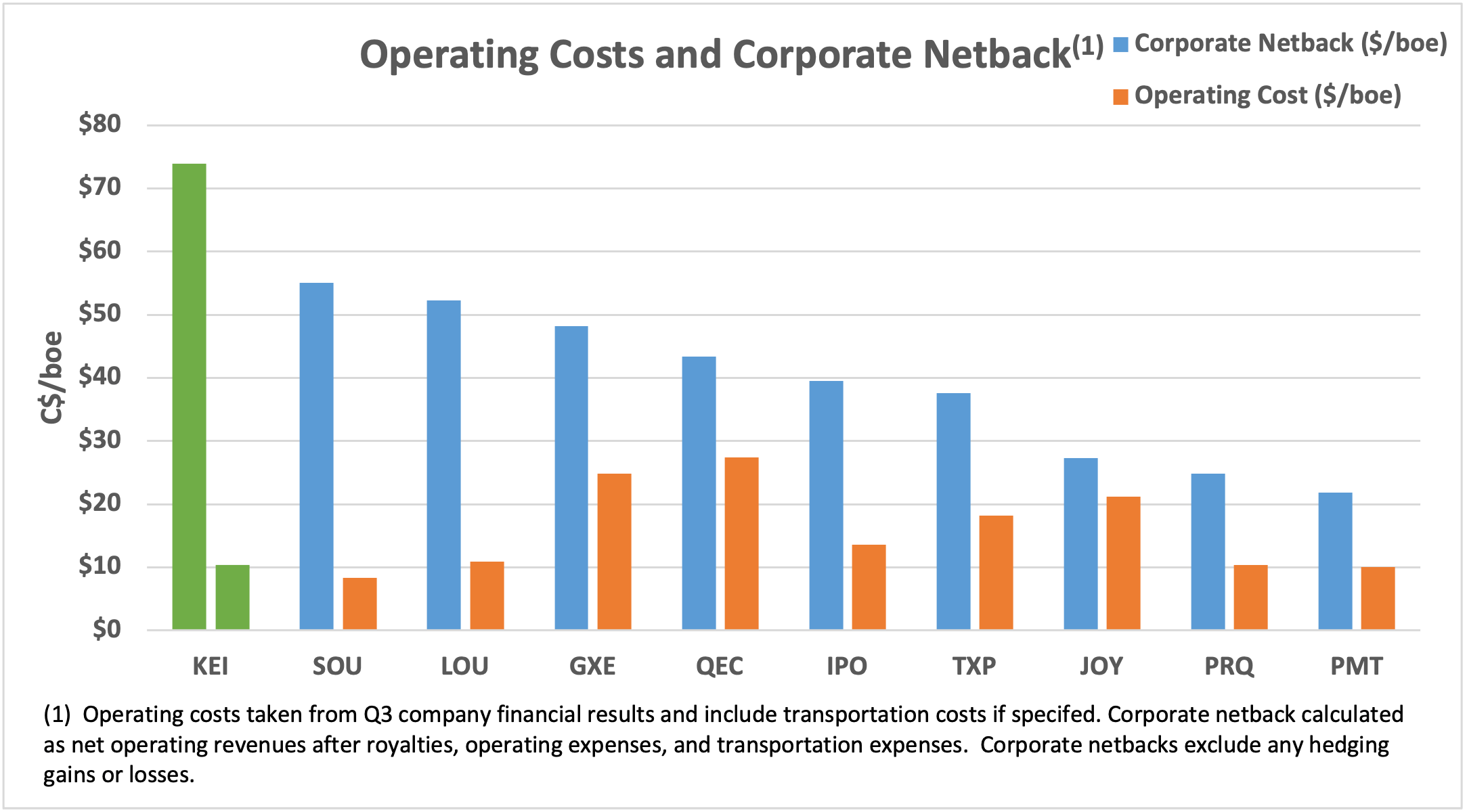

Kolibri operates in a fairly small area with a low well count, and as such is able to keep operating costs down. Gas volumes are pipelined to a nearby Exxon Mobil (XOM) gathering system and gas plant, and oil is trucked out. With manageable water cuts in the 10% range and nearby loading terminals, trucking and emulsion processing costs can be kept low. A low well count also means less costs on repairs and maintenance of surface equipment. As a result of this operating efficiency, Kolibri has lower operating costs and higher corporate netbacks as compared to peers, and as such can maintain profitability in a lower commodity price environment.

Author using Q3 2022 financial statements and company presentations

Risks

Like any other oil and gas company, there is the risk of commodity price fluctuations. In the case of a downturn in commodity prices, Kolibri has proven their ability to weather the storm as evidenced by their survival from 2019-21. Their low operating costs and high netbacks allow them to remain profitable in much lower commodity price environments.

As of Q3, the company had 530 bbl/d of hedges in place for Q1 2023, with further hedges for the remainder of 2023 and into 2024. These hedges are currently required as part of the credit facility agreement with the Bank of Oklahoma to help reduce risk.

Additionally, locations are currently booked at six horizontals per section of land. While the company has drilled a few wells this tightly in the past and management seems confident that this can be done successfully, there is a risk of communication between wells with the tight 250-300m spacing between horizontals. The recent change in completion design might help reduce the risk of communication by reducing fracture lengths.

Conclusion

Kolibri is poised to take advantage of a resource play with a ton of running room at current oil prices. Recently released drilling results should lead to upward revisions in proved reserves on the year-end reserves report, and it appears that completion designs have now been dialed in. As Kolibri continues to execute, the market might give more credit to current reserves in place.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment