Kevin Frayer

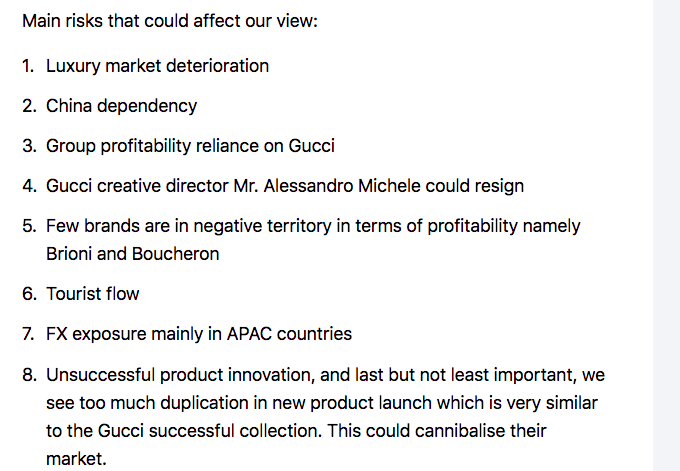

Here at the Lab, in 2022, we closely followed the Kering Group’s (OTCPK:PPRUF, OTCPK:PPRUY) story. Starting with our initiation of coverage called: Trading Multiple Too Low, and then moving on with the company’s quarterly release and capital market day analysis. Today, we would like to emphasize one of the risks previously quoted by our team: “Gucci creative director Mr. Alessandro Michele could resign“.

Mare Evidence Lab’s previous publication

Higher raw material costs and labor increases are hitting companies’ P&L. Thus, to survive, corporations need to pass inflationary pressure to consumers, hoping not to lose market share. Warren Buffett used to say: “If you’ve got the power to raise prices without losing business to a competitor, you’ve got a very good business”. Kering is our perfect match. We explained many times how the company is managing to increase prices, a move that could have disrupted sales with no change in volumes. High gross margins also provided the necessary foundation to implement innovations and invest in their brands so that they remain desirable over the long term.

Aside from the power to self-determine prices without losing market share, our supportive key takeaways were inorganic growth and middle-class potential. Starting with the latter, we should report an increase in the number of high-net-worth consumers buying expensive watches, designer clothes, and luxury handbags from Western brands. In addition, more important to note is the EU and US middle-class incremental expenditure in fashion. During the COVID-19 crisis, consumers used their budgets, which had actually been reserved for travel, to purchase in the domestic fashion market. The other important consideration is the fact that luxury fashion powerhouses have solid balance sheets. Kering is a company with low leverage, which protects them from rising debt costs or refinancing, which in turn gives them competitive advantages. For these reasons, many companies in our luxury sector are largely protected from inflation impact and we provided many buy rating targets (Richemont, Zegna, Moncler, and Capri Holding).

After Alessandro Michele, Sabato De Sarno will take Gucci’s creative lead, making his debut at the Milan fashion week in September 2023. In his new role, De Sarno, who for over 13 years has been in Valentino’s force alongside Pierpaolo Piccioli, will lead the design studio reporting to Marco Bizzarri, CEO and president of Gucci, following all product categories, womenswear, menswear, leather goods, accessories, and lifestyle.

Marco Bizzarri, President and CEO of Gucci, declared:

I am delighted that Sabato will join Gucci as the House’s new Creative Director, one of the most influential roles in the luxury industry. Having worked with a number of Italy’s most renowned luxury fashion houses, he brings with him vast and relevant experience. I am certain that through Sabato’s deep understanding and appreciation for Gucci’s unique legacy, he will lead our creative teams with a distinctive vision that will help write this exciting next chapter.”

Sabato De Sarno grew up in Naples. He began his career at Prada in 2005, then moved on to Dolce & Gabbana, before arriving at Valentino in 2009, where he held positions of increasing responsibility, up to his appointment as fashion director, with the task of supervising the men’s and women’s collections. His predecessor, Alessandro Michele completely reshaped Gucci, a brand with $10 billion in top-line sales that is generating more than 70% of Kerning’s profitability. He left last November after having led the brand for seven years.

Conclusion and Valuation

Here at the Lab, we believe that a radical change was needed to bring Gucci to the next growth phase. While investors are concerned about Mr. Michele’s replacement, on a twelve-month basis, we are confident in the Kering investment proposition. Despite a creative director change, as we always mentioned, Gucci is here to stay, and looking at the past year, the Italian brand had a difficult period and we believe that Kering current valuation adequately priced in the company’s near-term risk. Historically, the French luxury house has a better margin in H2 compared to the first half-year, and in 2022, the company delivered a plus 60 basis points in H1. Wall Street analysts are currently pricing a 37% margin for Gucci with a minus 100 basis points compared to H1. Overall, with positive data on tourism, and a stable trend in the EU coupled with the Christmas period, we are ahead of consensus estimates. With a reverse multiple analysis, if we priced in Kering ex-Gucci at 20x EBITDA with a discount to LVMH of more than 25%, the implied Gucci multiple on the EBITDA basis is just 3 times. This is too cheap to ignore – once again, we reiterate our buy rating on the company at €660 per share.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment