ADragan

Introduction

In December, I wrote an article focused on finding attractive housing-related investments in case 2023 would bring us more weakness. That article was based on rising rates and the need for the Fed to maintain its hawkish stance until inflation has eased substantially. The worst part (for the economy) is that this bear case is currently unfolding. In this article, we’ll discuss the latest earnings of major homebuilder KB Home (NYSE:KBH). This LA-based homebuilder reported horrible numbers, showing a sky-high cancellation rate, imploding new orders, and a somewhat grim outlook.

While there are some reasons to be bullish, I believe the best investments will be found the moment the Fed is forced to take its foot off the brake. At that point, KBH will turn into a long-term outperformer again.

Now, let’s dive into the details, starting with some fundamental background information.

Housing Market Woes

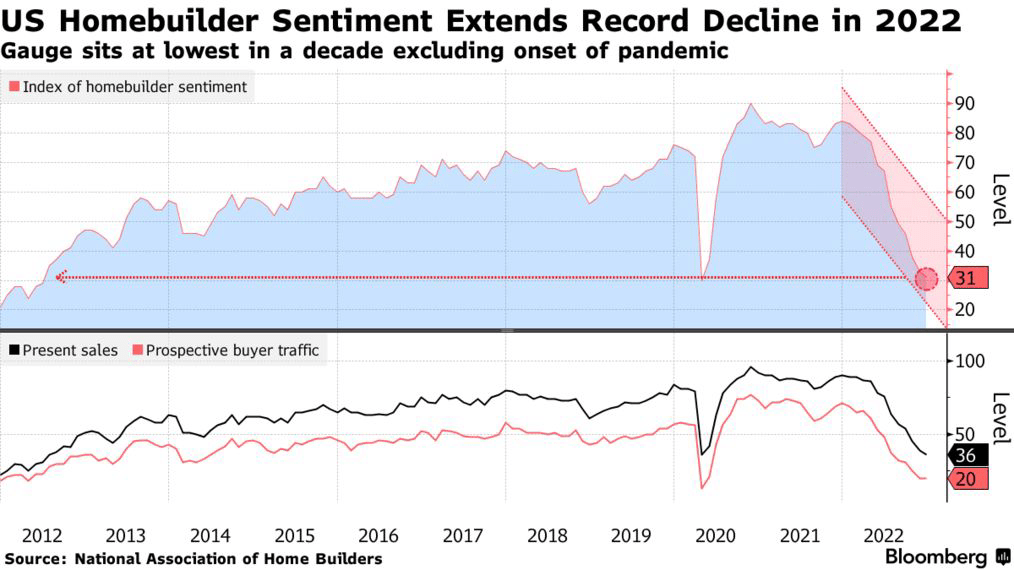

Homebuilders are not in a great position. Sentiment in the industry has been plummeting. Most recent numbers for December show a decline in the National Association of Home Builders (“NAHB”)/Wells Fargo sentiment index to 31. This is the lowest number since the housing market gained momentum in 2012. It’s also an uninterrupted slide, as every month of 2022 saw lower sentiment.

Bloomberg

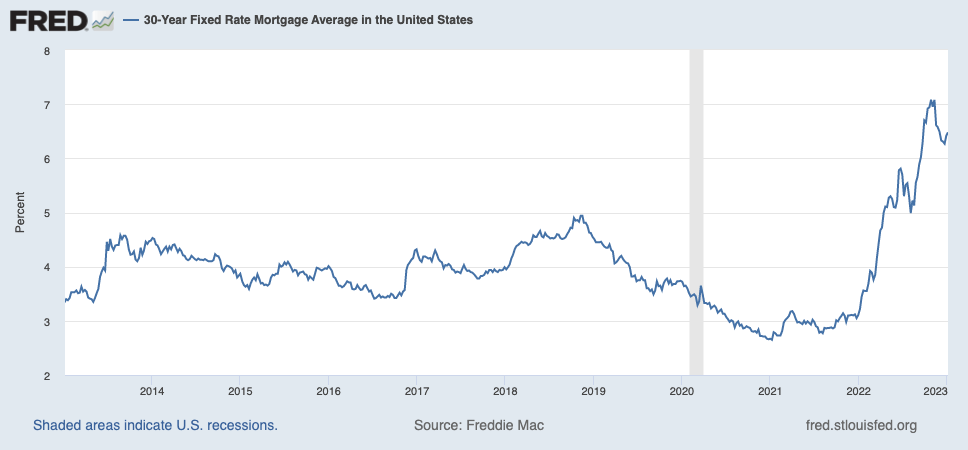

The problem is that high mortgage rates are hurting demand, while higher costs for materials and labor make it more expensive to work on existing backlog. Affordability issues are so bad that even structural housing shortages are not able to support demand anymore.

Federal Reserve Bank of St. Louis

According to Bloomberg, 62% of builders are using incentives like mortgage rate buy-downs and paying points to buyers to try to boost sales. Yet, it hasn’t worked – so far.

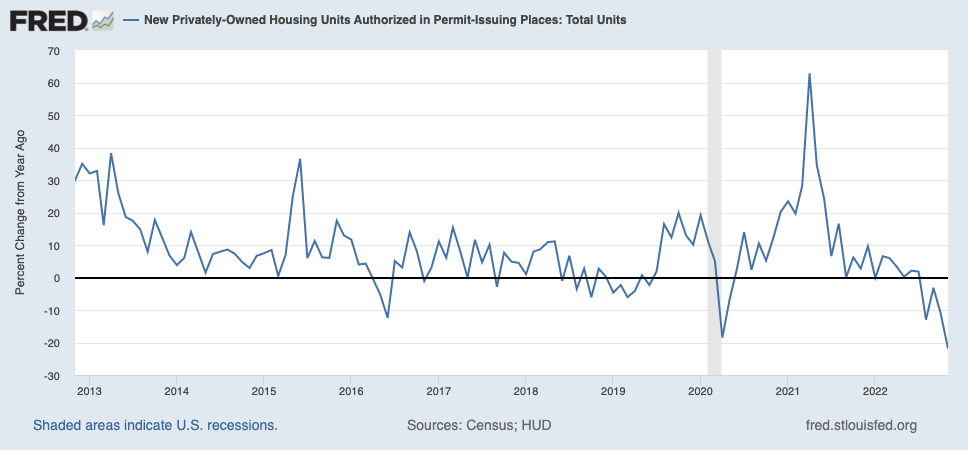

Building permits, which I use as a leading indicator for homebuilding new orders were down 21% in November, suggesting that demand is in an abysmal state. Contraction in permits is now as bad as it was during the first pandemic lockdown of 2020.

Federal Reserve Bank of St. Louis

Moreover, according to the NAHB:

“In this high inflation, high mortgage rate environment, builders are struggling to keep housing affordable for home buyers.”

[…] But with construction costs up more than 30% since inflation began to take off at the beginning of the year, there is little room for builders to cut prices. Only 35% of builders reduced homes prices in December, edging down from 36% in November. The average price reduction was 8%, up from 5% or 6% earlier in the year.”

Based on these numbers and comments, let us take a look at what KB Home did report, and what management has to tell us.

What’s KB Home?

But first, let us quickly discuss what we’re dealing with here. With a market cap of $3.1 billion, KBH is the 10th-largest stock-listed homebuilder in the United States. Headquartered in Los Angeles, the company maintains a built-to-order model, which efficiently uses lot spaces as it doesn’t build inventory without having the demand to back it up.

Moreover, the company focuses on median household incomes in each sub-market. 50% of its buyers are first-time buyers. 24% are first move-up buyers. In 2021, more than 60% were first-time buyers. I believe that the decline to 50% is caused by market fundamentals, which made housing unaffordable for starters with often limited budgets.

When it comes to regional exposure, the company generates 41% of its revenues on the West Coast, despite delivering just 29% of homes in that area. This is caused by a much higher average selling price of almost $740,000. The company also has Southwest, Central, and Southeast exposure, which somewhat lowers regional risks.

KB Home

Now, onto the numbers.

What To Make Of KB Home’s Earnings

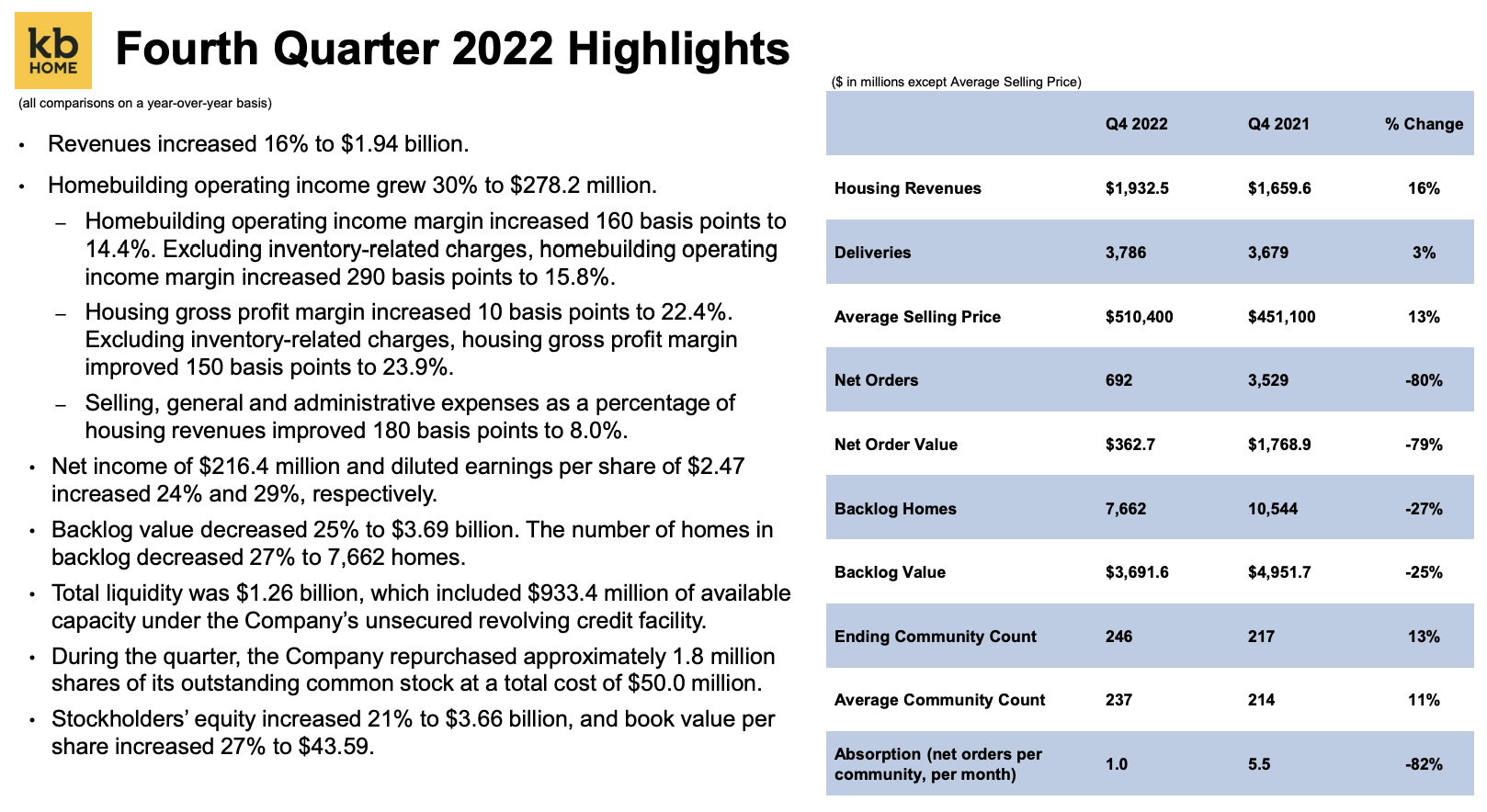

In 4Q22, the company did $2.47 in GAAP earnings per share. This missed estimates by $0.39. Total revenue came in at $1.94 billion, which is an improvement of 15.5% vs. 4Q21 and $40 million less than expected. The operating income margin came in at 15.8%, which is an improvement of 290 basis points, excluding inventory-related charges. Higher gross margins and lower SG&A costs allowed the company to improve its margins.

KB Home

Unfortunately, housing market weakness hit the company’s orders.

- 4Q22 new orders decline by 80% to a mere 692.

- The value of these orders fell by 79% as pricing benefits are eroding.

- The cancellation rate was 68% of gross orders.

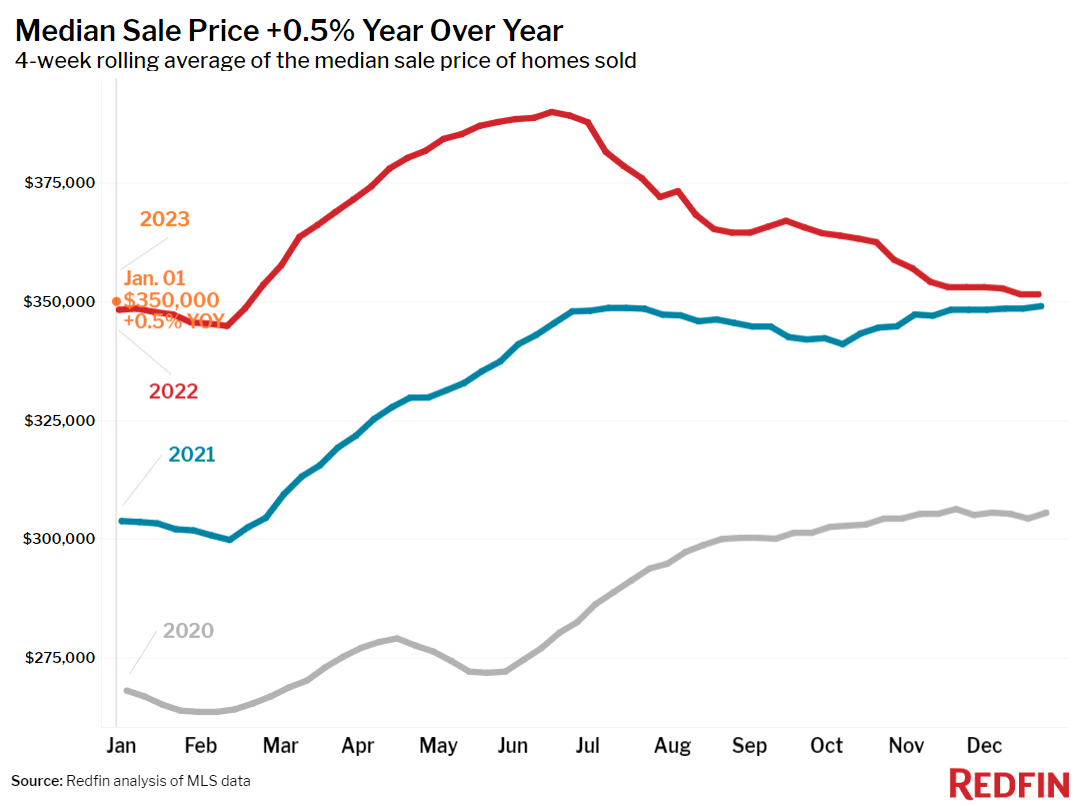

Pricing is best visualized using Redfin’s median four-week rolling home sales price. Prices are now just 0.5% higher on a year-on-year basis.

Redfin

The new order numbers are horrible. However, a few things need to be added. First of all, while there’s no denying that demand is weakening, it’s not as bad as these numbers suggest. The company had a high backlog of 50 homes per community. It decided to work on these with high margins instead of pursuing incremental sales in a softer demand quarter. Moreover, the company had only 210 finished homes available for sale at the start of the quarter. Prioritizing completions was more important than working on new orders in a soft market. The company believes it’s a disadvantage to build lower-priced homes in communities with a high backlog as it has a severely negative impact on the resell value of homes.

This is what the company said concerning the impact of higher rates on demand:

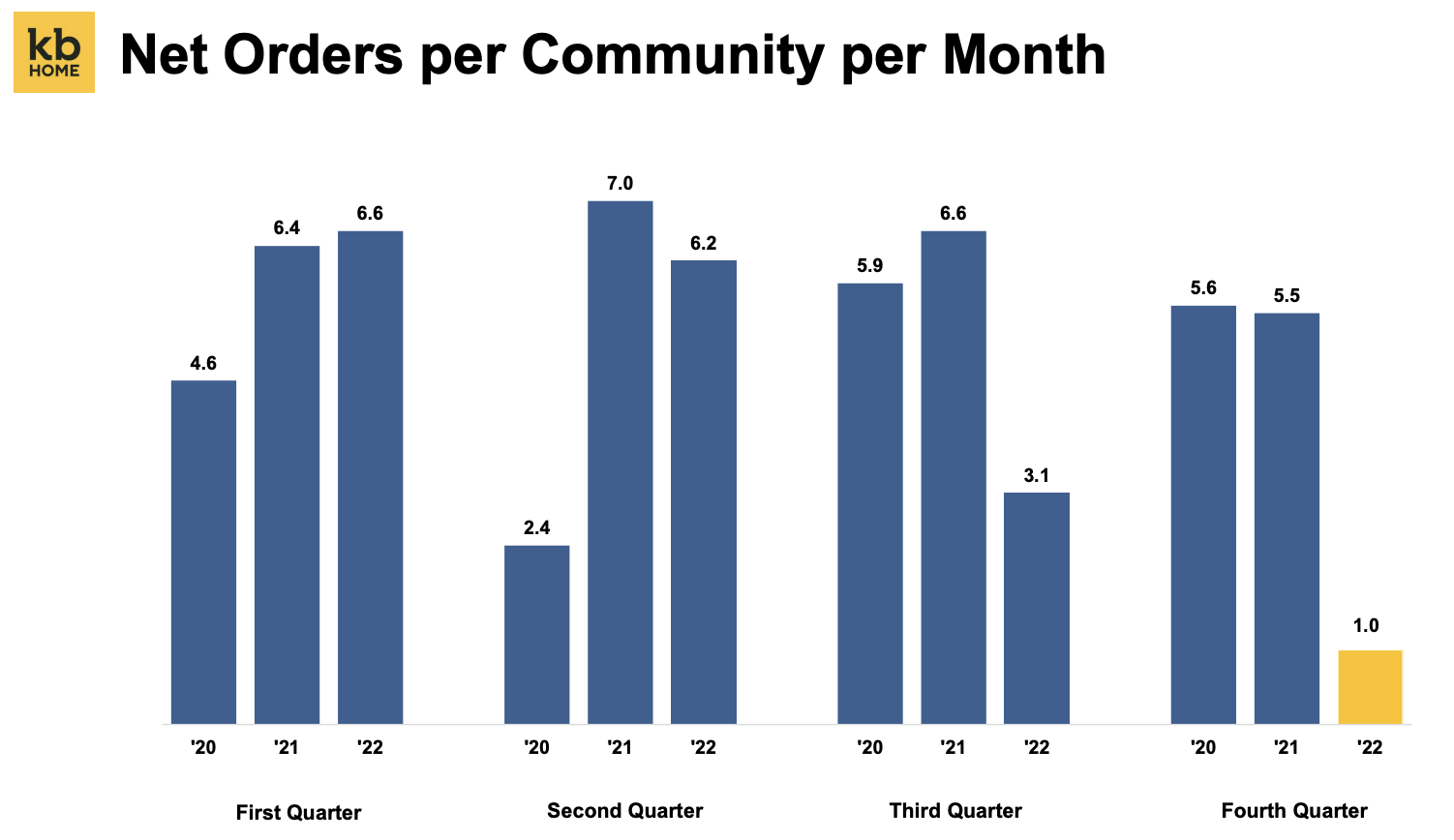

On our last earnings call in September, we shared that with the rise in interest rates to above 6%, we had seen a softening gross orders trend sequentially. As rates continued higher in October, hitting 7% late in the month, our orders declined further. Then, with rates moving slightly lower in November, gross orders stabilized roughly at October’s level. For the quarter, our gross orders were 2,169 a year-over-year decline of 47%. On a per-community basis, our gross absorption pace was 3.1 orders per month.

Net orders per community per month dropped to 1.0.

KB Home

The same goes for the cancellation rate. 68% is a devastating number and it was discussed a lot on social media. This cancellation rate was made much worse by the aforementioned decision to not focus on new orders. Due to a low number of gross new orders, a relatively “normal” number of cancellations amplified the cancellation rate.

This is what the company had to say:

“[…] due to the unusually low level of gross orders and our large beginning backlog, we believe looking at cancellations relative to backlog is a good way to understand the dynamics during the quarter. At 14%, our cancellation rate on the 10,756 homes we had in backlog at the start of the fourth quarter represented a sequential increase, although it was still slightly below our historical mid-teens average. The primary reason for cancellations continue to be buyers lack of confidence to move forward in these uncertain times […]”

In the first weeks of 2023 (the 1Q23 quarter), the company is dealing with a decline of 72% in net orders compared to the prior-year period. The target is to end up with 50% lower net orders on a full-quarter basis. In this case, the company is dealing with market weakness and a very tough comparison quarter. Overall new orders should come in close to 1,900 homes. That’s the midpoint of the company’s range.

The good news is that supply chain issues are fading. Overall build times have improved by 14 days vs. the third quarter. The company experienced a 21-day improvement from sale to frame. These times are expected to improve further as a result of a decline in overall housing starts.

Federal Reserve Bank of St. Louis

While issues persist, we could be looking at a normalization by the end of 2023, three years after the pandemic.

According to the company:

We are encouraged by the significant improvement in the front end of our build times and with industry starts lower into the new year, we believe we can gradually return to our historical build times. Each of our divisions has an action plan in place to significantly reduce build times by the end of 2023.

Other things worth mentioning include the fact that the average customer household had a $130,000 income and a FICO score of 734. This allowed 66% of KBH customers to qualify for conventional mortgages. The average cash down payment was 17%, which is roughly $87,000.

Moreover, on a full-year basis, the company invested $2.4 billion in land acquisition and returned $200 million to stockholders through buybacks and dividends. The company has 69,000 lots owned and controlled. That is a decline of 20% year-on-year as the company adjusted to lower demand (built-to-order).

KB Home

On a full-year basis, the company generated $2.6 billion in gross operating cash flow. When subtracting the aforementioned land acquisitions, the company ends up with $183 million in net operating cash flow.

Moreover, unlike during prior recessions, the company has a stellar balance sheet. The debt-to-capital ratio is at 33.4%. Total liquidity is $330 million based on cash alone. When adding available credit, the company has total liquidity of more than $1.2 billion.

KBH also is not subject to any major debt maturities until 2026.

Outlook and Stock Price Performance

It’s almost obvious, but KBH sees weakness on the horizon. The company anticipates challenging housing market conditions, which means it will focus on delivering its large backlog of sold homes and further improve supply chain issues.

For the quarter, we expect to generate housing revenues in a range of $1.25 billion to $1.4 billion. For the 2023 full year, we are forecasting housing revenues in a range of $5 billion to $6 billion, supported by our backlog and growing portfolio of open selling communities.

Due to these economic uncertainties, the company only provides revenue guidance.

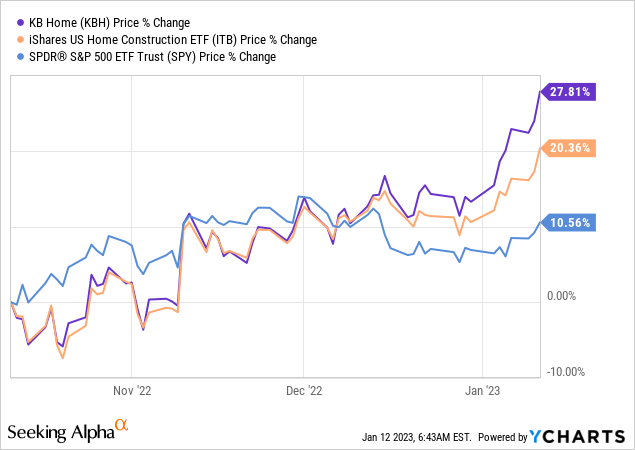

With all of this in mind, homebuilding stocks are doing quite well. While KBH is down 12.5% over the past 12 months, it is up 28% over the past three months.

What we’re dealing with here is peak negativity and investors rushing to buy into the bad news.

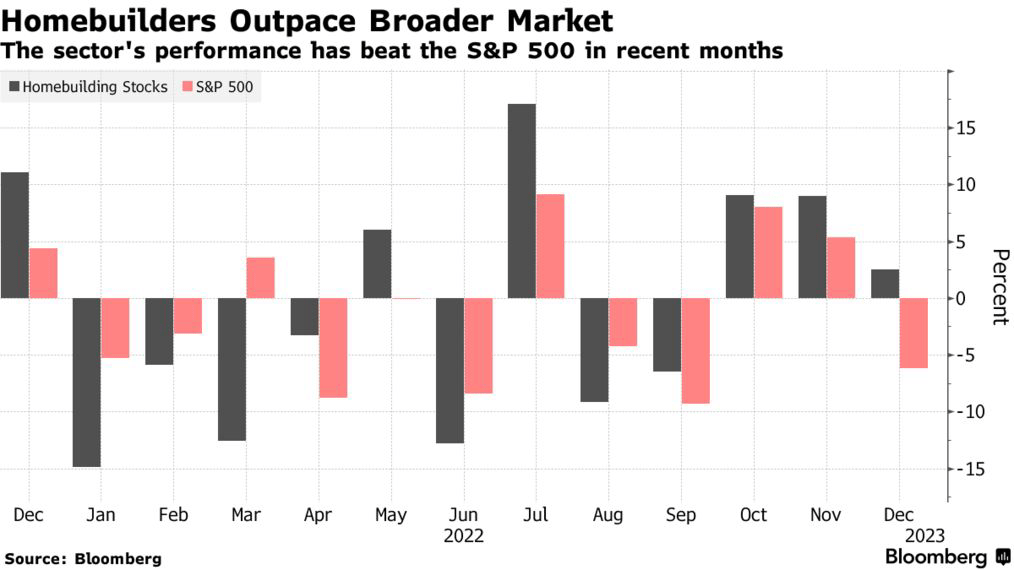

In December, Bloomberg reported that (top-ranked) homebuilding analyst Ken Zener has “never been more optimistic that homebuilders will outperform the market on a relative basis.”

Zener compared homebuilders to the broader market in recent decades. His grim outlook in January reflected how the stocks performed in Federal Reserve tightening periods, while his bullish pivot in September was due to the timing of the group’s stock performance relative to the S&P 500.

“Early pain” equals “early gain,” he wrote in his September note, highlighting that builders typically rebound ahead of the rest of the market.

[…] “Our positive sector call is not necessarily an absolute call on the stocks, but their relative performance to the S&P,” Zener said.

Bloomberg

It’s a smart call based on the fact that rates are falling after peaking last year. While this does not mean that homebuilders are out of the woods (he doesn’t make that call), it indicates that early buyers are returning.

This is confirmed by the stock price outperformance of the past three months and by KBH comments, as the company sees improving fundamentals as rates come down.

[…] cancellations declined in December and we anticipate a further moderation in January and February. A significantly higher percentage of our buyers are locked on their mortgage rates as compared to our 2022 third quarter. These buyers, together with our buyers who are paying in cash, which is also increased slightly sequentially, represent close to 80% of our backlog, giving us confidence in our ability to convert our backlog to closings.

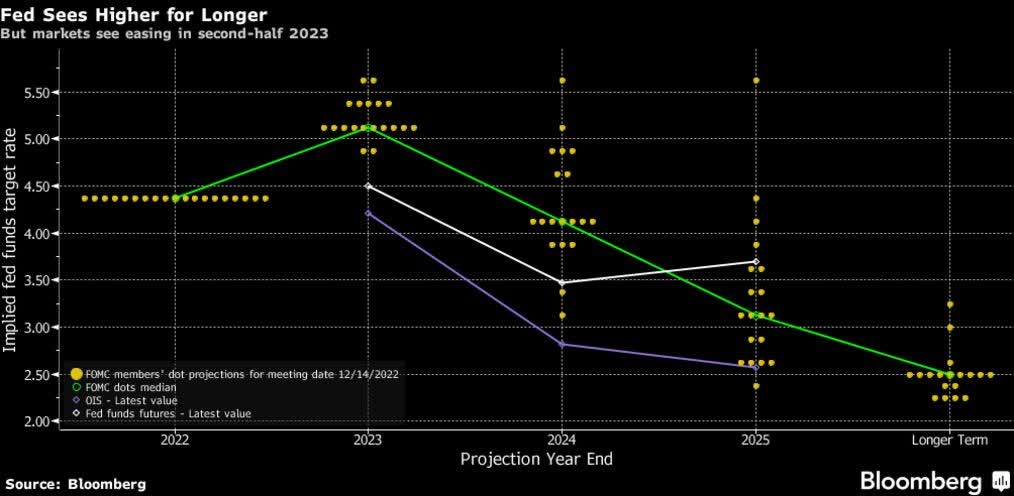

With that said, I’m sticking to my view that the pain might last for a while. After all, the Fed is not done hiking. The market has priced in a very dovish Fed as both fed funds futures and OIS rates predict that the Fed will significantly lower its own rate outlook. That’s one of the reasons why homebuilders have done rather well.

Bloomberg

However, this does not take into account that wage inflation remains persistent, as well as the fact that getting core inflation down is a tough task to achieve – let alone keeping inflation at 2% without risking new surges like the 1970s and 1980s.

Moreover, I still believe that demand will come back once unemployment has increased a lot. Major buyers have made clear that they are looking to re-enter the market when the Fed is forced to pivot due to weak economic fundamentals. At that point, (institutional) buyers benefit from lower rates and high unemployment, which makes it harder for the “masses” to compete with large buyers. I’m still convinced that such a scenario will mark the bottom for housing-related stocks.

It could look like this:

- High rates and economic weakness weaken the housing market.

- Eventually, unemployment comes down as these developments hurt the economy as a whole.

- The Fed will pivot as the economy has weakened along with inflation.

- Large players with cash reserves start buying, outbidding the average private buyer who suffers from a weak economy (high unemployment)

This also means that while KBH continues to be attractively valued, I’m not buying for the time being.

Takeaway

The headline numbers suggest that KBH had an abysmal quarter. The cancellation rate was high, new orders contracted by 80%, and the outlook wasn’t much better.

However, there’s some good news. New orders contraction was made worse due to the focus on backlog instead of providing pricing pressure in communities through the sale of new homes at lower prices. Adjusted for these developments, new orders contraction was less severe.

The company also is seeing improving supply chain headwinds and improving cancellation rates as interest rates have started to drop.

It also helps that KBH has a healthy balance sheet, no maturities until 2026, and buyers with healthy credit scores.

While I do not disagree that homebuilders deserved to outperform the market over the past three months, I’m not a buyer at these levels. I do not buy into the narrative that the Fed will quickly become dovish. Inflation is way too sticky, and Powell has made clear that more work needs to be done to fight i.e. wage inflation. The Fed is also keen to avoid what happened in the 1970s.

In other words, I stick to my outlook that we won’t see a major buyable bottom until unemployment has come up, which will eventually force the Fed to pivot. At that point, I’m looking to deploy a lot of my current cash reserves to buy housing-related stocks.

(Dis)agree? Let me know in the comments!

Be the first to comment