choochart choochaikupt

Introduction

Shares of Kandi Technologies (NASDAQ:KNDI) have risen +12% YTD. The company continues to show revenue growth to the market due to strong demand in the off-road vehicles category. In addition, increasing economies of scale, reducing R&D costs and optimizing costs allow the company to step by step increase operational efficiency and reduce losses. In my personal opinion, continued growth in revenue in existing markets, as well as the launch of new models and entry into new markets, can support the company’s shares in the future.

3Q overview

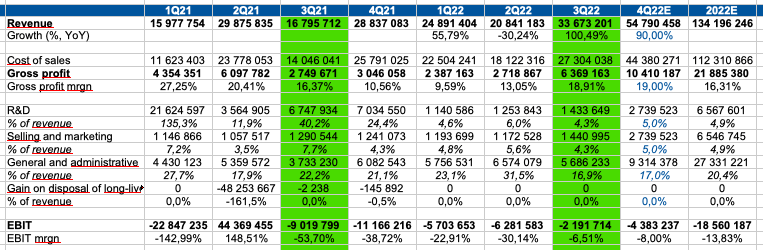

On November 8, the company released Q3 2022 results, which came in better than investors had expected. I’d like to take a closer look at the results and share my own observations based on the company’s financials and my personal assumptions about the future cash flows of the business. At the end of the 3rd quarter of 2022, the company showed revenue growth of more than 100% despite COVID in China, as well as the growth of macro and geopolitical tensions. Revenue in the US market grew by 190%, while revenue in the Chinese market grew by 36%.

Company’s information

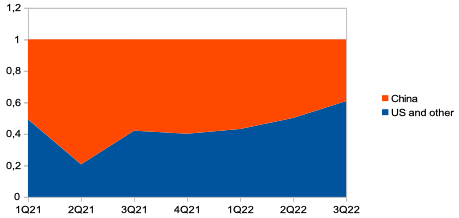

The share of the company’s revenue which falls under the USA continued to increase and reached 60.8%. I like that the company is able to create a competitive product and increase its own presence in the US market, thereby diversifying geographic risks. You can see the details in the charts below.

Company’s information Company’s information

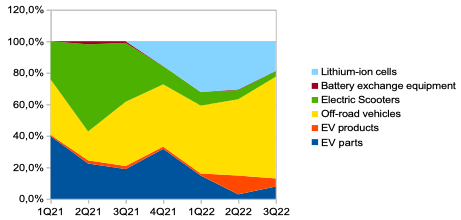

The off-road vehicles segment continues to be the main driver of revenue growth. The segment share continues to increase from 35.2% in Q1 2021 to 64.6% in Q3 2022. The share of segments such as EV parts and EV products continues to decline due to pressure on EV demand in China. According to management comments, the company will have a small presence in the EV segment. You can see the details of revenue by segments in the charts below.

Company’s information Company’s information

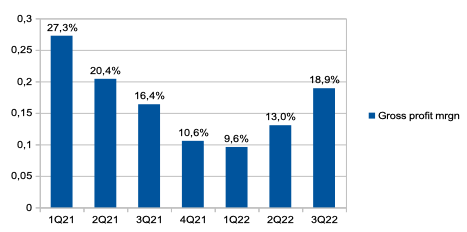

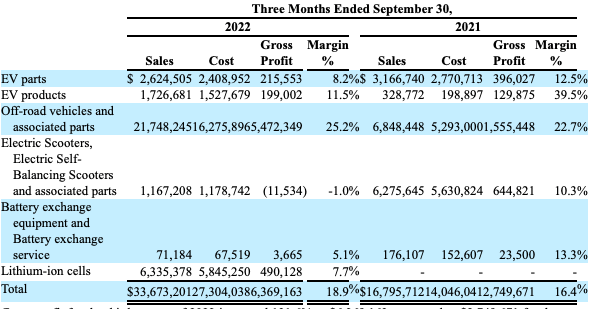

The growth in sales in the USA and China markets and the change in the product mix, where the share of the off-road vehicle segment is increasing, contributes to restoring the company’s gross margin. Gross margin in the off-road vehicle segment at the end of Q3 2022 was 25.2%, which is significantly higher than the gross margin in such segments as: EV parts, EV products and so on. You can see the details in the charts below.

Company’s information Company’s information

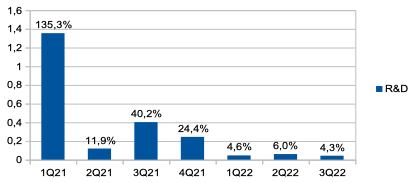

In addition, the company continues to cut R&D costs. Thus, the share of spending on R&D (% of revenue) decreased from 40.2% in Q3 2021 to 4.3% in Q3 2022. On the one hand, such a reduction in R&D costs for a company that operates in a technologically advanced and emerging market should cause investor concern, because this may lead to a loss of competitive advantage and delays in the launch of new models. On the other hand, based on management’s comments, cost cuts indicate that the company has already built a product and plans to scale up existing models. You can see the details in the chart below.

Company’s information

The company’s balance sheet continues to look strong. Cash on the balance sheet is $99 million, while long term loans are $2.2 million, and short term loans are $5.6 million. Thus, the company has negative net debt. In my opinion, a strong balance sheet positively distinguishes the company from the background of many competitors, as the company is able to continue development at its own expense. Moreover, a strong balance sheet is a competitive advantage in the face of monetary tightening and rising interest rates.

Projections & valuation

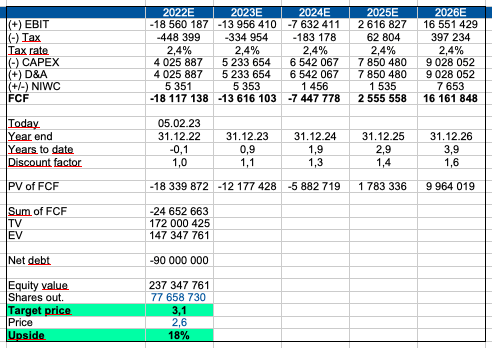

I decided to make my own assumptions about the company’s future cash flows and evaluate the company based on a fundamental approach. To value a company, I use the DCF method and calculate current and target multiples based on a fair price. I understand that the DCF approach is not absolutely correct for valuing such a company, however, this approach allows you to take into account revenue growth, economies of scale and increases in operational efficiency.

Assumptions:

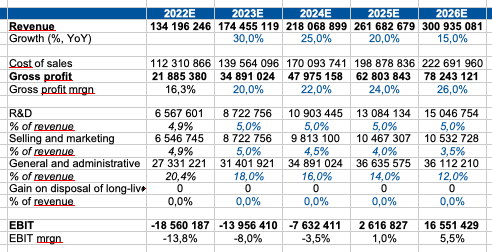

Revenue growth: I believe that the company will continue to increase sales through existing models and through the launch of new ones. I expect revenue to continue to grow by 90% in 4Q 2022, then by 30% in 2023 and decline to 15% by 2026 on the back of the high base effect of previous years.

Gross margin: in my opinion, the economies of scale will contribute to the growth of the company’s gross margin in the following periods. So, I predict an increase in gross margin from 19% in Q4 2022 to 26% in 2026.

R&D: I project R&D spending at a steady 5% through 2026 based on management comments and personal assumptions.

Selling and marketing: I predict an increase in efficiency and a decrease in costs (% of revenue) from 5% in 2023 to 3.5% in 2026.

Quarterly projections:

Personal calculations

Yearly projections:

Personal calculations

The main assumptions of my model are:

WACC: 13.2%

Terminal growth rate: 7%

Personal calculations

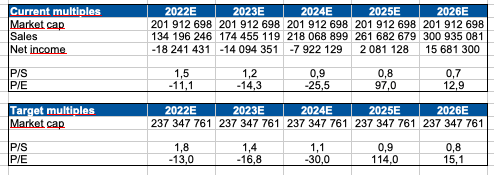

Multiples

On the chart below you can see the calculation of P/S and P/E multiples based on my forecasts.

Personal calculations

Drivers

Revenue: the company’s entry into new markets and growth in sales in the US and China markets are driven by the goal of generating revenue.

Launch of new models: production and sales of new models, such as gold crossovers and utility terrain vehicles, could also drive revenue growth in the coming quarters.

Margin: increasing economies of scale due to the increase in production volumes, discipline and tight control of production and operating costs can support operating margins in the following periods, which could potentially lead to a revaluation of the company’s shares.

Risks

Competition: increased competition in the EV market could lead to a decrease in the company’s market share, an increase in marketing and production costs, which could have a negative effect on revenue and profitability dynamics.

COVID: the resurgence of COVID in China could lead to a halt or slowdown in production, which could have a negative impact on the company’s sales, as the company’s manufacturing facilities are located in China.

Margin: rising inflation and high commodity prices could drive up operating costs and reduce financial efficiency.

Operating risks: decreased R&D costs and the elimination of tax benefits in China could lead to some difficulties in launching new models and lower profitability. In addition, shortages of components and supply chain risks can also have a negative impact on business operations.

Macro: growing macro and geopolitical tensions, declining real incomes and declining consumer confidence could lead to lower consumer spending in the discretionary segment, which is negative for business revenue.

Conclusion

The company continues to increase sales in its main sales markets, and the increase in the share of efficient segments such as off-road vehicles continues to make a positive contribution to the dynamics of business profitability. In addition, in my personal opinion, the growth of economies of scale will further increase the gross margin and reduce operating costs. Moreover, the company’s balance sheet continues to look strong, which is especially true in difficult macro-economic conditions. I believe the Q4 2022 report could be a catalyst for the stock price. Thus, in my personal estimation, the company’s fair share price is $3.1 with an upside potential of 18%.

Be the first to comment