HT Ganzo

Kaiser Aluminum (NASDAQ:KALU) is better-positioned among the secular-driven verticals, with underling long-standing customer relationships to drive future growth. The Warrick facility acquisition proved game-changing, as the deal allocated the company to more resilient flat-rolled aluminum demand by the packaging industry. Although KALU stock is trading at a considerable premium to the main competitors, I believe the major part of it is justified by a long journey of sustainable cash flow distributions to investors. I gave Kaiser Aluminum a Hold rating, mainly as a result of a favorable outlook and strong management commitment to returning cash flows to investors.

Financial results

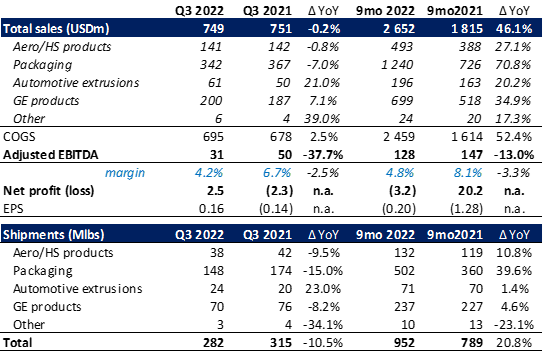

Kaiser Aluminum has managed to keep Q3 2022 total sales in the amount of $749 million on the level with the year-ago quarter. The flattish quarterly performance was due to a 12% increase in average selling price and some operational issues and outages, which resulted in a 10.5% YoY decrease in shipments.

Q3 2022 financial results and shipments (company reports)

Segment-wise, revenue in Automotive extrusions division grew by 21% YoY ($61 million) thanks to 23% YoY higher shipments and favorable pricing and mix. The General engineering segment was up by 7.1% YoY ($200 million) due to the strong demand underlying price increase, while despite lower shipments (-8.2% YoY). On the downside, the Packaging business line registered a 7% YoY decrease in sales ($342 million) as a result of a 15% decline in shipments impacted by operational challenges at the Warrick facility related to the magnesium and metal supply issue. Revenue from Aerospace/High strength was impacted by a planned outage at the company’s Trentwood facility, which resulted in 9.5% lower shipments, while a strong product mix of higher value-added products limited the decrease in sales to 0.8% YoY ($141 million).

Adjusted EBITDA for the quarter came to $32 million, down 37.7% YoY, while net profit amounted to $3 million, or $0.16 per share, compared to a net loss of $0.14 per share a year ago.

Outlook

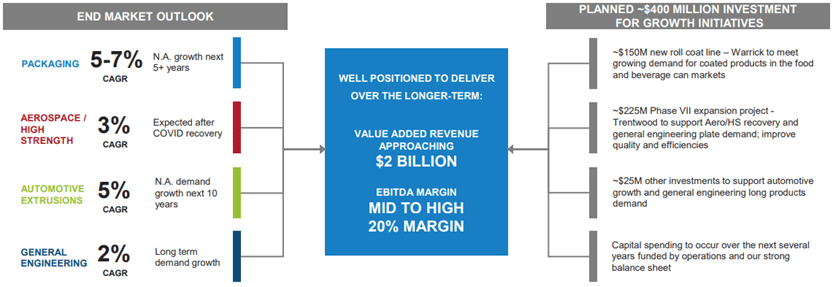

KALU is well positioned to benefit from growing demand for aluminum, underpinned by secular trends in the company’s each business line. With the packaging in the forefront, I expect Kaiser Aluminum to deliver sustainable profitability, due to the stable and recession-resilient profile of the end-market, and the underlying secular shift from plastic to aluminum.

The next solid demand driver for aluminum is associated with lightweighting megatrend in the automotive and aerospace industries. Kaiser has a solid position in applications that require high strength. High-strength aluminum alloys, which are capable of creating complex extrusions, would be highly regarded by manufacturers, struggling to bring the weight figures down.

Demand drivers and planned investments (company presentation)

In order to meet the secular tailwinds in strategic verticals, Kaiser Aluminum plans to allocate $400 million for capacity expansion. The largest pile would be destined for the Trentwood expansion project, followed by a new roll coal line in Warrick facility to match the growing demand for coated products in the packaging market.

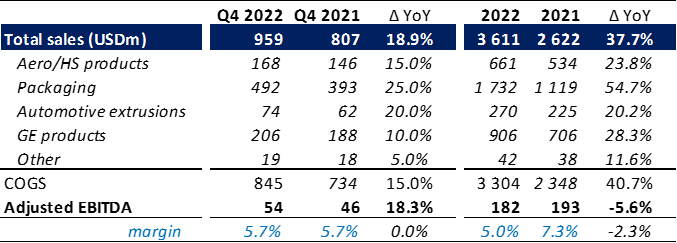

Q4 and 2022 full year forecasts (company reports, author’s estimates)

For 2022, I expect KALY to reach $3.6 billion in total sales and mark 37.7% growth. All business divisions should contribute strongly, where the Packaging segment is forecasted to mark a 54.7% surge, reflecting full year Warrick operations and production capacity problems settling. Aero/HS products should register 23.8% YoY following the resolution of the Trentwood outage. I also assume Automotive extrusions and GE products will register 20.2% and 28.3% growth. With the above expectations, I estimate full year EBITDA to stand at $182 million, where outperforming COGS growth should tapper off the EBITDA margin by 230 bps to 5%.

Looking forward, with the main focus on the packaging end-market, the prospects for Kaiser Aluminum are improving, where multi-year contracts in place should support solid long-term growth, favorable mix and margin improvement. The future growth will be underpinned by commercial aerospace recovery and demand for defense applications. Additionally, EV production expansion will further ensure aluminum application growth, while re-shoring will drive the domestic demand and minimize the risk of supply chain disruption. Overall, with long standing customer relationships, Kaiser Aluminum should continue to be well positioned to drive future growth.

Valuation

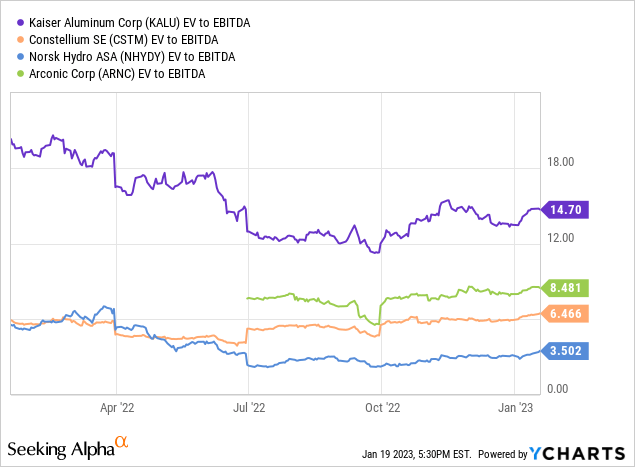

With the current Mcap of Kaiser Aluminum of $1.4 billion, $129 million cash position and $1 billion in LT debt, EV is $2.3 billion. Compared to the main competitors in the face of Arconic (ARNC), Constellium (CSTM) and Norsk Hydro (OTCQX:NHYDY), the company is trading at a much higher EBITDA multiple.

Applying my estimate of $182 million EBITDA for 2022, the company is trading at a forward EV/EBITDA multiple of 12.5x. According to the Seeking Alpha data, the median forward EV/EBITDA for the sector stands at 7.55x. This means that KALU is trading at a significant premium of around 65%.

With such a high premium to the sector’s median, one might argue that the stock is up for Sell recommendation. However, I rated KALU with a Hold rating, as in my view, the following graphs justify a large share of that premium.

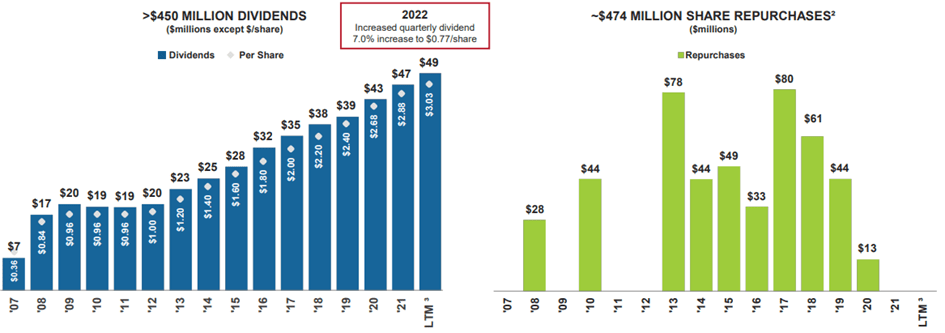

Dividend and buy-back history (company presentation)

Kaiser Aluminum has a strong, 16-year-long track record of either maintaining or raising its dividend payout through different economic environments. This gives a reasonable assurance for the dividend policy to take hold going forward as well. In terms of competition, Hydro can’t boast likewise consistency, while Arconic and Constellium are out of the chat when it comes to the dividend distribution. Additionally, the strong share buy-back procedures in the past resulted in persistent upside pressure on the stock price.

Risk factors

Significant increase in leverage could pose a risk on continuation of the divided distribution. At least it could spoil the sustainable uptrend of the company’s DPS amounts. On LTM basis, net debt was 5.3x to EBITDA, however, the management remains committed to de-leveraging activities in order to reduce the ration down to 2.0x.

Be the first to comment