JayLazarin

JPMorgan Chase (NYSE:JPM) has done rather well since I last visited it in July. At the time, the stock had fallen out of favor with the market, trading at just $113. However, beauty is in the eye of the beholder, and it appears that my buy rating has done well, with the stock giving investors a 19% total return since then, performing far better than the 1% decline in the S&P 500 (SPY) over the same timeframe. With the stock still trading well off its 52-week high of $170, I highlight why JPM still has plenty to offer at current levels.

Why JPM?

JPMorgan Chase is one of the largest and most influential financial institutions, with a history dating back over two centuries. The company is a global leader in investment banking, financial services for consumers and small businesses, commercial banking, financial transaction processing, and asset management.

What differentiates JPM from the likes of Goldman Sachs (GS) and Morgan Stanley (MS) is its multi-cylinder business approach that’s not overly reliant on deal-making, transactions, and IPOs. This has worked out well for JPM, especially over the last year, as M&A and IPO activity has substantially declined due primarily to higher interest rates and economic uncertainty. JPM’s multifaceted strengths were highlighted by Morningstar in its recent analyst report:

JPMorgan now benefits from an unrivaled combination of scale and scope within the United States. The company has become the largest bank in the country. Within payments, depending on the metric, JPMorgan is generally the largest credit card issuer in the U.S. and roughly tied as the largest U.S. merchant acquirer.

The company’s investment bank is the leading global generator of fees, and JPMorgan’s FICC trading desk remains one of the top global players. The bank also has a national commercial banking platform and its own asset and wealth management operations.

This differentiator is reflected by JPM’s solid performance amidst a tough macroeconomic backdrop with revenue growing by 10% YoY during the third quarter. This was driven by higher interest rates, resulting in strong net interest income of $17.5 billion. Notably, management has guided for even higher NII of $19 billion for the fourth quarter, and JPM is generating solid return on tangible common equity of 18%, helping it to earn an A+ profitability rating in comparison to peers.

Importantly, JPM maintains an A- credit rating from S&P and carries a common equity tier 1 ratio of 12.5% as of the last reported quarter, up 30 basis points sequentially. This sits well above the 4.5% requirement by the Federal Reserve for large banks. It’s worth noting that management is targeting an even stronger CET1 ratio of 13% for the first quarter of 2023.

The strong operating fundamentals and balance sheet lends support to JPM’s 3% dividend yield, which is well-supported by a 34% payout ratio. The dividend also comes with 8 years of consecutive annual growth and an impressive 5-year CAGR of 14.4%. While JPM has kept the dividend the same for the past six quarters, I would expect to see a rise should recessionary concerns ease and a clearer direction from the Federal Reserve.

Risks to JPM include potential for higher loan losses due to a recession. However, management expressed the bank’s preparedness to add $5 to $6 billion to its CECL should the unemployment rate go to 5% to 6%, and that this would be easy to handle. This makes sense, as the additional reserve would just be a fraction of JPM’s quarterly NII.

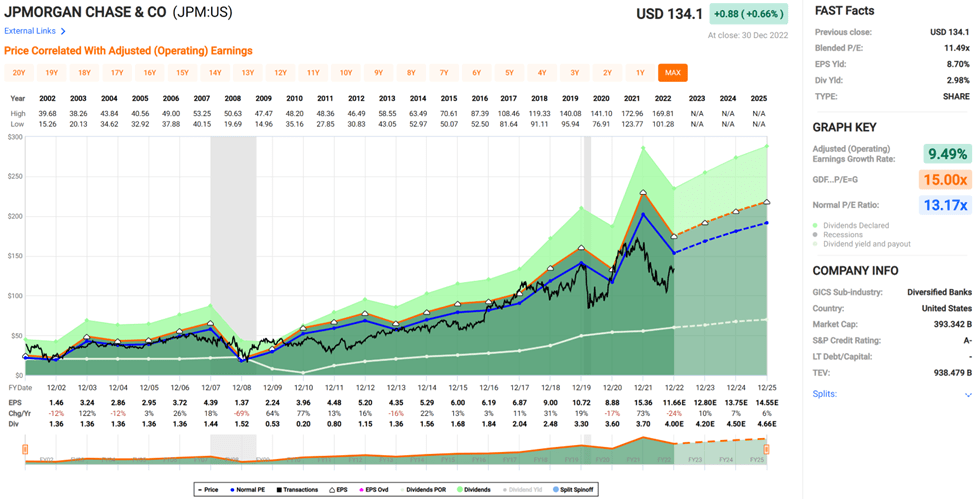

Lastly, a big part of whether a stock is a buy its valuation. At the current price of $134, JPM trades at a forward PE of just 11.6, sitting well below its normal PE of 13.2. I find the current valuation to be attractive, especially considering that analysts expect 9% EPS growth in 2023. Analysts also have a consensus Buy rating, with an average price target of $143.

JPM Valuation (FAST Graphs)

Investor Takeaway

JPM looks attractive at current levels, with the stock trading more than 20% below its 52-week high. Moreover, it has strong fundamentals and balance sheet, which should help it weather potential macroeconomic headwinds. With a well-covered dividend yield, track record of growth, and low valuation, JPM could give investors potentially strong long-term returns from present levels.

Be the first to comment