When we last covered JPMorgan Chase & Co. (JPM) we gave it a neutral rating despite the stock having declined a good deal. As with our earlier coverage, we were less than impressed with the valuation metrics that matter to us and those were not the highly volatile earnings. Specifically we said,

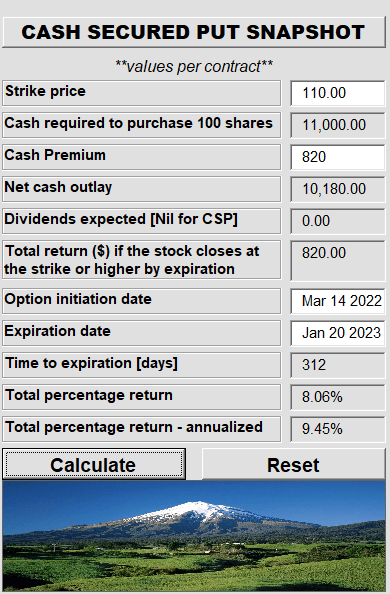

In an ideal world we would like to pick this up at 1.6X tangible book value. Of course that is a good deal lower. So what can an investor do? Well, if you are committed to buy at a good price, one can consider the cash secured puts for the price that is attractive. In this case we think the $110 strikes look particularly attractive. The January 2023 strikes at $8.20 offer an interesting risk-reward for the conservative income investor.

How did the defensive strategy do? Well for one, it dodged the decline in the stock.

Seeking Alpha

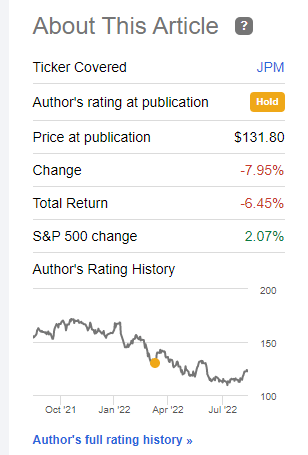

Keep in mind that the 52 week low was $106.09 so a buy would have taken a 20% drawdown in 3 months. The icing on that was the actual trade we suggested in lieu of a long position. Jan $110 puts are trading for $4.25. So going that route would have made you money instead of losing 6%.

Seeking Alpha

We look at how we can continue to look for responsible trades in this stock without breaking the bank.

Q2-2022

JPM missed the Q2-2022 estimates with a rather large revenue miss. EPS did not fare much better and came in 13 cents below estimates. It is a general policy for companies to guide analysts estimates down to the point that everyone can collectively celebrate a “beat”. Of course if the deterioration happens late in the quarter and rather briskly, we get something like this. The first lesson here that the “low P/E” crowd of 2021 got was that extrapolating 1 year of earnings into infinity is a bad idea.

JPM Q2-2022

Financials in general and banks in particular always look cheap at the top of the cycle. That is why we got so much push back when we called JPM expensive at $141.

JPM’s earning contraction was driven by rising non-interest expenses (up 6% year over year) and a big reversal in the provision for credit losses. Q2-2022 was of course not the first quarter that we saw an actual expense (vs a credit) for that category and the provision was in line with what JPM should be booking here. Investors though were rather upset with the suspension of share buybacks.

“As a result of the recent stress tests and the already scheduled G-SIB increase, we will build capital and continue to effectively and actively manage our RWA. In order to quickly meet the higher requirements, we have temporarily suspended share buybacks which will allow us maximum flexibility to best serve our customers, clients and community through a broad range of economic environments.”

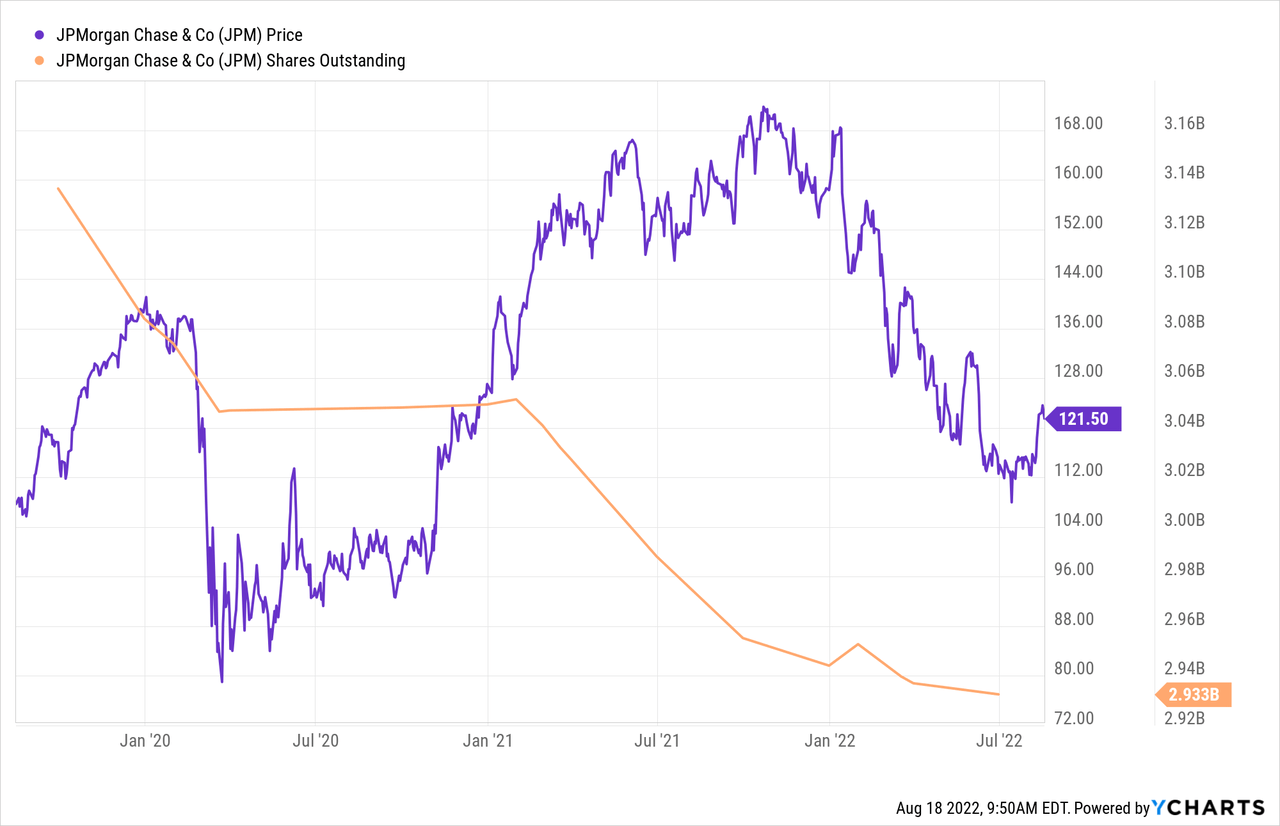

While some may be upset over this, it is a middling path. The facts have changed, so management changed their minds. It is better to have suspended the buyback rather than continue in the face of new troubling information. The last thing anyone wants is to buyback at $120 and reissue stock at $80. There are countless companies which have done something like that. Buy high and sell low. At least JPM share count has headed more or less in a singular direction and that is good.

The combination of rapid monetary tightening, extreme food and energy inflation, alongside a steep fiscal cliff makes a recession almost a certainty in our view. Alongside that, the very tight labor market means that expenses will rise for most firms faster than revenues. We think JPM won’t be able to dodge this and we expect lower earnings and lower multiples on its earnings in 2023. Analysts are modeling $12.41 for next year and we think the low end of $9.94 won’t be met.

Seeking Alpha

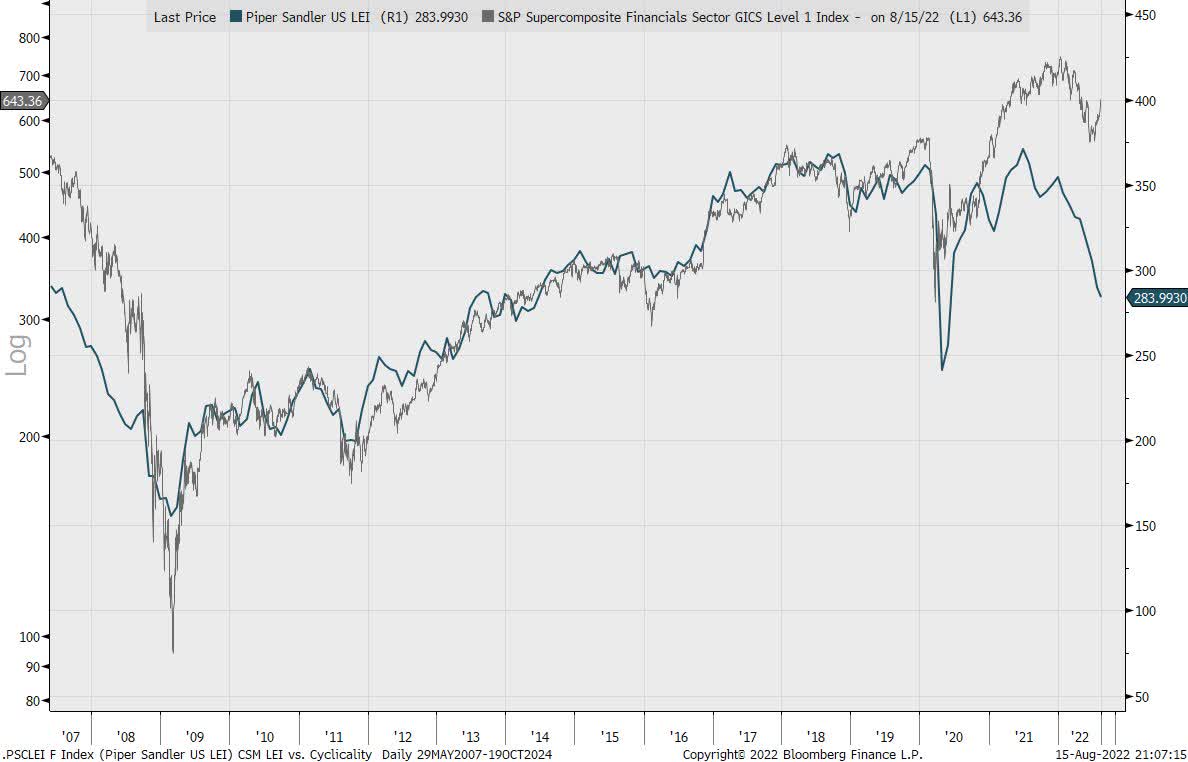

Financials have recently diverged from Leading Economic Indicators and by a rather huge margin as well.

Michael Kantro- Twitter

This reinforces our view that we are looking at a bear market rally here and would not get attached to the current stock price. That brings us to where would you actually want to buy this? When we last suggested $110 strikes, we were nowhere in the zone of pricing in a recession. So all other things being equal you would want to aim slightly lower. We also have a completely flattened out yield curve and that adds one more headwind. At the same time, the earnings infusion and along with buybacks being stopped, raises tangible book value.

Verdict

Tangible book value has dropped in 2022, despite retained earnings and that comes from some mark to market noise on the portfolio. This is not unique to JPM and we have seen some far bigger drops in some other financial stocks. Some of this could reverse, but even without that, tangible book should rise to about $70 by year end. Our low point valuation would be about 1.4X tangible book value and that would be close to $100, versus the $110 we aimed for last time. Examining the landscape, we are not getting attractive option premiums for the $100 strikes so we are right now in a wait and see mode. We rate the bank a “hold” and will update after Q3-2022 results.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment