FotografiaBasica/E+ via Getty Images

The company of John B. Sanfilippo & Son (NASDAQ:JBSS) is one of those interesting little microcaps that is still too small for Wall Street to take note of but is still strong enough for the rest of us to consider. The company is conservatively managed, with little debt, and its primary product is one that is much loved: nuts.

As much as I like the company and its strengths, I rate the stock a hold.

Sanfilippo’s Business

Gaspare Sanfilippo and his son John founded a pecan shelling company in 1922. The fourth generation of Sanfilippos are now among the executives of the company. Jeffrey T. Sanfilippo is the CEO. Michael J. Valentine is the Group President and Secretary. Jasper B. Sanfilippo is the COO, President, and Assistant Secretary.

The Sanfilippo family continues to control the company. Jeffrey T. Sanfilippo, Jasper B. Sanfilippo, Jr., Lisa A. Sanfilippo, John E. Sanfilippo and James J. Sanfilippo own stock representing approximately 50.7% of the voting interest in the Company. In addition, Michael J. Valentine, the cousin of the Sanfilippos, owns approximately 23.8% voting interest.

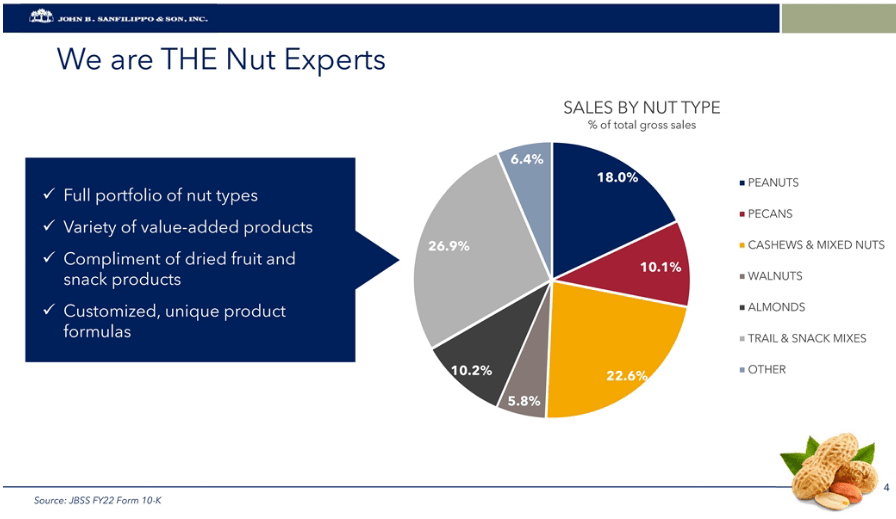

Nuts account for 94-95% of the gross sales for the last three years, according to the company’s most recent 10-K. “The nut product line includes almonds, pecans, peanuts, black walnuts, English walnuts, cashews, macadamia nuts, pistachios, pine nuts, Brazil nuts and filberts.” (A filbert is similar to a hazelnut.) Perhaps their most iconic product is Fisher peanuts. Other name brands include Orchard Valley Harvest, Hunter Mix, and Squirrel.

The company believes it has the single largest nut processing facility in the world. The vertically integrated processing allows the company to control “almost every step of the process.” Corporate headquarters is in a 1,000,000 square-foot processing facility in Illinois. Research & development is located there as well. A peanut processing facility is in Georgia. Almonds and walnuts are processed in California, and pecans are processed in Texas. Distribution channels include retailers, commercial ingredient users, and contract packaging customers.

The nut product mix is given in the most recent quarterly report:

Sanfilippo’s Product Mix (Sanfilippo Quarterly Report)

Growth plans include expanding capacity and growing into the snacking segment. Since then the company announced that it has acquired Just the Cheese brand from Specialty Cheese Company. The brand competes in the baked cheese snacking space. The acquisition will reportedly not have a significant impact on financial results, but it allows the company to expand into the snacking category.

The acquisition is certainly not the first for the company. Among the companies acquired are:

-

1974: Evon’s brand

-

1992 to 1994: Sunshine Nut Company and Crane Walnut

-

1995: Fisher

-

2010: Orchard Valley Harvest

-

2017: Squirrel Brand Co.

A dividend was started 2017, and to the company’s credit, the dividend has grown since then, right through the pandemic. However, the dividend is still small at a 0.95% yield.

The company’s strength is its balance sheet. The company has been gradually shrinking the debt load over the years, and can pay all of its liabilities with current assets. Another bolt-on acquisition is well within reach should management find another.

Valuation of Sanfilippo’s Business

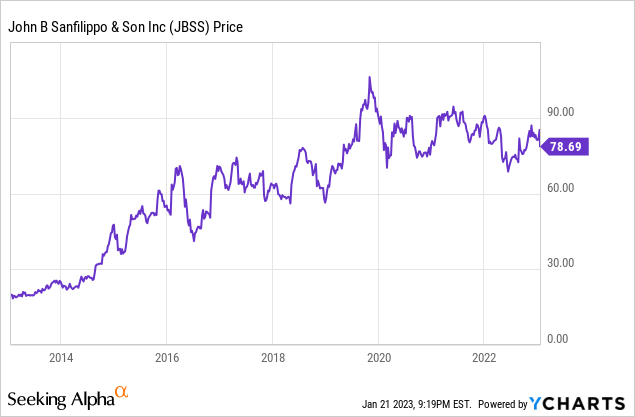

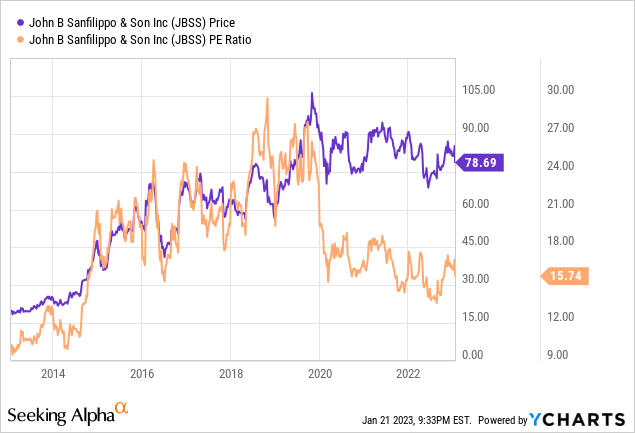

The company’s stock price can be mildly described as volatile. It has, however, gone up from $20 in 2013 to nearly $110 in late 2019, just before the pandemic hit. Since 2020 the stock has essentially traded sideways.

The stock the valuation dropped with the coming of the pandemic, and it has been dropping since:

Others have said the company has low growth. Viewed over ten years, the last two years do look anemic, and the compounded average growth rate has been slowing:

| 10-year CAGR | 12.93% |

| 5-year CAGR | 10.95% |

| 2-year CAGR | 6.60% |

Supply chain problems and higher costs have not been helping. In the most recent quarter, freight costs were reportedly stabilizing. Peanut acquisition costs, however, were significantly higher over last year: “Main reason is that peanut farmers needed to pay higher prices to plant their fields to compete with cotton and soy.”

What Could Go Wrong?

The problem with peanut costs is just one example showing that the company does not have control over the availability of nuts, nor the costs to acquire those nuts. It is not unreasonable to think that costs will continue to rise.

Fisher Peanuts might be a well-known brand, but it is not the only one. Planters Peanuts is possibly better known, and Hormel shelled out $3.35 billion to acquire the company in 2021, a company that had net sales of about $1 billion in 2020. Sanfilippo posted revenues of $880 million for the same year, so Planters was a larger competitor that was acquired by an even much larger competitor.

The company has grown in the past by acquisitions, and it is possible that any future acquisition will turn sour. Furthermore, current plans for growth look rather anemic. Growth is said to be enabled by digital commerce and an ESG strategy, but it is hard to understand at this point how either will help. The initiatives could well fall flat. If the company does not grow more, and the dividend stays small, it is hard to see much improvement in the stock price.

Further complicating matters is that the stock price is quite volatile.

Conclusions

Sanfilippo has much to say for it. It is still a family business after 100 years, and its management is committed to a conservative balance sheet with low debt. A dividend was started in 2017 and has been growing. The company has made strategic acquisitions over the years.

The issues have to do with its low growth and small dividend, neither of which has much to make investors excited. The company should not be dismissed entirely, though. A strategic acquisition could be catalyst to reignite some excitement, but acquisitions have risks of their own.

The hold rating is made with some hesitation. When I originally wrote this article a few days ago, I wrote that the stock price could well drop another 10% from 78.69, or it could just as well pop back up. A few days passed, and now the stock price at $81.09. Traders might well have a good time with this stock, but for investors like me, a price below $70 might be a consideration.

Be the first to comment