Boarding1Now/iStock Editorial via Getty Images

The whole airline sector has been beaten down due to rising oil prices and recession fears while the airlines have bloated debt levels from COVID losses. Most of the stocks are so cheap, investors should load up anyway, but JetBlue Airways (NASDAQ:JBLU) is the one airline stock to avoid now. The investment thesis is Bearish on this stock due to the large cash bid for Spirit Airlines (SAVE).

Merger Problems

The whole airline sector is under pressure due to fears the higher oil prices and a recession will prevent the repayment of debt. A lot of sector companies built up large debt loads during the lean COVID years and the whole hope was for booming travel demand on an economic reopen to provide the cash flows to help these airlines repay debt.

One of the big benefits to owning JetBlue was the limited debt loads. The airline only had a net debt balance of ~$1.1 billion at the end of March, leaving the airline with one of the better balance sheets in the industry. JetBlue has total debt of $3.93 billion with a solid cash balance to offset most of the debt.

The issue with the bid to acquire Spirit Airlines is the cash nature of the deal. JetBlue wants to use cheap debt to make the deal accretive, but a lot of investors would prefer the airline avoid a larger debt load considering having limited debt was a huge advantage.

JetBlue was just required to boost the bid for Spirit to $33.50 per share due to that BoD preferring a prior offer from Frontier Group (ULCC). The increased bid price of $2.00 per share would require JetBlue to spend $3.7 billion in cash and an enterprise value of $7.5 billion when including the debt levels of Spirit. The deal would increase the net debt of the larger JetBlue to closer to $6.6 billion. Also, the airline would pay an upfront accelerated prepayment of $1.50 per share.

In addition, the airline has agreed to pay $350 million in a reverse break-up fee, if management is unable to get regulatory approval. JetBlue has a lot to lose and not much to gain under a merger where the company piles on debt.

JetBlue proposes to proactively offer the U.S. Department of Justice a divestiture of all Spirit assets in the New York and Boston market and reduce gates and assets in Fort Lauderdale. Divesting a lot of key assets reduces the value of the deal.

Source: JetBlue May 16 presentation

The major saving grace for JetBlue shareholders is that Spirit hasn’t accepted a deal with the preference for the Frontier combination. For now, the Spirit management team is in favor of the business combination that provides more long-term value in comparison to the quick gains of a cash out with JetBlue.

Walk Away

The market is clear in a preference for JetBlue to walk away from the deal. The stock is down over 40% YTD while Frontier Group has only dipped 28% and Southwest Airlines (LUV) has only fallen 17%. The airline sector has definitely struggled with the weak stock market, but JetBlue would likely pop on cancellation of the bid for Spirit.

The Frontier offer doesn’t have the same regulatory risk and the deal is mostly stock. The ultra low-cost carrier isn’t taking on additional debt to pay for the deal, making the offer superior to those shareholders where the combination provides synergies to make a better airline to compete with the big four.

JetBlue has to take on substantial debt in order to complete this deal. Shareholders are taking on additional risks in order to possibly produce additional returns with the combined Spirit business.

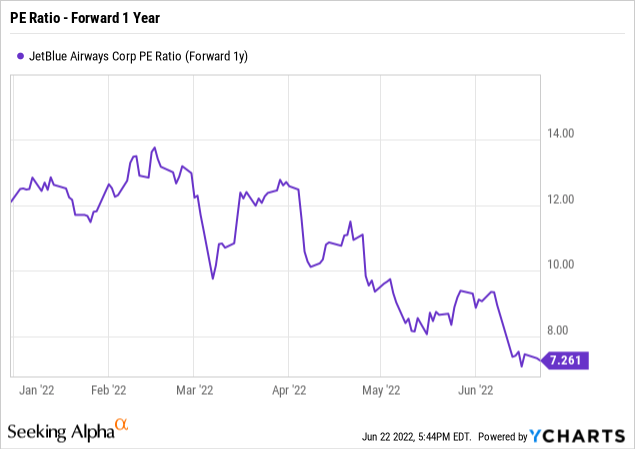

The market questions whether JetBlue can hit EPS targets of nearly $2 in 2024. The stock trades at only 7x current 2023 targets, making JetBlue clearly cheap by just meeting targets without the additional risk of the debt from Spirit.

In essence, shareholders have an easy path to strong stock returns by just executing on the current plans. Collecting a bunch of debt paying for Spirit while assuming the ultra-low cost carrier’s debt isn’t ideal and the stock price reflects this scenario.

Takeaway

The key investor takeaway is that a move by JetBlue to end the pursuit of Spirit Airlines would be a buy signal. Otherwise, investors should avoid this stock with the plan to build up a large debt position while having to engage in a lengthy regulatory battle in an attempt to create the 5th largest airline carrier.

Be the first to comment