alvarez/E+ via Getty Images

The construction industry is vast and complicated. There are many working parts in the space that are required in order for the end product to come together. And one firm that’s dedicated to providing some of the particular goods that are needed in the space is JELD-WEN Holding (NYSE:JELD). For the most part, JELD-WEN focuses on the production and sale of interior and exterior building products like windows, doors, and other related offerings. Fundamentally speaking, the picture seen by the business recently has been somewhat mixed. But that’s not necessarily horrible. Given how cheap the stock is, I believe that some fundamental weakness can be overlooked.

Don’t close the door on this one yet

The first and only article I ever wrote about JELD-WEN before now was published near the end of June of 2022. In that article, I talked about how the company’s financial performance had been rather mixed as of late. I also went so far as to say that trend may continue in the near term, largely because of uncertainty and weakness in the housing and construction markets. But even after factoring in potential weakness, I felt as though shares of the business were trading on the cheap, cheap enough at least to offer some attractive upside. As a result, I ended up rating the business a ‘buy’, a rating that reflected my belief that shares would likely outperform the broader market moving forward. Unfortunately, things have not gone exactly the way that I anticipated. While the S&P 500 is up 7% since the time I published that article, shares of JELD-WEN have seen downside of 10.7%.

Author – SEC EDGAR Data

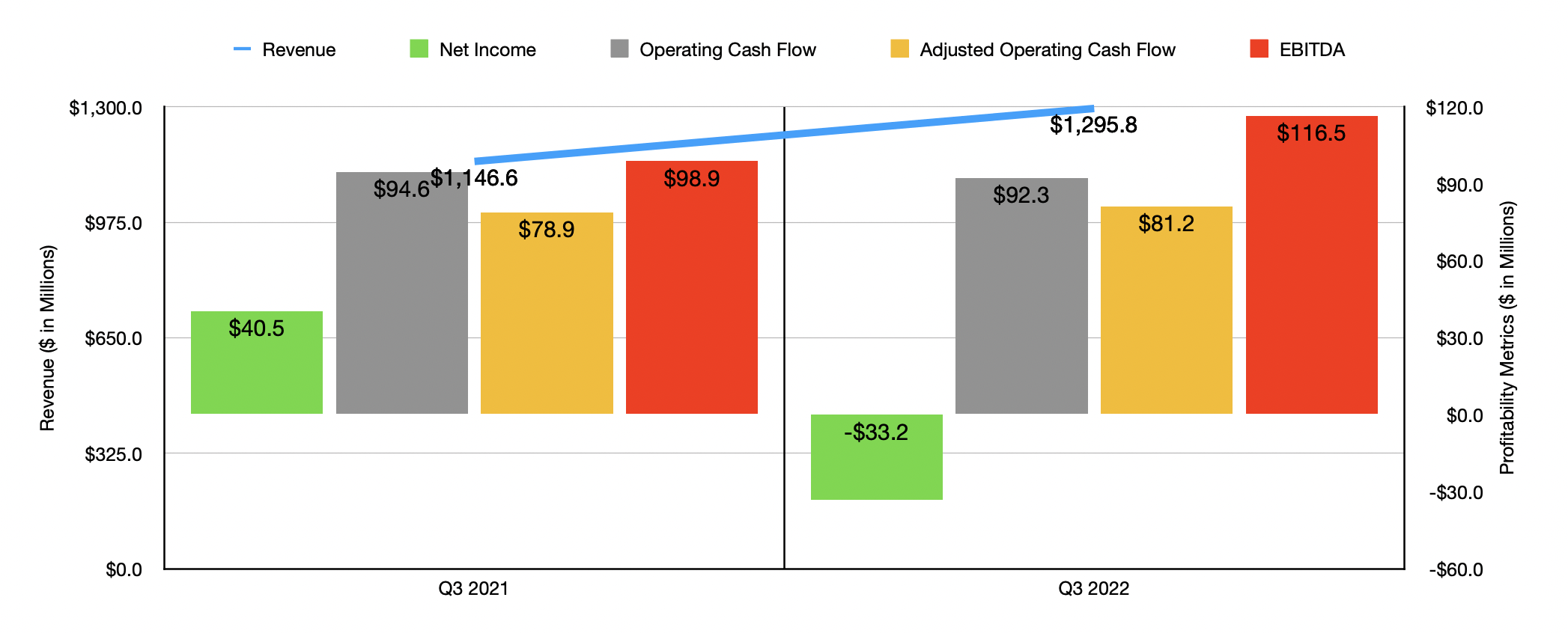

To be perfectly honest, I find this return disparity to be perplexing. I say this because, while financial results achieved by the company have been mixed, they haven’t exactly been bad. Consider how the company performed during the third quarter of its 2022 fiscal year. During this time, revenue came in at just under $1.30 billion. That’s 13% higher than the $1.15 billion reported one year earlier. According to management, this revenue increase was driven by an improvement in core revenues of 18%. This was offset some by foreign currency fluctuations. For the core revenue side of things, 15% of the 18% increase was driven by higher pricing, while the remaining 3% was driven by a favorable volume and product mix.

Even though sales rose nicely, and would have been better had it not been for foreign currency fluctuations, profits for the company worsened. The business went from generating a net profit of $40.5 million in the third quarter of 2021 to generating a net loss of $33.2 million. Most of this pain, however, was driven by a $54.9 million goodwill impairment reported in the third quarter of 2022. The company also reported an increase of $6 million worth of impairment and restructuring charges during that quarter. And, on top of this, inflationary and supply chain pressures were responsible for pushing its gross profit margin down from 19.9% to 19.4%. That alone was responsible for another $6.5 million in pretax profits disappearing. Other profitability metrics, however, did not exactly follow suit. It is true that operating cash flow dipped from $94.6 million to $92.3 million. But if we adjust for changes in working capital, it would have ticked up modestly from $78.9 million to $81.2 million. And finally, EBITDA during this time popped from $98.9 million to $116.5 million.

Author – SEC EDGAR Data

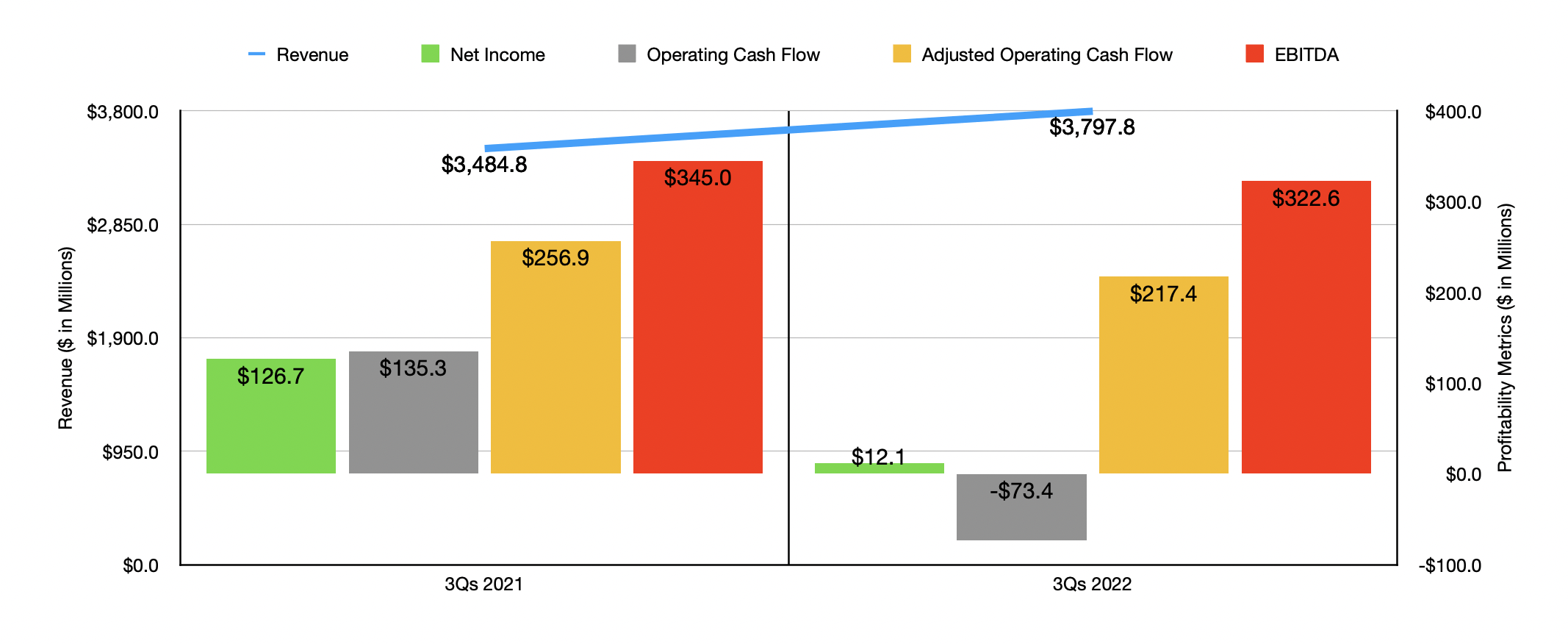

Interestingly, the third quarter on its own was actually better than what the company experienced for the first nine months of 2022 as a whole relative to the same time one year earlier. During that nine-month window, sales came in at $3.80 billion. That’s 9% higher than the $3.48 billion reported one year earlier. On the other hand, profits went from $126.7 million to only $12.1 million. Once again, impairment charges, restructuring charges, and margin pressures all played a role in this. But what is positive is that the overall gross margin situation for the business was drastically better in the third quarter than it was in the nine months as a whole. Year over year, for the nine-month window covered, the margin fell from 21.7% to 18.4%. Other profitability metrics, sadly, were not the same as they were in the third quarter. Operating cash flow went from $135.3 million to negative $73.4 million. On an adjusted basis, it still fell, dropping from $256.9 million to $217.4 million. Meanwhile, EBITDA ticked down from $345 million to $322.6 million.

For 2022 as a whole, management said that core revenue growth should be around 10%, with overall net revenue expected to rise by between 4% and 6%. The company also said that EBITDA would come in at between $400 million and $420 million. That bottom line estimate was probably the largest contributor to the company’s share price decline over the past several months. I say this because, previously, management was forecasting EBITDA for 2022 at between $430 million and $450 million. And when I last wrote about the company, they were talking about a reading of between $520 million and $565 million. Downward revisions are problematic and they impair the faith that investors have in management. No guidance was given when it came to other profitability metrics. But if we annualize the results experienced during the first nine months of 2022, we would expect adjusted operating cash flow of $281.3 million.

Author – SEC EDGAR Data

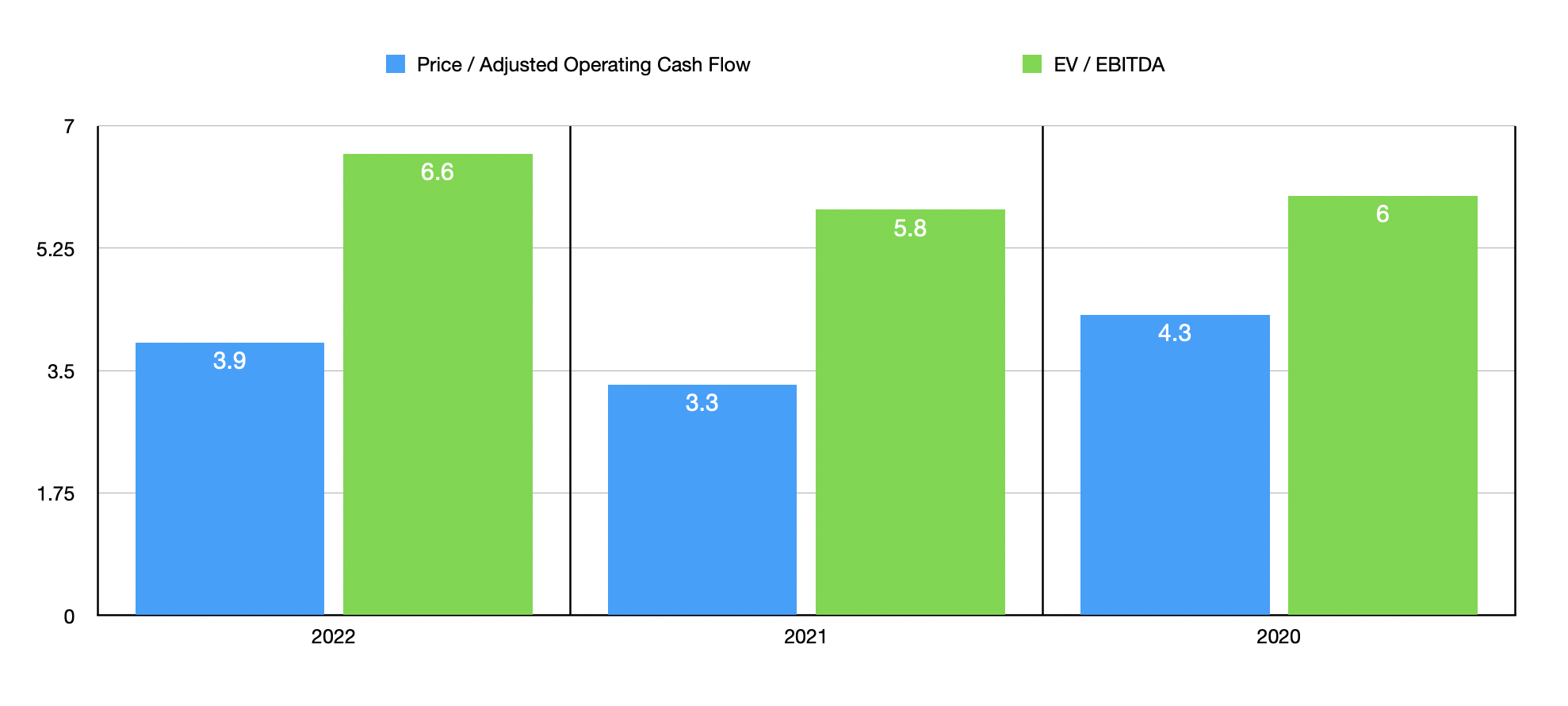

Based on these figures, JELD-WEN is trading at a price to adjusted operating cash flow multiple of 3.9 and at an EV to EBITDA multiple of 6.6. In the chart above, you can see pricing under the assumption that we revert to financial performance achieved in either 2020 or 2021. Even turning back the clock to the 2020 fiscal year would make shares very cheap on an absolute basis. As part of my analysis, I also compared JELD-WEN to five similar firms. On a price to operating cash flow basis, these companies ranged from a low of 6.8 to a high of 26. Meanwhile, using the EV to EBITDA approach, the range was from 7.8 to 15. In both cases, our prospect was the cheapest of the group.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| JELD-WEN Holding | 3.9 | 6.6 |

| Janus International Group (JBI) | 20.8 | 11.7 |

| Gibraltar Industries (ROCK) | 23.3 | 12.4 |

| Griffon Corporation (GFF) | 9.7 | 9.2 |

| CSW Industrials (CSWI) | 26.0 | 15.0 |

| PGT Innovations (PGTI) | 6.8 | 7.8 |

Takeaway

Fundamentally speaking, JELD-WEN is experiencing a bit of volatility. However, data from the third quarter of 2022 shows that the picture is improving to some degree. We could see some weakness if the construction and housing markets see further downside than what they have already. But given how cheap shares are, it’s difficult to imagine a scenario where the company could look anything worse than fairly valued. Because of this favorable risk-to-reward outlook, I cannot help but to keep it at the ‘buy’ rating I had it at previously.

Be the first to comment