Andrew Burton

Article Thesis

JD.com, Inc. (NASDAQ:JD) will report its quarterly earnings on Friday. In this article, we’ll look at what investors can expect from the upcoming report, and also what else is important for JD.com right now.

JD Quarterly Results Outlook

When JD.com reports its results on Friday, November 18, analysts believe that the company will announce that it has generated revenues of $34.5 billion, which would be up 1% from the previous year’s level. That’s not a lot of growth, but investors have to consider the macro environment, of course. First, inflation in China is way lower than in the US, Europe, and so on — expected consumer inflation in China is just 2.2% in 2022. Thus real growth is better relative to a scenario where an American e-commerce company reports a 1% nominal growth rate.

Amazon, for example, delivered revenue growth of 7% in H1, which is significantly better in absolute terms, but which is relatively comparable once we account for the higher rate of inflation in the United States.

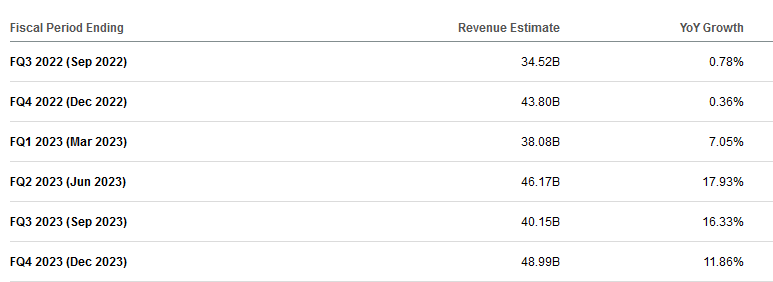

On top of that, China also continues to be impacted by strict COVID policies in the country. Lockdowns and other strict measures cause uncertainties among consumers and businesses, which are not very eager to spend. Supply chain issues and other problems that are caused by China’s COVID policies further hamper economic activity, which naturally also has an impact on companies such as JD.com. In general, a low-single-digit growth rate from an e-commerce powerhouse could be seen as very problematic, but once we consider the current macro headwinds that will hopefully not be in place forever, things do not seem as gloomy. There is a good chance that JD.com’s business picks up again in the future, once COVID measures are less strict and economic activity improves. That is why analysts are currently forecasting that JD.com’s revenue growth will improve to 7%-18% in the four quarters in 2023, as we can see in the following table:

Seeking Alpha

Revenue growth is not the only important metric, of course. Analysts are much more optimistic when it comes to JD.com’s profitability, as earnings per share are forecasted to have risen by 28% during the quarter, to $0.63. To see expected earnings growth of this magnitude is somewhat surprising at first sight, considering the slim expected revenue increase. But JD.com has essentially done the same during the previous quarter, when its revenue was up 5% year over year, and when the company nevertheless managed to grow its earnings per share by 31% year over year. With slightly higher revenue growth, relative to what is expected for Q3, and with an even higher earnings per share growth rate, the Q2 results were a comparable feat profitability-wise, relative to what analysts are forecasting for the third quarter, as JD managed to turn a smallish revenue increase into a big earnings per share increase during the second quarter, too.

One reason for JD’s ability to grow its earnings per share faster than its revenue is an improving product mix. The company has seen its services growth come in way above its product revenue growth in the recent past. During the second quarter, JD.com saw its services revenue grow by 22% year over year, for example, while product revenue was up by just 2% over the same time frame. Services revenue comes with higher margins and better scalability — gross expenses are generally lower for services than for product sales, thus operating leverage is more powerful at services companies. This relationship is showcased, for example, by the much stronger accretiveness of business growth at many software companies, relative to what lower-margin product companies such as automobile companies are experiencing. With JD’s services business growing fast, operating leverage in that area works heavily in its favor, helping boost profitability on a company-wide basis.

On top of that, JD has also, like many other tech companies, started to bring down expenses as it has become clear that many investors are increasingly focused on bottom line performance — the reason Meta (META), Amazon (AMZN), and so on are cutting their employee count. JD has also realized that the times have become tougher and that putting more focus on working efficiently is a good idea. JD has, for example, cut back on marketing spending in recent quarters — in Q2, marketing expenses were down year over year. That results in lower top line growth, but profits can improve through such measures.

Valuation And Balance Sheet Flexibility

Like many other Chinese tech companies, JD has a balance sheet with considerable investments. Between cash, cash equivalents, restricted cash, and short-term investments, the company owned $31 billion in assets at the end of the second quarter. It would not be surprising to see this number come in even higher at the end of the third quarter, although working capital movements might prevent JD from growing its cash (and equivalents) position further in the short-term.

$31 billion in cash and short-term assets are equal to around 40% of the company’s current market capitalization, which makes for a very large cash pile. That is a way larger cash position compared to the cash positions of major American tech companies such as Apple (AAPL) or Alphabet (GOOG) that are oftentimes in the 5% to 10% range (which is also quite meaningful already). When we look at JD’s net cash position instead of its gross cash position, by subtracting $2 billion in short-term debt and $2 billion in long-term debt, JD still has a pretty sizeable $27 billion in net cash on its balance sheet — equal to around 35% of the company’s current market capitalization.

Looking at JD’s cash generation, we see that the company has generated $4.1 billion in free cash over the last twelve months. That’s mostly due to the company’s somewhat low spending on capital expenditures, which totaled just $2.5 billion over the last year. JD has been way more disciplined in spending on growth relative to past years, which can be a good thing, although it has a negative impact on business growth which helps explain why top line growth has come down from previous highs.

Since JD already has a very strong balance sheet, utilizing free cash flows for balance sheet strengthening does not make a lot of sense. JD has thus decided to return cash to its owners via share repurchases and dividends. The company made a special dividend payment earlier this year, and has a $3 billion share repurchase authorization in place. I’m not a big fan of special dividends, but buybacks could create value over time, assuming management times these purchases correctly — buying in the low $50s or the $40s is way better than buying in the $60s and above.

Based on current earnings per share estimates for this year, JD.com is valued at 26x forward earnings. That’s not a low valuation in absolute terms, and also far from cheap relative to how other tech companies are valued — META, GOOG, and so on, are way cheaper, for example, despite no China-related macro risk. When we account for JD’s net cash position, however, things look different. Subtracting the $27 billion in net cash from its market capitalization and dividing that number by the expected profits for this year gets us to a cash-adjusted earnings multiple of 17. That’s still higher than the valuation of Alibaba (BABA), for example, but seems much more reasonable compared to a 26x earnings multiple.

Final Thoughts

JD.com is extremely reliant on China. This makes the company vulnerable versus COVID measures in its home market, and Taiwan-related tensions are also not to be forgotten. But on the other hand, JD also has potential in case China’s economy opens up again — as a Chinese consumer play, JD could be among the companies benefitting most from relaxed COVID measures once that happens.

The earnings outlook for the third quarter is very positive, as disciplined spending and expense controls, coupled with an improving product mix, should allow JD to grow its earnings meaningfully despite the fact that its revenue growth is rather low in the current environment.

I do not see JD as an extreme bargain right here, but when we consider the large net cash position and the potential for JD if China opens up again, a bullish case can be made with JD trading at a high-teens cash-adjusted earnings multiple.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment