Credit Crisis, Coronavirus, Japanese Yen, Leveraged Loan, CLOs – TALKING POINTS

- Japanese Yen may rise as coronavirus threatens global financial stability

- Delicate corporate debt markets could catalyze market-wide credit crisis

- Leveraged loan market, collateralized loan obligations could be culprits

CORONAVIRUS MAY TRIGGER CREDIT CRISIS AS CORPORATE DEBT WOBBLES

The anti-risk Japanese Yen has rallied while global equity markets continue to face intense selling pressure as fear about the coronavirus inducing a recession permeates sentiment. Global economic normalization is at risk of being derailed by COVID-19 while financial vulnerabilities in the corporate debt sector are on the verge of potentially causing a world-wide credit crisis.

In the OECD’s Capital Market Series, the international organization emphasized their report on the corporate bond market and how its structurally-precarious nature poses a risk to global financial stability. At the end of 2019, global corporate debt reached an all-time high at $13.5 trillion. The catalyst behind the surge in corporate bond issuance was attributed to favorable credit conditions provided by hyper expansionary monetary policy.

Just in that year, non-financial firms borrowed $2.1 trillion viacorporate bond issuance, though the overall credit quality of these debt obligations has significantly declined. The newly-issued bonds have longer maturities, higher repayment thresholds and weaker covenants. The latter term refers to conditions a borrower has to fulfill in order to acquire the desired funds.

Consequently, both lenders and borrowers are now more exposed to an adverse turn in market conditions or from economic shocks – like the coronavirus – that could hinder the borrower’s ability to service their debt. These so-called covenant lite loans – that are now also being securitized into collateralized loan obligations or CLOs – constitute a growing market share of corporate debt. OECD analyst wrote that:

“The portion of non-investment grade issuance has also increased. Since 2010, at least 20% of all bond issues have been non-investment grade and, in 2019, they accounted for 25% of all non-financial corporate bond issues. This is the longest period since 1980 when the portion of non-investment grade issuance has remained this high and indicates that default rates in a future downturn will likely be higher than in previous credit cycles.” – OECD report.

According to the report, 51 percent of all new investment grade bonds were rated BBB, the precipice between a credit assessment designated as “investment grade” and “noninvestment grade”. The significance of this cannot be overstated: a majority of corporate bond issuance is a hair away from being labelled as “junk”. The nature of covenant lite loans may also distort the actual level of risk tied to trillions of dollars’ worth of debt.

The OECD warned – and I as outlined in 2018 – that due to the precarious nature of this debt market, a downturn could catalyze an onslaught of defaults and trigger or deepen a recession. Furthermore, policymakers stressed that the inability of borrowers to meet their minimum payment thresholds will likely be worse than in prior credit cycles.

Without the support of low interest rates or strong growth, the same circumstances which allowed highly-leveraged companies to take on more debt without losing their credit rating will likely be at risk of a downgrade. Consequently, this will raise borrowing costs for them at a time when their revenue stream would be drying up as external demand softens in fundamentally-unsound environment.

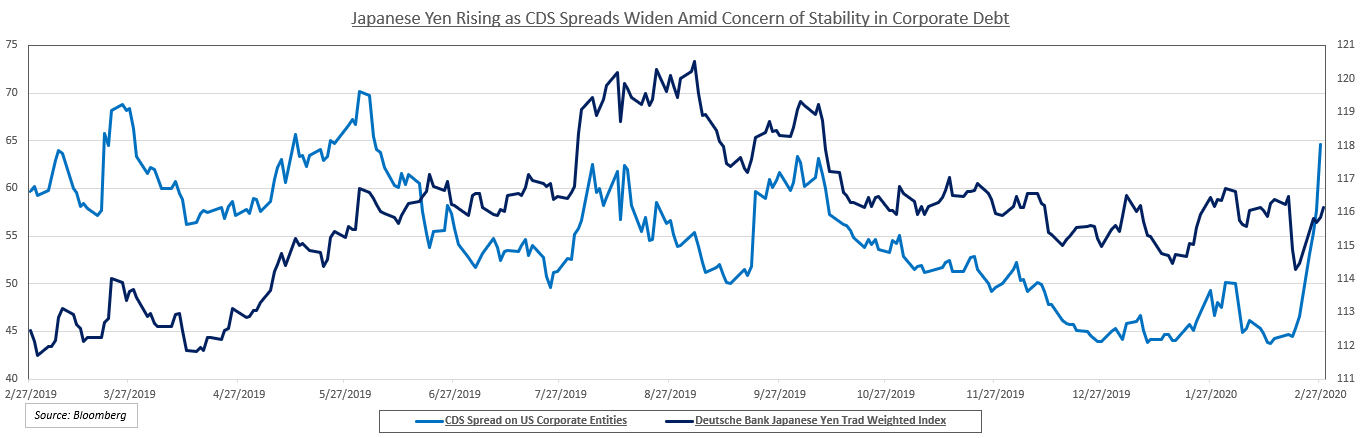

If default rates were to skyrocket, a worldwide credit crisis may ensue as interbank lending freezes. Much like what was seen in the last major financial crash in 2008, risk appetite for growth-oriented assets collapsed while demand for highly liquid, anti-risk assets like the Japanese Yen surged. Markets are already seeing this dynamic play out right now (see charts below).

{kind=link}

The Japanese Yen – using Deutsche Bank’s JPY Trade Weighted Index – has been rising alongside premiums on credit defaults swaps for ensuring US corporate entities while the leveraged loan index has been falling. This occurred while US junk bonds experienced their biggest capital outflow in two years as confidence in their durability quickly evaporated in the face of growing fundamental uncertainty.

JAPANESE YEN TRADING RESOURCES

— Written by Dimitri Zabelin, Jr Currency Analyst for DailyFX.com

To contact Dimitri, use the comments section below or @ZabelinDimitrion Twitter

Be the first to comment