Michael H/DigitalVision via Getty Images

Investment thesis

Shares in Japan System Techniques (OTCPK:JAPPF) listed in its home Tokyo Stock Exchange outperformed significantly in CY2022, driven by improving fundamentals as well as activities of MIRI Capital Management, a fund that actively engages with its portfolio companies. With a decelerating earnings growth profile and fair valuation multiples, we rate the shares as neutral.

Quick primer

Established in 1973, Japan System Techniques is a niche IT services company based in Osaka, Japan. Its core business is bespoke software development for customers, as well as working as a subcontractor for prime vendor IT companies. It also develops and sells a packaged software platform business called ‘Gakuen‘, catering to the higher education sector. Smaller parts of the business include medical data analytics targeted at the health insurance market and overseas system development projects.

The company was listed on the Tokyo Prime exchange in April 2022 (from the previous listing in the First Section) and has conducted a 2-for-1 share split (was announced in August 2022, and the pay date was October 1st, 2022). The company IPOed back in November 2001.

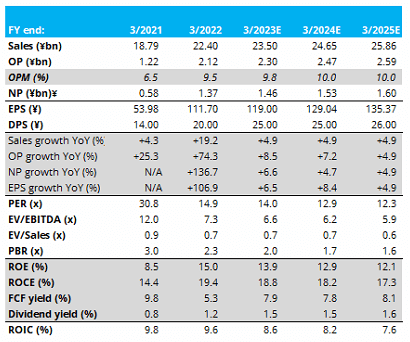

Key financials with earnings estimates

Key financials with earnings estimates (Company, Toyo Keizai, Karreta Advisors)

Our objectives

The shares (listed on the Tokyo Stock Exchange) in Japan System Technique rose 46% in CY2022, showing significant outperformance versus the TOPIX index (down 6%). We note that the shares began to rally in November 2022, despite the notable slowdown in profit growth YoY expected in FY3/2023.

In this piece we want to assess what drove the share price in CY2022, and if there are any fundamental reasons for the shares to continue outperforming going forwards.

Corporate actions or something else?

Japan System Technique had a notably successful FY3/2022 as it released a new version of its ‘Gakuen’ software platform, resulting in upgrade demand from existing customers as well as new account wins. As in-house packaged software sales are the most profitable activity for the company, it booked a record high operating margin of 9.5%, versus a 10-year historical average of 4.9%. Although this was a major positive, the shares initially did not react.

The company guided for a dividend hike YoY for FY3/2023 (from JPY20 to JPY25) (page 1) and announced a 2-for-1 split in August 2022. We believe that management was becoming more active in terms of managing shareholder returns. Historically, the company had been seen as a cash-rich value name with net cash making up over 50% of market capitalization in FY3/2021. The company started to conduct small share buybacks from FY3/2021 as well.

Recent trading in Q2 FY3/2023 has shown a significant slowdown in growth YoY, due to high hurdles YoY from the ‘Gakuen’ upgrade in the previous year. However, the shares have remained stable.

Our view is that although there have been notable improvements in company fundamentals as well as shareholder returns, the recent slowdown in growth pointed to something else driving the share price. We decided to check the shareholder register.

Engaging with the company

We note that the largest current shareholder of the company is a corporate entity called JAST with a passive 23.3% stake which has remained unchanged over the last 5 years – this appears to be a vehicle owned by the founding Hirabayashi family. The second largest shareholder with 20.1% is MIRI Capital Management LLC, which has built up its position since August 2021. This fund presents itself as a ‘consultavist’, taking a position between a consultant and an activist. By engaging and working with its portfolio companies, the fund seeks to invest in businesses that are undiscovered or misunderstood. This style is similar to other peers such as Taiyo Pacific and Ichigo Asset Management. Clearly, MIRI Capital Management has been successful with its investment to date – but what could be next?

The company is undergoing a shift away from its legacy bespoke system development work, and growing its value-added software and digital transformation services; this will help to improve the sales mix. The company remains well-capitalized and M&A for bolt-on deals is an option to expand its service offering as well as acquiring new customers – the company has over JPY6 billion/USD44 million in net cash.

There has been notable improvements in business performance as well as shareholder returns. However, the business is currently in stable single-digit growth mode in FY3/2023, and we cannot see a major acceleration in organic growth prospects.

Valuation

On our estimates the shares are trading on PER FY3/2024 12.9x with a free cash flow yield of 7.8%. Whilst these are low valuations, we believe that it reflects fair expectations for a stable and decent microcap stock. With the current daily trading liquidity at less than USD1m, this places it out of scope for most institutional investors.

Risks

Upside risk comes from an accelerating earnings growth profile into FY3/2024, driven by digital transformation demand from end customers as well as subcontracting work. M&A resulting in material accretive growth will also help the growth profile.

Downside risk comes from the relationship between MIRI Capital Management and the company breaking down, resulting the position being sold off. Lack of major fundamental developments will mean the shares remaining a cheap microcap.

Conclusion

Japan System Techniques has benefitted from its relationship with MIRI Capital Management, and it has made significant progress in improving its profitability. Capital allocation towards shareholders has also become more attractive. Its net cash can still be put to work to grow the business, but at this current juncture we believe the shares are fairly priced. We believe it will be harder work to grow and scale the business from here; we rate the shares as neutral.

Note: Japan is seeing more engagement and activist fund investing in the small cap space. We covered our view on a potential tender offer for Cybernet Systems (OTCPK:CBSZF) here.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment