ablokhin/iStock Editorial via Getty Images

The last time I covered J.B. Hunt (NASDAQ:JBHT) in April of this year, the biggest issue was falling economic growth expectations, which caused me to advise people to break up an initial investment. The bad news for the stock is that economic growth has further deteriorated. The good news for investors is that the market has priced in a lot of weakness. We’re in one of the fastest valuation compressions in history as money has left the market rapidly. At this point. the risk/reward for a J.B. Hunt investment is much, much better, which is a reason to assess the company from a dividend-growth point of view. While the stock is yielding just 1%, it is accelerating dividend growth as its investments in its own business are starting to pay off. Even if the next (potential) recession hurts sales, the company’s earnings power is great, its balance sheet is fantastic, and opportunities for shareholders are looking good.

Now, let’s look at the details!

A 1% Yield

Let’s get the bad news out of the way first. J.B. Hunt is paying a $0.40 quarterly dividend per share. This translates to $1.60 per year per share, which is roughly 1.0% of the current stock price.

1% isn’t a lot. The US 10-year government bond is yielding 3.2%. The S&P 500 is yielding almost 1.6%, and the Vanguard Dividend Growth ETF (VIG) is yielding 2.1% thanks to the current market sell-off.

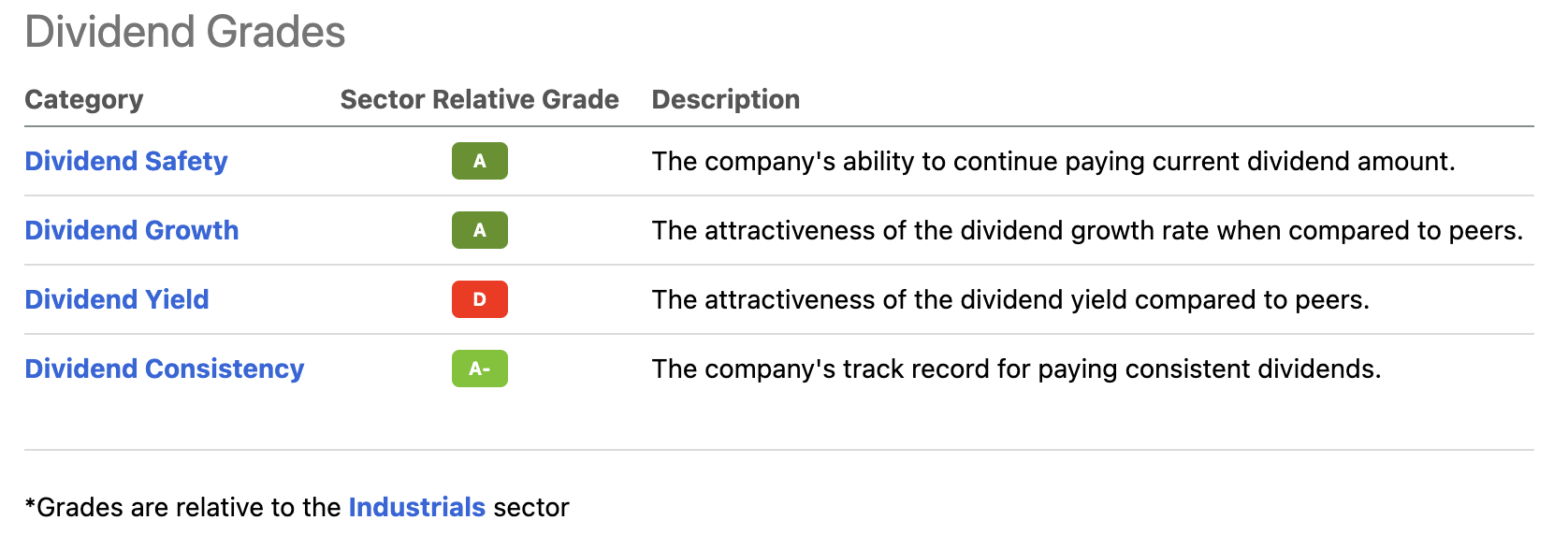

Using the Seeking Alpha dividend scorecard for JBHT, we see that the yield is indeed scoring very poorly compared to its industry peers. It gets a big fat D.

The good news is that all other categories score As (one A-).

Seeking Alpha

These “As” are the reason why JBHT is a good dividend growth stock as it will sooner than later turn the yield into something that’s actually acceptable for many.

See, the $0.40 per share per quarter dividend I just mentioned is the result of a 33% dividend hike on January 20. Before that, the company hiked by 11.1% on April 22, 2021. In January of the same year, JBHT hiked by 3.7%.

In other words, there’s clearly upside momentum, which puts the 10-year average annual dividend growth rate at 10.0%.

Accelerating Growth

Accelerating dividends are often the result of improving financials and management’s belief that the trend is sustainable. After all, rapidly increasing a dividend is somewhat of a “commitment” – not legally, but it raises expectations from investors.

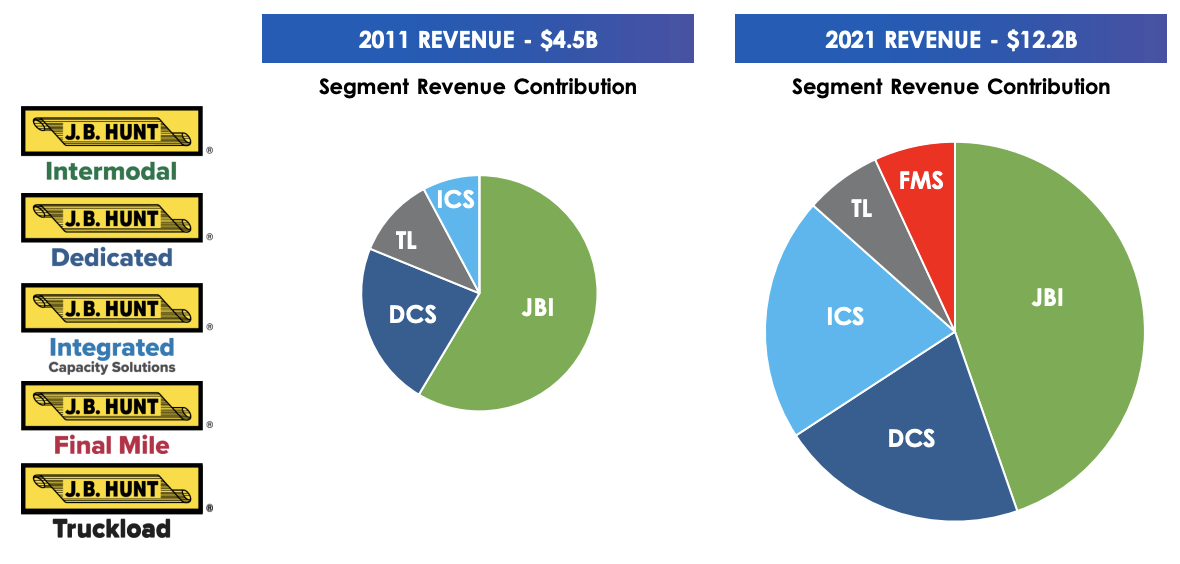

Between 2011 and 2021, the company improved its revenue from $4.5 billion to $12.2 billion, which translates to 9.4% sales growth per year. Moreover, the company has a new segment – final mile services – which aims to benefit from an increasing e-commerce business and the need to have efficient supply chains close to consumers. This includes fulfillment and retail pooling distribution services and the delivery of certain big and bulky items to consumers.

J.B. Hunt

Its largest segment, intermodal, is what most people will know J.B. Hunt from. The company has the largest fleet of containers and chassis in the world: more than 100,000. For example, the header photo of this article may be a common sight as JBHT’s containers are common goods on the nation’s freight trains.

The company also owns the largest dray fleet of trucks, totaling more than 6,100 trucks. The company’s containers are equipped with tracking.

The dedicated capacity solutions segment has a 98% customer retention rate as it services customers with more than 11,600 trucks and close to 30,000 trailers. The company is an expert in private fleet management. Now more than ever, this segment stands to benefit the company given ongoing supply chain issues:

We specialize in the design, development, and execution of supply chain solutions that support a variety of transportation networks.

Last year, this segment boosted revenue from $2.2 billion to $2.6 billion, that’s an 18% increase.

Moreover, and with regard to supply chain issues, the company’s integrated capacity solutions segment has grown to roughly a quarter of total revenues.

To quote the company:

ICS provides traditional freight brokerage and transportation logistics solutions to customers through relationships with thousands of third-party carriers and integration with our owned equipment within other segments. By leveraging the J.B. Hunt brand, systems, and network, we provide a broader service offering to customers by providing flatbed, refrigerated, expedited, and LTL, as well as a variety of dry-van and intermodal solutions.

This segment excites me as it reduces risks to the company while leveraging technology. For example, J.B. Hunt uses its 360 freight marketplace. According to Transportation Topics:

The primary goals, he said, have been to improve shippers’ access to capacity, provide more visibility into the status of their shipments and offer greater transparency through better use of data.

“We have a lot of data,” he said. “It’s really what we do with it.”

The industry stands to gain if more carriers, brokers, and shippers “let [their] guard down some” and find ways to share more information, McGee said.

By reducing risk to the company, I mean that the company can use the transportation capabilities from shippers across North America by brokering services. It allows J.B. Hunt to benefit from more than its own assets so to speak.

This segment had the following revenue growth rates in its 2019, 2020, and 2021, business years (note the uptrend): 1%, 23%, and 53%.

In the past few years, I was impressed by J.B. Hunt, but their business didn’t really excite me. That has changed as the company is using technology to elevate its massive business to a whole new level. Given its assets, business connections, and expertise, the company is in a terrific place to achieve higher growth.

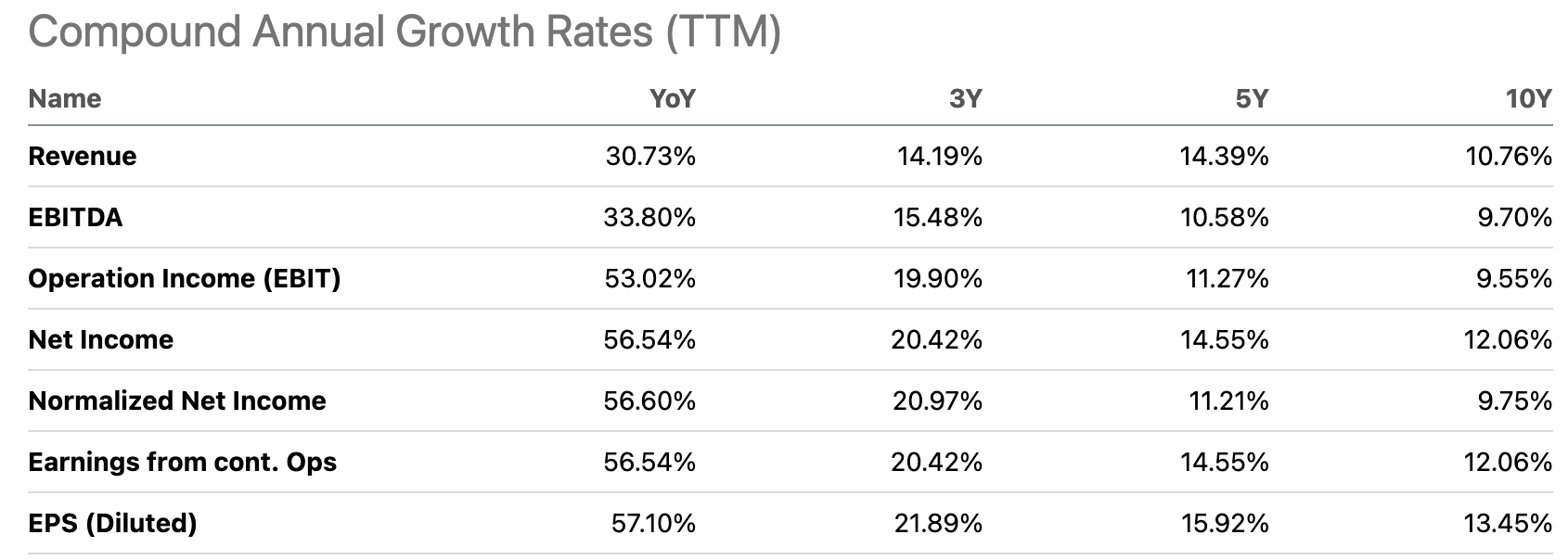

Using Seeking Alpha’s handy overview of compounded annual growth rates, we clearly see that the company’s growth rates have improved. Revenue added more than 14% per year over the past 5 years. The same goes for net income. Net income growth started to outperform revenue growth by roughly 600 basis points over the past three years.

Seeking Alpha

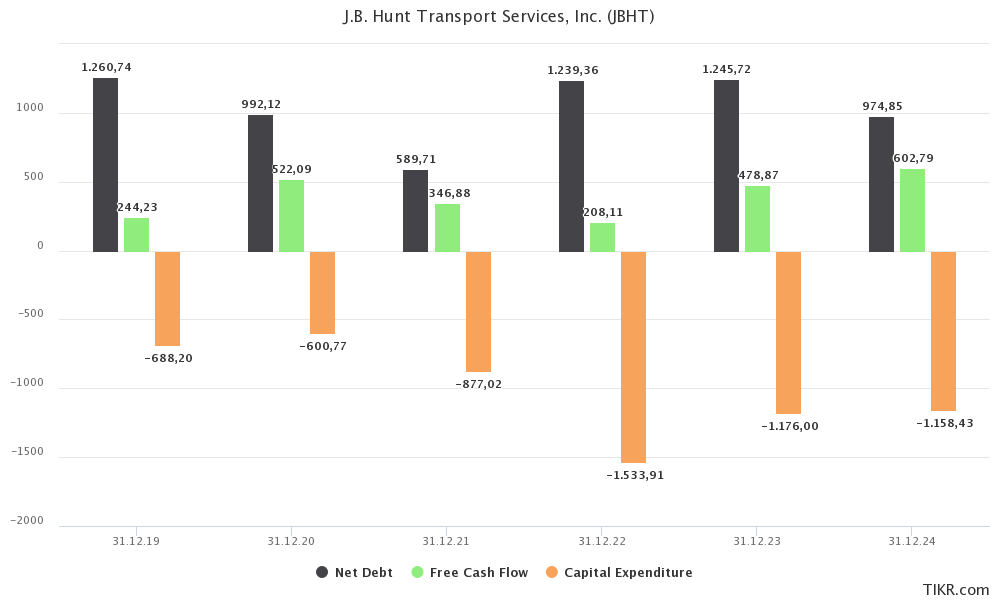

With that in mind, and with regard to the company’s dividends, I want to show you the chart below. In order to pay a dividend or to buy back shares, a company needs free cash flow. Free cash flow is operating cash flow minus capital expenditures. Free cash flow is basically “excess” cash that can be spent on buybacks, dividends, or to reduce debt. This year, the company is expected to accelerate CapEx to $1.5 billion, which will likely end up pushing free cash flow down to $200 million. In the years ahead, CapEx is still elevated, but higher earnings are still expected to support a free cash flow increase to more than $600 million in 2024.

TIKR.com

This would imply a free cash flow yield of 3.7% using the company’s $16.4 billion market cap. That not only covers the 1.0% yield but provides plenty of upside potential. It also helps that $1.2 billion in expected 2023 net debt is really low. It’s just 0.6x expected EBITDA.

The graph below was published earlier this year. It shows total operating cash flow, as well as outgoing cash flows. Needless to say, net CapEx is the biggest use of cash. The gap is filled with stock buybacks, dividends, and acquisitions.

J.B. Hunt

While it’s hard to say what the future will look like, rising free cash flow will almost certainly end up in investors’ pockets. Not just because there’s growing and spendable excess cash, but also because its healthy balance sheet does not require special attention (cash).

So, what about the valuation?

Valuation

The S&P 500 is down 23% year-to-date while I am writing this. As I have 95% of my money in my long-only dividend growth portfolio, I’m certainly not having that much fun. However, I’m not worried at all. It’s based on the opportunity to reinvest dividends and to buy quality stocks at good prices. I would be worried if I had invested in companies with shaky business models and financials.

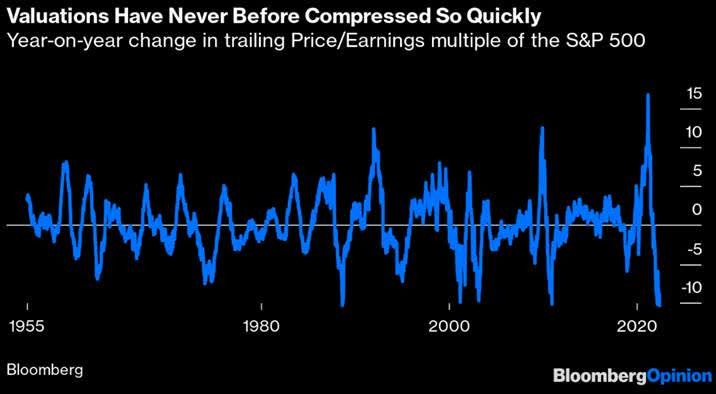

Yet, there’s no denying that this market is truly wild. As a matter of fact, valuations have never before compressed so quickly according to the macro newsletter of my friend Nick Glinsman.

Bloomberg, via Intelligence Quarterly

The problem is that valuation is based on at least two factors. On the one hand the price you pay for an asset (price). On the other hand, the value one gets (i.e., earnings). In other words, stocks can fall another 5-10% without getting any cheaper if earnings expectations come down.

The good news is that “everyone” expects earnings to come down. After all, by now, everyone is aware that there’s something wrong with the economy. Inflation is high, commodity inflation is hard to get down, the war in Ukraine will go on for a while, and the Fed is now aggressively hiking.

Hence, and to use Nick’s words:

The BofA survey found serious bearishness about the profit outlook. Only in the immediate aftermath of the Lehman Brothers bankruptcy in 2008 has a greater proportion of fund managers expected global profits to fall.

Bank of America, via Intelligence Quarterly

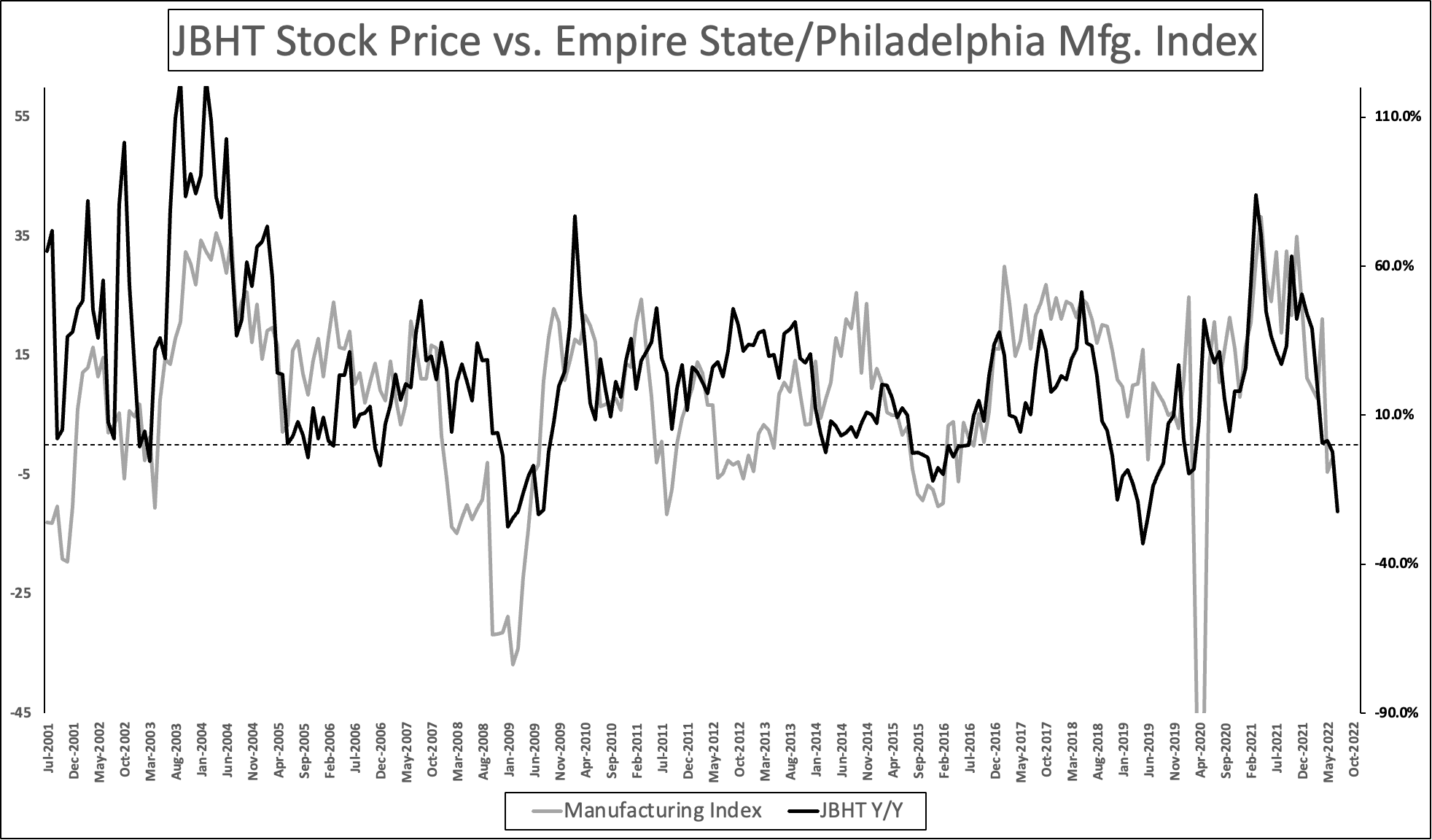

Speaking of expectations, economic expectations according to the New York and Philadelphia Fed are already in contraction territory as the graph below shows. In this case, I added the year-on-year stock price development of JBHT to the graph. For June, I used the stock’s max drawdown from its recent high. Investors have started to price in a recession. If the stock were to close at current prices this month, it would be one of the worst sell-offs since the Great Financial Crisis – excluding COVID.

Author (Raw Data: New York, Philadelphia Fed)

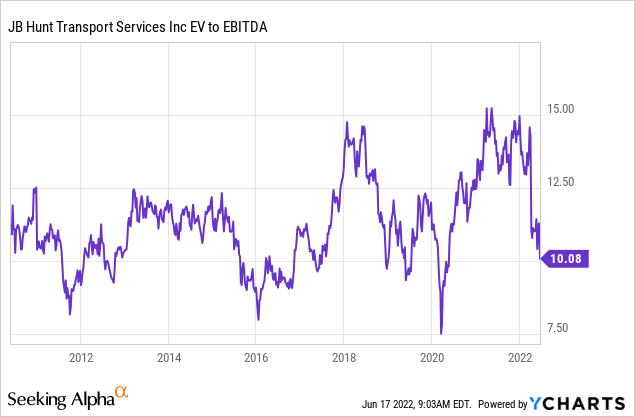

Right now, we’re dealing with a $16.4 billion market cap and $1.25 billion in expected 2023 net debt, which gives the company an enterprise value of $17.65 billion. That’s roughly 8.4x next year’s expected EBITDA ($2.05 billion).

That’s a good valuation, especially because it gives investors some safety. For example, if next year’s expected EBITDA comes in at $1.8 billion instead of more than $2.0 billion it’s still a 10x EBITDA valuation. Given the company’s business transition, that’s a good deal.

Takeaway

J.B. Hunt is doing a tremendous job accelerating growth. The company is not only streamlining its existing business but actively using technology to deeper penetrate the market for brokerage services and related.

Margins are rising, along with an accelerating uptrend in sales, EBITDA, and free cash flow after 2022.

On top of that, the company is now using its momentum to accelerate dividend growth as management is highly dedicated to boosting shareholder returns whenever possible. Its balance sheet is healthy and peaking CapEx should lead to accelerating free cash flow in the years ahead.

The problem is that JBHT is yielding just 1%. That’s a dealbreaker for a lot of investors as it will take time until this turns into a decent yield on cost.

However, the current bear market is giving the company an attractive valuation. Even if we account for lower-than-expected 2023 EBITDA, I think this stock offers a great risk/reward at current prices.

Nonetheless, because of ongoing market uncertainty, I advise new investors against buying a full position right away. I would break up an initial investment. I.e., buy 25% now and add on a regular basis. If the stock continues to fall, investors can average down. If the stock suddenly takes off, investors have a foot in the door. I am applying this approach to all new investments. Nobody knows exactly where or when stocks will bottom, but I do like buying good valuations. By breaking up an initial investment, I feel that I can spread entry risks a bit.

The only reason why I’m not long JBHT is that I have close to 50% industrial exposure.

(Dis)agree? Let me know in the comments!

Be the first to comment