Bulat Silvia

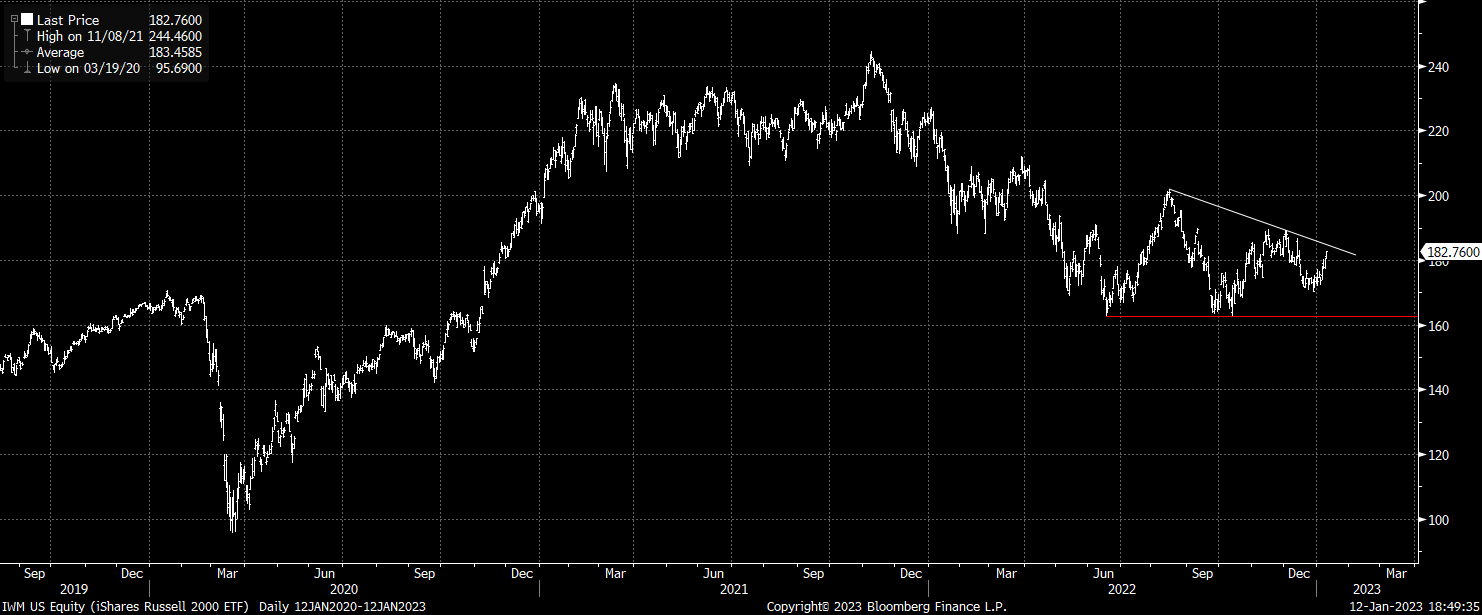

The price action in the iShares Russell 2000 ETF (NYSEARCA:IWM) suggests a big move is on the way as the trading range continues to contract. A break above USD185 from the current level of USD183 would likely trigger an upside reversal and the performance of the growth component of the index is likely to determine the price action of the IWM over the coming months. From a long-term perspective, the IWM remains a poor investment due to expensive valuations.

The IWM ETF

IWM tracks a market-cap-weighted index of U.S. small-cap stocks. The index selects stocks ranked 1,001-3,000 by market cap and currently holds 1,951 companies. The fund tracks the popular Russell 2000 index, and its broad basket makes it one of the most diversified funds in the segment. The current dividend yield sits at just 1.4% while the expense ratio is 0.19%. Investors should be aware that the PE ratio shown on the iShares website actually excludes companies with negative earnings, and when these companies are included, the ratio is significantly higher.

The ETF is extremely well diversified in terms of exposure to individual stocks, with no stock making up more than 0.5% of the index. It is also fairly well diversified in terms of sector exposure, with Financials and Health Care making up the largest weighting at 17% each. However, the fund’s relatively high weighting towards micro-cap stocks makes the ETF particularly risky.

Contracting Range Suggests A Breakout Is Near

The IWM is closing in on down trendline resistance from the October 2022 high which currently comes in at around USD185. A break above here would be a major technically bullish sign, targeting a move up to the USD225 area. Failure to overcome this hurdle however would put the focus back on the downside and at the USD170 level. Below here would put the emphases clearly to the downside and on horizontal support around USD163. Below here would target a move all the way down to the USD120 area.

IWM ETF Price (Bloomberg)

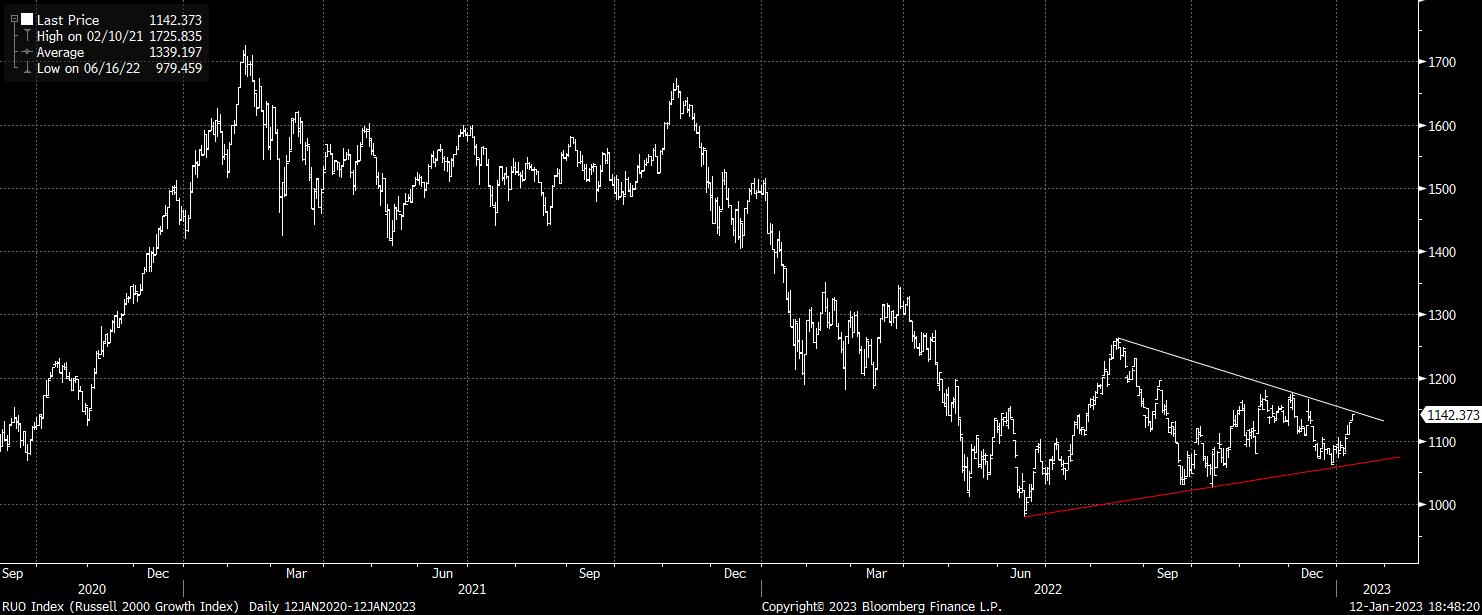

The contracting range pattern is even clearer in the Russell 2000 Growth index as seen below. The growth component of the IWM has been the major cause of the weakness seen since the peak, with the Russell 2000 Growth index still down 34% from its 2021 peak, and the IWM will likely continue to be driven predominantly by its performance.

Russell 2000 Growth Index (Bloomberg)

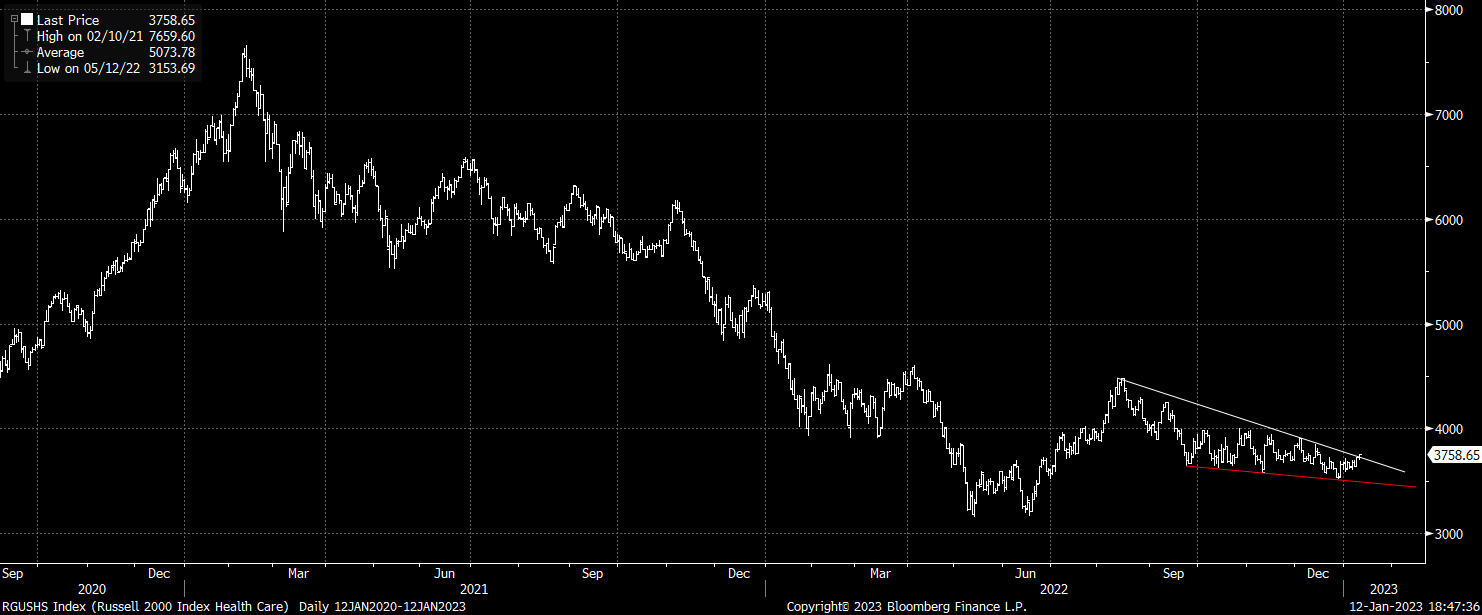

As one of the highest weighted sectors in the index, the Health Care sector is also a key driver of the IWM, and the chart is looking very bullish. The index appears to be mounting an upside break of the wedge formation that has been in place since August 2022. The reaction to today’s CPI could be a key determinant of price action over the coming months.

Russell 2000 Health Care (Bloomberg)

Valuations Suggest The IWM Remains A Poor Investment At These Valuations

While there is potential for an upside reversal in the IWM in the near term, the long-term outlook remains poor as valuations remain elevated. The Russell 2000 trades at a PE ratio of 50x when loss-making companies are included in the calculation, which is incredible considering the decline already seen from the peak. Because of the volatility of earnings in the small cap sector, I prefer to use the price-to-peak earnings ratio, which strips out temporary declines in earnings. This figure sits at 40x, which is still above its 2000 and 2007 peaks. Even the forward PE ratio, at 21.8x, is still high from a historical and global perspective.

Even if we focus on earnings excluding interest, tax, depreciation, and amortization, the Russell 2000 is by no means cheap. The EV/EBITDA ratio sits at 13.0x, and while this is down significantly from its peak, it remains on par with the S&P500, which itself remains deeply overvalued (see ‘SPX: Bear Market Is A Long Way From Over‘).

Summary

The IWM looks set for a big move in the near term after trading in a contracting range for several months, and a bullish near-term break would likely suggest further upside over the coming months. The performance of the Health Care sector and Growth stocks will be key in this regard, and the risks appear weighted to the upside. However, from a long-term perspective, the Russell 2000 remains a poor investment at these valuations.

Be the first to comment