Don Farrall/DigitalVision via Getty Images

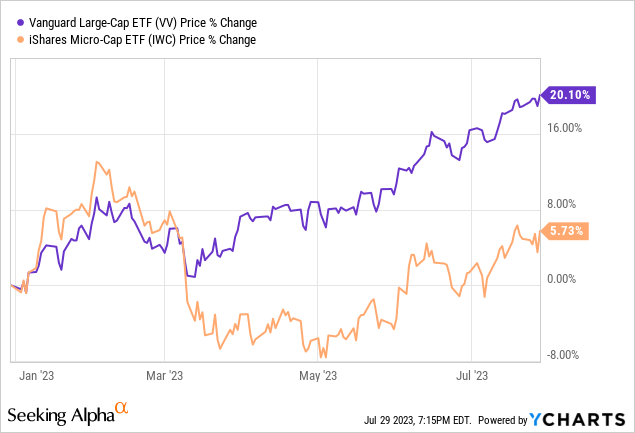

iShares Micro-Cap ETF (NYSEARCA:IWC) is an ETF that focuses on the smallest stocks in the market. The fund holds slightly more than 1,500 such stocks. There is no universally agreed market cap cut off for “micro cap” but most definitions set the cut off around $200-300 million range. Micro caps can include many different types of companies from small regional companies to start ups or biotech companies that are still in testing stage. It can also include a lot of pre-revenue companies. As a matter of fact, healthcare companies claim 25% of IWC’s total weight and most of these are biotech companies without a product in the market yet. Many of these companies are such bets that they could either become “10 baggers” or go bust but considering that the fund has hundreds of such stocks, it likely won’t suffer too much from some of its bets going bust.

IWC sector distribution (iShares)

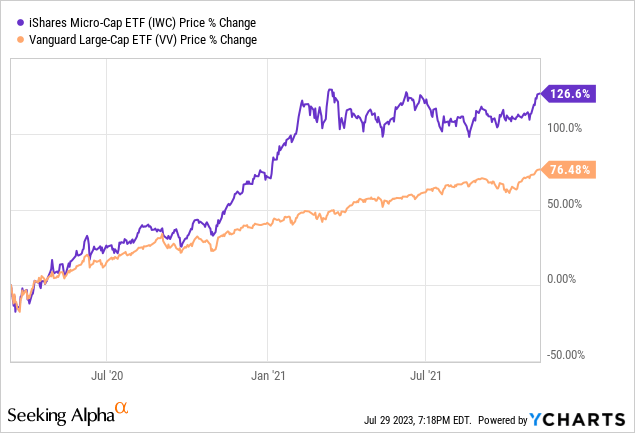

It is generally believed that micro cap stocks underperform during bear markets and more volatile times and they outperform during secular bull markets. They tend to underperform during difficult times because they have less access to capital, less resources to withstand big storms and less flexibility to survive. They are thought to outperform during secular bull markets because they have more room to grow and they typically start out with lower valuations. For example, at the end of last year the average micro cap stock had a P/E of 7 after a year-long brutal bear market. I still don’t fully agree with the idea that micro caps outperform during bull markets though. While it is true that they sometimes outperform under certain circumstances, there are also many times where people crowd into large caps and mega caps where stocks with lower caps underperform even though we might be in a bull market. This year is a good example of that where large caps are up 20% year to date while micro caps were up only 6% so far. As a matter of fact, micro cap stocks were actually down year to date up until the end of June as you can see below.

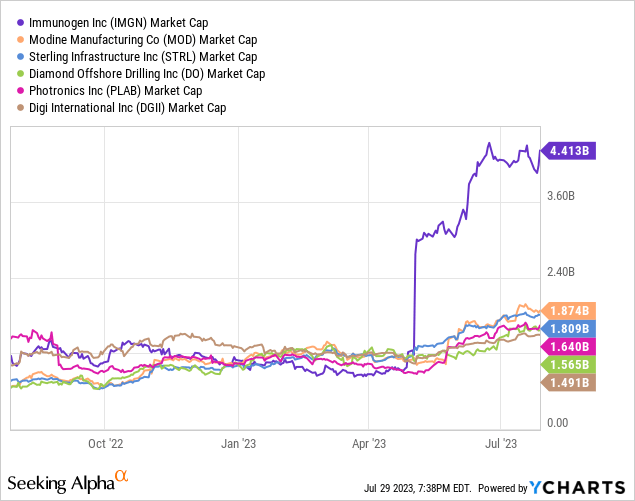

Then there are periods like the period between March 2020 and November 2021 where micro caps significantly outperformed. In order to micro caps to outperform you need not only a secular bull market but also a risk appetite for smaller stocks. If everyone is crowding into the same mega caps and there is little appetite for small and micro caps, a mere existence of a bull market can only help them so much. Since micro caps don’t have as many resources and as much access to money as large caps, they tend to perform better when money base is expanding and the Fed is highly accommodative. When the Fed is cutting rates and running a QE (quantitative easing), small caps and micro caps tend to do very well but they tend to struggle when the Fed has a monetary policy like today’s policy where it is hiking rates and running a QT (quantitative tightening) program.

Another factor to consider is that the fund is overweight in financial stocks and this mostly means regional banks since they fit the bill of “micro cap” stocks for the most part. A few months ago we saw several regional banks go bust but most of them had rather larger market caps in multiple billions such as Silicon Valley Bank, Signature Bank and First Republic Bank. It looks like smaller regional banks took less risks and they were less conservative and we haven’t heard many of them going bust so far. It doesn’t mean they can never go bust but so far things haven’t looked too bad for them. In the event of a real credit crunch like what we saw in 2008-2009, many smaller banks could still face serious risk and investors should be aware of that since this fund is overweight in smaller banks.

Another thing I found interesting about this fund is that even though it is a micro-cap fund, it still holds some stocks that aren’t exactly micro cap. Below are some examples of such stocks. It is entirely possible that these funds were micro caps when they were purchased by the fund but they are no longer micro caps after rallying significantly over time. This is not necessarily something good or bad but just something to be aware of for investors especially if they were looking for a fund that purely owns micro cap stocks only.

One issue that follows many funds that exclusively own small or micro-cap stocks is what I call “graduation” risk. This happens when a small cap stock is so successful that it rallies hard and graduates from a small cap and moves onto become a mid-cap stock. Many funds that own exclusively small caps or micro caps have to sell such stocks that don’t fit their criteria anymore. This allows these funds to underperform over time because they sell their winners and hold companies that aren’t exactly outperformers. They can also hold a lot of companies that are failing where the company’s stock got “relegated” from large cap or mid-cap to small cap due to bad performance. This might result in small cap and micro-cap funds having a lot of loser stocks and fewer winner stocks. As a result, this will cap future performance of such funds. The fact that this fund holds several stocks with market caps above $1 billion tells me that this fund might not suffer from this issue as much.

Ideally speaking, the best time to invest into this fund would be when the Fed finishes hiking rates, starts cutting rates and initiates a more loose money policy. When printers start “printing money”, small caps and micro caps do better because many of them depend on liquidity to survive and thrive. They also like low-inflation environments because micro cap companies don’t have as much pricing power as large companies so they can’t easily pass higher costs to customers without losing customers. This is why they don’t perform well during inflationary periods but perform much better when inflation rate is low.

Having said that, we also know that markets are forward looking and they will likely start pricing in a loose money policy about 6-7 months before it happens so if you feel that the Fed will have a looser money policy in the next 6-12 months, this might be a good time to start buying funds like IWC.

Be the first to comment