baona

U.K.-based fuel cell developer ITM Power (OTCPK:ITMPF) has form in disappointing investors, and its latest profit warning is no exception. However, it may be that this is something of an air clearing exercise by new management, paving the way for more realistic expectations ahead: if so, that could turn out to be good news for the investment case.

I am still not persuaded by the risk to reward ratio here, even after a steep fall in the share price. My most recent piece was last April (ITM Power: Growing Revenues Don’t Justify Share Price) in which I was bearish. Since its publication, the shares have fallen 72%, but I remain bearish and continue to rate the shares as a “sell”.

Profit warning

The company announced last month that its longstanding chief executive would resign with immediate effect. He was to be replaced immediately by a new CEO whose appointment had been announced only days earlier and was coming from Linde Engineering, with which ITM has a strategic relationship.

On 16 January, the company issued an unscheduled trading statement. It said that a detailed operational review is ongoing, but that already, “it has become clear that the outcome for the financial year ending 30 April 2023 will be materially different from the current guidance, with lower revenue and a higher EBITDA loss.”

The interim results are scheduled for 31 January, and the company said in this week’s announcement that they will include further guidance and a strategic 12-month priorities plan. That is anticipated to cover three areas: product portfolio, testing capabilities and automation and capital allocation/expenditure.

It sounds as if the new boss has got his feet firmly under the desk and is trying to knock ITM’s strategy into shape, including taking a disciplined approach to its finances. In itself, this is positive (if not long overdue). However, talking a good strategic fight while lowering financial expectations in the first few weeks of the job is the easy part. What matters is how this plan is delivered. A decent strategic plan at the end of the month could boost investor sentiment and the share price, albeit any uplift may be countered by scepticism if the new financial outlook is worse than expected. However, I see a decent chance that there could be a bump in the share price after the announcement later this month.

What matters, I think, is what happens in the longer term when it comes to putting any such plan into action. On this, I think, the jury is out. The new chief executive is unproven, and the commercial model has not yet shown itself to be worthwhile.

With small revenues (£5.6m last year) and heavy losses, I think investing in ITM remains a punt on the firm’s technology rather than in its commercial model.

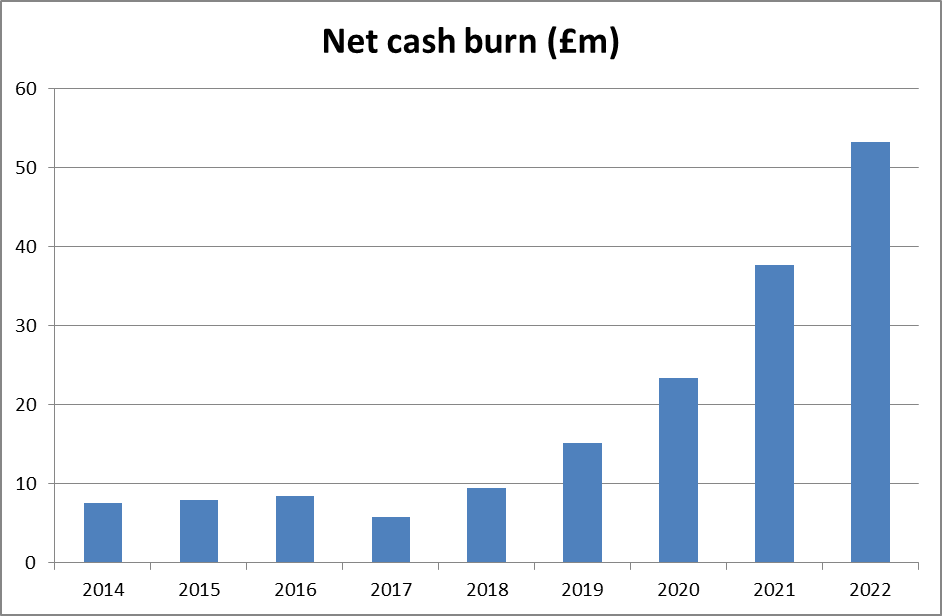

Strong liquidity as cash burn mounts

The announcement emphasised the strength of the balance sheet, with net cash as at 30 October 2022 of £318m. Compared to the current market cap of £563m, that is a substantial amount.

Although that cash pile looks large enough to meet the company’s liquidity needs in the next few years, it is worth noting that the company’s cash burn has soared in recent years.

Chart compiled by author using data from company annual reports.

ITM Power calculates net cash burn by deducting from annual cash flow the effects of any equity fund raise after costs.

That raises the possibility of further fundraising at some point, diluting existing shareholdings.

Valuation Continues to Look Stretched

Setting aside the cash pile, the company has an enterprise value of around $300m.

That is a lot less than it was, reflecting the steep share price fall in the past two years. But is the prospect of a healthier business if ITM can refine its commercial model and achieve scale worth $300m? I do not think so, relative to the risks involved. There is simply too little proven success to date to justify such a valuation, in my view.

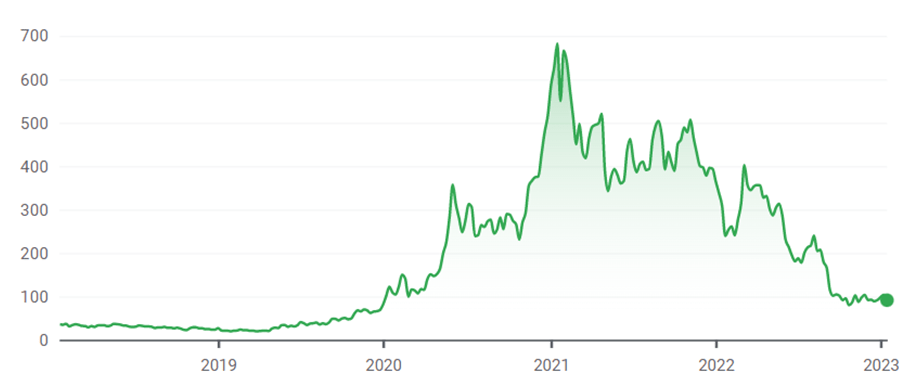

(y-axis shows share price in pence) (Google Finance)

Nonetheless, at this stage, I continue to see ITM Power shares as overvalued for the company as judged on its current prospects.

2023 is set to be an important year, with a new strategic focus. That could mean that the share price climbs up from here. I consider that as speculative, though, and I see sizeable execution risks. The company has yet to prove that it has a workable, profitable business model, more than two decades into its existence.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment