Dilok Klaisataporn

The Investment Thesis

Cigna Corporation (NYSE:CI) is a company operating in the United States in the healthcare industry. Here it provides customers with insurance and other healthcare-related products. One of their largest segments is called Evernorth. Here the focus lies on offering point solution health services as well as benefits management and care delivery. Besides this, they have a broader segment called Cigna Healthcare. Here they have a diversified list of different services, like dental, vision, or pharmacy. The company has grown vastly in the last few years and is now one of the largest in the country.

I think that Cigna Corporation will continue growing in the industry and provide investors with incredible value as they remain to have a strong cash flow. This all leads me to have a buy rating as they are trading well below the sector average multiple too.

Last Earnings Report Highlights

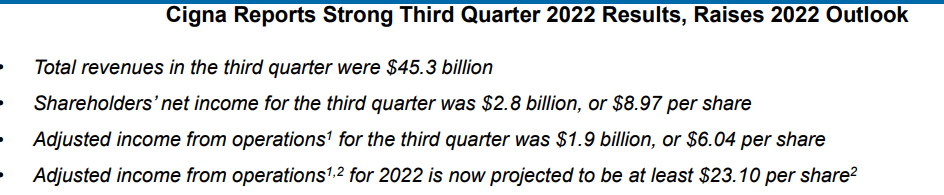

In the latest earnings report by Cigna, they had investors pleased. The revenues came in at an impressive $45 billion. This is pretty close to half their current market cap right now. For the TTM the company has generated over $190 billion in revenues which puts them at a P/S ratio of just 0.55. That should be enough to grab anyone’s attention.

Earnings Highlights (Q3 Earnings Report)

The shareholder’s net income came in at just over $2.8 billion, which meant the company achieved a net margin of 4.1%. To me, this is a very good sign as it means the TTM net margin keeps increasing for the company.

TTM Net Margin (Seeking Alpha)

The management seemed to remain optimistic and proud of their achievements so far in 2022. The CEO David M. Cordani can be quoted saying “We built on our momentum from the first half of 2022 with strong execution in the third quarter across our businesses and a continued focus on serving customers and clients with our differentiated health and well-being solutions’ ‘.

The company said that they now expect the full-year EPS to be at least $23.1 per share. Which would put the company at a p/e of just 13.

Sector Outlook

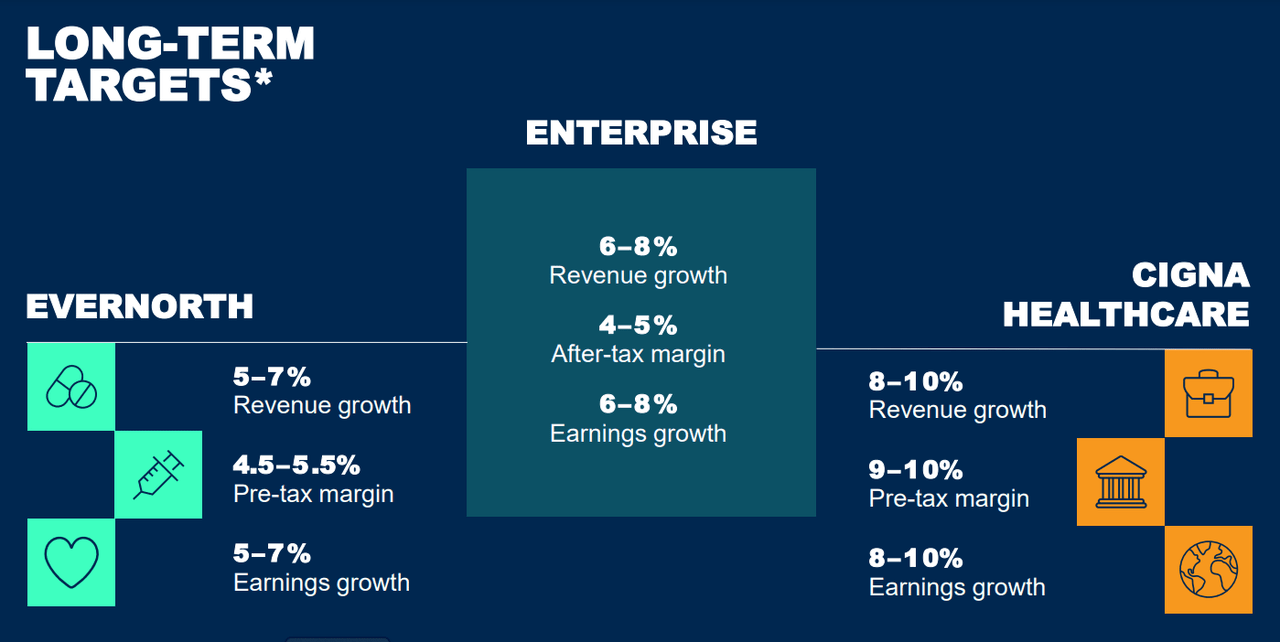

Cigna has a long history of growth and has since 2010 achieved an EPS growth of 15% YoY. Looking ahead this momentum can definitely be kept up as the healthcare market is expected to continue to flourish. The company itself remains optimistic about its ability to grow with the sector and provide long-term value for investors.

Company Prioritize (Investor Presentation)

With a heavier focus on increasing the bottom line and in turn having more cash flow available, they will be able to keep a generous dividend and steady EPS growth. In their latest earnings report the management seems very focused on buying back shares. Stating that around $10 billion would be set aside between 2022-2026 for share repurchases.

Competition

Given that Cigna Corporation is a health insurance company there are many larger players in the sector all fighting for their share of the pie. Some of the notable competitors the company faces are Elevance Health (ELV) and Humana (HUM).

What I think gives Cigna a little bit of edge is that it’s trading at a very low P/S ratio of just 0.55. I think this could potentially give investors more incentive to go with Cigna as the upside is higher. What Cigna will need to improve, however, is the free cash flow. Elevance Health is beating out slightly though as the expected EPS growth for the next several years would be higher. Until 2027, it would be 14.6% YoY whilst Cigna is expected to achieve 9.5%. It will be very important to see how these companies manage to buy back shares and also offer a sustainable but high dividend, all aspects that would attract investors.

The Balance Sheet

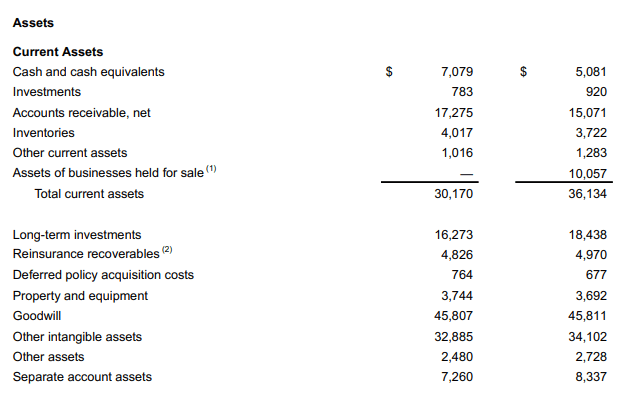

The balance sheet of Cigna is a joy to read. They have managed to both build up a bigger cash position whilst also paying down more debt. Right now the company holds just over $7 billion in cash. It has increased by 40% compared to 2021. I think this is a very healthy step for the company to go in as it will greatly help them as the economic challenges start to amount with higher interest rates and demands for higher wages too.

Balance Sheet (Q3 Earnings Report)

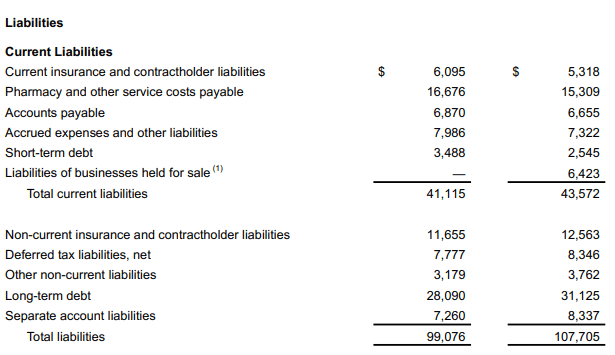

Looking at the debt, they have short-term debts of $3.4 billion and $28 billion in long-term debt. I think that there is no risk of them defaulting on debt any time soon as their free cash flow is so strong. With over $9 billion of it in the last 12 months. This will help the company be able to pay off any current liabilities whilst also building a strong cash position and any remaining money will be distributed to shareholders via repurchases or dividends.

Balance Sheet (Q3 Earnings Report)

The assets have seen a decline YoY but not as fast as the liabilities have decreased. Which to me is a very good sign they are heading in the right direction and the financial priorities are where they should be.

Cash Flow History (Seeking Alpha)

I mentioned before that the cash flow the company has is incredibly strong. As the company matures more and more, this point becomes important as investors want to extract as much value as possible from their investors. I think the management will be able to sustain this growth, which will give even more incentive for investors to buy into the company.

Outstanding Shares (Seeking Alpha)

With such a strong cash flow the risk for share dilution is in my opinion close to zero. The company has in the last years bought back large amounts of outstanding shares and will continue to do so. Until 2026 the company expects to have around $30 billion in cash available to share repurchases as they focus more and more on giving value back to shareholders.

Valuing The Company

One of my favorite segments in reading and researching a company is valuing it to have an idea of the potential return on investment could make. Cigna Corporation carries a lot of potential with it in terms of opening a long-term position.

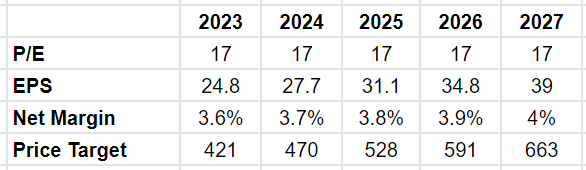

Future Valuations (Author’s Own Calculations)

You might see straight away that the current share price the company has is quite a bit below my estimates. I think they are undervalued and have great potential to provide long-term investment appreciation. During these 5 years, I am forecasting the annual growth to be around 11.4%. This doesn’t include potential dividends, which the company has made clear is a priority. This number will most likely also be boosted by the company promising to buy back a substantial amount of shares. Further boosting investor value.

A p/e of 17 I think is a fair valuation to have. It’s slightly below the sector average of 19. A conservative valuation is often better to provide more upside if there is some, but also protects against potential downside risk.

As the health insurance market has a bright future ahead with continued growth, I believe Cigna will be able to pass on quite a lot of costs to their members and therefore maintain a good net margin.

All in all, I think at the current price Cigna offers a great entry point for investors and this is why I have it as a buy now.

Conclusion

Cigna Corporation is a massive health insurance company with a price/sale ratio of just about 0.55. With TTM revenues of $190 billion, they have a massive market share and will most likely continue to grow along with the industry. Seeing more members sign up each quarter gives me further confidence in the company.

With incredibly strong free cash flows the management is very openly positive towards returning as much as possible to investors by either buying back large amounts of shares or distributing it through dividends.

This all accumulates to me having a buy rating for the company. The long-term outlook looks strong and I think Cigna would be a great stable addition to any portfolio.

Be the first to comment