metamorworks/iStock via Getty Images

On the fourth of January this year, we took a position in Iteris (NASDAQ:ITI), a market-leading company in the smart mobility market, for our marketplace at $2.95 a share.

With hindsight, we wished we had bought more but it was our first endeavor in this name and it always takes several efforts to get our confidence levels up. Still, despite the strong rally, we don’t think the shares are done for the year, we still see plenty of upside.

The company operates on an asset-light business model (CapEx is less than 1% of revenue) and generates recurring revenue from two sources, managed services and their SaaS platform, together good for 23% of revenue.

After the Q3/22 results we continue to be bullish on the shares and we’re very bullish on the shares.

- Booming market, record backlog

- Product leadership, taking market share

- Asset-light, business model generating recurring revenues

- New products

- Lapping $15M of FY22 cost will put the company in the black and generate cash.

Product leadership

We have dealt with the first two in greater detail in our previous article but nothing has really changed quite the contrary.

Product revenue grew a whopping 44%, with backlog setting another record, increasing another 22% at $112.2M, and net bookings in Q3 of $41.1M

The company is obviously gaining market share and they keep on winning (Q3CC):

virtually every large competitively sourced detection sensor, fixed travel time sensor and cellular CV2X sensor initiatives across the country

The market is getting a boost from the IIJA (Infrastructure Investment and Jobs Act), which helped the company receive a Notice of Intent to Award a multi-year, multi-element contract from a public agency in Southern California.

That’s a large project and will take a couple of quarters to finish the final contract, but the bigger point is here that the IIJA is starting to pay off for the company.

The company is on the technological front end, having developed four generations of sensors. The latest two, AI-powered Apex and Fusion are still in the very early innings with only small sales and it will take time to ramp.

Their recently introduced roadside unit made up about 10-20% of sensor revenue. It’s very early days, but management believes that in five years it can have a $1B TAM.

It’s not just being on the front end of technology that wins the company so many orders and takes market share. Management argues that domain expertise is crucial (Q3CC):

And so understanding how people operate these sensors and what kinds of information they need out of it has allowed us to build product that meets the needs of the customers. And then we supplement that with, we think, the best field support in the industry. So I think, again, I mean, just generally, people are like, wow, this does exactly what I need, whereas I don’t see this from other vendors. But there’s a lot that goes into that, right? I mean it sounds easy, but there’s a lot of work on the back end.

Recurring revenues

ARR stands at 23% of revenue and consists of their SaaS and DaaS platforms and managed services. The company is set to increase it as the newer sensors have higher attach rates (Q3CC):

we’re attaching annual recurring revenue to each new Vantage Apex system and sense Spectra CV sensor has occurred with the CVAG and Florida orders… our desire is to attach annual recurring revenue or cloud revenue to every sensor sale, every professional services engagement that we have but that can occasionally slow things down but they have developed a secret sales technique recently to get this done

Management was coy about this secret sales technique, so we’ll have to see how it performs. There was some noise from a substantial 700bp gross margin decline for services on a high percentage of subcontract revenue (which gathers lower margins) and the change in contracts with data providers that produce a short-term hit for longer-term gains (once the company gets over a threshold).

They are also introducing strategic price increases for certain of their SaaS services.

Cost

Q3/22 is the inflection point with respect to their supply chain problems, which have two dimensions:

- The added cost of ordering scarce parts on secondary markets.

- The added cost of designing new circuit boards reduces the dependence on these scarce and/or expensive parts.

On the first, in Q3 only $970K was spent on the secondary market, down from $8.4M in Q2 and it is projected to decrease further to less than $600K in Q4.

The company finished the design of 4 additional circuit boards in Q3 taking the total to 6, the related hit to COGS decreased to $3.9M in Q3, from $7.8M in Q2.

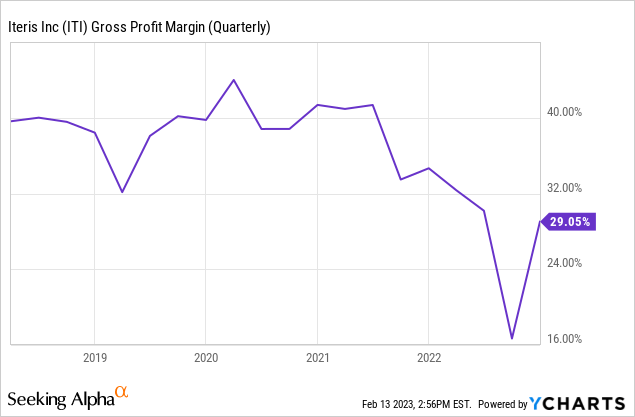

All in all, by Q4 most of these costs are done and product gross margin will recover to 40%+ in Q4 (from 30.1% in Q3 and 20.6% YTD).

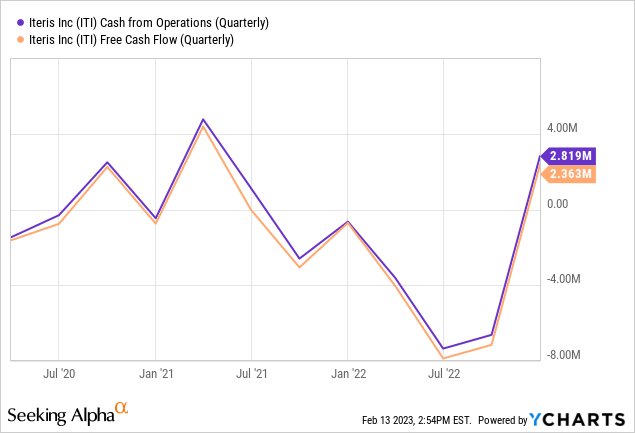

Next year some $15M of these costs will lap out, giving profitability and cash generation a big boost. In fact, cash already moved into the black in Q3 (to $10.2M) and there will be another $2M-$4M added in Q4.

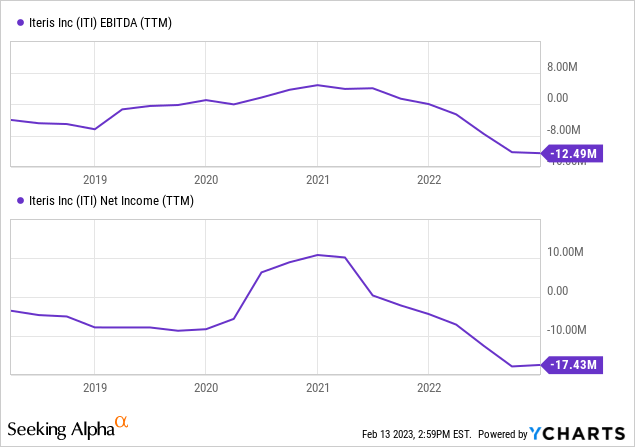

Gross margins took a hit from the pandemic and supply chain problems but are on the way back and will recover to normal levels in Q4:

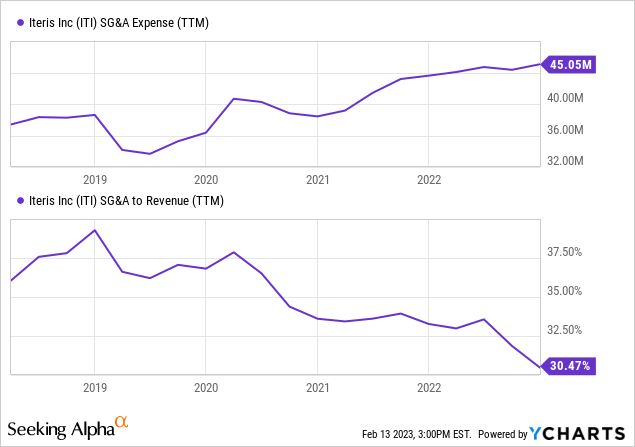

There is also a considerable degree of operational leverage:

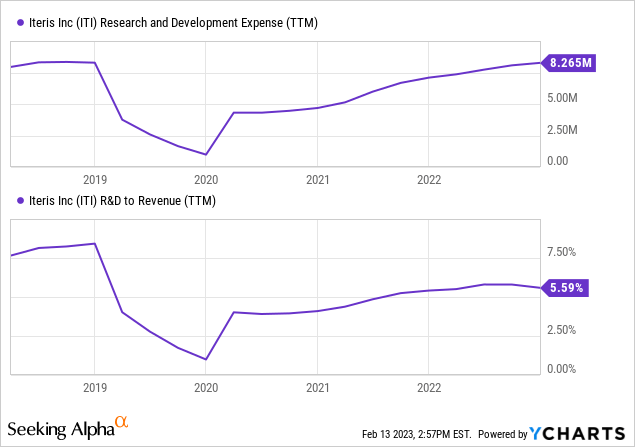

Although R&D roughly grows with revenue but is a much smaller component:

It is not surprising, the company is moving at the cutting edge of the industry and this takes considerable investments in R&D.

Management was so consumed with the supply chain problems and designing alternative circuit boards that the focus on M&A was almost entirely lost, but with the supply chain problems largely resolved and cash starting to come into the company’s accounts again, management will be looking for financially viable acquisitions next year again.

Valuation

According to analysts, loss in FY23 (ending in March) will be 17 cents per share but in FY24 (starting in two months) the company will swing back into profits with an EPS of $0.29.

There are 42.8M shares outstanding and 6.35M options and 500K RSU for a fully diluted 49.6M shares with a market cap (at $4.50 per share) of $223M.

The company has $10.2M in cash and no debt for an EV of $213M on an estimated FY23 revenue of $153M (midpoint guidance) and a FY24 revenue of $170M (average analyst expectations, which seems low to us) for an EV/S of 1.25x.

We still see ample room for valuation multiple expansion at these levels, an EV/S of 1.25x for a company that generates gross margins of 40%+ on its products.

Risk

We see little in the way of competitive risks at the moment as the company produces market-leading sensors, but it’s always possible a better-capitalized company emerges.

Management argues that the supply chain problems are easing and gross margin and cash burn have already improved significantly (cash flow was already positive in Q3).

Still, one can’t exclude the possibility that this is too optimistic a view or that there will be a relapse of these problems. Still, with $10M+ in cash and no debt the company should be able to withstand the most severe downturns.

The macro-environment could deteriorate but we think there is a counterbalance from the infrastructure bill as funding of projects is only in the very early innings.

Conclusion

There is plenty to like:

- Secular tailwind from an expanding market

- Asset-light business model generating substantial recurring revenues

- Dominant market position at the cutting edge of technology and solutions, taking market share

- Margins recovering from supply chain problems

- Considerable operational leverage in the business model

- Despite the recent strong rally valuation multiples are still modest

The obvious risk is a substantial deterioration in the economy, but so far that’s not happening and demand for the company’s solutions remains strong.

Be the first to comment