REIT, Real Estate Investment Trust Maxxa_Satori/iStock via Getty Images

ETF Overview

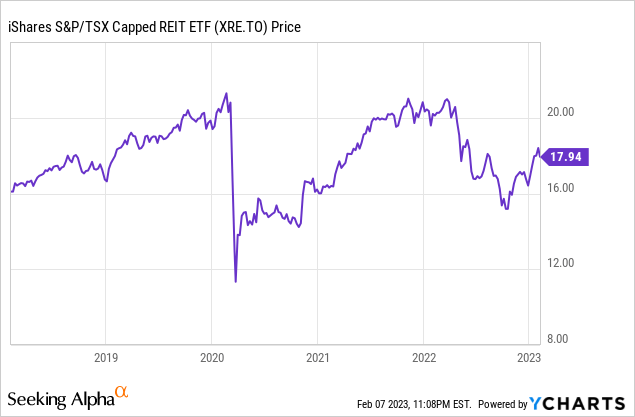

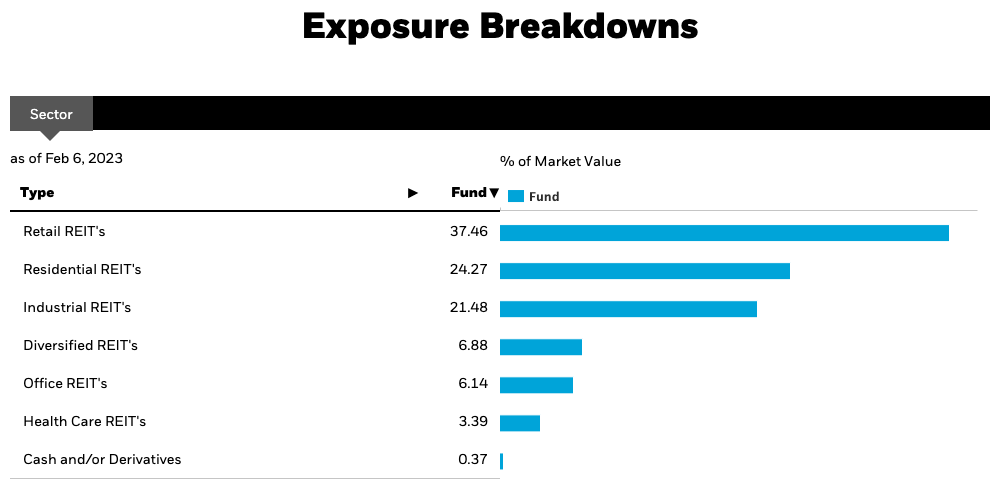

iShares S&P/TSX Capped REIT Index ETF (XRE:CA) (“XRE”) invests in Canada’s real estate investment trusts (“REITs”). The REIT has a high exposure to cyclical subsectors. In fact, retail, industrial and office REITs consists of nearly two-thirds of XRE’s portfolio. REITs in XRE’s portfolio will continue to face challenging macroeconomic conditions. Rising interest expenses will also be a problem. Investors may want to wait for more certainty before jumping in.

YCharts

Fund Analysis

XRE has a high exposure to cyclical sectors

Let us do some analysis on XRE. First, we will take a look at XRE’s portfolio. As the table below shows, XRE has a high exposure to cyclical subsectors such as retail, industrial, and office REITs. These three represent nearly two-thirds of the total portfolio. While retail REITs benefited from the reopening of the economy in 2022 and that occupancy ratios have improved considerably in the past year, this subsector is not immune in an economic recession. Demand for industrial REITs also remained strong in the past year, but many major online retailers have scaled back their capital spending as they have overspent during the pandemic to expand their logistics.

The Office REITs segment is probably the most uncertain of the 3, as the future working environment is likely going to be one of hybrid arrangements, and hence demand for office spaces will likely remain weak. Fortunately, office REITs only represent about 6.14% of XRE’s total portfolio.

iShares Website

An economic recession is likely not too far away

XRE’s high exposure to cyclical subsectors will be positive if the economy is growing and expanding. Unfortunately, the economy appears to be weakening. The rapidly rise of interest rate of 425 basis points in Canada in 2022 has caused a slowdown in economic activities in Canada. Although unemployment rate has ticked lower from about 6% in early 2022 to just under 5% towards the end of the year, the total hours worked decreased in December. This is an early sign of demand softening as businesses usually cut hours worked first, before moving to cut jobs. A softening economy cannot be interpreted as good news in the real estate rental market as occupancy rate growth may soon be reversed into occupancy rate decline.

Interest rates may stay elevated for a while

The 425 basis points hike in interest rate in Canada over the last year is having a ripple effect in the real estate market. REITs of all subsectors will be impacted negatively, as a significant portion of their operating expense is interest expense. While Bank of Canada has indicated that it will pause its rate hikes and play a wait and see approach, the bank is not prepared to lower interests rate any time soon due to still-elevated inflation.

We think the bank needs to keep the rate elevated for a while in order to make sure inflation really drops to the 2% target. Therefore, we think REIT operating incomes will be impacted negatively in the near-term. Soon or later, these REITs will have to refinance their mortgages with higher interest rates.

Should you buy XRE right now?

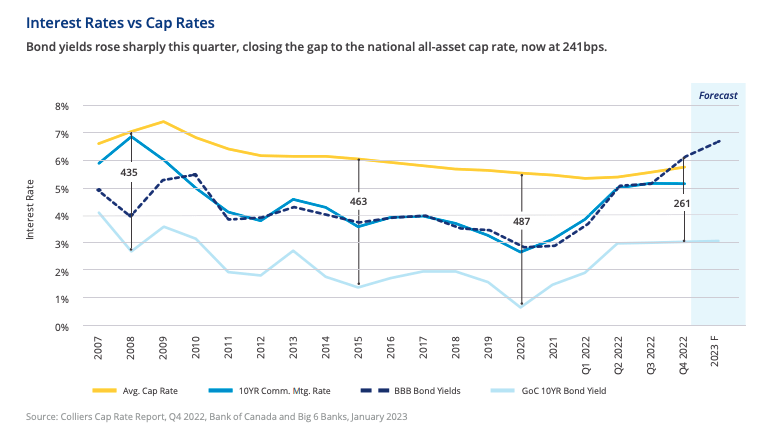

Share prices of REITs are sensitive to the rate changes. The rapid rate increase in the past year has resulted in valuation compression in most REITs. XRE’s share price has also fallen by about 15.5% in the past year. The chart below shows the impact of interest rates and capitalization rates in Canada since 2007. Capitalization rate is typically used to calculate the net asset value of a property. Hence, it is a good measure to calculate a REIT’s net asset value per share. As cap rate moves up, the net asset value will go down and vice versa.

Colliers Cap Rate Report, Q4 2022

As can be seen from the chart above, average cap rate in Canada is generally several percentage points higher than Government of Canada’s 10 year bond yield. This is because GoC’s bond is considered risk free. To compensate the risk for investors to invest in real estates, the cap rate needs to be higher. As can be seen from the chart above, in average, the spread is in the range of 350 basis points to 500 basis points since 2007. However, in Q4 2022, the spread is only 261 basis points. This is the lowest level we have seen in the past 15 years and we think the spread will eventually need to return to the range of 350 ~ 500 basis points.

Therefore, either the cap rate will need to move higher, or the bond yield will need to move lower. If the former is the case, the net asset value will need to move lower, suggesting that there will be more decline to go in REIT’s share price. We hold the view that the Bank of Canada will not lower interest rate too soon, as it needs to stand firm to make sure inflation really moves down to its target of 2%. Therefore, we believe there is still more room for REITs net asset values to drop. Hence, we do not think it is a good time to buy XRE right now.

Investor Takeaway

XRE has a high exposure to cyclical subsectors. This makes it a good investment vehicle in an era of economic boom. However, given the economic uncertainty, elevated inflation, and high interest expenses, we believe it is still too early to jump to invest in XRE right now. Hence, we think investors may want to stay on the sideline. A pullback will provide a more attractive buying opportunity.

Be the first to comment