violinconcertono3/iStock Editorial via Getty Images

State Street Corp (NYSE:STT) has had a year to forget with shares off nearly 40% from highs in early January. The bank’s performance as an asset manager is seen as tied to trends in capital markets as a key driver of its fee-based revenues. Simply put, lower equity market values pressure management fees while client activity also suffers. That being said, our message here is that State Street remains a high-quality leader with a positive long-term outlook.

The bank successfully passed the Fed’s annual stress test with a projected minimum common equity tier 1 capital ratio (CET1) of 13.2% above the 12.4% average among 34 large banks tested by the Fed under a severe recessionary scenario. In other words, State Street is seen as having a strong balance sheet with resilient fundamentals. With the result, the bank announced its latest dividend hike, planning to increase the quarterly rate by 10% and opening the door for share repurchases. Recognizing the challenging macro environment, we are bullish on STT which is well-positioned to recover with the stock offering compelling value at the current level.

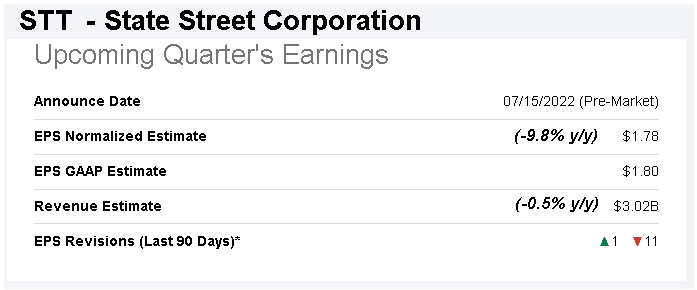

STT Q2 Earnings Preview

State Street is set to report its Q2 earnings on Wednesday, July 15th. According to consensus, the forecast is for revenue of $3.0 billion down -0.5% compared to Q2 2022 while the headline EPS estimate of $1.78 if confirmed, would be around -10% lower than the period last year. The setup here considers what was a record 2021 for the company benefiting from the early pandemic boom and strong equity market returns that now represent a tough comparison period.

Seeking Alpha

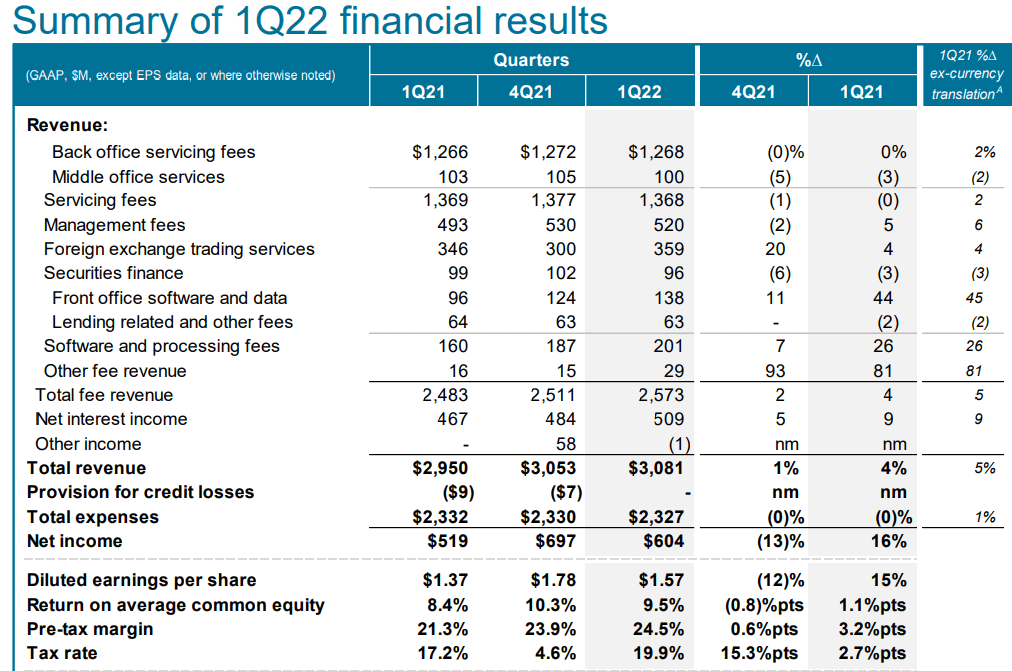

State Street is recognized for its large portfolio of exchange-traded products including the SPDR family of funds and S&P 500 Trust ETF (SPY). As the returns across most sectors have been poor this year, the result is that assets under management decline, translating directly into lower fees at the margin. For context, investment management represented approximately 25% of the business in Q1 which was already seeing weakness compared to Q4. On the other hand, the larger servicing business which includes asset custody services and fund administration is seen as less variable but also impacted by financial market trends.

Favorably, the one area of the business that should be strong this quarter is the net interest income that benefits from climbing rates. From the Q1 results, interest income was up 9% y/y reflecting higher market rates. The recent Fed rate hikes in Q2 coupled with higher deposit values and a larger loan portfolio can contribute positively to EPS this quarter.

The question in the Q2 report is how much organic growth and new business will be able to mitigate the near-term market headwinds. On the costs and expenses side, a monitoring point will be salaries and compensation levels amid what has been tight labor market conditions within financial services. In Q1, State Street noted some savings through its “footprint optimization” as it manages real estate with some hybrid work options for employees.

Overall, it’s fair to say that the expectations for this earnings report are low considering the stock price trading action. We’d also note that STT has seen 11 EPS revisions lower for this quarter compared to just one revision higher in the last 90 days. Our take is that an earnings beat on the EPS side is possible depending on how much financial momentum the bank was able to maintain from the trends last year.

source: company IR

When Will State Street Increase Their Dividend?

We mentioned State Street’s dividend hike. The company intends to distribute $0.63 per share in the third quarter. While this dividend has not been formally declared, the company has a relatively consistent schedule with the Q3 dividend featuring a record date on the first business day of October. This means that all investors on the books by around October 3rd should be eligible for the new dividend amount. We expect an official announcement with the upcoming Q2 earnings release which follows a similar pattern from last year.

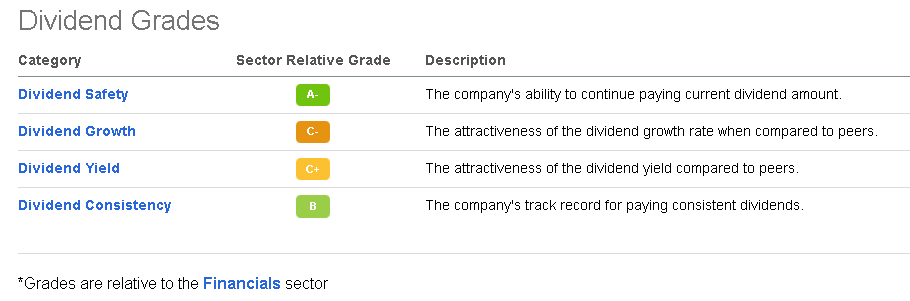

At the new dividend rate, the annualized amount of $2.52 represents a payout of approximately $925 million or roughly 33% of annual earnings. State Street earns an (A-) as a relative dividend safety grade according to Seeking Alpha’s Dividend Scorecard. All indications are that this dividend is safe for the foreseeable future, well supported by underlying cash flow and earnings.

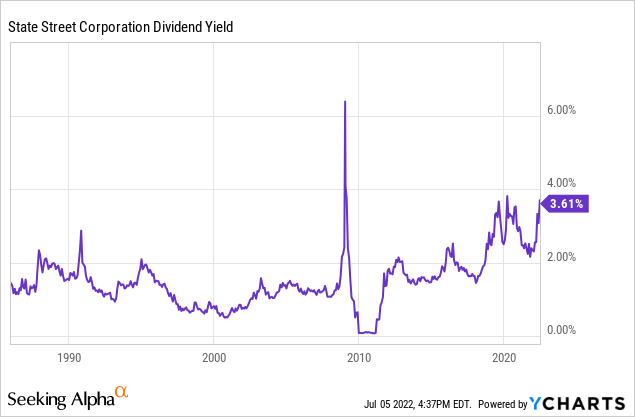

While the company’s dividend growth score at a (C-) is underwhelming, we expect this metric as well as the dividend yield score to climb once the latest dividend increase is incorporated. Notably, the forward yield on the stock at 4.0% is now well above the sector average closer to 3.2%, and even above the Financial Select Sector SPDR (XLF) at a modest 3.1%

Seeking Alpha

What Is State Street Stock’s Long-Term Forecast?

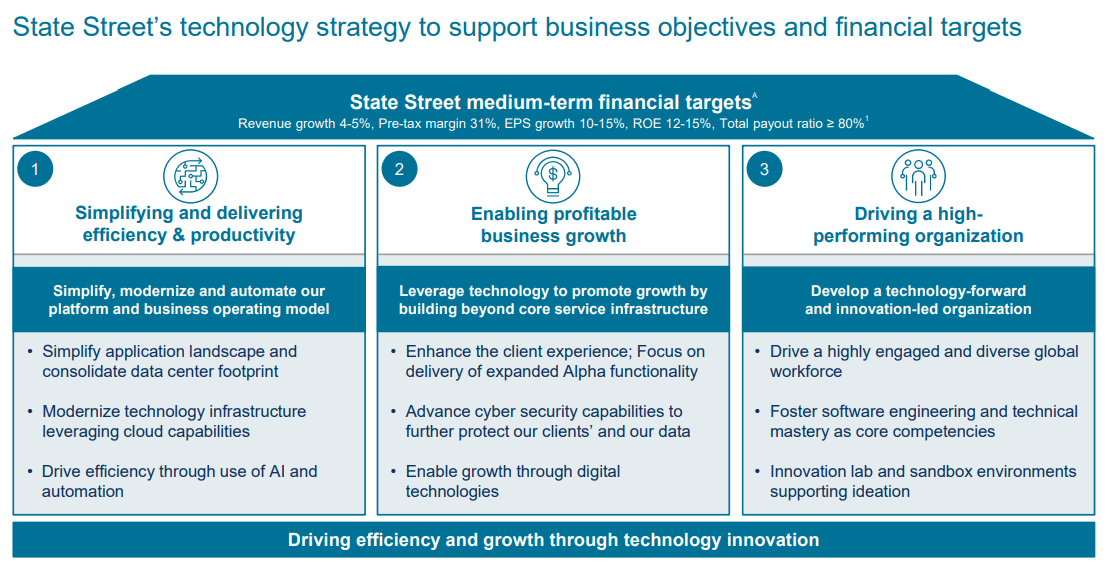

The attraction of State Street is the company’s ability to leverage its existing leadership position in several segments of financial services including asset servicing and financial custody to consolidate market share. Integrating new technologies adding to productivity and continued global expansion support long-term growth opportunities with upside to earnings and continued dividend growth. Anecdotally, the business can generate steadier growth compared to more traditional banks with concentrated exposure to volatile lending and credit risk. The stability of State Street’s diversified financial services is a strong point.

source: company IR

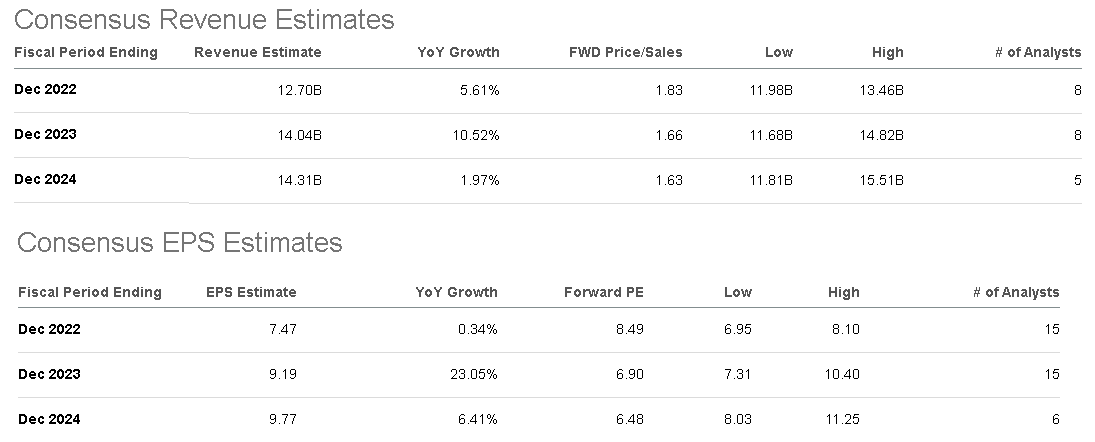

According to consensus, 2022 is shaping up to be a transition year with an EPS forecast of $7.47, roughly flat compared to 2021. The market expects revenue growth of 5.6% to $12.7 billion which also includes some continued operational momentum from new investing mandates. 2023 could be stronger with an outlook for revenues to climb 10.5% y/y while EPS accelerates towards $9.19. The trends here are in line with State Street’s financial targets expecting growth to average 4-5% per year while EPS is higher in the 10-15% range.

Seeking Alpha

The near-term outlook for State Street is going to depend on how macro conditions and the financial market environment evolve. If anyone has a view that the global economy is going to collapse or financial assets will decline significantly lower, State Street would probably be in trouble.

We’re keeping a more optimistic outlook with a sense that economic conditions will ultimately pass through what has been an admittedly rough patch. As covered in our recent article, an outlook for slowing inflation through the second half of the year can support a more stabilized economic outlook with improving sentiment towards risk assets. Shares of STT can recover.

Ideally, State Street would want to see financial market levels across sectors gain momentum and reclaim all-time highs. This would support higher assets under management across its portfolio of mutual funds and exchange-traded products contributing to more positive operating and earnings momentum.

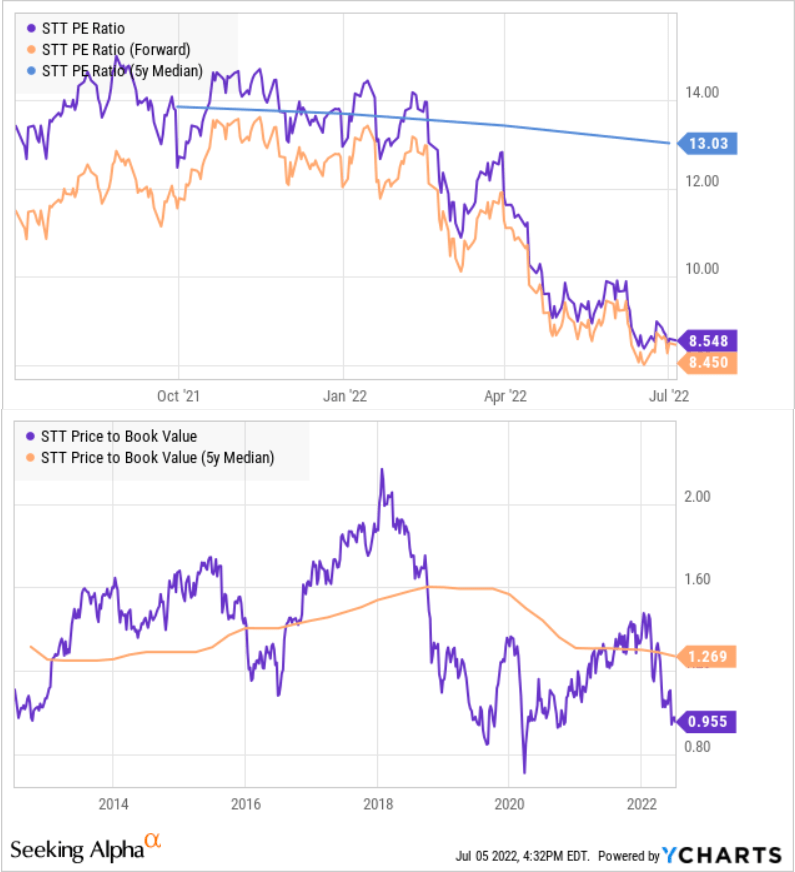

As it relates to valuation, two key metrics stand out as making STT particularly attractive. First, the stock is trading at a forward P/E of just 8.5x which is well below the 5-year average closer to 13x. Similarly, STT is trading at a price-to-book ratio under 1x which compares to an average of 1.3x since 2017.

source: YCharts

The depressed multiples here suggest the market is deeply pessimistic while our take is that the stock is simply undervalued. The forward dividend yield which we mentioned was at 4.0% is also at a historically wide level which further makes STT a compelling choice among large-cap financial stocks.

Is STT Stock A Buy, Sell, or Hold?

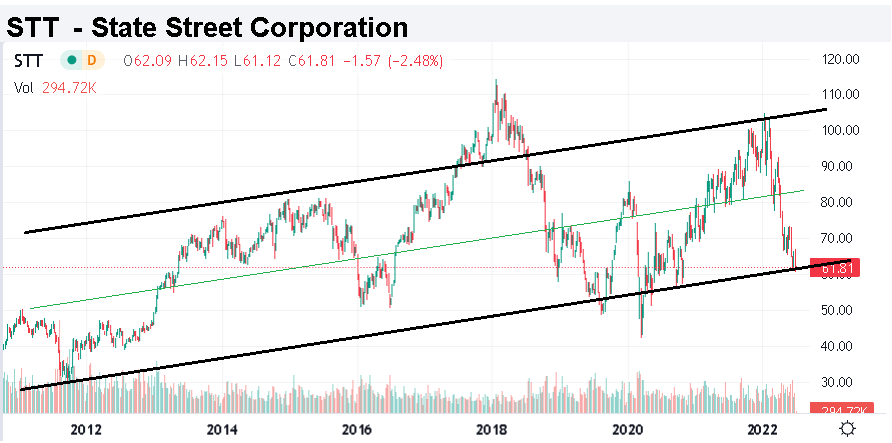

We rate STT as a buy with a price target for the year ahead at $80.00 representing an 11x multiple on the current consensus 2022 EPS. From the chart below, shares appear to be trading at an area of long-term technical support ahead of a potential rebound. Our price target also implies room for the forward dividend yield to narrow from 4.0% to 3.2%, converging toward the sector average.

The Q2 earnings report will be important to brush aside concerns of a deeper deterioration of operating and financial conditions. We expect management to highlight the strong points of the business. Longer-term, improving economic conditions can support shares trading significantly higher through a dynamic of valuation multiples expansion.

Seeking Alpha

Be the first to comment