Justin Sullivan/Getty Images News

Hasbro, Inc. (NASDAQ:HAS), together with its subsidiaries, operates as a play and entertainment company. In July 2022, we have published an article on Hasbro, titled: “Hasbro: It Is Not The Time For Playing“. Back then, we have rated the firm’s stock as a hold. The primary reasons for assigning a neutral rating to the firm were:

- Continuing demand for Hasbro’s products in the beginning of 2022

- Increasing costs

- Price multiples were indicating that the stock is trading at a premium compared to the respective sector median

- Dividend payout ratio appeared to be too high

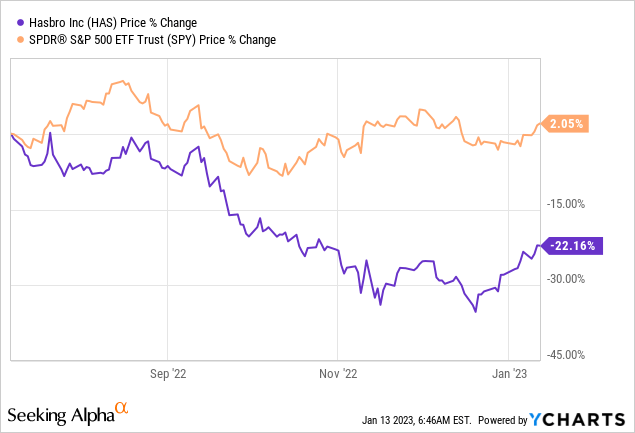

Since our writing, Hasbro’s stock price has declined by as much as 22%, while the broader market has gained about 2%.

As Hasbro is set to report earnings in early February, we decided to take a look at the company once again, and assess whether a potential buying opportunity could exist before the earnings release.

Let us start our discussion by looking at the development of consumer confidence in the past months and how it has influenced Hasbro’s performance.

Consumer confidence

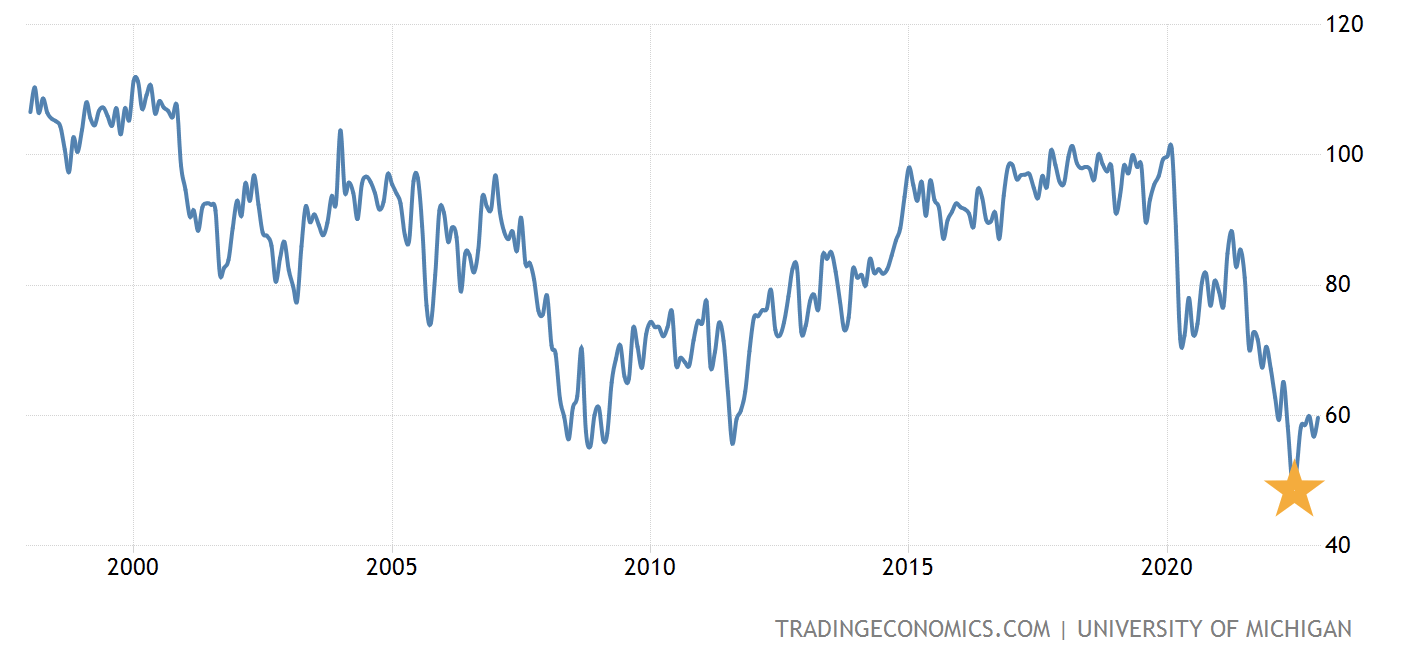

At the time of our last writing, consumer confidence has hit its lowest reading during the past 25 years. Since then, the sentiment has somewhat improved, but the readings continue to remain at extreme low levels.

U.S. Consumer confidence (tradingeconomics.com)

Low consumer confidence tend to lead to reduced spending on durable and discretionary items, just like the ones that Hasbro sells.

This reduced spending has already been observed during the holiday season. Hasbro’s holiday sales have been one of the weakest ever. BMO Capital Markets analyst Gerrick Johnson has pointed out that the lower than expected sales may lead to an increase in inventory levels, which may eventually result in the need for substantial discounting. Additionally, EPS and revenue expectations for both Q4 of 2022 and the full year for both 2022 and 2023have been revised downwards.

In our opinion, the likelihood of seeing a substantial positive earnings surprise is not particularly high this time. From this perspective, we do not recommend starting a new position before the earnings release.

What we would like to see to be more optimistic?

We would like to see a meaningful improvement in the consumer confidence before we would get bullish on the company. As consumer confidence is often treated as a leading economic indicator, its increase could potentially forecast increasing spending by the consumers, which could positively impact Hasbro’s financial performance as well.

Dividends

In December 2022, Hasbro has declared a quarterly dividend of $0.7 per share, in-line with the previous. This corresponds to a forward yield of 4.65%.

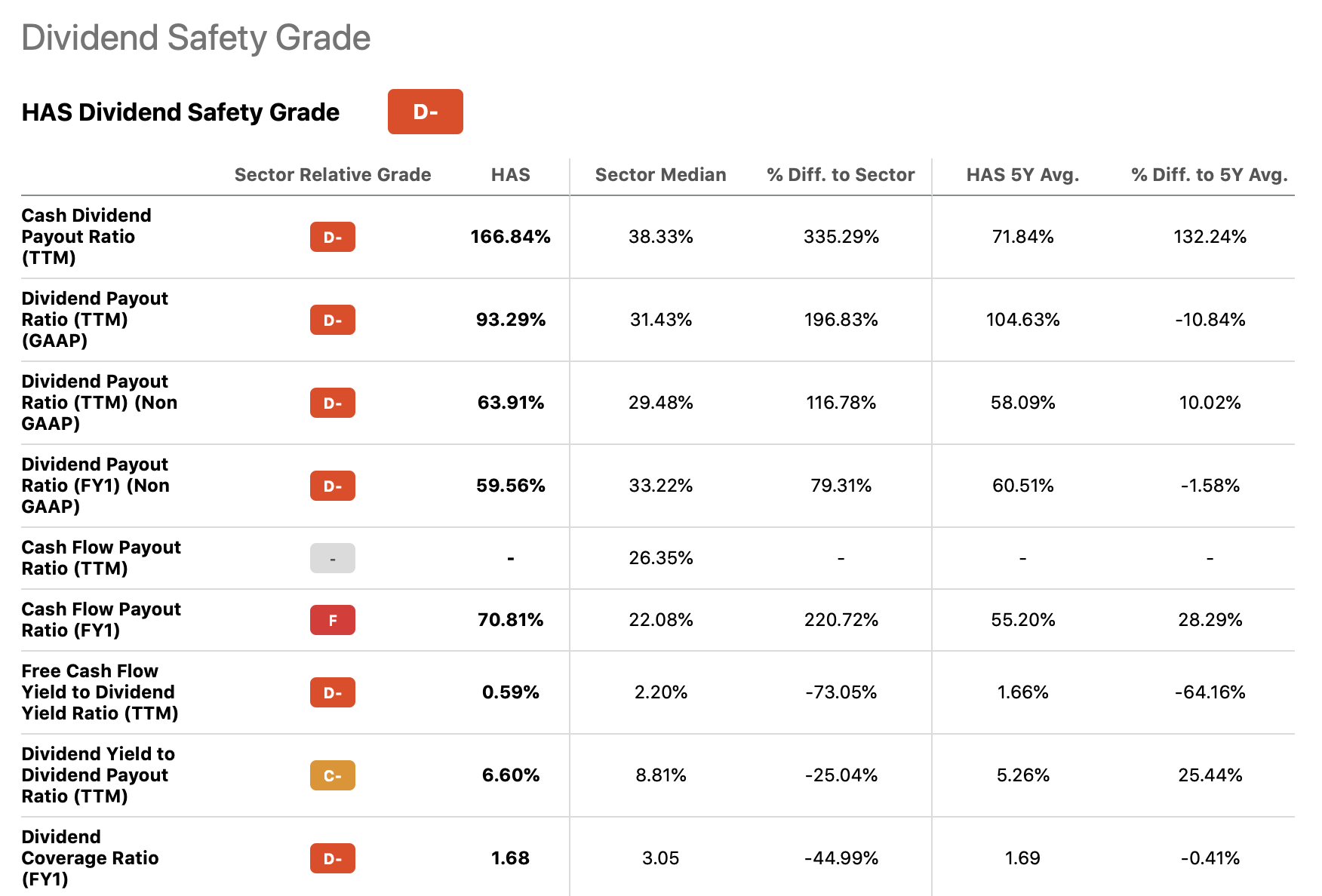

In our previous writing, we have argued that the relatively high yield may be appealing for dividend investors, but we have pointed out that the payout ratios appear unsustainably high, while the coverage ratios appear unsustainably low.

Dividend safety (Seeking Alpha)

Since then, most of the metrics have further deteriorated. As neither earnings nor revenues are expected to improve meaningfully in the coming quarters, investors have to keep in mind that Hasbro may not be able to keep paying the current dividend for much longer.

Input and freight costs

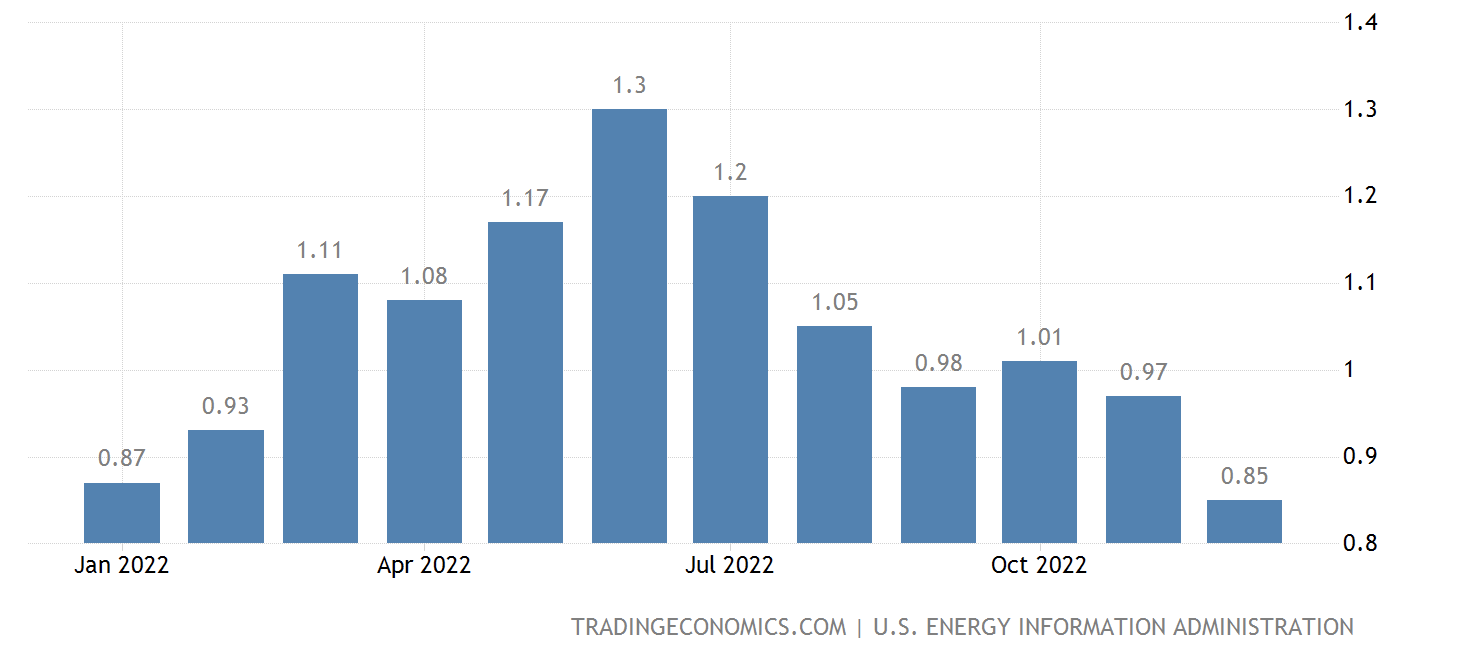

Input and freight costs have been one of the main reason in the beginning of 2022, why Hasbro has been struggling with increasing their earnings. In our opinion, input costs may have already started moderating in the past months and are likely to stay at the current level or decrease even further in 2023.

The reasons for our hypothesis is the recent trend in the gasoline prices in the United States. Since June, prices have fallen by more than 30%. This development can have a positive impact on the company’s margins in the coming quarters.

Gasoline price USD/L (tradingeconomics.com)

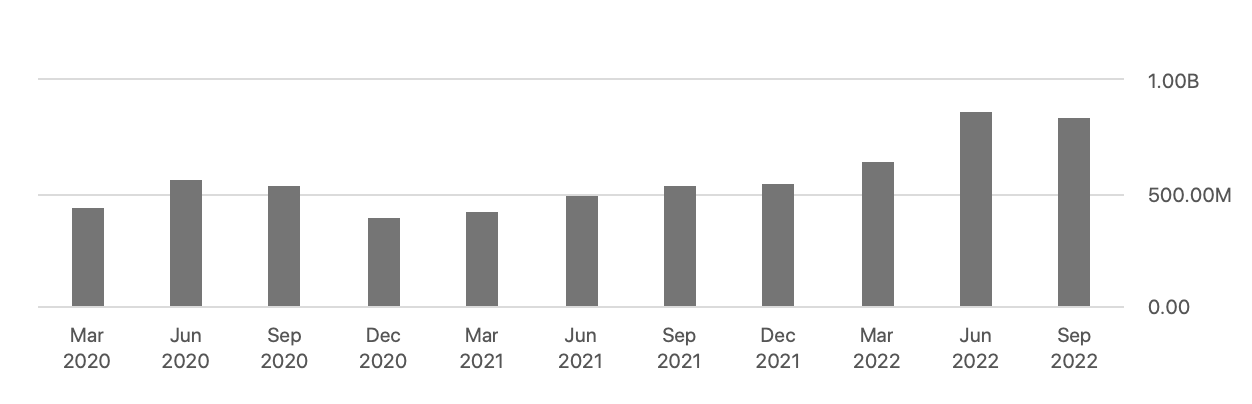

Inventory

Hasbro’s inventory has been consistently growing in the past quarters.

Inventory (Seeking Alpha)

Considering that holiday sales have been also disappointing, we are expecting that inventory levels are still substantially higher than normally. While the reduced input costs may positively impact Hasbro’s margins, inventory related problems, leading to significant discounting, may offset these potential benefits. The high inventory levels also negative impact the company’s liquidity position and its financial flexibility, which is reflected primarily by the declining quick ratio.

To remember

Due to the challenging macroeconomic environment, we do not expect a substantial increase in the demand for Hasbro’s products in the near future. The recent news about the weakness during the holiday season is also a warning sign.

The 4%+ quarterly dividend payments may not be sustainable in the long term, if the firm’s financial performance does not improve materially.

The development of gasoline price over the past quarters may have a positive impact on the firm’s margins, but the increasing inventory levels and the potential need for discounting could offset the positive impact.

As the valuation of Hasbro’s stock has not substantially improved since our last writing, we believe that it is not worth buying or owning Hasbro’s stock before the earnings release. In order to be more bullish, we would like to see improving consumer confidence, improving inventory levels and a more sustainable dividend.

Be the first to comment