Arand

Thesis

Innoviz (NASDAQ:INVZ) is a LiDAR company focused on the automotive market, with a recent emphasis on serving as a Tier 1 to provide a LiDAR sensing solution to OEM customers. Despite a narrow portfolio of hardware products, the company had one of the earliest auto OEM wins with BMW and has followed it up with a large win with VW (with its second-generation LiDAR product). Innoviz is attractive in relation to both the portfolio of products as well as costs relative to most LiDAR peers, but the products are capable of supporting Level 3 highway autonomy applications. I expect rapid growth in the order book from expansion with existing OEM relationships, as well as translating a higher percentage of engagements into wins. I use 17x earnings on 2030 forecasts, to derive my Dec-30 price target of $140.5.

Why am I bullish on INVZ?

Management team boasts a strong technical background

Innoviz’s management team includes Mr. Omer Keilaf, CEO, who helped co-found Innoviz in 2016. He formerly worked in senior managerial positions at STMicroelectronics, Consumer Physics, and the IDF. Mr. Eldar Cegla, CFO, has spent 20 years serving in financial and operational roles at various Israeli tech companies. Prior to Innoviz, he held management roles at Consumer Physics, Metrolight, Mantis-Vision, and Browzwear International. Mr. Oren Buskila, Chief R&D Officer, has over 11 years of experience managing R&D projects. He designed the HW system at Consumer Physics and earned the Head of Military Intelligence Directorate Award from his time at the IDF.

Innoviz’s Top Management (Company Presentation)

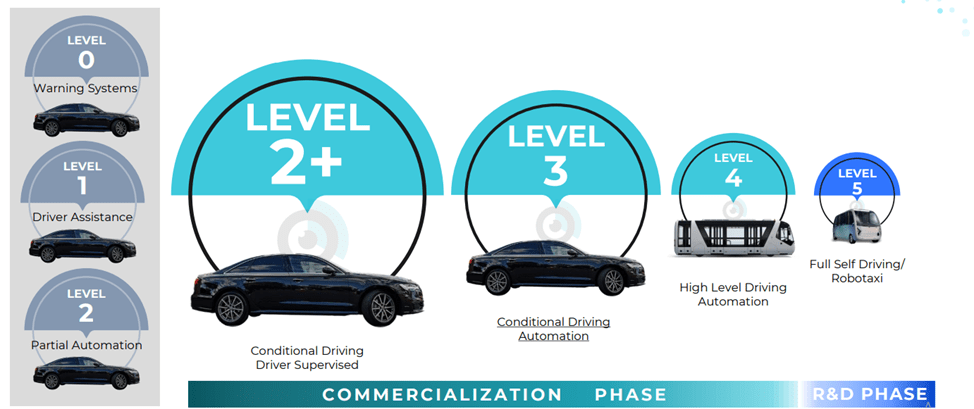

Largest TAM for Innoviz belongs to L2+ and L3 consumer auto applications

Autos present the largest TAM for LiDAR, projected to exceed $100 billion in 2030. Innoviz was the first company to land an L3 LiDAR design win with BMW; it later developed Innoviz Two to bridge the gap to the AVs. Together, this L2+ and L3 consumer automotive opportunity is the largest addressable market for Innoviz, at least till the end of this decade, with L2+ and L3 consumer auto opportunity together representing 55% ($38 billion) of the expected TAM in 2030E. Robotaxis & Shuttles is expected to be an addressable market of $11 billion by 2030E, and Trucking is expected to be $6 billion.

Solid product line-up covering a wide range of technical specification

Innoviz’s current and forward-looking product line comprises InnovizOne, InnovizTwo, Innoviz360 and the Perception Software. InnovizOne is a solid state MEMS based LiDAR sensor designed specifically for L3-L5 automotive applications, containing four lasers and detectors. InnovizOne is the sensor that will be used in the BMW cars. Aside from automotive applications, InnovizOne has use cases in trucking, delivery, drones, and industry. InnovizTwo is designed specifically to accelerate adoption of LiDAR by offering L2+ ADAS functionality with hardware that can later support L3 and L4 as well. In addition to offering a bridge between L2 and L3 functionality, InnovizTwo has a 70% cost reduction and 30x performance improvement relative to InnovizOne. The latest revealed product, Innoviz360 is a 360° LiDAR to enable a higher degree of perception for L4 and L5 applications in automotive as well as applications in nonautomotive industries including heavy machinery, smart cities, logistics and construction. In addition to the sensor hardware, Innoviz also offers perception software, which leverages its proprietary AI algorithms to enable object detection, classification and tracking features as well as collision classification, localization and calibration capabilities.

L2+ to L3 Autonomy Megatrend is Emerging (Company Presentation)

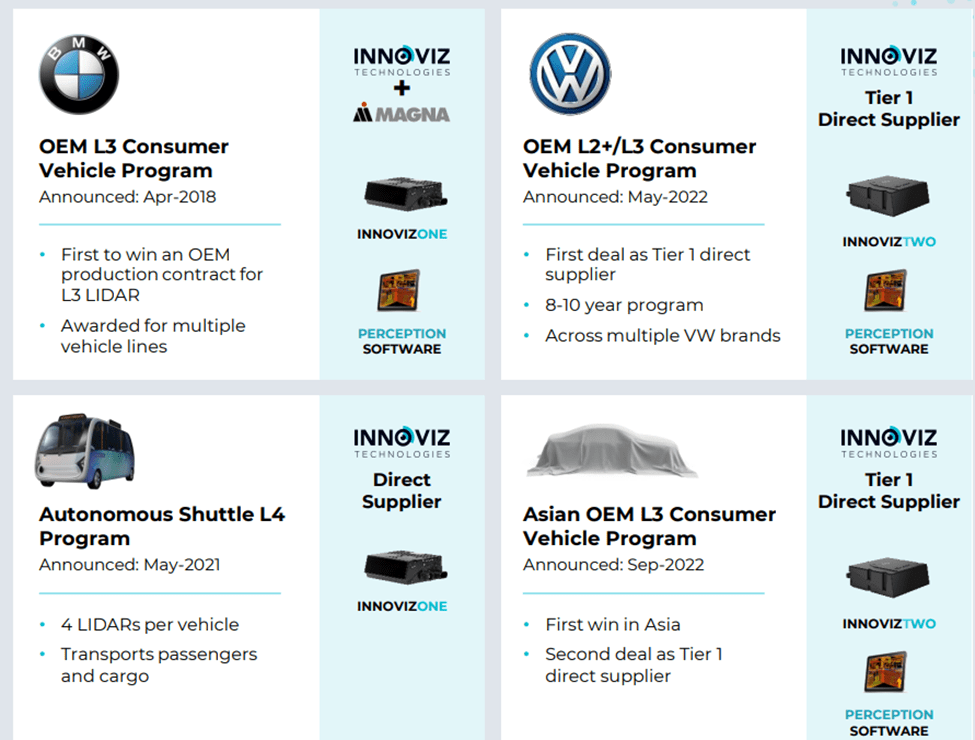

Key partners from automotive include OEMs and Tier 1s

For any new technology, commercial success/ customer adoption is the ultimate validation. Innoviz has secured 4 key deal wins in the automotive space, including BMW, European L4 Shuttle program and the latest ones with Volkswagen, which is the second-largest automotive OEM by production volumes after Toyota, and with a non-traditional Asian OEM. BMW is expected to implement InnovizOne in its Series 5 and Series 7 automobiles. Innoviz has a wide breadth of partners across industries, but they are especially concentrated in the automotive market. In the automotive market, which has the largest TAM relative to other industries, Innoviz has partnered with significant Tier 1s, including Harman, HiRain, Magna (Tier 1 on BMW series production), and Aptiv.

Innoviz Has Secured 4 Production Wins with Leading OEMs (Company Presentation)

Financial Outlook

Wins with BMW and VW set up the company for $3.5 billion of revenue in 2030

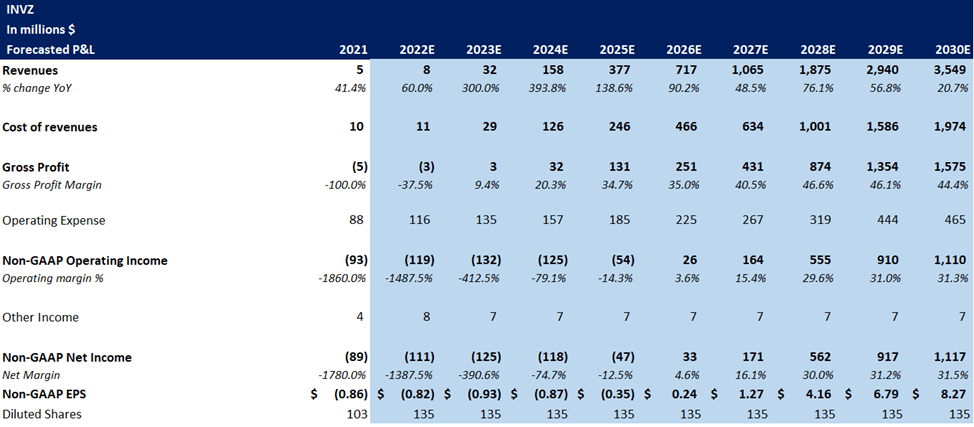

As shown below, I have forecasted 2030 revenues of ~$3.5 billion in 2030, led by the wins on series production vehicles with BW and VW. Not only do I see an opportunity for Innoviz to drive further wins with new automakers treating the recent wins as validation of the technology solution, but I also see a more realistic opportunity to expand the pipeline of wins with Volkswagen, including with more brands and more vehicle models.

Innoviz’s major wins to date are BMW, VW, and a shuttle program. The volume implications of the shuttle win and the BMW win, which are together ramping in the first half of the decade, is more modest and implies a revenue run-rate of around ~$400 million. However, the volume implications of the VW win are large, with the automaker accounting for almost 10% of global light vehicle production. The timing of the win with VW implies a ramp in series production in the later part of the decade, implying that the revenue ramp for the company is more likely to accelerate to ramp in the second half of the decade.

Project gross margins to ramp steadily to industry-leading levels

Led by the 30%-40% gross margins forecasted by Innoviz on the VW win, I forecast gross margins to ramp steadily. However, the scale of the win, particularly with Volkswagen, ensures that the commonality of components and design will be a tailwind for the company and drive robust long-term margins of around ~45%.

Valuation

I expect Innoviz to be one of the industry leaders in LiDAR. However, it is important to realize the company is still in nascent stages and therefore I don’t have a near-term price target on the stock. I have modeled the company’s P&L through 2030 and have embedded modest discounts to valuation multiples for diversified Industrial Technology companies to account for the concentrated exposure to Auto customers. I use 17x earnings on 2030 forecasts to derive my Dec-30 price target of $140.5.

Innoviz forecasted P&L (my estimates)

Risks

Industry-Specific Downside Risks

Challenges in driving penetration of l3 autonomous driving systems based on LiDARs

I expect most OEMs to initially sell LiDAR equipped vehicles, i.e., L3 autonomous functionality, as an additional option available for purchase to consumers relative to standard. Lower-than-expected ramp in adoption of L3 equipped vehicles could result in more moderate revenue for LiDAR companies than anticipated.

Company-Specific Downside Risks

Lack of broad portfolio could limit industrial opportunities

Innoviz’s portfolio of Innoviz One, Innoviz Two and Innoviz 360 is adequate for automotive applications designs at this time. However, companies with greater focus on industrial applications, separate from the automotive markets, tend to have a broader portfolio with different specifications for varied use cases, which could limit Innoviz’s opportunities.

Final Thoughts

I keep a Buy rating on Innoviz, as the company is following up the early wins in automotive (BMW), a shuttle program with big volume wins (with VW), and a non-traditional auto OEM (Asia OEM and EV), and currently boasts a large order book. I anticipate that the combination of several wins, big volumes, a balance of LiDAR prices and performance, and the ability to enable highway autonomy at high speeds will position Innoviz to increase revenues well into the end of the decade, while cost discipline will drive profitability. I have a December 2030 price target of $140.5 on the stock, derived from 17x P/E of 2030 forecasted earnings.

Be the first to comment